Questions

1. Integrating Asset and Liability Management. What is accomplished when a bank integrates its

liability management with its asset management?

ANSWER: Integrating asset and liability decisions can improve performance. For example, the

2. Liquidity. Given the liquidity advantage of holding Treasury bills, why do banks hold only a

relatively small portion of their assets as T-bills?

ANSWER: Treasury bill yields are sometimes lower than a bank’s cost of obtaining funds. Thus,

3. Illiquidity. How do banks resolve illiquidity problems?

ANSWER: Banks can resolve illiquidity by selling some assets to obtain funds, or borrowing funds in

4. Managing Interest Rate Risk. If a bank expects interest rates to decrease over time, how might it

alter the rate sensitivity of its assets and liabilities?

5. Rate Sensitivity. List some rate-sensitive assets and some rate-insensitive assets of banks.

6. Managing Interest Rate Risk. If a bank is very uncertain about future interest rates, how might it

insulate its future performance from future interest rate movements?

7. Net Interest Margin. What is the formula for the net interest margin? Explain why it is closely

monitored by banks.

Net interest margin

=

Interest revenue

–

Interest expenses

Assets

8. Managing Interest Rate Risk. Assume that a bank expects to attract most of its funds through

short-term CDs and would prefer to use most of its funds to provide long-term loans. How could it

follow this strategy and still reduce interest rate risk?

9. Bank Exposure to Interest Rate Movements. According to this chapter, have banks been able to

insulate themselves against interest rate movements? Explain.

ANSWER: Banks can attempt to minimize their exposure to interest rate risk because they have the

10. Gap Management. What is a bank’s gap, and what does it attempt to determine? Interpret a negative

gap. What are some limitations of measuring a bank’s gap?

ANSWER: A bank gap is measured to determine its exposure to interest rate risk. A negative gap

Value of Value of

11. Duration. How do banks use duration analysis?

12. Measuring Interest Rate Risk. Why do loans that can be prepaid on a moment’s notice complicate

the bank’s assessment of interest rate risk?

ANSWER: A fixed-rate loan may be perceived as rate insensitive. Yet, if it is prepaid, the funds are

13. Bank Management Dilemma. Can a bank simultaneously maximize return and minimize default

risk? If not, what can it do instead?

ANSWER: Banks cannot maximize return unless they incur some default risk, so they must balance

the risk and return objectives, based on their degree of risk aversion.

14. Bank Exposure to Economic Conditions. As economic conditions change, how do banks adjust

their asset portfolio?

ANSWER: Expectations of a stronger economy may encourage banks to provide more risky loans,

15. Bank Loan Diversification. In what two ways should a bank diversify its loans? Why? Is

international diversification of loans a viable strategy for dealing with credit risk? Defend your

answer.

ANSWER: Banks should diversify across geographic regions and industries, to reduce exposure to

Not necessarily. If the countries receiving loans tend to experience similar business cycles,

16. Commercial Borrowing. Do all commercial borrowers receive the same interest rate on loans?

17. Bank Dividend Policy. Why might a bank retain some excess earnings rather than distribute them as

dividends?

18. Managing Interest Rate Risk. If a bank has more rate-sensitive liabilities than rate-sensitive assets,

what will happen to its net interest margin during a period of rising interest rates? During a period of

declining interest rates?

19. Floating-Rate Loans. Does the use of floating-rate loans eliminate interest rate risk? Explain.

20. Managing Exchange Rate Risk. Explain how banks become exposed to exchange rate risk.

ANSWER: When banks accept deposits in one currency and provide loans in a different currency,

Advanced Questions

21. Bank Exposure to Interest Rate Risk. Oregon Bank has branches overseas that concentrate in

short-term deposits in dollars and floating-rate loans in British pounds. Because it maintains

rate-sensitive assets and liabilities of equal amounts, it believes it has essentially eliminated its

interest rate risk. Do you agree? Explain.

