3-27. Solution:

Jolie Foster Care Homes Inc.

a.

Net income

Total assets

20X1 $155,000/$2,390,000 = 6.49%

Comment: There is a strong upward movement in return on

assets over the four-year period.

b.

Net income

Stockholders’ equity

20X1 $155,000/$761,000 = 20.37%

Comment: The return on stockholders’ equity ratio is going

3-27. (Continued)

Optional: This can be confirmed by computing total debt to

total assets for each year.

Total debt

Total assets

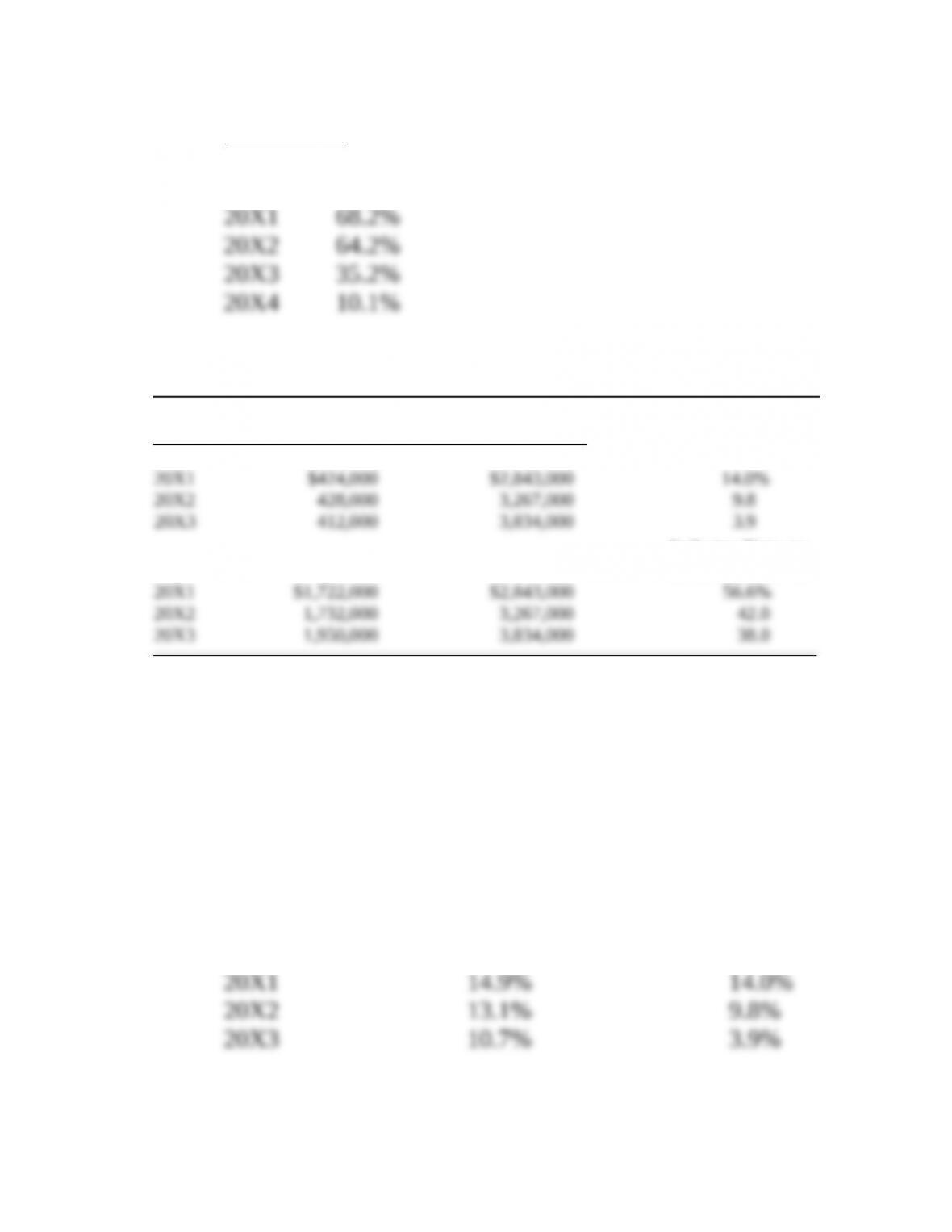

27. Trend analysis (LO4) Quantum Moving Company has the following data. Industry

information also is shown.

