5-24. Solution:

Edsel Research Labs

Income Statement

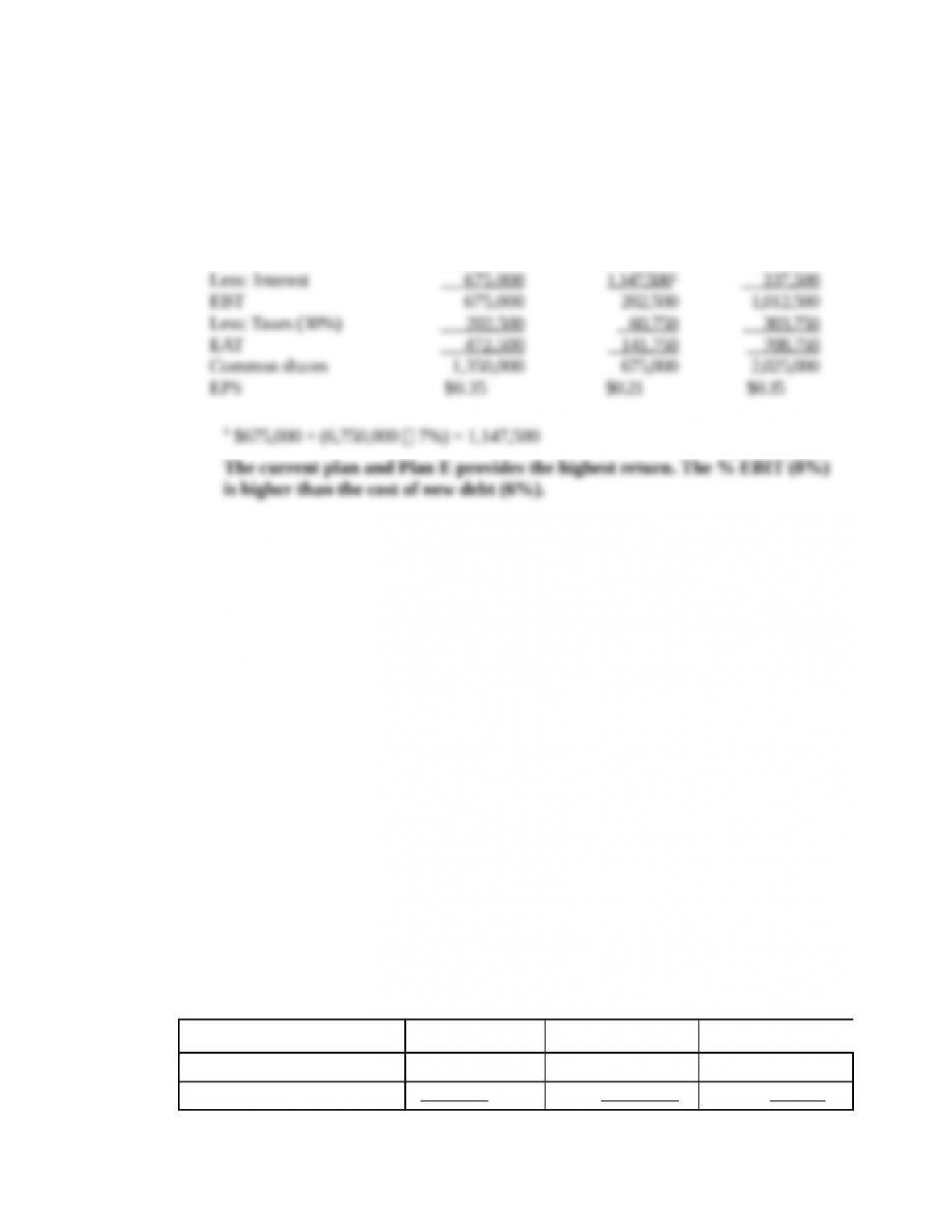

a. Return on assets = 5% EBIT = $1,350,000

Current Plan D Plan E

EBIT $1,350,000 $1,350,000 $1,350,000

1$13,500,000 debt @ 5% = $675,000

2$675,000 interest + ($6,750,000 new debt @ 11%) = $1,417,500

The current plan and Plan E provide the highest return of $0.35.

