Gale Force Surfing Case 5

Working Capital—Level vs. Seasonal Production

Purpose: The case forces the student to view the impact of level versus seasonal production on inventory levels, bank loan requirements, and

profitability. It also considers the efficiencies (or inefficiencies) covered by the different production plans. The computations in the case are

parallel to Table 6-1 through Table 6-5 in the text, with the only difference being that seasonal production rather than level production is being

utilized. The case allows the student to properly track the movement of cash flow through the production process.

Relation to Text: The case should follow Chapter 6.

Complexity: The case involves numerous computations and may require 2 hours.

Solutions

1. New Tables 1 through 5, with Tim’s suggestion implemented, are shown in the following pages. Observe that the inventory level is now

constant at 400 units or $800,000 a month because all units produced are sold. As a side point, note that there may be no apparent need now to

Though not required, you may wish to refer to the old and new Table 4 to make a special point. Note that Tim’s suggestion causes inventory

2. New Table 5 shows the new cumulative loan balances and the interest expenses incurred each month. Under the old system (level production),

3. The first step is to compute total sales. Using the second row of Table 3 (either the old or new table), the total is $14,400,000. With an added

GALE FORCE SURFING (With Tim’s suggestion implemented)

TABLE 1. SALES FORECAST (in units)

1st Quarter 2nd Quarter 3rd Quarter 4th Quarter

TABLE 2. PRODUCTION SCHEDULE AND INVENTORY (seasonal production)

Beginning

Inventory

Production

this Month Sales

Ending

Inventory

Inventory

($2,000 per

unit)