ANSWER: U.S. interest rates will not necessarily move in tandem with British interest rates, thus, it

22. Managing Interest Rate Risk. Dakota Bank has a branch overseas with the following balance sheet

characteristics: 50 percent of the liabilities are rate sensitive and denominated in Swiss francs; the

remaining 50 percent of liabilities are rate insensitive and are denominated in dollars. With regard to

assets, 50 percent are rate-sensitive and are denominated in dollars; the remaining 50 percent of assets

are rate-insensitive and are denominated in Swiss francs.

a. Is the performance of this branch susceptible to interest rate movements? Explain.

ANSWER: Dakota Bank is susceptible to interest rate movements. If Swiss interest rates rise, the

b. Assume that Dakota Bank plans to replace its short-term deposits denominated in U.S. dollars

with short-term deposits denominated in Swiss francs, because Swiss interest rates are currently

lower than U.S. interest rates. The asset composition would not change. This strategy is intended

to widen the spread between the rate earned on assets and the rate paid on liabilities. Offer your

insight on how this strategy could backfire.

ANSWER: The strategy could backfire if the Swiss franc appreciates against the dollar over time,

c. One consultant has suggested to Dakota Bank that it could avoid exchange rate risk by making

loans in whatever currencies it receives as deposits. In this way, it will not have to exchange one

currency for another. Offer your insight on whether there are any disadvantages to this strategy.

ANSWER: One disadvantage is that the bank may not be able to satisfy some potential borrowers

Interpreting Financial News

Interpret the following statements made by Wall Street analysts and portfolio managers.

a. “The bank’s biggest mistake was that it did not recognize that its forecast of a strong local real

estate market and declining interest rates could be wrong.”

The bank apparently tried to capitalize on expectations of a strong real estate market by

b. “Banks still need some degree of interest rate risk to be profitable.”

If banks attempted to perfectly match the maturities of the liabilities with maturities of their

assets, the interest rate spread might not be sufficient to cover their own expenses. Thus, they can

c. “The bank used interest rate swaps so that its spread is no longer exposed to interest rate

movements. However, its loan volume and therefore its profits are still exposed to interest rate

movements.”

Managing in Financial Markets

As a manager of Stetson Bank, you are responsible for hedging Stetson’s interest rate risk. Stetson has

forecasted its cost of funds as follows:

Year Cost of Funds

1 6%

2 5%

3 7%

4 9%

5 7%

It expects to earn an average rate of 11 percent on some assets that charge a fixed interest rate over the

next five years. It considers engaging in an interest rate swap in which it would swap fixed payments of

10 percent in exchange for variable-rate payments of LIBOR + 1 percent. Assume LIBOR is expected to

be consistently 1 percent above Stetson’s cost of funds.

a. Determine the spread that would be earned each year if Stetson uses an interest rate swap to

hedge all of its interest rate risk. Would you recommend that Stetson use an interest rate swap?

Stetson’s overall spread is derived as follows:

Year 1 Year 2 Year 3 Year 4 Year 5

Average rate earned

on assets 11% 11% 11% 11% 11%

Stetson should not use an interest rate swap because its expected spread is more favorable in

most years if it does not hedge.

b. Although Stetson has forecasted its cost of funds, it recognizes that its forecasts may be

inaccurate. Offer a method that Stetson can use to assess the potential results from using an

interest rate swap while accounting for the uncertainty surrounding future interest rates.

c. The reason for Stetson’s interest rate risk is that it uses some of its funds to make fixed-rate loans,

as some borrowers prefer fixed rates. An alternative method of hedging interest rate risk is to use

adjustable-rate loans. Would you recommend that Stetson use only adjustable-rate loans to hedge

its interest rate risk? Explain.

.

Problems

1. Net Interest Margin. Suppose a bank earns $201 million in interest revenue but pays $156 million in

interest expense. It also has $800 million in earning assets. What is its net interest margin?

ANSWER:

Net interest margin =

Interest revenues – Interest expenses

Assets

$201 million – $156 million

$800 million

5.625%

2. Calculating Return on Assets. If a bank earns $169 million net profit after tax and has $17 billion

invested in assets, what is its return on assets?

