11-21. Solution:

Sauer Milk Inc.

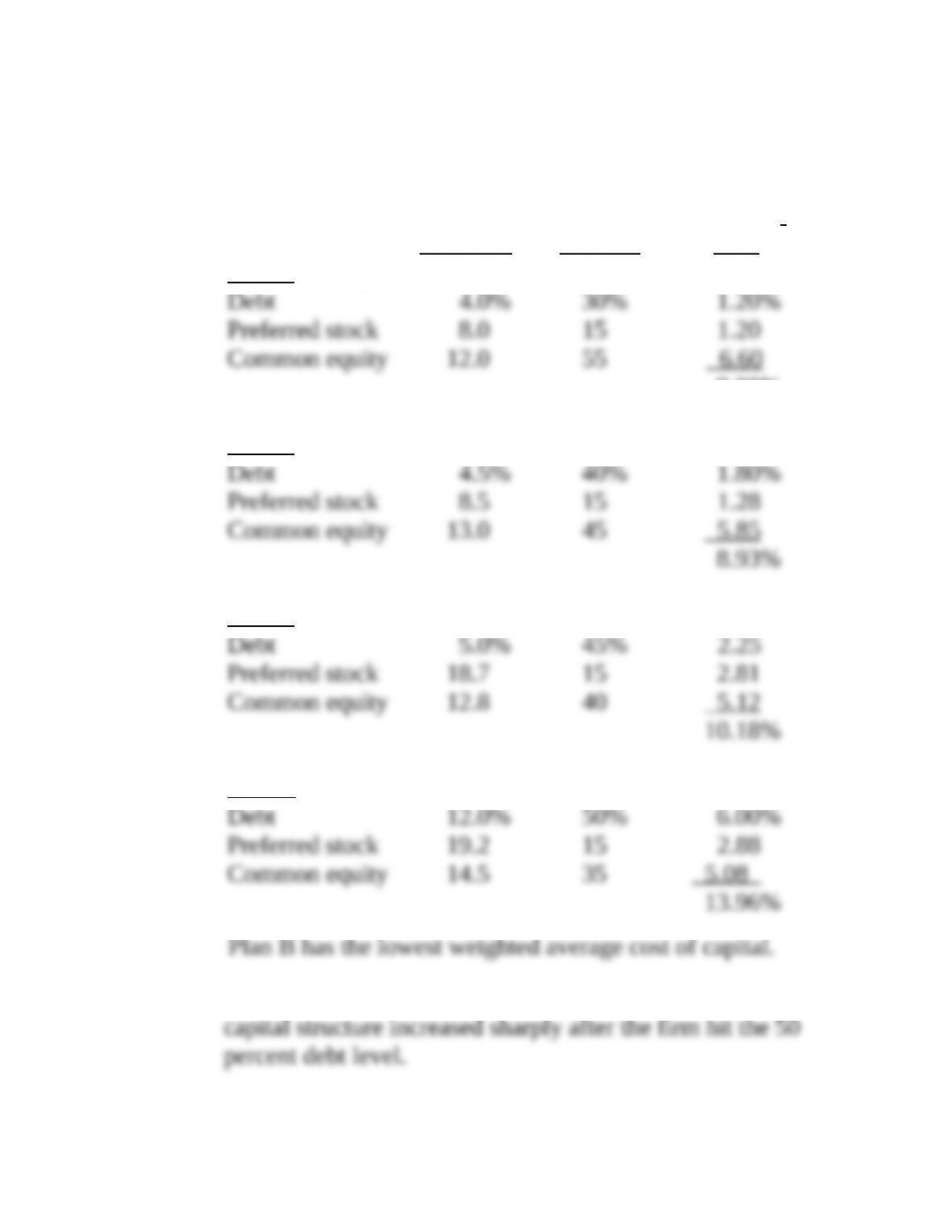

a. Cost Weighted

(aftertax) Weights Cost

Plan A

9.00%

Plan B

Plan C

Plan D

b. Plan D is higher than Plan C because all components in the

22. Weighted average cost of capital (LO11-1) Given the following information, calculate the

weighted average cost of capital for Hamilton Corp. Line up the calculations in the order

shown in Table 11-1.

