5-17. Solution:

Cain Supplies

Cain

EBIT $50,000

Less: Interest 9,000

18. Leverage and stockholder wealth (LO4) Sterling Optical and Royal Optical both make

glass frames and each is able to generate earnings before interest and taxes of $132,000.

The separate capital structures for Sterling and Royal are shown here:

Sterling Royal

Debt @ 12%……………… $ 660,000 Debt @ 12%…………… $ 220,000

Common stock, $5 par…… 440,000 Common stock, $5 par 880,000

Total……………………… $1,100,000 Total…………………… $1,100,000

Common shares………….. 88,000 Common shares………… 176,000

a. Compute earnings per share for both firms. Assume a 25 percent tax rate.

b. In part a, you should have gotten the same answer for both companies’ earnings per

share. Assuming a P/E ratio of 22 for each company, what would its stock price be?

c. Now as part of your analysis, assume the P/E ratio would be 16 for the riskier

company in terms of heavy debt utilization in the capital structure and 24 for the less

risky company. What would the stock prices for the two firms be under these

assumptions? (Note: Although interest rates also would likely be different based on

risk, we will hold them constant for ease of analysis.)

d. Based on the evidence in part c, should management be concerned only about the

impact of financing plans on earnings per share, or should stockholders’ wealth

maximization (stock price) be considered as well?