Industry Data on

Company Data Net Income/Total Assets

Year Net Income Total Assets

Industry Data on

Year Debt Total Assets Debt/Total Assets

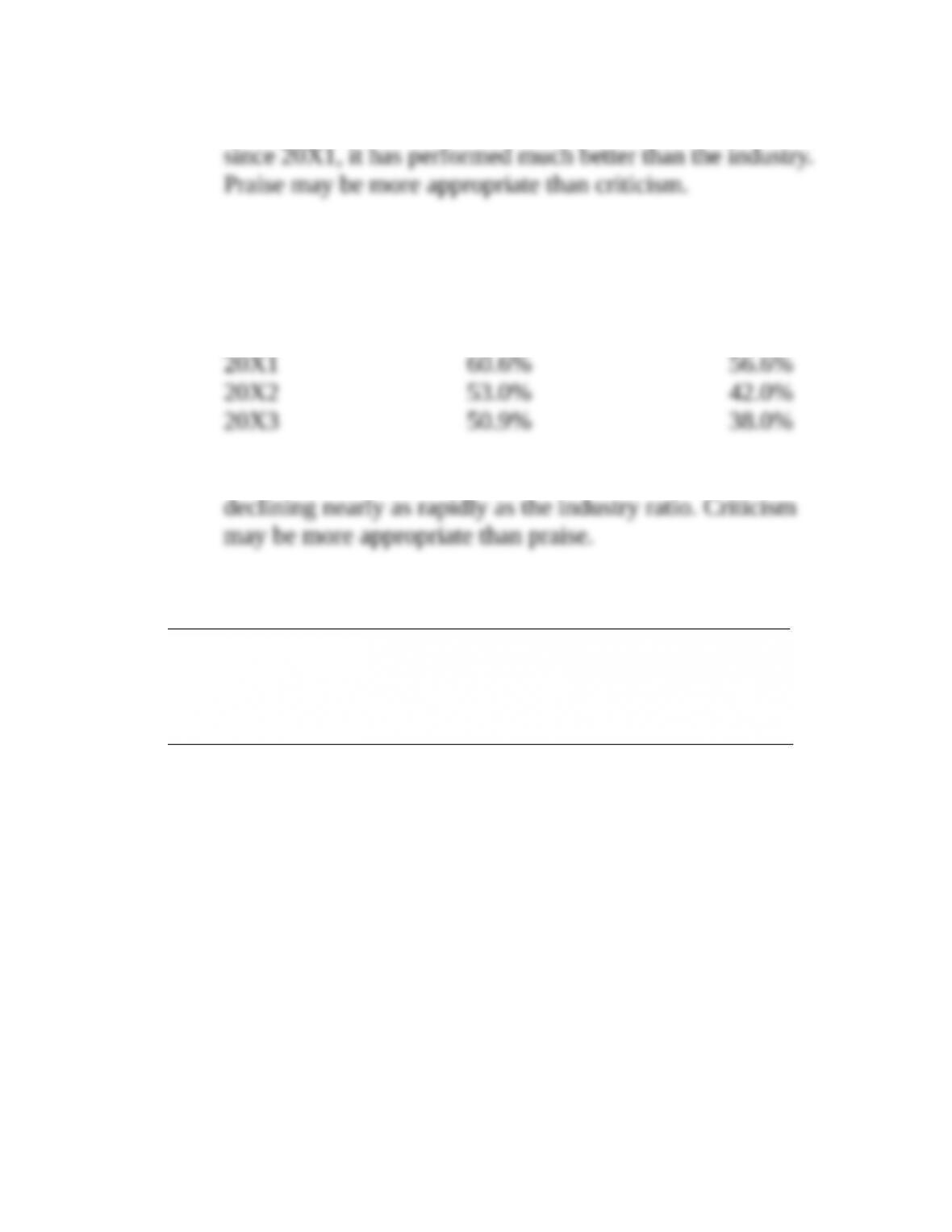

As an industry analyst comparing the firm to the industry, are you likely to praise or

criticize the firm in terms of the following:

a. Net income/Total assets.

b. Debt/Total assets.

3-28. Solution:

Quantum Moving Company

a. Net income/total assets

Year Quantum Ratio Industry Ratio

Although the company has shown a declining return on assets

3-28. (Continued)

b. Debt/total assets

Year Quantum Ratio Industry Ratio

While the company’s debt ratio is declining, it is not

29. Analysis by divisions (LO2) The Global Products Corporation has three subsidiaries.

Medical Supplies Heavy Machinery Electronics

Sales………………………………… $20,040,000 $5,980,000 $4,730,000

Net income (after taxes)……… 1,700,000 592,000 402,000

Assets………………………………. 8,340,000 8,760,000 3,570,000

.

a. Which division has the lowest return on sales?

b. Which division has the highest return on assets?

c. Compute the return on assets for the entire corporation.

d. If the $8,760,000 investment in the heavy machinery division is sold off and

redeployed in the medical supplies subsidiary at the same rate of return on assets

currently achieved in the medical supplies division, what will be the new return on

assets for the entire corporation?