Percent of capital structure:

Debt………………………. 35%

Preferred stock……….. 20

Common equity………. 45

Additional information:

Bond coupon rate…………………………. 11%

Bond yield to maturity………………….. 9%

Dividend, expected common…………. $ 5.00

Dividend, preferred………………………. $ 12.00

Price, common…………………………….. $ 60.00

Price, preferred…………………………….. $106.00

Flotation cost, preferred………………… $ 4.50

Growth rate…………………………………. 6%

Corporate tax rate…………………………. 35%

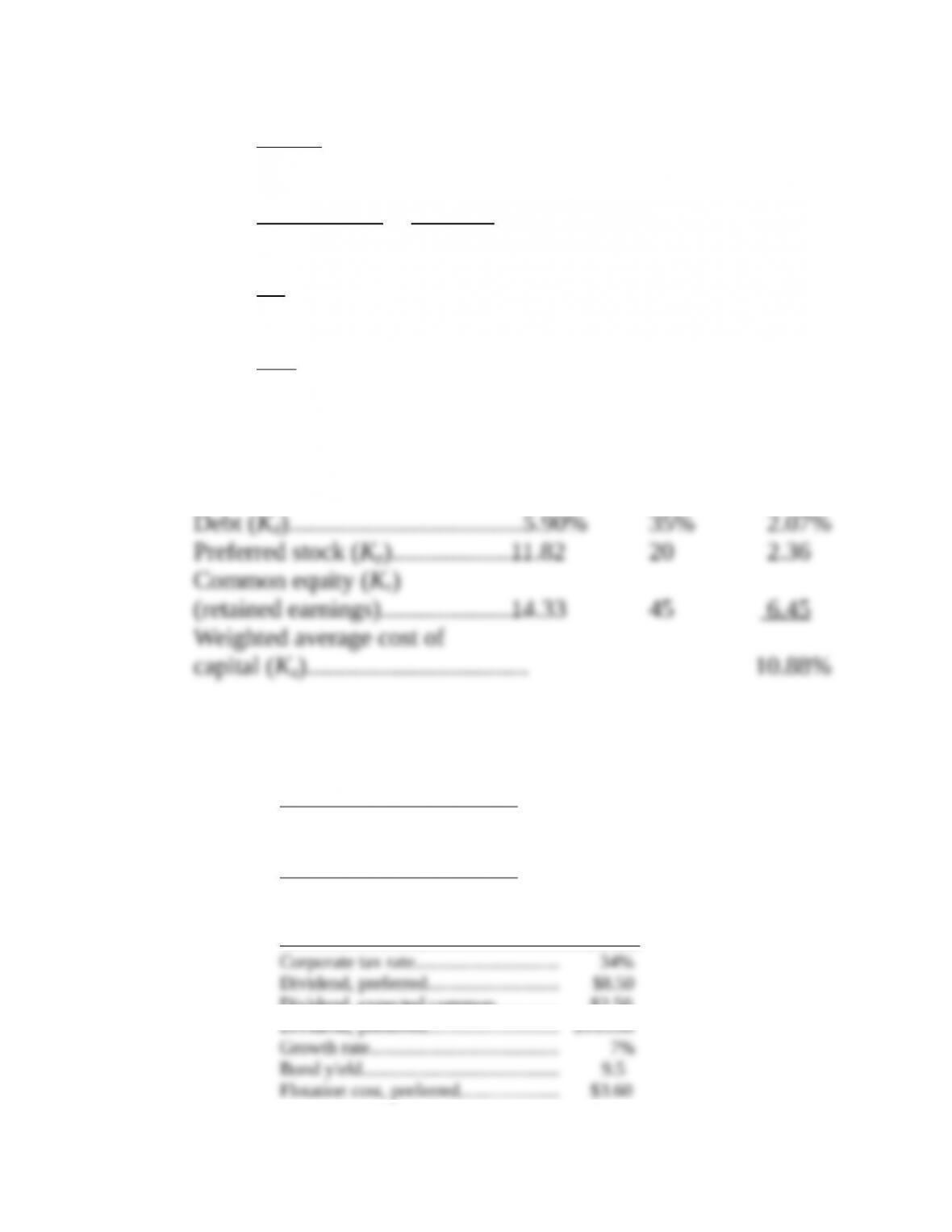

11-22. Solution:

The Hamilton Corp.