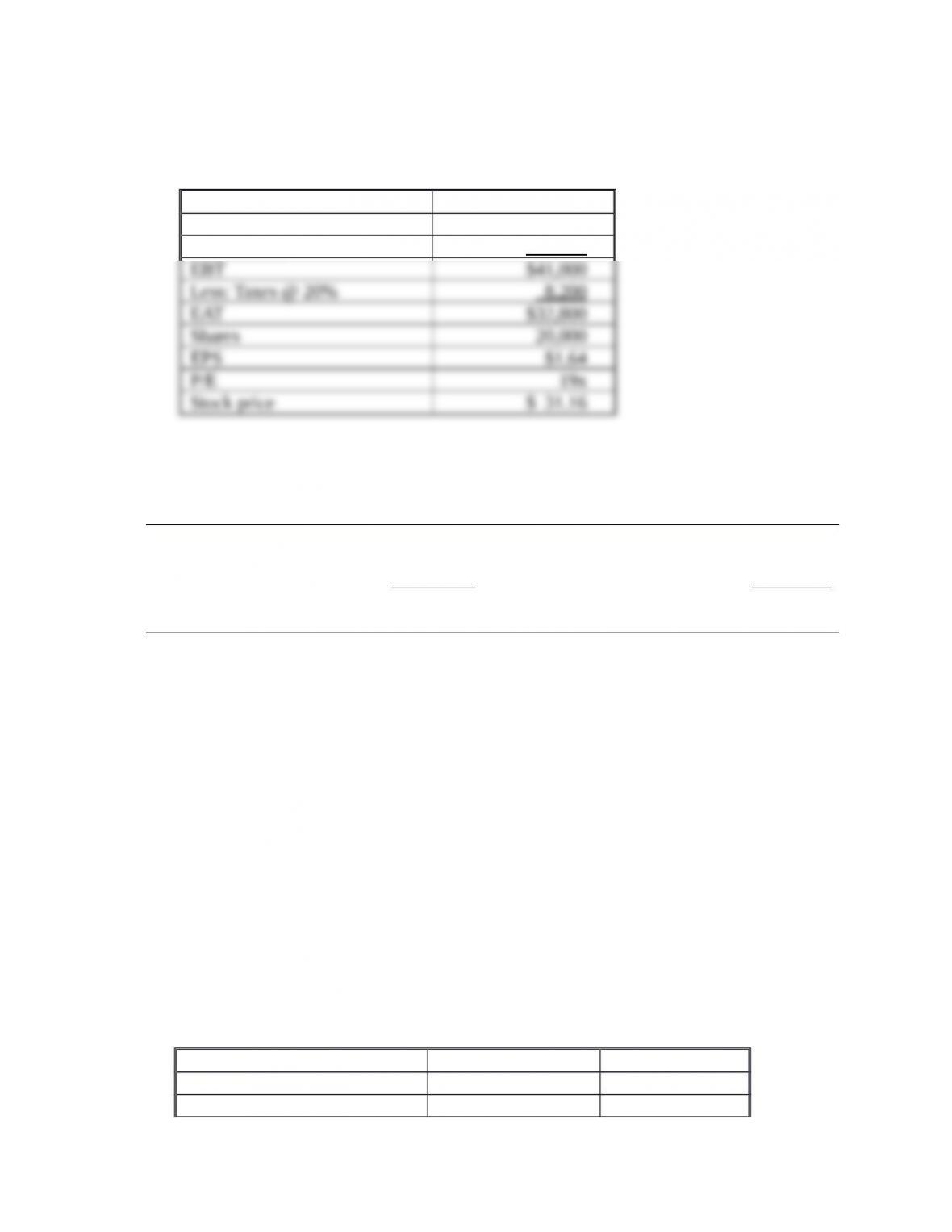

5-18. Solution:

Sterling Optical and Royal Optical

a.

Sterling Royal

EBIT $132,000 $132,000

Less: Interest 79,200 26,400

b. Stock price = P/E ×EPS

c. Sterling Royal

d. Clearly, the ultimate objective should be to maximize the stock price. While

19. Japanese firm and combined leverage (LO5) Firms in Japan often employ both high

operating and financial leverage because of the use of modern technology and close

borrower–lender relationships. Assume the Mitaka Company has a sales volume of 130,000

units at a price of $30 per unit; variable costs are $10 per unit and fixed costs are

$1,850,000. Interest expense is $405,000. What is the degree of combined leverage for this

Japanese firm?

5-19. Solution:

Mitaka Company

( VC)

DCL ( VC) FC

130,000 ($30 $10)

130,000 ($30 $10) $1,850,000 $405,000

130,000 ($20)