3-29. Solution:

Global Products Corporation

a. Medical Heavy

Supplies Machinery Electronics

b. Medical Heavy

Supplies Machinery Electronics

3-29. (Continued)

c.

Corporate net income $1,700,000 $592,000 $402,000

Corporate total assets $8,340,000 $8,760,000 $3,570,000

$2,694,000

$20,670,000

13.03%

+ +

=+ +

=

=

d. Return on redeployed assets in heavy machinery.

20.38% × $8,760,000 = $1,785,288

Return on assets for the entire corporation:

Corporate net income $1, 700,000 $1, 785, 288 $402,000

Corporate total assets $20,670,000

$3,887, 288

$20,670,000

18.81%

+ +

=

=

=

30. Analysis by affiliates (LO1) Omni Technology Holding Company has the following three

affiliates:

Personal Foreign

Software Computers Operations

Sales…………………………… $40,200,000 $60,080,000 $100,680,000

Net income (after taxes)… 2,086,000 2,880,000 8,510,000

Assets…………………………. 5,820,000 25,790,000 60,630,000

Stockholders’ equity……… 4,090,000 10,170,000 50,950,000

a. Which affiliate has the highest return on sales?

b. Which affiliate has the lowest return on assets?

c. Which affiliate has the highest total asset turnover?

d. Which affiliate has the highest return on stockholders’ equity?

e. Which affiliate has the highest debt ratio? (Assets minus stockholders’ equity

equals debt.)

f. Returning to question b, explain why the software affiliate has the highest return on

total assets.

g. Returning to question d, explain why the personal computer affiliate has a higher

return on stockholders’ equity than the foreign operations affiliate even though it has

a lower return on total assets.

3-30. Solution:

Omni Technology Holding Company

a. Net income/Sales

Personal Foreign

Software Computers Operations

5.19% 4.79% 8.45%

The foreign operation affiliate has the highest return on sales.

b. Net income/Total assets

Personal Foreign

Software Computers Operations

35.84% 11.17% 14.04%

The personal computer affiliate has the lowest return on

assets.

3-30. (Continued)

c. Sales/Total assets

Personal Foreign

Software Computers Operations

6.91x 2.33x 1.66x

The software affiliate has the highest return on total asset

turnover.

d. Net income/

Stockholders’ equity

The software affiliate has the highest return on stockholders’

equity.

e. Debt/Total assets

Personal Foreign

Software Computers Operations

29.73% 60.57% 15.97%

The personal computer affiliate has the highest

debt-to-total-assets ratio.