5-25. (Continued)

b. Return on assets = 8% EBIT = $2,160,000

Current Plan D Plan E

EBIT $2,160,000 $2,160,000 $2,160,000

The current plan and Plan D provides the highest return. The % EBIT

(12%) is higher than the interest rate (8% and 10%). Thus, the more debt the

firm takes on, the higher the EPS.

c. Return on assets = 5% EBIT = $1,350,000

Current Plan D Plan E

EBIT $1,350,000 $1,350,000 $1,350,000

25. Leverage and sensitivity analysis (LO6) The Lopez-Portillo Company has $10.6 million

in assets, 80 percent financed by debt, and 20 percent financed by common stock. The

interest rate on the debt is 9 percent and the par value of the stock is $10 per share.

President Lopez-Portillo is considering two financing plans for an expansion to $18 million

in assets.

Under Plan A, the debt-to-total-assets ratio will be maintained, but new debt will cost a

whopping 12 percent! Under Plan B, only new common stock at $10 per share will be

issued. The tax rate is 40 percent.

a. If EBIT is 9 percent on total assets, compute earnings per share (EPS) before the

expansion and under the two alternatives.

b. What is the degree of financial leverage under each of the three plans?

c. If stock could be sold at $20 per share due to increased expectations for the firm’s

sales and earnings, what impact would this have on earnings per share for the two

expansion alternatives? Compute earnings per share for each.

d. Explain why corporate financial officers are concerned about their stock values.

5-25. Solution:

Lopez-Portillo Company

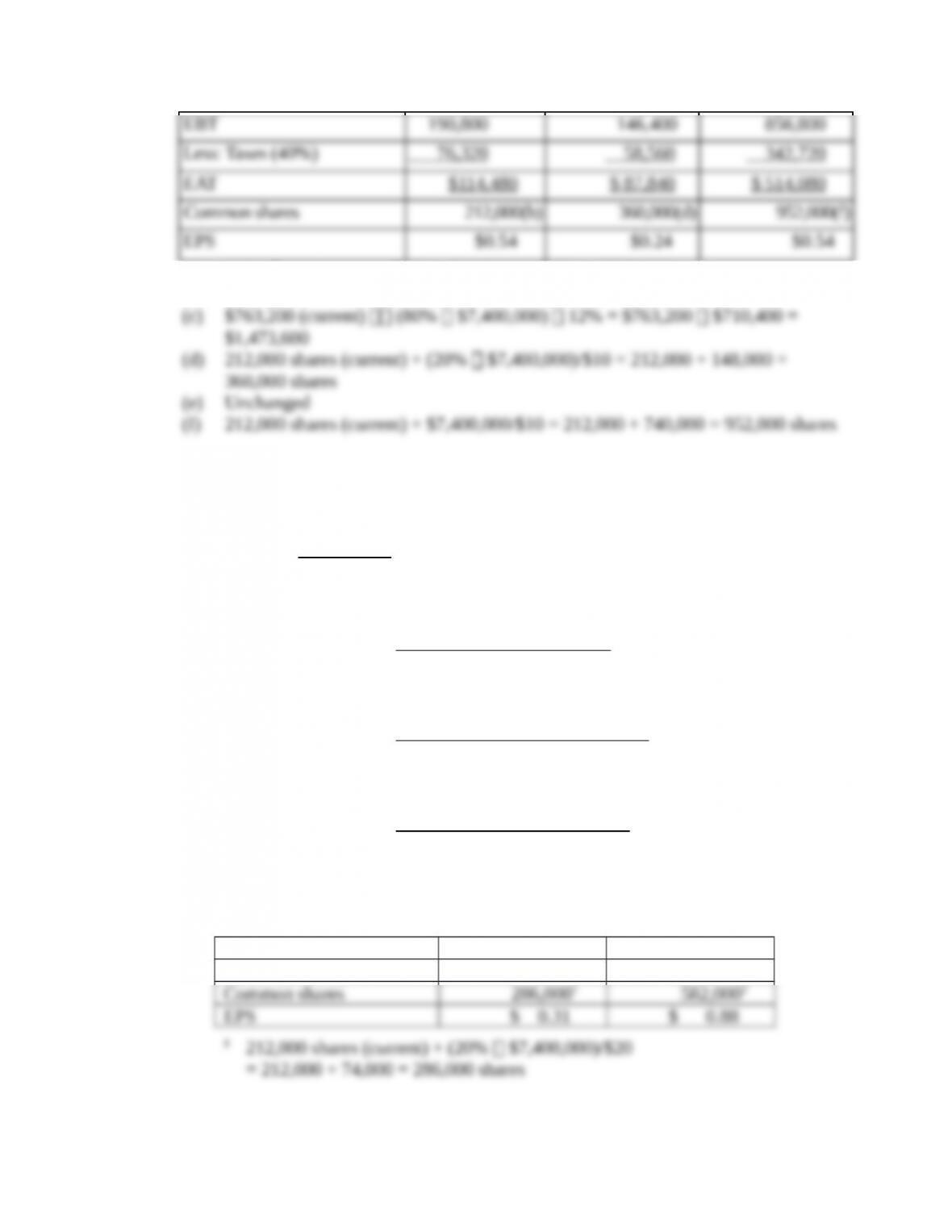

a. Return on Assets = 20%

Current Plan A Plan B

EBIT $954,000 $1,620,000 $1,620,000

Less: Interest 763,200(a) 1,473,600(c) 763,200(e)

(a) (80% $10,600,000) 9% = $8,480,000 9% = $763,200

(b) (20% $10,600,000)/$10 = $2,120,000/$10 = 212,000 shares

5-25. (Continued)

b.

EBIT

DFL EBIT I

=–

$954,000

DFL (Current) 5.00x

$954,000 $763, 200

$1,620,000

DFL (Plan A) 11.07x

$1, 620, 000 $1, 473, 600

$1,620,000

DFL (Plan B) 1.89x

$1, 620, 000 $763, 200

= =

–

= =

–

= =

–

c.

Plan A Plan B

EAT $87,840 $514,080

2212,000 shares (current) + $7,400,000/$20

d. Not only does the price of the common stock create wealth to the shareholder,

which is the major objective of the financial manager, but it greatly influences the

26. Operating leverage and ratios (LO6) Mr. Gold is in the widget business. He currently

sells 1.5 million widgets a year at $6 each. His variable cost to produce the widgets is $4

per unit, and he has $1,550,000 in fixed costs. His sales-to-assets ratio is six times, and 30

percent of his assets are financed with 10 percent debt, with the balance financed by

common stock at $10 par value per share. The tax rate is 35 percent.

His brother-in-law, Mr. Silverman, says he is doing it all wrong. By reducing his price to

$5.00 a widget, he could increase his volume of units sold by 60 percent. Fixed costs would

remain constant, and variable costs would remain $4 per unit. His sales-to-assets ratio

would be 7.5 times. Furthermore, he could increase his debt-to-assets ratio to 50 percent,

with the balance in common stock. It is assumed that the interest rate would go up by 1

percent and the price of stock would remain constant.

a. Compute earnings per share under the Gold plan.

b. Compute earnings per share under the Silverman plan.

c. Mr. Gold’s wife, the chief financial officer, does not think that fixed costs would

remain constant under the Silverman plan but that they would go up by 15 percent.

If this is the case, should Mr. Gold shift to the Silverman plan, based on earnings per

share?

