CHAPTER 16: MANAGING BOND PORTFOLIOS

CHAPTER 16: MANAGING BOND PORTFOLIOS

PROBLEM SETS

1. While it is true that short-term rates are more volatile than long-term rates, the

2. Duration can be thought of as a weighted average of the maturities of the cash

flows paid to holders of the perpetuity, where the weight for each cash flow is

3. The percentage change in the bond’s price is:

7.194 0.005 0.0327 3.27%,

1 1.10

Dy

y

– ´ D =- ´ =- =-

+

or a 3.27% decline

4. a. YTM = 6%

(1) (2) (3) (4) (5)

Time until

Payment

(Years) Cash Flow

PV of CF

(Discount

Rate = 6%) Weight

Column (1)

Column (4)

1 $ 60.00 $ 56.60 0.0566 0.0566

16-1

CHAPTER 16: MANAGING BOND PORTFOLIOS

b. YTM = 10%

(1) (2) (3) (4) (5)

Time until

Payment

(Years) Cash Flow

PV of CF

(Discount

Rate = 10%) Weight

Column (1)

Column (4)

1 $ 60.00 $ 54.55 0.0606 0.0606

5. For a semiannual 6% coupon bond selling at par, we use the following parameters:

coupon = 3% per half-year period, y = 3%, T = 6 semiannual periods.

(1) (2) (3) (4) (5)

Time until

Payment

(Years) Cash Flow

PV of CF

(Discount

Rate = 3%) Weight

Column (1)

Column (4)

1 $ 3.00 $ 2.913 0.02913 0.02913

2 3.00 2.828 0.02828 0.05656

If the bond’s yield is 10%, use a semiannual yield of 5% and semiannual coupon

of 3%:

(1) (2) (3) (4) (5)

Time until

Payment

(Years) Cash Flow

PV of CF

(Discount

Rate = 5%) Weight

Column (1)

Column (4)

1 $ 3.00 $ 2.857 0.03180 0.03180

2 3.00 2.721 0.03029 0.06057

16-2

CHAPTER 16: MANAGING BOND PORTFOLIOS

6. If the current yield spread between AAA bonds and Treasury bonds is too wide

compared to historical yield spreads and is expected to narrow, you should shift

7. D. Investors tend to purchase longer term bonds when they expect yields to fall

8. a. Bond B has a higher yield to maturity than bond A since its coupon

b. Bond A has a lower yield and a lower coupon, both of which cause Bond A

9. a.

(1) (2) (3) (4) (5)

Time until

Payment

(Years) Cash Flow

PV of CF

(Discount Rate =

10%) Weight

Column (1)

Column (4)

1 $10 million $ 9.09 million 0.7857 0.7857

10 In each case, choose the longer-duration bond in order to benefit from a

rate decrease.

a. ii. The Aaa-rated bond has the lower yield to maturity and therefore the

longer duration.

16-3

CHAPTER 16: MANAGING BOND PORTFOLIOS

11. a., b., c. The table below shows the holding period returns for the three bonds:

Maturity

1 Year

2 Years

3 Years

YTM at beginning of year 7.00% 8.00% 9.00%

a. Beginning of year prices

$1,009.35

$1,000.

$974.69

b. Prices at year-end (at 9% YTM)

$1,000.00

$990.83

$982.41

Capital gain

–$9.35

–$9.17

$7.72

Coupon

$80.00

$80.00

$80.00

1-year total $ return

$70.65

$70.83

$87.72

c. 1-year total rate of return

7.00%

7.08%

9.00%

Buy the three-year bond because it provides a 9% holding-period return over the

next year, which is greater than the return on either of the other bonds.