Kd = Yield (1 – T)

The bond yield of 9 percent is used rather than the coupon rate

1

0

$12.00 $12.00 11.82%

$106 $4.50 $101.50

$5 6.00% 8.33% 6.00% 14.33%

$60

p

p

p

e

D

KP F

D

K g

P

=–

= = =

–

= +

= + = + =

Cost

(aftertax) Weights

Weighted

Cost

23. Given the following information, calculate the weighted average cost of capital for Digital

Processing Inc. Line up the calculations in the order shown in Table 11-1.

Percent of capital structure:

Preferred stock…………….. 20%

Common equity……………. 40

Debt……………………………. 40

Additional information:

Dividend, preferred………………………. $8.50

Dividend, expected common…………. $2.50

Dividend, preferred………………………. $105.00

Price, common…………………………….. $75.00

11-23. Solution:

Digital Processing Inc.

Cost

(aftertax) Weights

Weighted

Cost

24. Changes in costs and weighted average cost of capital (LO11-1) Brook’s Window

Shields Inc. is trying to calculate its cost of capital for use in a capital budgeting decision.

Mr. Glass, the vice president of finance, has given you the following information and has

asked you to compute the weighted average cost of capital.

The company currently has outstanding a bond with a 12.2 percent coupon rate and

another bond with a 9.5 percent coupon rate. The firm has been informed by its investment

banker that bonds of equal risk and credit rating are now selling to yield 13.4 percent.

The common stock has a price of $58 and an expected dividend (D1) of $5.30 per share.

The firm’s historical growth rate of earnings and dividends per share has been 9.5 percent,

but security analysts on Wall Street expect this growth to slow to 7 percent in future years.

The preferred stock is selling at $54 per share and carries a dividend of $6.75 per share.

The corporate tax rate is 35 percent. The flotation cost is 2.1 percent of the selling price for

preferred stock. The optimal capital structure is 40 percent debt, 25 percent preferred stock,

and 35 percent common equity in the form of retained earnings.

Compute the cost of capital for the individual components in the capital structure, and

then calculate the weighted average cost of capital (similar to Table 11-1).

11-24. Solution:

Brook’s Window Shields Inc.

