Questions

1. Interest Income. How can gross interest income rise, while the net interest margin remains somewhat

stable for a particular bank?

ANSWER: Gross expenses may rise during periods in which gross interest income rises, as both

2. Impact on Income. If a bank shifts its loan policy to pursue more credit card loans, how will its net

interest margin be affected?

ANSWER: If the customers repay their loans, the net interest margin will increase. However, if many

3. Noninterest Income. What has been the trend in noninterest income in recent years? Explain.

ANSWER: Noninterest income increased during the 1990s, as banks were providing more financial

4. Net Interest Margin. How could a bank generate higher income before tax (as a percentage of

assets) when its net interest margin has decreased?

ANSWER: Even if the net interest margin decreased, a bank could generate higher before-tax income

5. Net Interest Income. Suppose the net income generated by a bank is equal to 1.5 percent of assets.

Based on past experience, would the bank experience a loss or a gain? Explain.

ANSWER: This bank would experience a loss, because even though the bank will also have some

6. Noninterest Income. Why have large money center banks’ noninterest income levels typically been

higher than those of smaller banks?

7. Bank Leverage. What does the assets/equity ratio of a bank indicate?

ANSWER: A bank’s assets/equity ratio is a measure of financial leverage, because it indicates how

8. Analysis of a Bank’s ROA. What are some of the more common reasons for a bank to experience a

low ROA?

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Chapter 20: Bank Performance 2

9. Loan Loss Provisions. Explain why loan loss provisions of most banks could increase in a particular

period.

10. Bank Performance During the Credit Crisis. Why do you think some banks suffered larger losses

during the credit crisis than other banks?

11. Weak Performance. What are likely reasons for weak bank performance?

ANSWER: Weak performance may be due to:

12. Bank Income Statement. Assume that SUNY Bank plans to liquidate Treasury security holdings and

use the proceeds for small business loans. Explain how this strategy will affect the different income

statement items. Also identify any income statement items for which the effects of this strategy are

more difficult to estimate.

ANSWER: Gross interest income would be expected to increase because small business loans

generate higher interest revenues (assuming the loans are repaid). Noninterest expenses may increase

Interpreting Financial News

Interpret the following statements made by Wall Street analysts and portfolio managers.

a. “The three most important factors that determine a local bank’s bad debt level are the bank’s

location, location, and location.”

The bad debt level of a local bank is very susceptible to economic conditions within the local

b. “The bank’s profitability was enhanced by its limited use of capital.”

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Chapter 20: Bank Performance 3

c. “Low risk is not always desirable. Our bank’s risk has been too low, given the market conditions.

We will restructure operations in a manner to increase risk.”

The bank expects that the economy will be strong, so it can make more loans to customers that

Managing in Financial Markets

As a manager of Hawaii Bank, you anticipate the following information provided to you:

Loan loss reserves at end of year = 1 percent of assets

Gross interest income over the next year = 9 percent of assets

Noninterest expenses over the next year = 3 percent of assets

Noninterest income over the next year = 1 percent of assets

Gross interest expenses over the next year = 5 percent of assets

Tax rate on income = 30 percent

Capital ratio (capital/assets) at end of year = 5 percent

a. Forecast Hawaii Bank’s net interest margin.

b. Forecast Hawaii Bank’s earnings before taxes as a percentage of assets.

c. Forecast Hawaii Bank’s earnings after taxes as a percentage of assets.

d. Forecast Hawaii Bank’s return on equity.

Return on equity = ROA (Assets/Capital)

e. Hawaii Bank is considering a shift in its asset structure to reduce its concentration of Treasury

bonds and increase its volume of loans to small businesses. Identify each income statement item

that would be affected by this strategy, and explain whether the forecast for that item would

increase or decrease as a result.

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Chapter 20: Bank Performance 4

Gross interest income is now expected to be higher. Noninterest expenses are now expected to be

higher because of increased efforts on loan evaluation. Loan losses are expected to be higher.