12. a. PV of the obligation = $10,000 Annuity factor (8%, 2) = $17,832.65

(1) (2) (3) (4) (5)

Time until

Payment

(Years) Cash Flow

PV of CF

(Discount

Rate = 8%) Weight

Column (1)

Column (4)

1 $10,000.00 $ 9,259.259 0.51923 0.51923

b. A zero-coupon bond maturing in 1.4808 years would immunize the

obligation. Since the present value of the zero-coupon bond must be

c. If the interest rate increases to 9%, the zero-coupon bond would decrease

in value to

92.590,17$

09.1

26.985,19$

4808.1

The present value of the tuition obligation would decrease to $17,591.11

The net position decreases in value by $0.19

d. If the interest rate decreases to 7%, the zero-coupon bond would increase

in value to

99.079,18$

07.1

26.985,19$

4808.1

The present value of the tuition obligation would increase to $18,080.18

The net position decreases in value by $0.19

16-4

CHAPTER 16: MANAGING BOND PORTFOLIOS

The reason the net position changes at all is that, as the interest rate

changes, so does the duration of the stream of tuition payments.

13. a. PV of obligation = $2 million/0.16 = $12.5 million

Call w the weight on the five-year maturity bond (which has duration of four

years). Then

b. The price of the 20-year bond is

Therefore, the bond sells for 0.4071 times its par value, and

Another way to see this is to note that each bond with par value $1,000

Call w the weight of the zero-coupon bond. Then

Therefore, the portfolio weights would be as follows: 11/16 invested in the

zero and 5/16 in the perpetuity.

b. Next year, the zero-coupon bond will have a duration of 4 years and the

perpetuity will still have a 21-year duration. To obtain the target duration

16-5

CHAPTER 16: MANAGING BOND PORTFOLIOS

15. a. The duration of the annuity if it were to start in one year would be

(1) (2) (3) (4) (5)

Time until

Payment

(Years) Cash Flow

PV of CF

(Discount

Rate = 10%) Weight

Column (1) ×

Column (4)

1 $10,000 $ 9,090.909 0.14795 0.14795

2 10,000 8,264.463 0.13450 0.26900

3 10,000 7,513.148 0.12227 0.36682

Because the payment stream starts in five years, instead of one year, we

b. The present value of the deferred annuity is

968,41$

10.1

)10%,10(factor Annuity 000,10

4

Alternatively, CF 0 = 0; CF 1 = 0; N = 4; CF 2 = $10,000; N = 10; I = 10;

Solve for NPV = $41,968.