Cost

(aftertax) Weights

Weighted

Cost

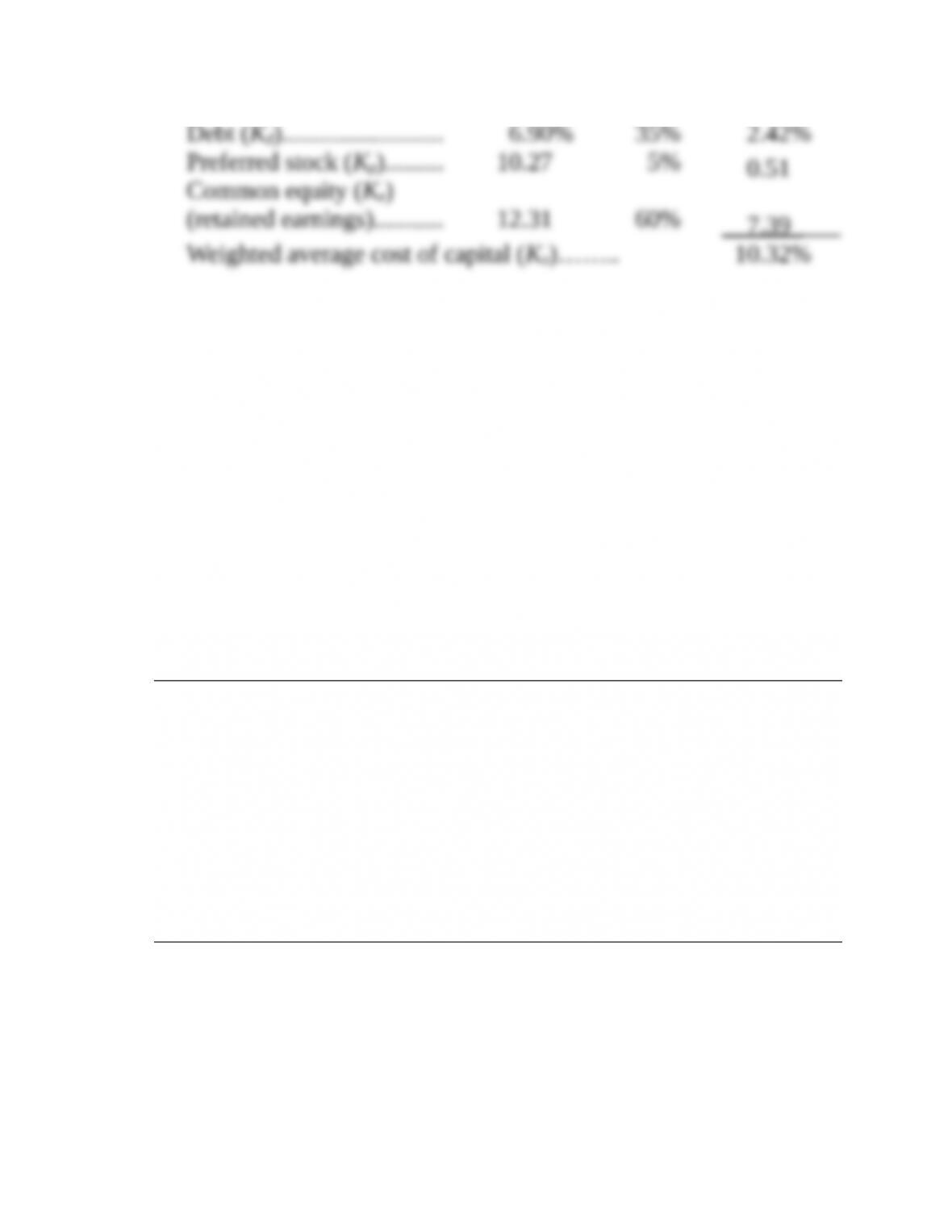

25. Changes in cost and weighted average cost of capital (LO11-1) A-Rod Manufacturing

Company is trying to calculate its cost of capital for use in making a capital budgeting

decision. Mr. Jeter, the vice president of finance, has given you the following information

and has asked you to compute the weighted average cost of capital.

The company currently has outstanding a bond with a 10.6 percent coupon rate and

another bond with an 8.2 percent rate. The firm has been informed by its investment banker

that bonds of equal risk and credit rating are now selling to yield 11.5 percent. The

common stock has a price of $65 and an expected dividend (D1) of $1.50 per share. The

historical growth pattern (g) for dividends is as follows:

$1.40

1.54

1.69

1.85

Compute the historical growth rate, round it to the nearest whole number, and use it for g.

The preferred stock is selling at $85 per share and pays a dividend of $8.50 per share.

The corporate tax rate is 40 percent. The flotation cost is 2.6 percent of the selling price for

preferred stock. The optimal capital structure for the firm is 35 percent debt, 5 percent

preferred stock, and 60 percent common equity in the form of retained earnings.

Compute the cost of capital for the individual components in the capital structure, and

then calculate the weighted average cost of capital (similar to Table 11-1).

11-25. Solution:

A-Rod Construction Company

Kd = Yield (1 – T)

Kp = Dp/(Pp – F)

Ke = (D1/P0) + g

g = 10% (see the following)

Bring the preceding values together to compute the weighted average

cost of capital.

Cost

(aftertax) Weights

Weighted

Cost

26. Impact of credit ratings on cost of capital (LO11-3) Northwest Utility Company faces

increasing needs for capital. Fortunately, it has an Aa3 credit rating. The corporate tax rate

is 40 percent. Northwest’s treasurer is trying to determine the corporation’s current

weighted average cost of capital in order to assess the profitability of capital budgeting

projects.

