Chapter 12: The Capital Budgeting Decision

12-29. (Continued)

Next, determine the net present value.

Cash Flow Present

Year (Inflows) PVIF at 12% Value

New asset should be purchased.

Calculator Solution:

Using a financial calculator,

Press the following keys: 2nd, CF, 2nd, Clear.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 12: The Capital Budgeting Decision

Press down arrow, enter 33,960, and press Enter.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 12: The Capital Budgeting Decision

The asset should be purchased because NPV is positive.

30. Working capital requirements in capital budgeting (LO12-4) The Spartan Technology

Company has a proposed contract with the Digital Systems Company of Michigan. The initial

investment in land and equipment will be $120,000. Of this amount, $70,000 is subject to

five-year MACRS depreciation. The balance is in nondepreciable property. The contract covers

six years; at the end of six years, the nondepreciable assets will be sold for $50,000. The

depreciated assets will have zero resale value.

The contract will require an additional investment of $55,000 in working capital at the

beginning of the first year and, of this amount, $25,000 will be returned to the Spartan

Technology Company after six years.

The investment will produce $50,000 in income before depreciation and taxes for each of

the six years. The corporation is in a 40 percent tax bracket and has a 10 percent cost of capital.

Should the investment be undertaken? Use the net present value method.

12-30. Solution:

Spartan Technology Company

Although there are some complicated features to this problem,

we are still comparing the present value of cash flows to the

total initial investment.

The initial investment is:

In computing the present value of the cash flows, we first

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 12: The Capital Budgeting Decision