Call w the weight of the portfolio invested in the five-year zero. Then

The investment in the five-year zero is equal to

The investment in the 20-year zeros is equal to

These are the present or market values of each investment. The face

values are equal to the respective future values of the investments. The

face value of the five-year zeros is

Therefore, between 50 and 51 zero-coupon bonds, each of par value $1,000,

would be purchased. Similarly, the face value of the 20-year zeros is

16-6

CHAPTER 16: MANAGING BOND PORTFOLIOS

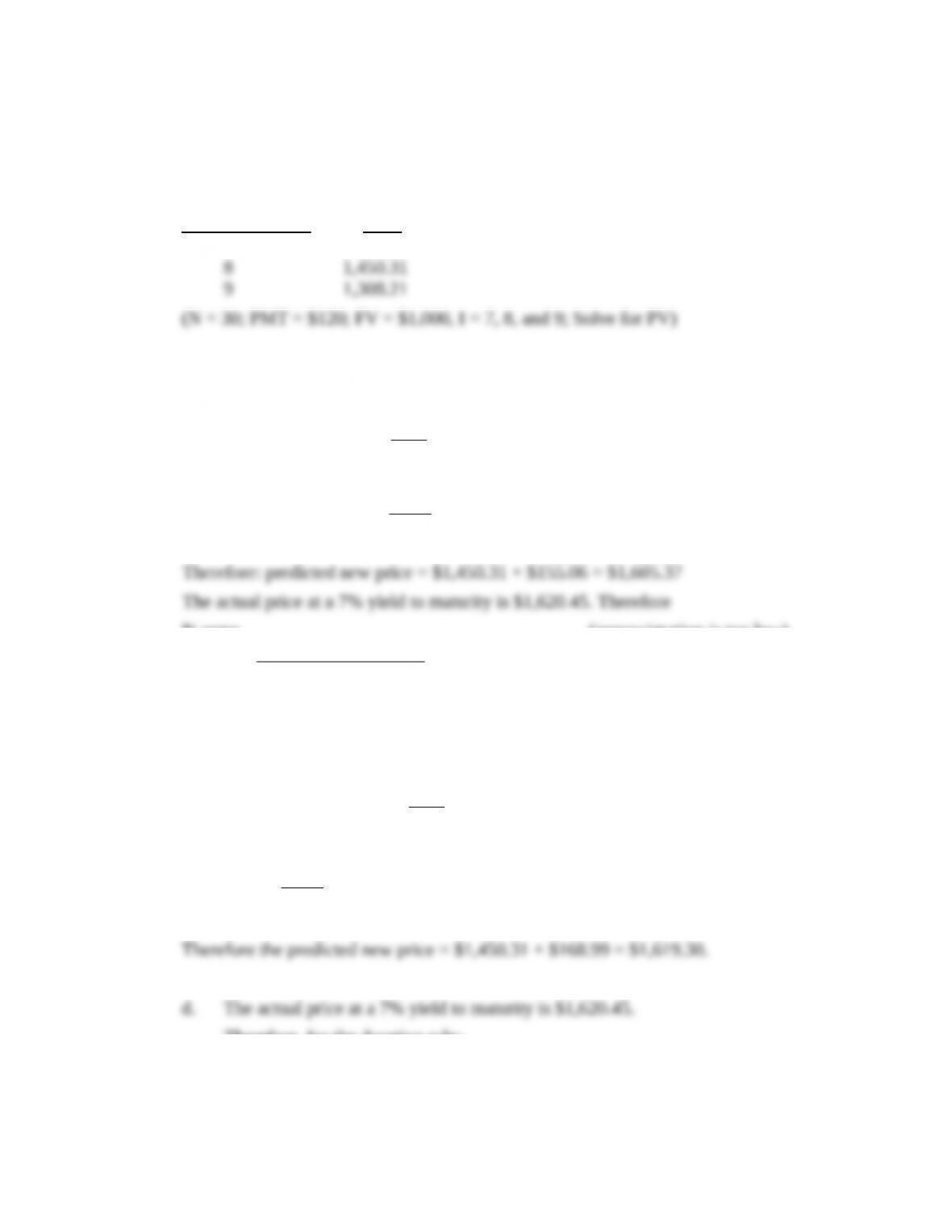

16. a. Using a financial calculator, we find that the actual price of the bond as a

function of yield to maturity is

Yield to Maturity Price

7% $1,620.45

b. Using the duration rule, assuming yield to maturity falls to 7%

Predicted price change

0

1

Dy P

y

æ ö

= – ´ D ´

ç ÷

+

è ø

11.54 ( 0.01) $1, 450.31 $155.06

1.08

æ æ

– –

æ æ

æ æ

Therefore: predicted new price = $1,450.31 + $155.06 = $1,605.37

The actual price at a 7% yield to maturity is $1,620.45. Therefore

% error

$1, 605.37 $1, 620.45 0.0093 0.93%

$1, 620.45

–

= =- =-

(approximation is too low)

c. Using duration-with-convexity rule, assuming yield to maturity falls

to 7%

Predicted price change

2

0

0.5 Convexity ( )

1

Dy y P

y

æ æ

æ æ

æ æ

æ æ

æ æ

– D + D

æ æ

æ æ

æ æ æ æ

+

æ æ

æ æ

æ æ

æ æ

2

11.54 ( 0.01) 0.5 192.4 ( 0.01) $1, 450.31 $168.99

1.08

ì ü

é ù

æ ö é ù

= – ´ – + ´ ´ – ´ =

í ý

ç ÷

ê ú ë û

è ø

ë û

î þ

Therefore the predicted new price = $1,450.31 + $168.99 = $1,619.30.

d. The actual price at a 7% yield to maturity is $1,620.45.