Amount as a Percent of Assets

Gross interest income 9%

Gross interest expense – 5 %

Problems

1. Assessing Bank Performance. Select a bank whose income statement data are available. Using

recent income statement data about a commercial bank, assess its performance. How does the

performance of this bank compare to the performance of other banks? Compared with other banks, is

its return on equity higher or lower than the ROE of other banks as reported in this chapter? What is

the main reason why its ROE is different from the norm? (Is it due to its interest expenses? Its

noninterest income?)

Flow of Funds Exercise

How the Flow of Funds Affects Bank Performance

In recent years, Carson Company has requested the services listed below from Blazo Financial, a financial

conglomerate. These transactions have created a flow of funds between Carson Company and Blazo.

a. Classify each service according to how Blazo benefits from the service.

advising on possible targets that Carson may acquire,

futures contract transactions,

options contract transactions,

interest rate derivative transactions,

loans,

line of credit,

purchase of short-term CDs,

checking account.

All the services except for the purchase of short-term CDs may generate fees for Blazo Financial,

and therefore generates non-interest income. Second, Blazo incurs an interest expense on the CD,

but it channels the funds into loans or investments that pay interest income. Third, Blazo’s loans

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Chapter 20: Bank Performance 5

b. Explain why Blazo’s performance from providing these services to Carson Company and other

firms will decline if economic growth is reduced.

If economic growth is reduced, the demand for advisory services, because there are less

c. Given the potential impact of slow economic growth on a bank’s performance, do you think

that commercial banks would prefer that the Fed use a restrictive monetary policy or an

expansionary monetary policy?

Solution to Integrative Problem for Part IV

Forecasting Bank Performance

1. The interest income and expenses are determined by applying the specified interest rate on each asset

and liability to the dollar amount for each Treasury bill rate scenario. The loan losses must be

deducted from the loan amounts before determining the interest income on loans.

The noninterest income and expenses were given in the question. The loan losses are determined by

applying the assumed loan loss percentage to the dollar amount of each type of loan. The ROA for

each of the three Treasury bill rate scenarios is derived in the following table:

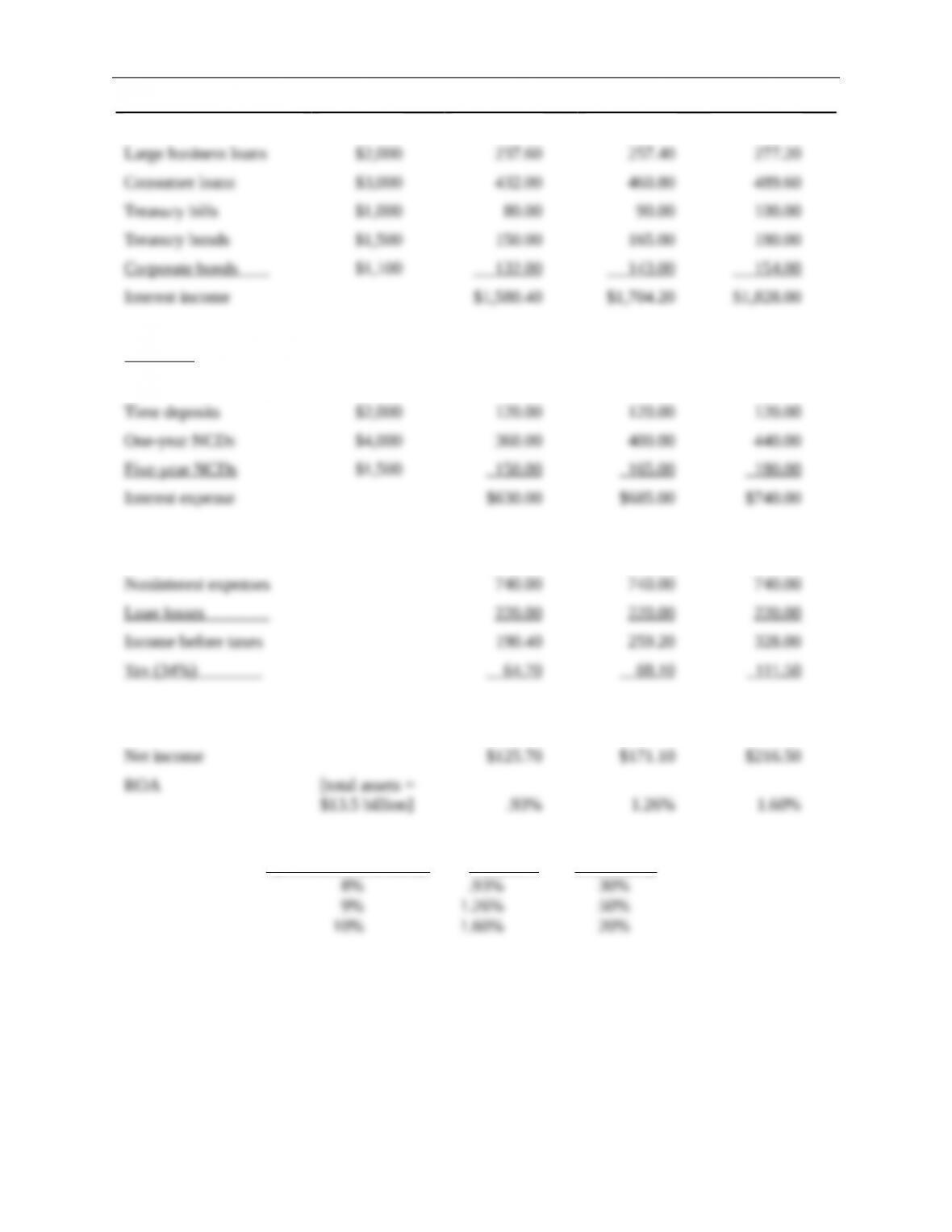

Income and Expenses (in millions) Based on Treasury Bill Rate Scenarios

Possible Treasury Bill Rate

Assets

Amount in

Millions 8% 9% 10%

Small business loans $4,000 548.80 588.00 627.20

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Chapter 20: Bank Performance 6

Liabilities

Demand deposits $5,000 0 0 0

Noninterest income 200.00 200.00 200.00

Interest Rate Scenario Forecasted

(Possible T-bill Rate) ROA Probability

2. Next year’s ROA will be higher if interest rates are higher as of the beginning of the year.

Much of the bank’s sources of funds (from its demand deposits and time deposits) are insensitive to

3. The two NCD expense items change, allowing for slightly lower total interest expenses and therefore

a slightly higher ROA, as shown in the following table:

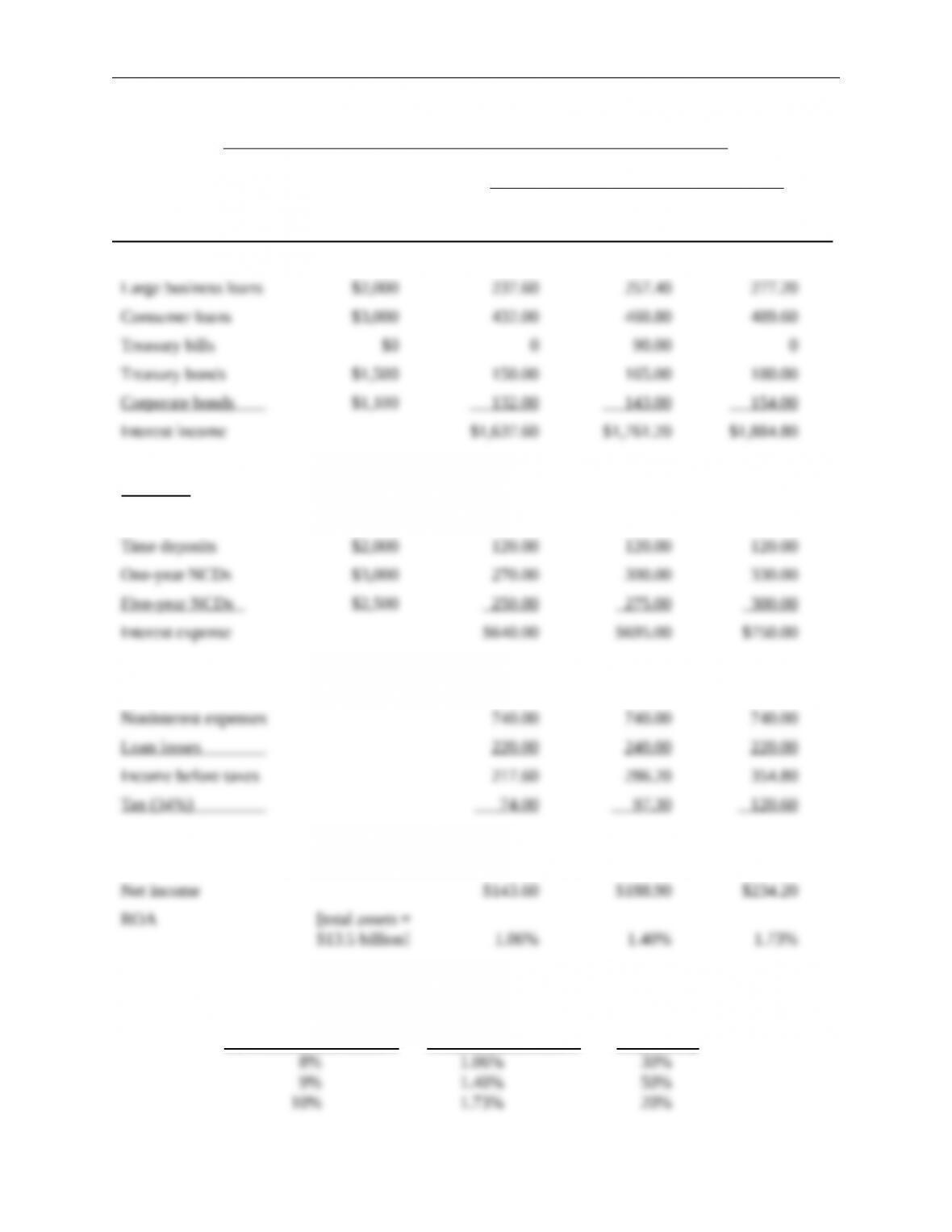

Income and Expenses (in millions) Based on Treasury Bill Rate Scenarios

Possible Treasury Bill Rate

Assets

Amount in

Millions 8% 9% 10%

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Chapter 20: Bank Performance 7

Small business loans $4,000 548.80 588.00 627.20

Liabilities

Demand deposits $5,000 0 0 0

Noninterest income 200.00 200.00 200.00

Interest Rate Scenario Forecasted

(Possible T-bill Rate) ROA Probability

4. Higher.

5. If interest rates rise over time, the interest paid on one-year NCDs will rise while the interest paid on

five-year NCDs issued in previous years is unaffected.

6. The interest income and loan losses are affected because of the change in the asset composition. The

new levels are shown in the following table. The total loan loss amount is increased by $20 million

because of the increased allocation of small business loans.

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Chapter 20: Bank Performance 8