ANSWER:

ROA

=

Net profit after taxes

Total assets

$169 million

$17 billion

.

%

99

3. Calculating Return on Equity. If a bank earns $75 million net profits after tax and has $7.5 billion

invested in assets and $600 million equity investment, what is its return on equity?

ANSWER:

ROE

=

Net profit after tax

Equity

$75,000,000

$600,000,000

12.5%

4. Managing Risk. Use the balance sheet for San Diego Bank in Exhibit A (below and next page) and

the industry norms in Exhibit B (page following Exhibit A) to answer the following questions:

a. Estimate the gap and determine how San Diego Bank would be affected by an increase in interest

rates over time.

ANSWER:

Gap = Rate-sensitive assets – Rate-sensitive liabilities

The bank would be adversely affected by rising interest rates.

b. Assess San Diego Bank’s credit risk. Does it appear high or low relative to the industry? Would

San Diego Bank perform better or worse than other banks during a recession?

c. For any type of bank risk that appears to be higher than the industry, explain how the balance

sheet could be restructured to reduce the risk.

ANSWER: The bank could reduce its interest rate risk by using floating-rate loans and by trying to

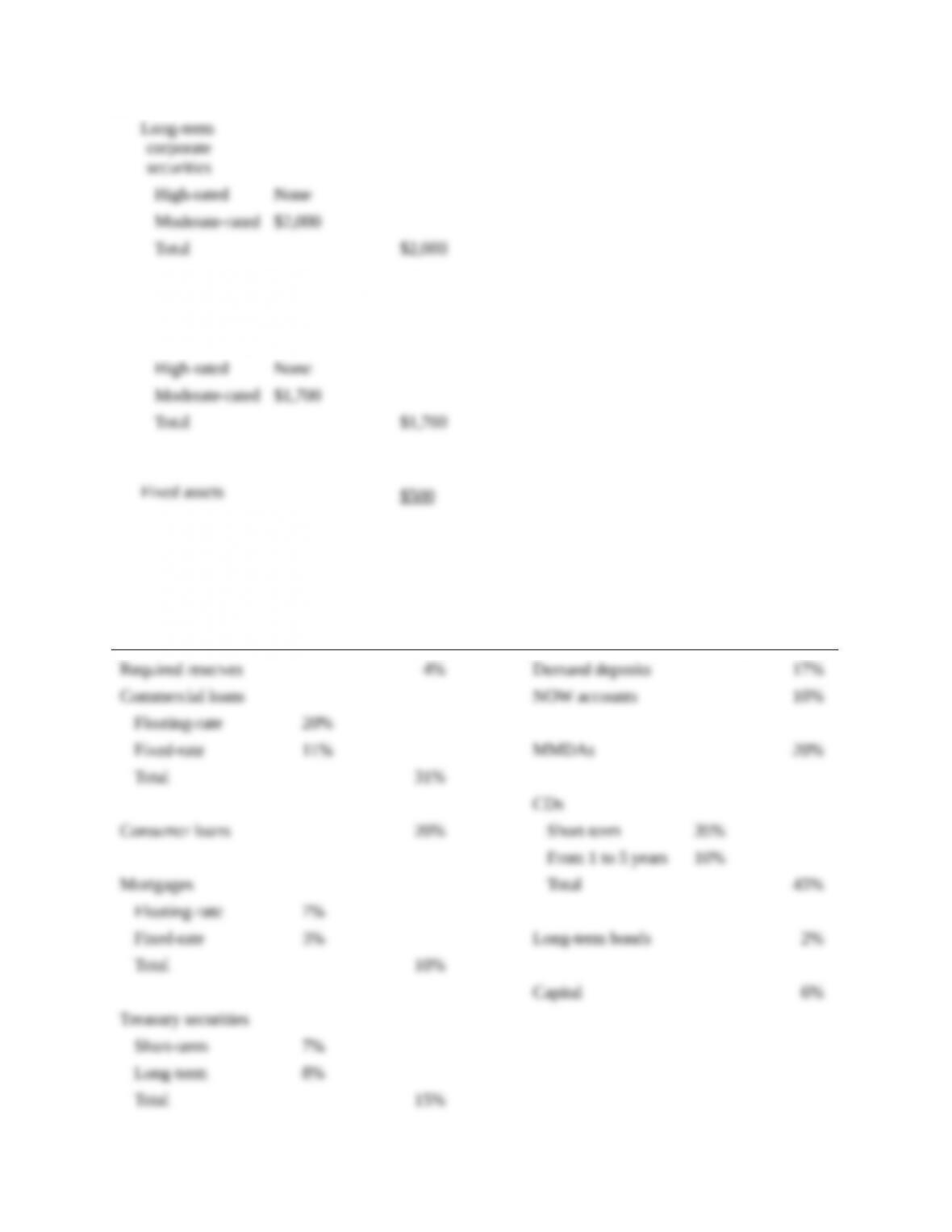

Exhibit A: Balance Sheet for San Diego Bank

(in Millions of Dollars)