Therefore, for the duration rule:

16-7

CHAPTER 16: MANAGING BOND PORTFOLIOS

% error

$1, 605.37 $1, 620.45 0.0093 0.93%

$1, 620.45

–

= =- =-

(approximation is too low)

And the Duration-Convexity Rule:

% error

$1, 619.30 $1,620.45 0.0007,or 0.07%

$1, 620.45

–

= =- –

(approximation is too low).

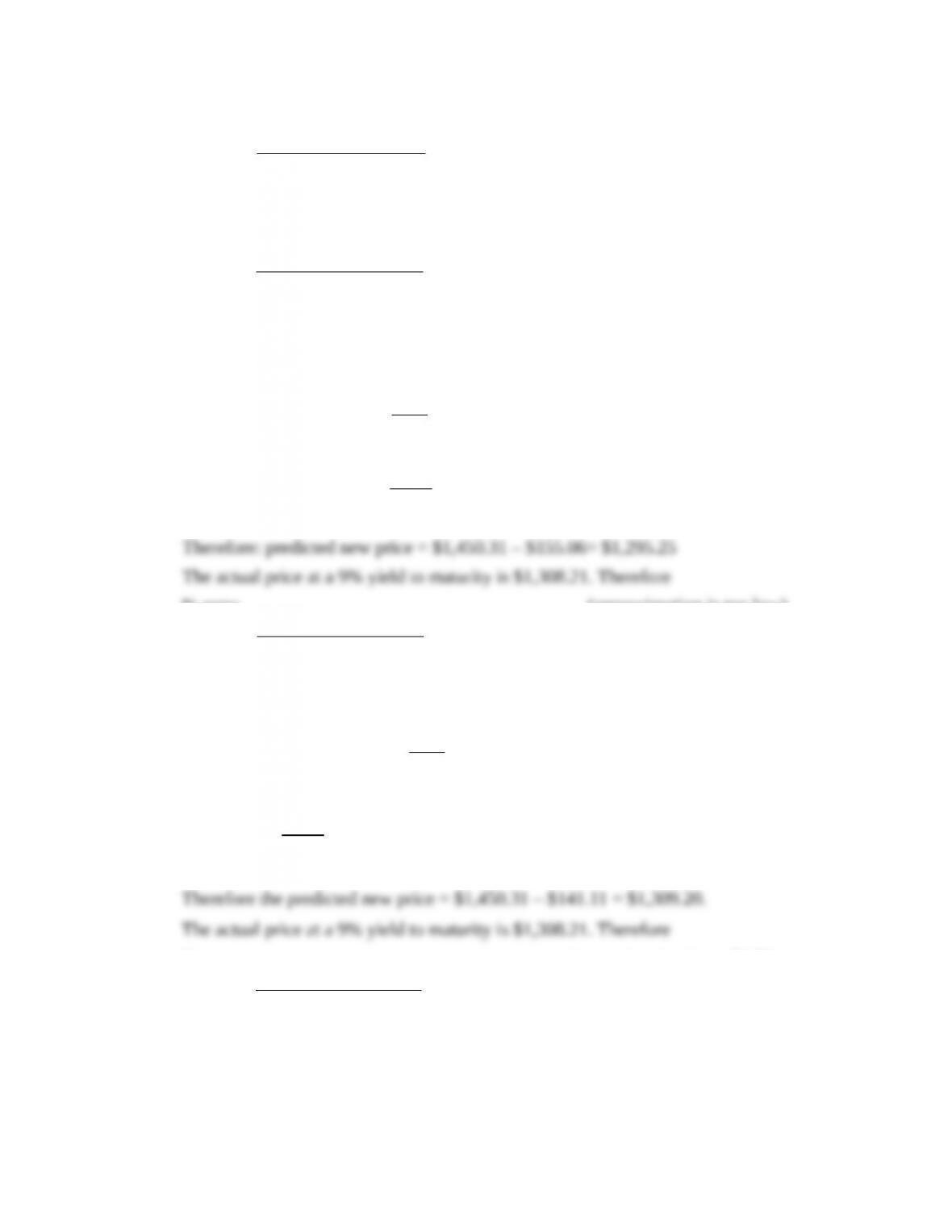

e. Using the duration rule, assuming yield to maturity increases to 9%

Predicted price change

0

1

Dy P

y

æ ö

= – ´ D ´

ç ÷

+

è ø

11.54 0.01 $1, 450.31 $155.06

1.08

æ æ

– -

æ æ

æ æ

Therefore: predicted new price = $1,450.31 – $155.06= $1,295.25

The actual price at a 9% yield to maturity is $1,308.21. Therefore

% error

$1, 295.25 $1,308.21 0.0099 0.99%

$1,308.21

–

= =- =-

(approximation is too low)

Using duration-with-convexity rule, assuming yield to maturity rises to 9%

Predicted price change

2

0

0.5 Convexity ( )

1

Dy y P

y

æ æ

æ æ

æ æ

æ æ

æ æ

– D + D

æ æ

æ æ

æ æ æ æ

+

æ æ

æ æ

æ æ

æ æ

2

11.54 0.01 0.5 192.4 (0.01) $1, 450.31 $141.11

1.08

ì ü

é ù

æ ö é ù

= – ´ + ´ ´ ´ =-

í ý

ç ÷

ê ú ë û

è ø

ë û

î þ

Therefore the predicted new price = $1,450.31 – $141.11 = $1,309.20.

The actual price at a 9% yield to maturity is $1,308.21. Therefore

% error

$1,309.20 $1,308.21 0.0008,or 0.08%

$1,308.21

–

= =

(approximation is too high).

Conclusion: The duration-with-convexity rule provides more accurate

approximations to the true change in price. In this example, the percentage error

16-8

CHAPTER 16: MANAGING BOND PORTFOLIOS

17. Shortening his portfolio duration makes the value of the portfolio less sensitive

18. Predicted price change:

¿

(

−D

1+y

)

× ∆ y × P0=

(

−$3.5851

1.05

)

×.01 ×100=−$3.41(decrease )

19. Using Spreadsheet 16.2:

Settlement date 5/27/2020

Maturity date 11/15/2031

20. a. The maturity of the 30-year bond will fall to 25 years, and its yield is forecast

to be 8%. Therefore, the price forecast for the bond is $893.25

b. The maturity of the 20-year bond will fall to 15 years, and its yield is forecast to

be 7.5%. Therefore, the price forecast for the bond is $911.73.