Historically, the corporation’s earnings and dividends per share have increased about

8.2 percent annually and this should continue in the future. Northwest’s common stock is

selling at $64 per share, and the company will pay a $6.50 per share dividend (D1).

The company’s $96 preferred stock has been yielding 8 percent in the current market.

Flotation costs for the company have been estimated by its investment banker to be $6.00

for preferred stock.

The company’s optimal capital structure is 55 percent debt, 20 percent preferred stock,

and 25 percent common equity in the form of retained earnings. Refer to the following

table on bond issues for comparative yields on bonds of equal risk to Northwest:

Data on Bond Issues

Issue

Moody’s

Rating Price

Yield to

Maturity

Utilities:

Southwest Electric Power––7¼ 2023……………Aa2 $ 895.18 8.74%

Pacific Bell––7⅜ 2025………………………………..Aa3 891.25 8.73

Pennsylvania Power & Light––8½

2022……………………………………………………….A2 970.66 8.77

Industrials:

Johnson & Johnson––6¾ 2023…………………….Aaa 880.24 8.55%

Dillard’s Department Stores––71/8

2023……………………………………………………….A2 960.92 8.22

Marriott Corp.––10 2015…………………………….B2 1,035.10 9.77

Compute the answers to the following questions from the information given:

a. Cost of debt, Kd (use the accompanying table––relate to the utility bond credit rating

for yield)

b. Cost of preferred stock, Kp

c. Cost of common equity in the form of retained earnings, Ke

d. Weighted average cost of capital

11-26. Solution:

Northwest Utility Company

a. The student must realize that the cost of debt is related to

the cost of debt for other debt issues of the same risk class.

Kd = Yield (1 – T)

b. Kp = Dp/(Pp – F)

c. Ke = (D1/P0) + g

d. Cost

(aftertax) Weights

Weighted

Cost

27. Marginal cost of capital (LO11-5) Delta Corporation has the following capital structure:

Cost

(aftertax) Weights

Weighted

Cost

Debt……………………………………………………………………………. 8.1% 35% 2.84%

Preferred stock (Kp)………………………………………………………. 9.6 5 .48

Common equity (Ke)

(retained earnings)…………………………………………………….10.1 60 6.06

Weighted average cost of capital (Ka)……………………………… 9.38%

a. If the firm has $18 million in retained earnings, at what size capital structure will the

firm run out of retained earnings?

b. The 8.1 percent cost of debt referred to earlier applies only to the first $14 million of

debt. After that, the cost of debt will go up. At what size capital structure will there be

a change in the cost of debt?

11-27. Solution:

Delta Corporation

a.

Retained earnings

% of retained earnings in the capital structure

$18 million /.60 $30million

X=

= =

b.

Amount of lower cost debt

% of debt in the capital structure

$14 million / .35 $40 million

Z=

= =

28. Marginal cost of capital (LO11-5) The Nolan Corporation finds it is necessary to

determine its marginal cost of capital. Nolan’s current capital structure calls for 50 percent

debt, 30 percent preferred stock, and 20 percent common equity. Initially, common equity

will be in the form of retained earnings (Ke) and then new common stock (Kn). The costs of

the various sources of financing are as follows: debt, 9.6 percent; preferred stock, 9

percent; retained earnings, 10 percent; and new common stock, 11.2 percent.

a. What is the initial weighted average cost of capital? (Include debt, preferred stock, and

common equity in the form of retained earnings, Ke.)

b. If the firm has $18 million in retained earnings, at what size capital structure will the

firm run out of retained earnings?

c. What will the marginal cost of capital be immediately after that point? (Equity will

remain at 20 percent of the capital structure, but will all be in the form of new

common stock, Kn.)

d. The 9.6 percent cost of debt referred to earlier applies only to the first $29 million of

debt. After that, the cost of debt will be 11.2 percent. At what size capital structure will

there be a change in the cost of debt?

e. What will the marginal cost of capital be immediately after that point? (Consider the

facts in both parts c and d.)