Assets Liabilities and Capital

Required

reserves

$800 Demand deposits $800

Long-term

municipal

securities

TOTAL ASSETS $20,000

TOTAL LIABILITIES

AND CAPITAL $20,000

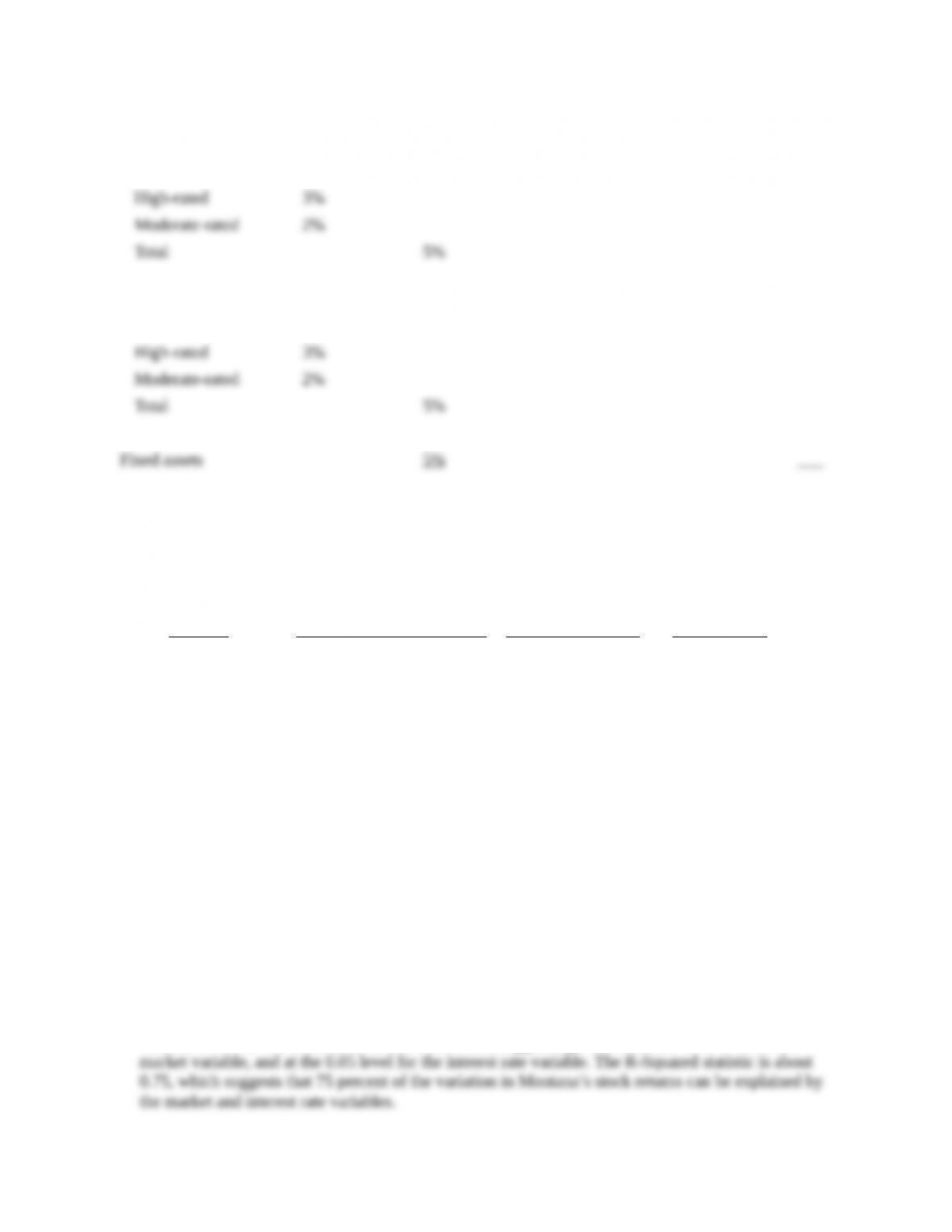

Exhibit B: Industry Norms in Percentage Terms

Assets Liabilities and Capital

Long-term corporate

securities

Long-term municipal

securities

TOTAL ASSETS 100%

TOTAL LIABILITIES

AND CAPITAL 100%

5. Measuring Risk. Montana Bank wants to determine the sensitivity of its stock returns to interest rate

movements, based on the following information:

Quarter Return on Montana Stock Return on Market Interest Rate

1 2% 3% 6.0%

2 2 2 7.5

3 –1 –2 9.0

4 0 –1 8.2

5 2 1 7.3

6 –3 –4 8.1

7 1 5 7.4

8 0 1 9.1

9 –2 0 8.2

10 1 –1 7.1

11 3 3 6.4

12 6 4 5.5

Use a regression model in which Montana’s stock return is a function of the stock market return and

the interest rate. Determine the relationship between the interest rate and Montana’s stock return by

assessing the regression coefficient applied to the interest rate. Is the sign of the coefficient positive or

negative? What does it suggest about the bank’s exposure to interest rate risk? Should Montana Bank

be concerned about rising or declining interest rate movements in the future?

ANSWER: The coefficient for the market variable is 0.38, while the coefficient for the interest rate

variable is –1.15. The t-statistics for the coefficients suggest significance at the 0.10 level for the

Flow of Funds Exercise

Managing Credit Risk

Recall that Carson Company relies heavily on commercial banks for loans. When the company was first

established with equity funding from its owners, Carson Company could easily obtain debt financing,