October………………… 400 + 50 – 150 = 400 $800,000

November…………….. 400 75 75 400 $800,000

December…………….. 400 25 25 400 $800,000

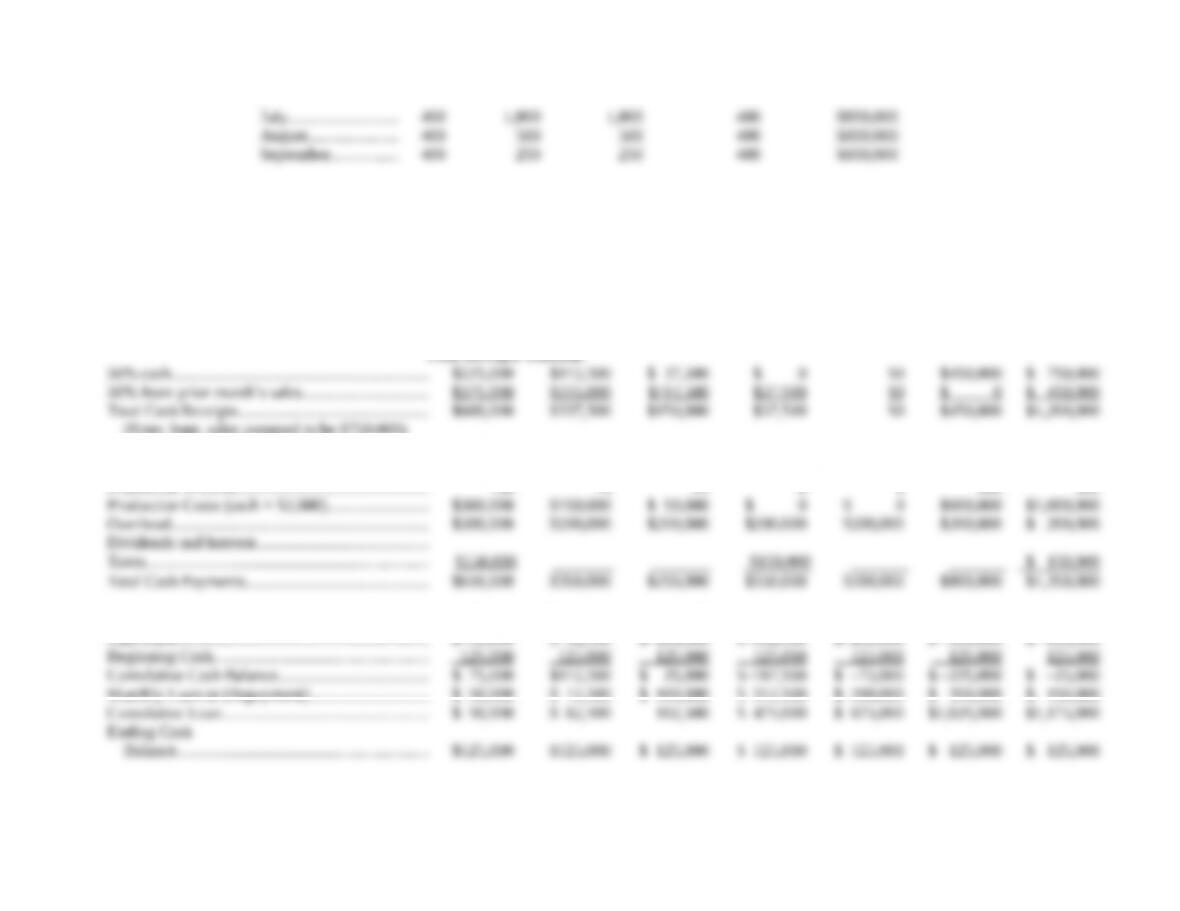

TABLE 3. SALES FORECAST, CASH RECEIPTS AND PAYMENTS, AND CASH BUDGET

October November December January February March April

Sales Forecast

Sales (units)………………………………………………….. 150 75 25 0 0 300 500

Sales (unit price: $3,000)……………………………….. $450,000 $225,000 $75,000 $0 $0 $900,000 $1,500,000

Cash Receipts Schedule

(Note: Sept. sales assumed to be $750,000)

Cash Payments Schedule

Production in Units………………………………………… 150 75 25 0 0 300 500

Cash Budget—Required Minimum Balance is $125,000

Cash Flow…………………………………………………….. $–50,000 $–12,500 $–100,000 $–312,500 $–200,000 $ –350,000 $ –150,000

Monthly Loan or (Repayment)……………………….. $ 50,000 $ 12,500 $ 100,000 $ 312,500 $ 200,000 $ 350,000 $ 150,000

Ending Cash

TABLE 3. (Continued) SALES FORECAST, CASH RECEIPTS AND PAYMENTS, AND CASH BUDGET

May June July August September

Sales Forecast

Sales (units)…………………………………………………………………………………………. 1,000 1,000 1,000 500 250

Sales (unit price: $3,000)………………………………………………………………………. $3,000,000 $3,000,000 $3,000,000 $1,500,000 $750,000

Cash Receipts Schedule

(Note: Sept. sales assumed to be $750,000)

Cash Payments Schedule

Production in Units……………………………………………………………………………….. 1,000 1,000 1,000 500 250

Cash Budget—Required Minimum Balance is $125,000

Cash Flow……………………………………………………………………………………………. $ 50,000 $ 800,000 $ 500,000 $ 50,000 $ 425,000

Beginning Cash……………………………………………………………………………………. 125,000 125,000 125,000 300,000 350,000

Cumulative Cash Balance……………………………………………………………………… 175,000 925,000 625,000 350,000 775,000

TABLE 4. TOTAL CURRENT ASSETS, FIRST YEAR

Cash

Accounts*

Receivable Inventory

Total

Current

Assets

October………………… $125,000 + $ 225,000 + $800,000 = $1,150,000

November…………….. $125,000 $ 112,500 $800,000 $1,037,500

December…………….. $125,000 $ 37,500 $800,000 $ 962,500

January…………………. $125,000 $ 0 $800,000 $ 925,000

*Equals 50 percent of monthly sales

TABLE 5. CUMULATIVE LOAN BALANCE AND INTEREST EXPENSE

(17% per month)

October Novembe

r

Decembe

r

January February March April

Cumulative

(Prime, 8.0%, + 4.0%)

Total Interest Expense for the Year: $50,750