Income and Expenses (in millions) Based on Treasury Bill Rate Scenarios

Possible Treasury Bill Rate

Assets

Amount in

Millions 8% 9% 10%

Small business loans $5,000 686.00 735.00 784.00

Liabilities

Demand deposits $5,000 0 0 0

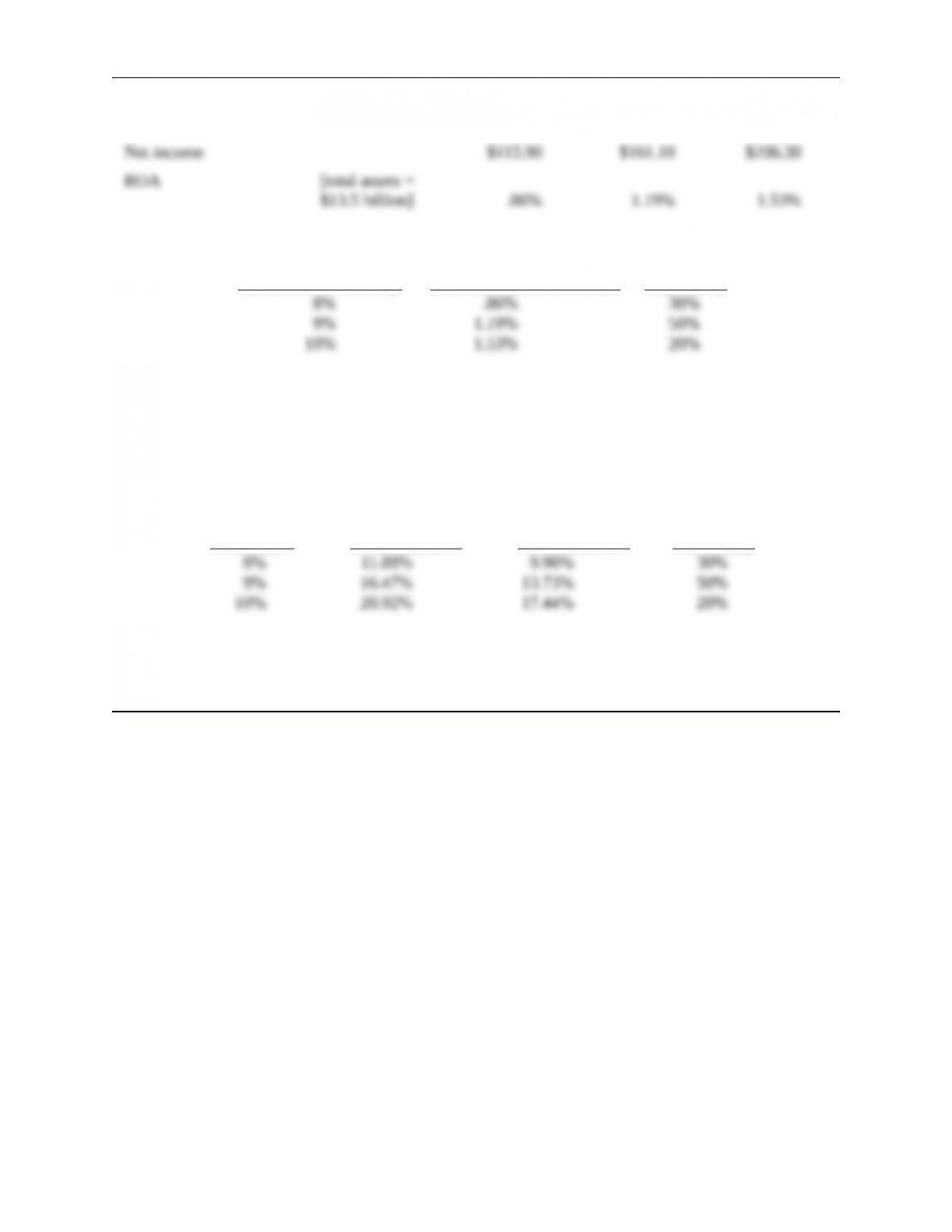

Noninterest income 200.00 200.00 200.00

Forecasted ROA if an

Extra $1 Billion is

Interest Rate Scenario Used for Loans to

(Possible T-bill Rate) Small Businesses Probability

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Chapter 20: Bank Performance 9

8. The default rate on consumer loans may increase in the following years, causing the bank’s ROA to

be lower with the extra consumer loans than it would have been if it purchased Treasury bills.

10. The interest income is higher as a result of the increased allocation of consumer loans, but loan losses

Income and Expenses (in millions) Based on Treasury Bill Rate Scenarios

Possible Treasury Bill Rate

Assets

Amount in

Millions 8% 9% 10%

Small business loans $4,000 548.80 588.00 627.20

Liabilities

Demand deposits $5,000 0 0 0

Noninterest income 200.00 200.00 200.00

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Chapter 20: Bank Performance 10

Possible ROA if an

Interest Rate Scenario Extra $1 Billion is

(Possible T-bill Rate) Used for Consumer Loans Probability

11. If interest rates rise after the loans are provided, the interest received on consumer loans will be

unaffected, while the interest received on business loans would rise (because their rates are tied to the

T-bill rate). In this case, the consumer loans would not perform as well as the business loans.

12. Interest Rate

Scenario Forecasted ROE Forecasted ROE

(Possible T- if Capital = if Capital =

bill Rate $1 Billion $1.2 Billion Probability

The ROE will be lower if the capital level is increased.

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.