130,000 ($20) $2,255,000

$2,600,000 $2,255,000

Q P

Q P I

–

=– – –

–

=– – –

=–

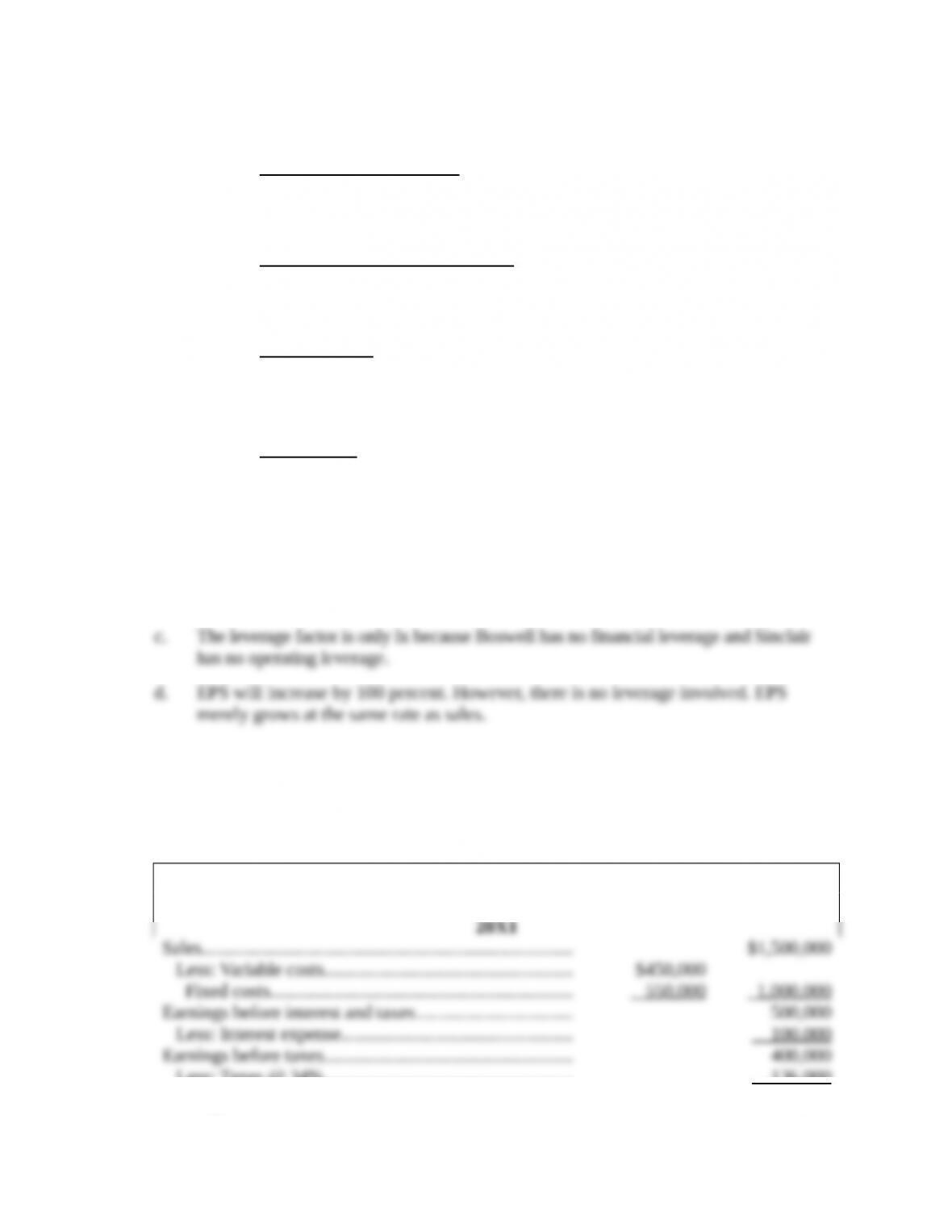

20. Combining operating and financial leverage (LO5) Sinclair Manufacturing and Boswell

Brothers Inc. are both involved in the production of brick for the homebuilding industry.

Their financial information is as follows:

Capital Structure

Sinclair Boswell

Debt @ 11%…………………………………………………… $ 900,000 0

Common stock, $10 per share………………………….. 600,000 $ 1,5000,000

Total…………………………………………………………… $ 1,500,000 $ 1,500,000

Common shares………………………………………………. 60,000 150,000

Operating Plan

Sales (55,000 units at $20 each)………………………… $ 1,100,000 $ 1,100,000

Less: Variable costs……………………………………… 880,000 550,000

………………………………………………………………………. ($16 per unit) ($10 per unit)

Fixed costs……. 0 305,000

Earnings before interest and taxes (EBIT)…………… $ 220,000 $ 245,000

a. If you combine Sinclair’s capital structure with Boswell’s operating plan, what is the

degree of combined leverage? (Round to two places to the right of the decimal point.)

b. If you combine Boswell’s capital structure with Sinclair’s operating plan, what is the

degree of combined leverage?

c. Explain why you got the results you did in part b.

d. In part b, if sales double, by what percentage will EPS increase?

5-20. Solution:

Sinclair Manufacturing and Boswell Brothers

a.

( VC)

DCL ( VC) FC

55,000 ($20 $10)

55,000 ($20 $10) $305,000 $99,000

550,000

550,000 $305,000 $99,000

3.77x

Q P

Q P I

–

=– – –

–

=– – –

=– –

=

b.

( VC)

DCL ( VC) FC

55,000($20 $16)

55,000($20 $16) 0 0

55,000($4)

55,000($4)

$220,000

$220,000

1x

Q P

Q P I

–

=– – –

–

=– – –

=

=

=

5-20. (Continued)

21. Expansion and leverage (LO5) DeSoto Tools Inc. is planning to expand production. The

expansion will cost $300,000, which can be financed either by bonds at an interest rate of

14 percent or by selling 10,000 shares of common stock at $30 per share. The current

income statement before expansion is as follows:

DESOTO TOOLS Inc.

Income Statement

Shares………………………………………………………………….. 100,000

Earnings per share…………………………………………………. $ 2.64

After the expansion, sales are expected to increase by $1,000,000. Variable costs will

remain at 30 percent of sales, and fixed costs will increase to $800,000. The tax rate is

34 percent.

a. Calculate the degree of operating leverage, the degree of financial leverage, and the

degree of combined leverage before expansion. (For the degree of operating leverage,

use the formula developed in footnote 2. For the degree of combined leverage, use the

formula developed in footnote 3. These instructions apply throughout this problem.)

b. Construct the income statement for the two alternative financing plans.

c. Calculate the degree of operating leverage, the degree of financial leverage, and the

degree of combined leverage, after expansion.

d. Explain which financing plan you favor and the risks involved with each plan.

5-21. Solution:

DeSoto Tools Inc.

a.