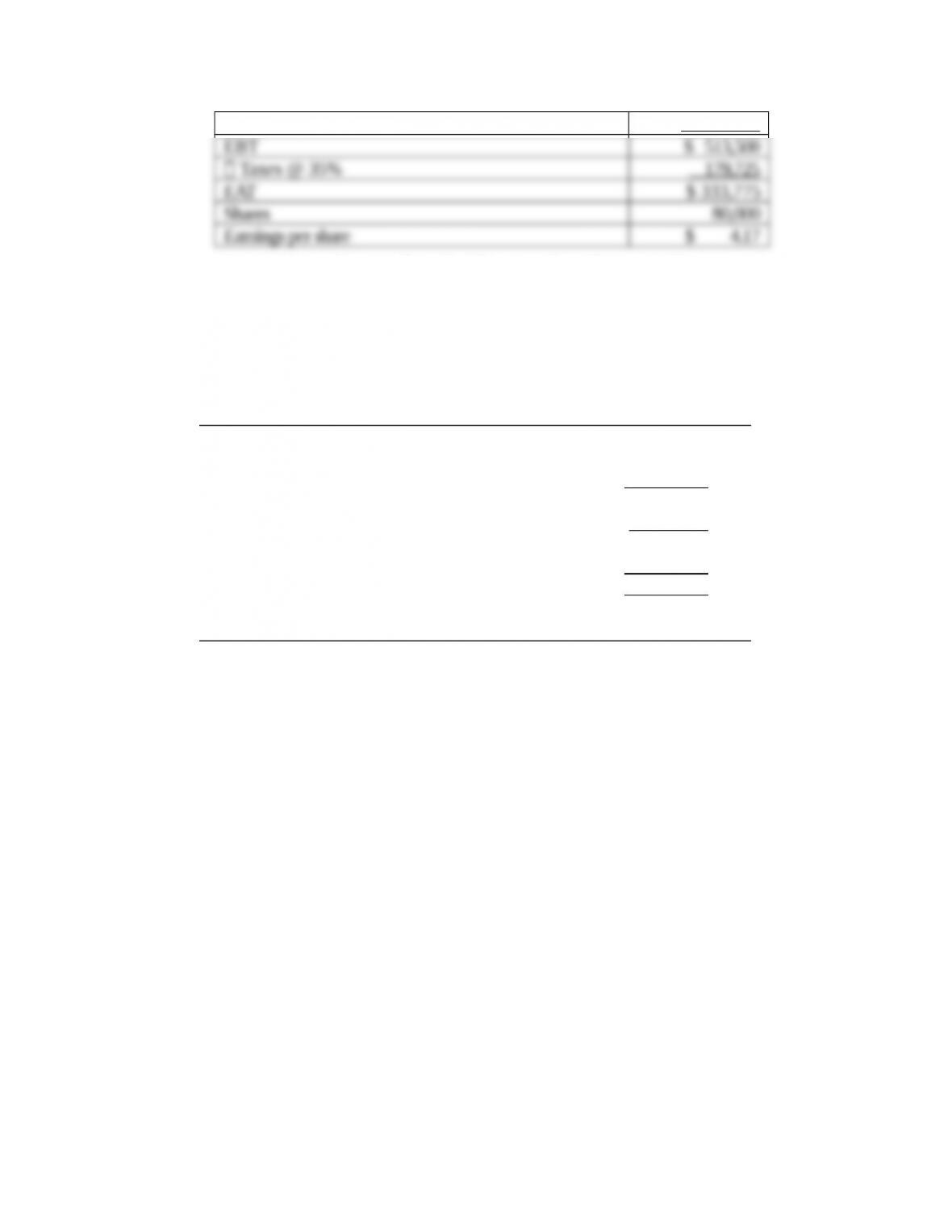

5-26. Solution:

Gold-Silverman

a. Gold Plan

Sales ($1,500,000 units $6) $9,000,000

Fixed costs 1,550,000

Variable costs 6,000,000

Operating income (EBIT) $ 1,450,000

Sales $9,000,000

Assets $1,500,000

Asset turnover 6

= = =

1Debt = 30% of Assets = 30% × $1,500,000 = $450,000

5-26. (Continued)

b. Silverman Plan

Sales ($2,400,000 units at $5.00) $12,000,000

Fixed costs 1,550,000

Variable costs (2,400,000 units $4) 9,600,000

Interest 104,000

No! Gold should not shift to the Silverman Plan if Mrs. Gold’s assumption is

correct.