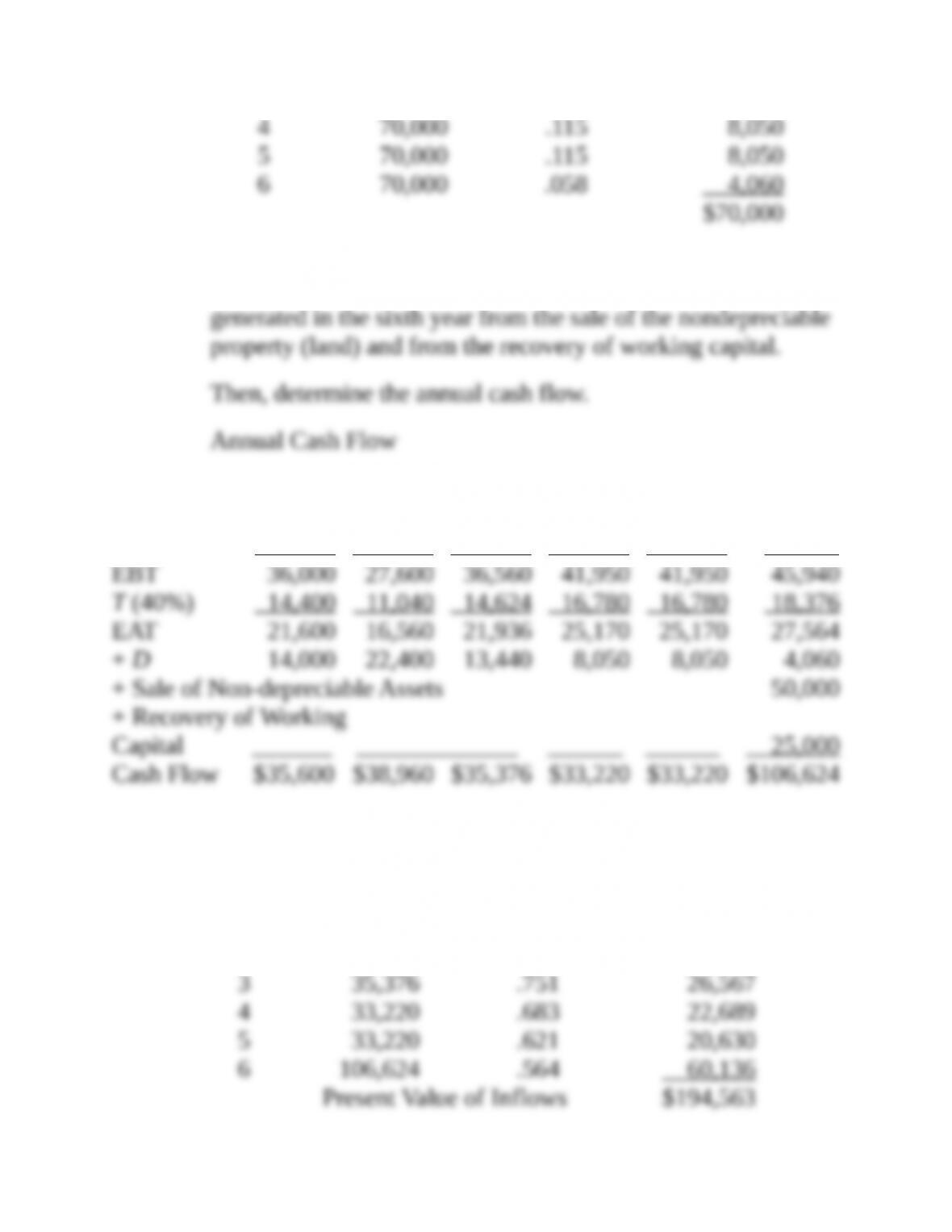

We then determine the annual cash flow. In addition to normal

cash flow from operations; we also consider the funds

1 2 3 4 5 6

EBDT $50,000 $50,000 $50,000 $50,000 $50,000 $50,000

– D 14,000 22,400 13,440 8,050 8,050 4,060

We then determine the net present value.

Cash Flow Present

Year (Inflows) PVIF @ 10% Value

1 $ 35,600 .909 $ 32,360

2 38,960 .826 32,181

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 12: The Capital Budgeting Decision

Calculator Solution:

Using a financial calculator:

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, press 175,000 +|–, press the Enter key.

Press down arrow, enter 35,600, and press Enter.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 12: The Capital Budgeting Decision

31. Tax losses and gains in capital budgeting (LO12-2) An asset was purchased three years

ago for $120,000. It falls into the five-year category for MACRS depreciation. The firm is

in a 35 percent tax bracket. Compute the following:

a. Tax loss on the sale and the related tax benefit if the asset is sold now for $15,060.

b. Gain and related tax on the sale if the asset is sold now for $56,060. (Refer to footnote 4 in

the chapter.)

12-31. Solution:

First determine the book value of the asset.

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

a. $15,060 sales price

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 12: The Capital Budgeting Decision

b. $56,060 sales price

32. Capital budgeting with cost of capital computation (LO12-5) DataPoint Engineering is

considering the purchase of a new piece of equipment for $240,000. It has an eight-year

midpoint of its asset depreciation range (ADR). It will require an additional initial

investment of $140,000 in nondepreciable working capital. Thirty-five thousand dollars of

this investment will be recovered after the sixth year and will provide additional cash flow

for that year. Here is the projected income before depreciation and taxes for the next six

years:

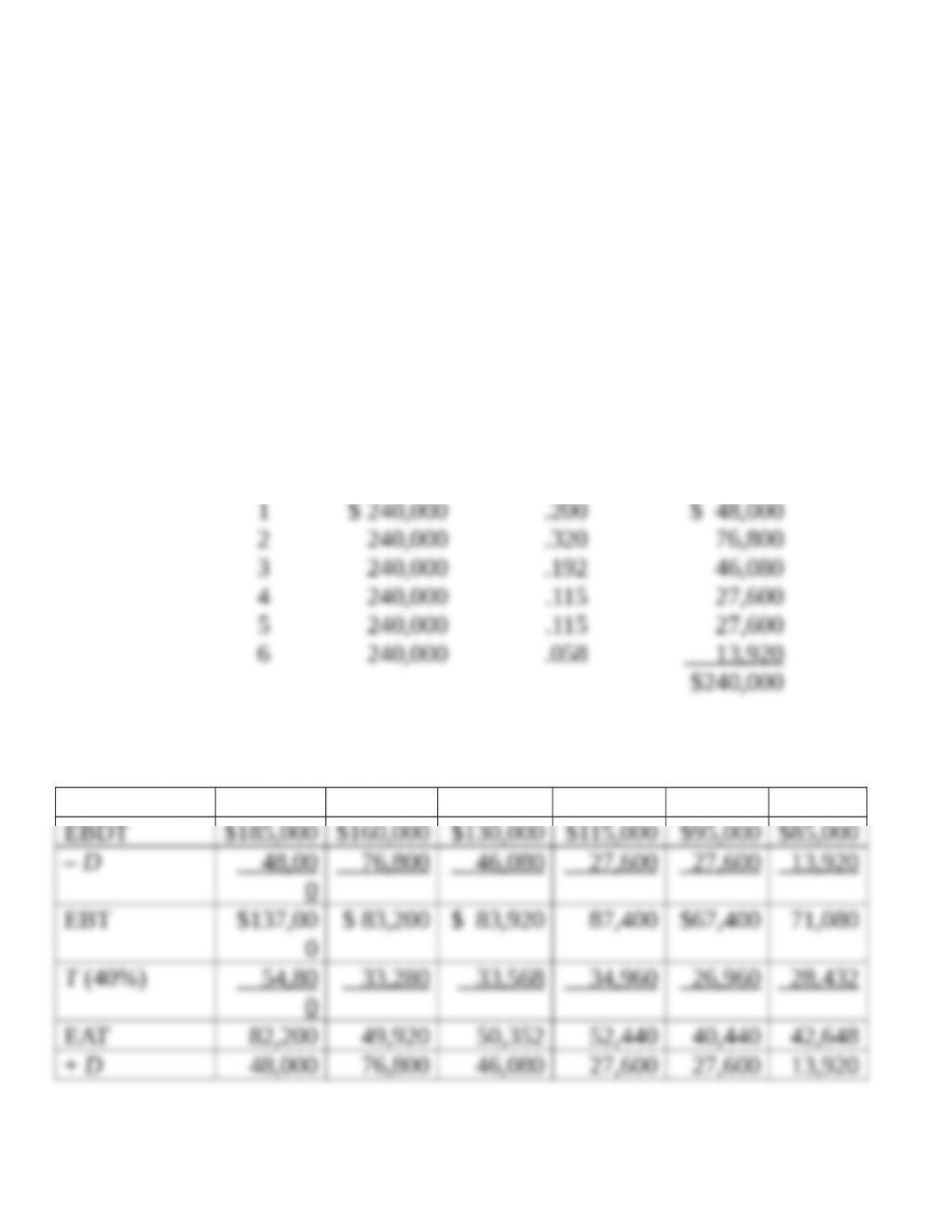

Year Amount

1…………………. $185,000

2…………………. 160,000

3…………………. 130,000

4…………………. 115,000

5…………………. 95,000

6………………… 85,000

The tax rate is 40 percent. The cost of capital must be computed based on

the following (round the final value to the nearest whole number):