VC

DOL TVC FC

S

S

–

=– –

$1,500,000 $450,000 2.1x

$1,500,000 $450,000 $550,000

EBIT

DFL EBIT

$500,000

$500,000 $100,000

$400,000

I

–

= =

– –

=–

=–

TVC

DCL TVC FC

$1,500,000 $450,000

$1,500,000 $450,000 $550,000 $100,000

$1,050,000 2.63x

$400,000

S

S I

–

=– – –

–

=—

= =

5-21. (Continued)

b. Income Statement after Expansion

Debt Equity

Sales $2,500,000 $2,500,000

Less: Variable costs (30%) 750,000 750,000

1 New interest expense level if expansion is financed with debt.

2 Number of common shares outstanding if expansion is financed with equity.

c.

TVC

DOL TVC FC

$2,500,000 $750,000

DOL (Debt/Equity) $2,500,000 $750,000 $800,000

$1,750,000 1.84x

$950,000

S

S

–

=– –

–

=– –

= =

5-21. (Continued)

EBIT

DFL EBIT

$950,000 $950,000

DFL (Debt) 1.18x

$950,000-$142,000 $808,000

$950,000 $950,000

DFL (Equity) 1.12x

$950,000-$100,000 $850,000

$2,500,000 $750,000

DCL (Debt) $2,500,000 $750,000 $800,000 $142,00

I

=–

= = =

= = =

–

=—0

$1,750,000 2.17x

$808,000

= =

$2,500,000 $750,000

DCL (Equity) $2,500,000 $750,000 $800,000 $100,000

–

=– – –

22. Leverage analysis with actual companies (LO6) Using Standard & Poor’s data or annual

reports, compare the financial and operating leverage of Chevron, Eastman Kodak, and

Delta Airlines for the most current year. Explain the relationship between operating and

financial leverage for each company and the resultant combined leverage. What accounts

for the differences in leverage of these companies?

5-22. Solution:

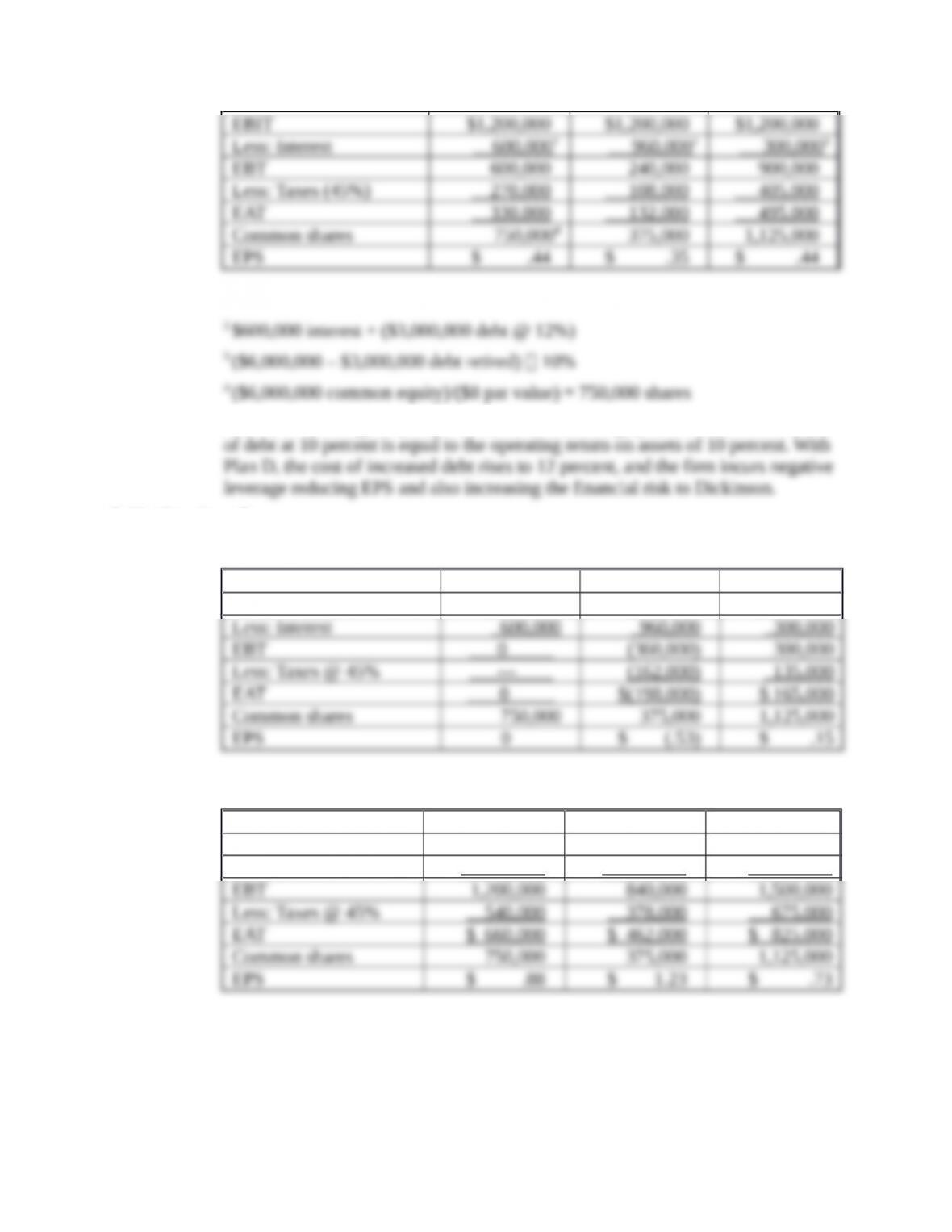

23. Leverage and sensitivity analysis (LO6) Dickinson Company has $12 million in assets.

Currently half of these assets are financed with long-term debt at 10 percent and half with

common stock having a par value of $8. Ms. Smith, vice president of finance, wishes to

analyze two refinancing plans, one with more debt (D) and one with more equity (E). The

company earns a return on assets before interest and taxes of 10 percent. The tax rate is 45

percent.

Under Plan D, a $3 million long-term bond would be sold at an interest rate of

12 percent and 375,000 shares of stock would be purchased in the market at $8 per share

and retired.

Under Plan E, 375,000 shares of stock would be sold at $8 per share and the $3,000,000

in proceeds would be used to reduce long-term debt.

a. How would each of these plans affect earnings per share? Consider the current plan

and the two new plans.

b. Which plan would be most favorable if return on assets fell to 5 percent? Increased to

15 percent? Consider the current plan and the two new plans.

c. If the market price for common stock rose to $12 before the restructuring, which plan

would then be most attractive? Continue to assume that $3 million in debt will be

used to retire stock in Plan D and $3 million of new equity will be sold to retire debt

in Plan E. Also assume for calculations in part c that return on assets is 10 percent.

5-23. Solution:

Dickinson Company

Income Statements

a. Return on assets = 10% EBIT = $ 1,200,000

Current Plan D Plan E

1 $6,000,000 debt @ 10%

Plan E and the original plan provide the same earnings per share because the cost

5-23. (Continued)

b. Return on assets = 5% EBIT = $600,000

Current Plan D Plan E

EBIT $600,000 $600,000 $ 600,000

Return on assets = 15% EBIT = $1,800,000

Current Plan D Plan E

EBIT $1,800,000 $1,800,000 $1,800,000

Less: Interest 600,000 960,000 300,000

If the return on assets decreases to 5 percent, Plan E provides the best EPS, and at

15 percent return, Plan D provides the best EPS. Plan D is still risky, having an

interest coverage ratio of less than 2.0.

5-23. (Continued)

c. Return on Assets = 10% EBIT = $1,200,000

Current Plan D Plan E

1 750,000 – ($3,000,000/$12 per share)

2 750,000 + ($3,000,000/$12 per share)

As the price of the common stock increases, Plan E becomes more attractive

24. Leverage and sensitivity analysis (LO6) Edsel Research Labs has $27 million in assets.

Currently, half of these assets are financed with long-term debt at 5 percent and half with

common stock having a par value of $10. Ms. Edsel, the vice president of finance, wishes

to analyze two refinancing plans, one with more debt (D) and one with more equity (E).

The company earns a return on assets before interest and taxes of 5 percent. The tax rate is

30 percent.

Under Plan D, a $6.75 million long-term bond would be sold at an interest rate of 11

percent and 675,000 shares of stock would be purchased in the market at $10 per share and

retired. Under Plan E, 675,000 shares of stock would be sold at $10 per share and the

$6,750,000 in proceeds would be used to reduce long-term debt.

a. How would each of these plans affect earnings per share? Consider the current plan

and the two new plans. Which plan(s) would produce the highest EPS? Note that due

to tax loss carry-forwards and carry-backs, taxes can be a negative number.

b. Which plan would be most favorable if return on assets increased to 8 percent?

Compare the current plan and the two new plans. What has caused the plans to give

different EPS numbers?

c. Assuming return on assets is back to the original 5 percent, but the interest rate on

new debt in Plan D is 7 percent, which of the three plans will produce the highest

EPS? Why?