f. This is because of its high total asset turnover ratio of 6.91x

g. This is because the personal computer affiliate has a higher

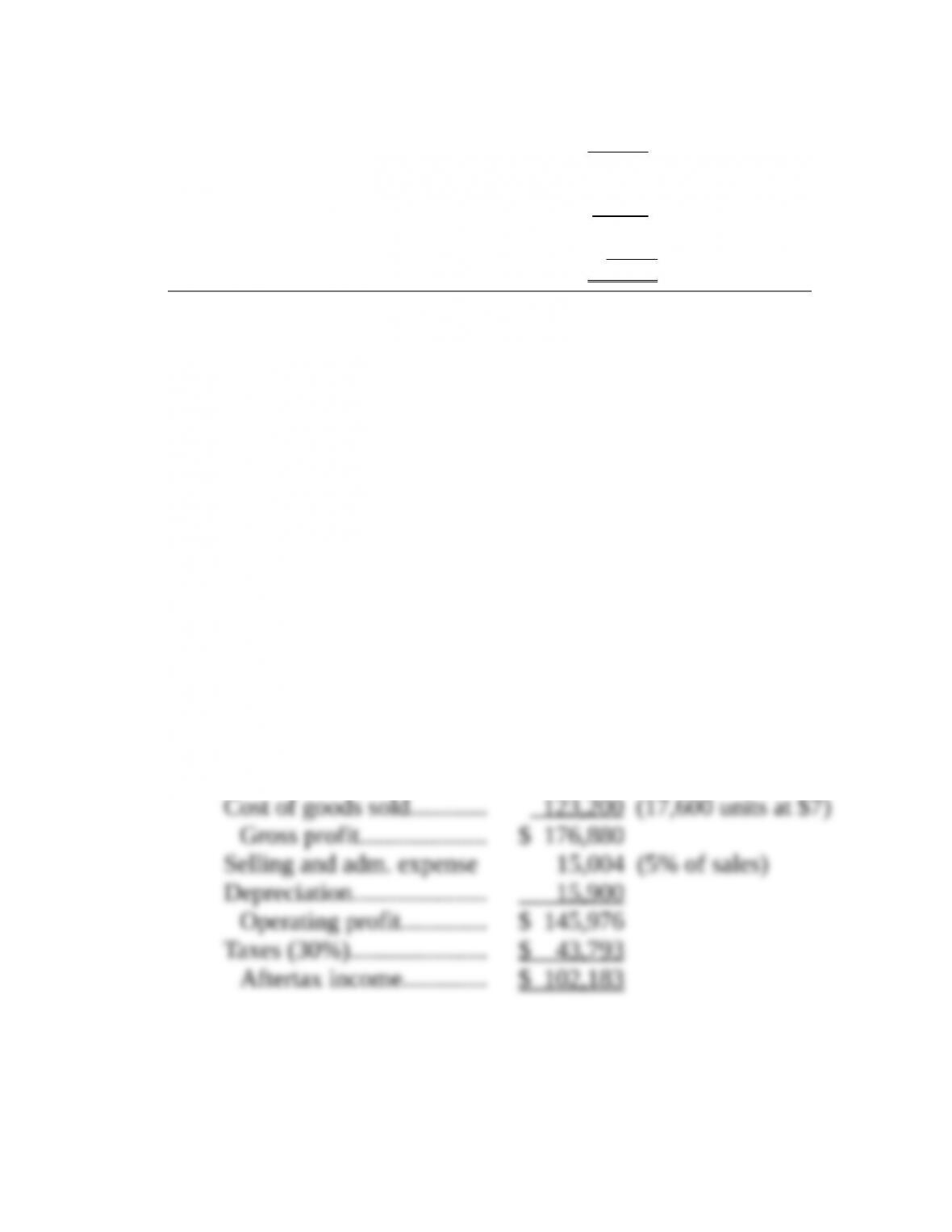

31. Inflation and inventory accounting effect (LO5) The Canton Corporation shows the

following income statement. The firm uses FIFO inventory accounting.

CANTON CORPORATION

Income Statement for 20X1

Personal Foreign

Software Computers Operations

51.0% 28.32% 16.70%

Sales…………………………………………………………… $272,800 (17,600 units at $15.50)

Cost of goods sold………………………………………… 123,200 (17,600 units at $7.00)

Gross profit…………………………………………………. 149,600

Selling and administrative expense…………………. 13,640

Depreciation………………………………………………… 15,900

Operating profit……………………………………………. 120,060

Taxes (30%)………………………………………………… 36,018

Aftertax income…………………………………………… $ 84,042

a. Assume in 20X2 that the same 17,600-unit volume is maintained, but that the sales

price increases by 10 percent. Because of FIFO inventory policy, old inventory will

still be charged off at $7 per unit. Also assume selling and administrative expense will

be 5 percent of sales and depreciation will be unchanged. The tax rate is 30 percent.

Compute aftertax income for 20X2.

b. In part a, by what percent did aftertax income increase as a result of a 10 percent

increase in the sales price? Explain why this impact took place.