because the financing was backed by some of the firm’s assets. However, as Carson expanded, it

continually relied on extra debt financing, which increased its ratio of debt to equity. Some banks were

unwilling to provide more debt financing because of the risk that Carson would not be able to repay

additional loans. A few banks were still willing to provide funding, but they required an extra premium to

compensate for the risk.

a. Explain the difference in the willingness of banks to provide loans to Carson Company. Why

is there a difference between banks when they are assessing the same information about a firm

that wants to borrow funds?

First, some banks may be more optimistic about economic conditions than other banks, and

therefore expect that the strong economy will generate more sales for the firm in the future.

b. Consider the flow of funds for a publicly traded bank that is a key lender to Carson Company.

This bank received equity funding from shareholders, which it uses to establish its business. It

channels bank deposit funds, which are insured by the FDIC, to provide loans to Carson

Company and other firms. The depositors have no idea how the bank uses their funds. Yet, the

FDIC does not prevent the bank from making risky loans. So who is monitoring the bank? Do

you think the bank is taking more risk than its shareholders desire? How does the FDIC

discourage the bank from taking too much risk? Why might the bank ignore the FDIC’s efforts to

discourage excessive risk taking?

The bank is monitored by its shareholders. It is probably taking the risk that is desired by its

shareholders. Yet, the FDIC may need to intervene if the bank experiences financial problems.