16-9

CHAPTER 16: MANAGING BOND PORTFOLIOS

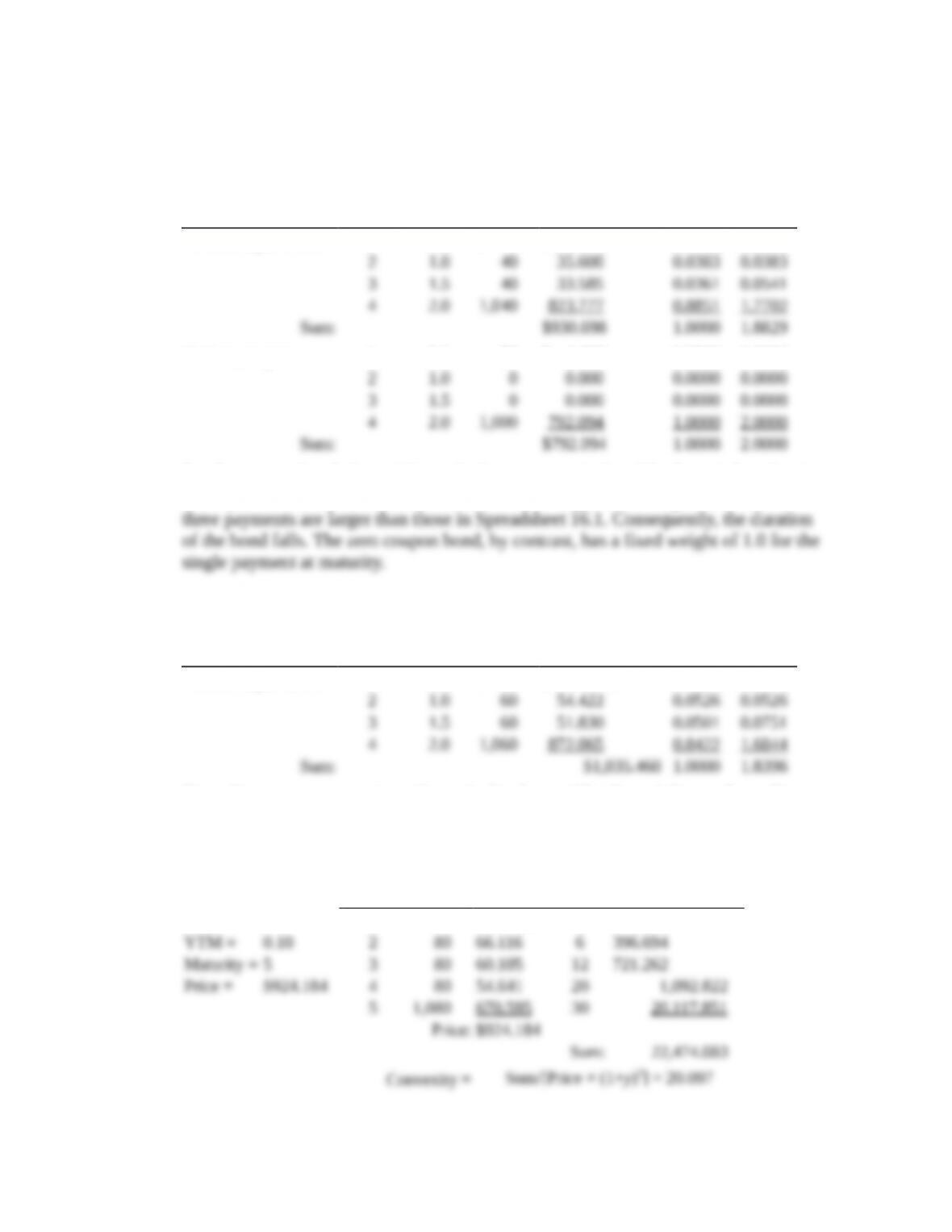

21.

a.

Period

Time

until

Payment

(Years)

Cash

Flow

PV of CF

Discount Rate =

6% per Period Weight

Years ×

Weight

A. 8% coupon bond 1 0.5 $ 40 $ 37.736 0.0405 0.0203

B. Zero-coupon 1 0.5 $0 $ 0.000 0.0000 0.0000

For the coupon bond, the weight on the last payment in the table above is less than it

is in Spreadsheet 16.1 because the discount rate is higher; the weights for the first

b.

Period

Time

until

Payment

(Years)

Cash

Flow

PV of CF

Discount Rate =

5% per Period Weight

Years ×

Weight

A. 8% coupon bond 1 0.5 $ 60 $ 57.143 0.0552 0.0276

Since the coupon payments are larger in the above table, the weights on the earlier

payments are higher than in Spreadsheet 16.1, so duration decreases.

22.

a.Time

(t)

Cash

Flow

PV(CF)

t + t2(t + t2) × PV(CF)

Coupon = $80 1 $ 80 $ 72.727 2 145.455

16-10

CHAPTER 16: MANAGING BOND PORTFOLIOS

b.Time

(t)

Cash

Flow

PV(CF)

t2 + t(t2 + t) × PV(CF)

Coupon = $0 1 $ 0 $ 0.000 2 0.000

16-11