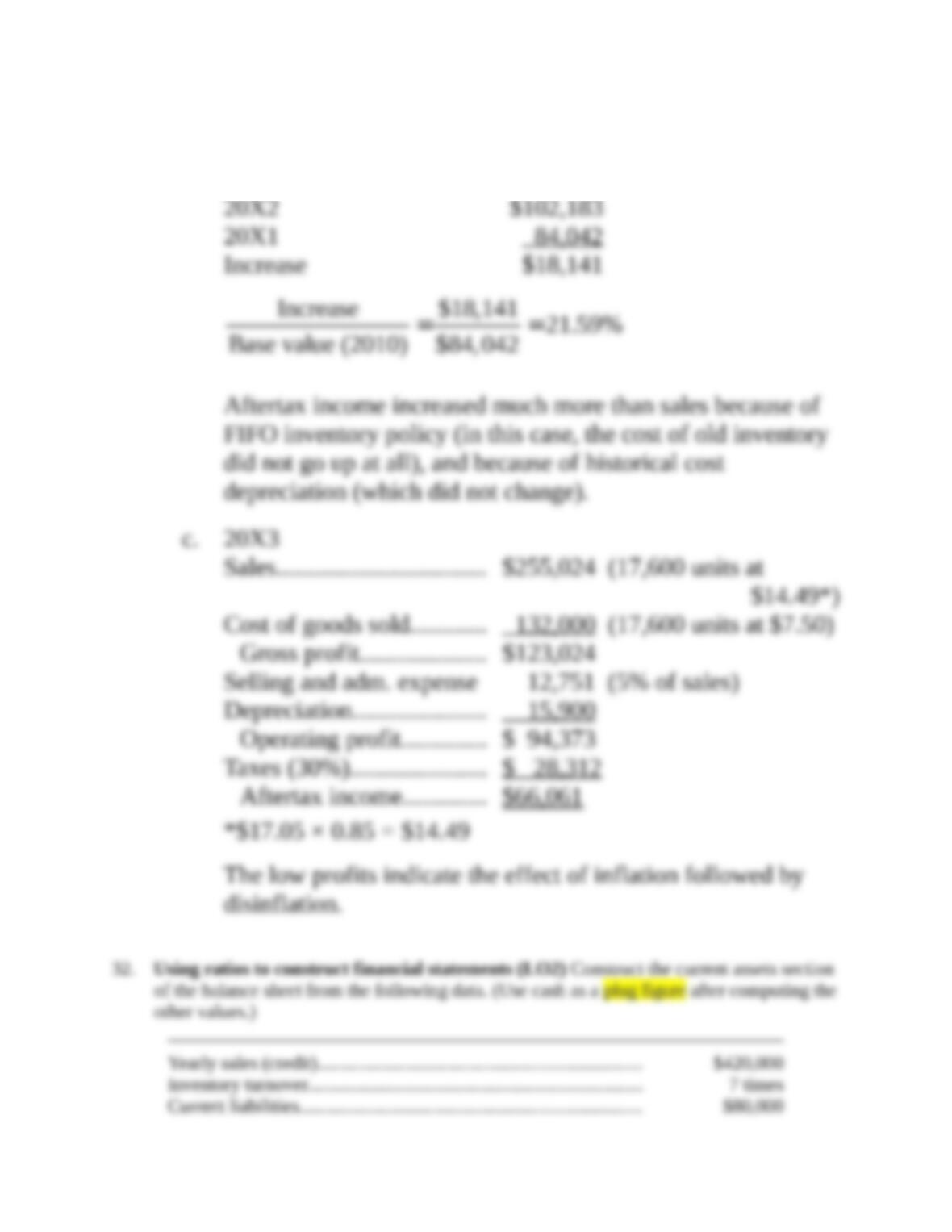

c. Now assume that in 20X3 the volume remains constant at 17,600 units, but the sales

price decreases by 15 percent from its year 20X2 level. Also, because of FIFO

inventory policy, cost of goods sold reflects the inflationary conditions of the prior

year and is $7.50 per unit. Further, assume selling and administrative expense will be

5 percent of sales and depreciation will be unchanged. The tax rate is 30 percent.

Compute the aftertax income.

3-31. Solution:

Canton Corporation

a. 20X2

Sales…………………………… $300,080 (17,600 units at

$17.05)

3-31. (Continued)

b. Gain in aftertax income

Current ratio……………………………………………………………………… 2

Average collection period…………………………………………………… 36 days

Current assets: $

Cash………………………………………………………………. ______

Accounts receivable………………………………………… ______

Inventory……………………………………………………….. ______

Total current assets……………………………………… ______

3-32. Solution:

Inventory = $420,000/7

= $60,000

Current assets = 2 × $80,000

33. Using ratios to construct financial statements (LO2) The Griggs Corporation has credit

sales of $1,200,000. Given these ratios, fill in the following balance sheet.

Total assets turnover…………………………….. 2.4 times

Cash to total assets……………………………….. 2.0%

Accounts receivable turnover………………… 8.0 times

Inventory turnover……………………………….. 10.0 times

Current ratio………………………………………… 2.0 times

Debt to total assets……………………………….. 61.0%

GRIGGS CORPORATION

Balance Sheet

Assets Liabilities and Stockholders’ Equity

Cash ………………………… _____ Current debt……………………………………… _____

Accounts receivable…… _____ Long-term debt………………………………….. _____

Inventory………………….. _____ Total debt…………………………………….. _____

Total current assets . _____ Equity………………………………………………. _____

Fixed assets ……………… _____ Total debt and stockholders’ equity _____

Total assets …………. _____