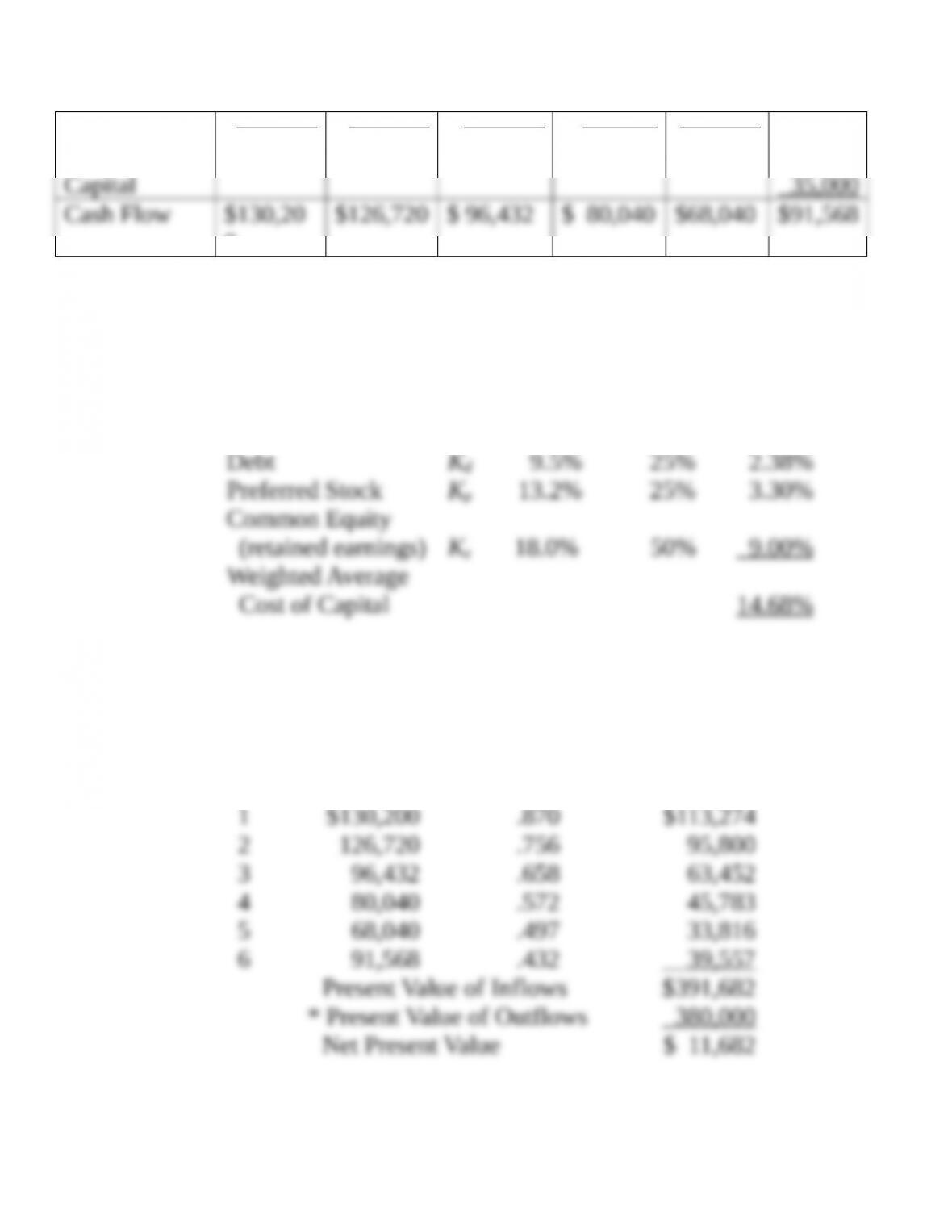

Cost (aftertax) Weights

Debt…………………………………………………… Kd 9.5% 25%

Preferred stock…………………………………….. Kp13.2 25

Common equity (retained earnings)……….. Ke18.0 50

a. Determine the annual depreciation schedule.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 12: The Capital Budgeting Decision

b. Determine annual cash flow. Include recovered working capital in the sixth year.

c. Determine the weighted average cost of capital.

d. Determine the net present value. Should DataPoint purchase the new equipment?

12-32. Solution:

DataPoint Engineering

a. An eight-year midpoint of the ADR leads to five-year

MACRS depreciation.

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

b. Annual Cash Flow

1 2 3 4 5 6

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 12: The Capital Budgeting Decision

+ Recovery of

Working

0

c. Weighted Average Cost of Capital

Cost

(aftertax) Weights Weighted

d. Net Present Value

Cash Flow Present

Year (inflows) PVIF at 15% Value

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 12: The Capital Budgeting Decision

*This represents the $240,000 for the equipment plus the

Calculator Solution:

Using a financial calculator:

(d)

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, press 380,000 +|–, press the Enter key.

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 12: The Capital Budgeting Decision

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 91,568, and press Enter.

Press down arrow, enter 1, and press Enter.

The net present value 11,619.93 is positive and DataPoint Engineering should purchase the

equipment.

33. Replacement decision analysis (LO12-4) Hercules Exercise Equipment Co. purchased a

computerized measuring device two years ago for $58,000. The equipment falls into the

five-year category for MACRS depreciation and can currently be sold for $24,800.

A new piece of equipment will cost $148,000. It also falls into the five-year category

for MACRS depreciation.

Assume the new equipment would provide the following stream of added cost savings

for the next six years.

Year Cash Savings

1………… $62,000

2………… 54,000

3………… 52,000

4………… 50,000

5………… 47,000

6………… 36,000

The firm’s tax rate is 35 percent and the cost of capital is 12 percent.

a. What is the book value of the old equipment?

b. What is the tax loss on the sale of the old equipment?

c. What is the tax benefit from the sale?

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.

Chapter 12: The Capital Budgeting Decision

d. What is the cash inflow from the sale of the old equipment?

e. What is the net cost of the new equipment? (Include the inflow from the sale of the

old equipment.)

f. Determine the depreciation schedule for the new equipment.

g. Determine the depreciation schedule for the remaining years of the old equipment.

h. Determine the incremental depreciation between the old and new equipment and the

related tax shield benefits.

i. Compute the aftertax benefits of the cost savings.

j. Add the depreciation tax shield benefits and the aftertax cost savings, and determine

the present value. (See Table 12-17 as an example.)

k. Compare the present value of the incremental benefits (j) to the net cost of the new

equipment (e). Should the replacement be undertaken?

Copyright © 2017 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw-Hill Education.