27. Expansion, break-even analysis, and leverage (LO2, 3, and 4) Delsing Canning

Company is considering an expansion of its facilities. Its current income statement is as

follows:

Sales………………………………………………………… $5,500,000

Less: Variable expense (50% of sales)……….. 2,750,000

Fixed expense………………………………………. 1,850,000

Earnings before interest and taxes (EBIT)…….. 900,000

Interest (10% cost)…………………………………….. 300,000

Earnings before taxes (EBT)……………………….. 600,000

Tax (40%)…………………………………………………. 240,000

Earnings after taxes (EAT)………………………….. $ 360,000

Shares of common stock—250,000………………

Earnings per share……………………………………… $1.44

The company is currently financed with 50 percent debt and 50 percent equity (common

stock, par value of $10). In order to expand the facilities, Mr. Delsing estimates a need for

$2.5 million in additional financing. His investment banker has laid out three plans for him

to consider:

1. Sell $2.5 million of debt at 13 percent.

2. Sell $2.5 million of common stock at $20 per share.

3. Sell $1.25 million of debt at 12 percent and $1.25 million of common stock at $25 per

share.

Variable costs are expected to stay at 50 percent of sales, while fixed expenses will increase

to $2,350,000 per year. Delsing is not sure how much this expansion will add to sales, but

he estimates that sales will rise by $1.25 million per year for the next five years.

Delsing is interested in a thorough analysis of his expansion plans and methods of

financing. He would like you to analyze the following:

a. The break-even point for operating expenses before and after expansion (in sales

dollars).

b. The degree of operating leverage before and after expansion. Assume sales of $5.5

million before expansion and $6.5 million after expansion. Use the formula in

footnote 2 of the chapter.

c. The degree of financial leverage before expansion and for all three methods of

financing after expansion. Assume sales of $6.5 million for this question.

d. Compute EPS under all three methods of financing the expansion at $6.5 million in

sales (first year) and $10.5 million in sales (last year).

e. What can we learn from the answer to part d about the advisability of the three

methods of financing the expansion?

5-27. Solution:

Delsing Canning Company

a. At break-even before expansion:

PQ FC VC

where PQ equals sales volume at break-even point

= +

Sales Fixed costs Variable costs

(Variable costs 50% of sales)

Sales $1,850,000 .50 Sales

.50 Sales $1,850,000

Sales $3,700,000

= +

=

= +

=

=

At break-even after expansion:

Sales $2,350,000 .50 Sales

.50 Sales $2,350,000

Sales $4,700,000

= +

=

=

b. Degree of operating leverage, before expansion, at sales of $5,500,000

( )

( )

VC TVC

DOL = VC FC TVC FC

$5,500,000 $2,750,000

$5,500,000 $2,750,000 $1,850,000

$2,750,000 3.06x

$900,000

Q P S

Q P S

––

=

– – – –

–

=– –

= =

5-27. (Continued)

Degree of operating leverage after expansion at sales of $6,500,000

$6,500,000 $3, 250,000

DOL = $6,500, 000 $3, 250,000 $2,350,000

$3, 250, 000 3.61x

$900,000

–

– –

= =

This could also be computed for subsequent years.

c. DFL before expansion:

EBIT

DFL = EBIT 1

$900,000

$900,000 $300,000

$900,000 1.50x

$600,000

=–

= =

(100% Debt) (1)

(100% Equity)

(2)

(50% Debt and

50% Equity) (3)

Sales $6,500,000 $6,500,000 $6,500,000

– TVC (.50) 3,250,000 3,250,000 3,250,000

5-27. (Continued)

EBIT

DFL = EBIT I–

(1) (2) (3)

( ) ( ) ( )

$900,000 $900,000 $900,000

$900,000 $625,000 $900,000 $300,000 $900,000 $450,000– – –

DFL = 3.27x 1.50x 2.00x

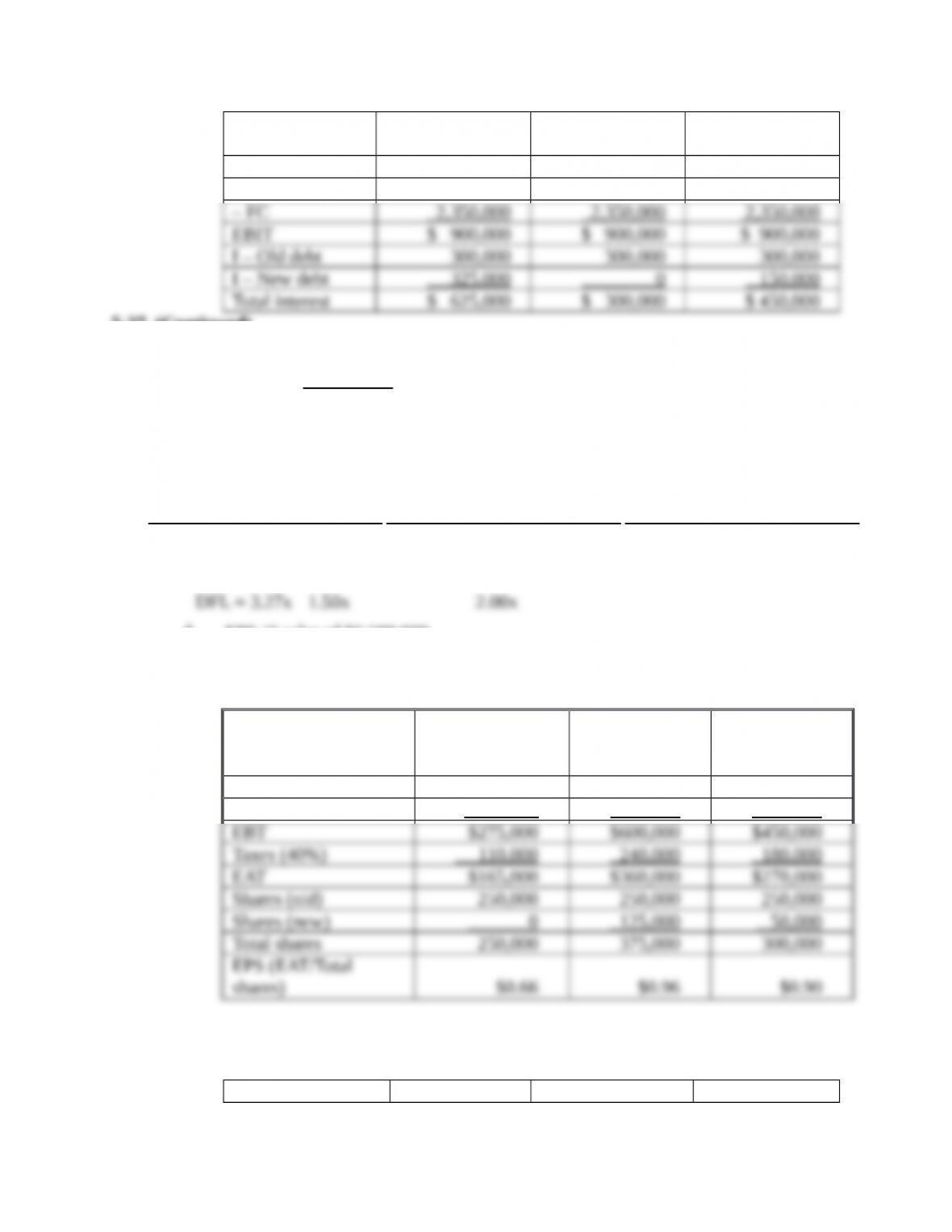

d. EPS @ sales of $6,500,000

(refer back to part c to get the values for EBIT and Total I)

(100% Debt) (1)

(100% Equity)

(2)

(50% Debt and

50% Equity)

(3)

EBIT $900,000 $900,000 $900,000

Total I 625,000 300,000 450,000

EPS @ sales of $10,500,000

(100% Debt) (100% Equity) (2) (50% Debt and

(1) 50% Equity) (3)

Sales $10,500,000 $10,500,000 $10,500,000

– TVC 5,250,000 5,250,000 5,250,000

– FC 2,350,000 2,350,000 2,350,000

e. In the first year, when sales and profits are relatively low, plan 2 (100% equity)