Questions

1. Hedging with Interest Rate Swaps. Bowling Green Savings & Loan uses short-term deposits to

fund fixed-rate mortgages. Explain how Bowling Green can use interest rate swaps to hedge its

interest rate risk.

ANSWER: Bowling Green could engage in a fixed-for-floating swap. If interest rates rise, its inflow

2. Decision to Hedge with Interest Rate Swaps. Explain the types of cash flow characteristics that

would cause a firm to hedge interest rate risk by swapping floating-rate payments for fixed payments.

Why would some firms avoid the use of interest rate swaps, even when they are highly exposed to

interest rate risk?

ANSWER: Interest rate swaps can possibly reduce potential returns. Consider a savings institution

that uses short-term deposits to finance fixed-rate mortgages. This institution will typically experience

3. Role of Securities Firms in Swap Market. Describe the possible roles of securities firms in the swap

market.

ANSWER: Securities firms can act as an intermediary by matching up firms that have opposite swap

If a firm’s business resulted in fixed-rate outflows and floating-rate inflows, it would be adversely

4. Hedging with Swaps. Chelsea Finance Company receives floating inflow payments from its

provision of floating-rate loans. Its outflow payments are fixed because of its recent issuance of

long-term bonds. Chelsea is concerned that interest rates will decline in the future. Yet, it does not

want to hedge its interest rate risk, because it believes interest rates may increase. Recommend a

solution to Chelsea’s dilemma.

ANSWER: Chelsea could negotiate a putable swap, which represents a floating payment in exchange

5. Basis Risk. Comiskey Savings provides fixed-rate mortgages of various maturities, depending on

what customers want. It obtains most of its funds from issuing certificates of deposit with maturities

ranging from one month to five years. Comiskey has decided to engage in a fixed-for-floating swap to

hedge its interest rate risk. Is Comiskey exposed to basis risk?

ANSWER: Yes. Comiskey’s liabilities are more rate-sensitive than its assets, but it is difficult to

6. Fixed-for-Floating Swaps. Shea Savings negotiates a fixed-for-floating swap with a reputable firm in

South America that has an exceptional credit rating. Shea is very confident that there will not be a

default on inflow payments because of the very low credit risk of the South American firm. Do you

agree? Explain.

7. Fixed-for-Floating Swaps. North Pier Company entered into a two-year swap agreement, which

would provide fixed-rate payments for floating-rate payments. Over the next two years, interest rates

declined. Based on these conditions, did North Pier Company benefit from the swap?

8. Equity Swap. Explain how an equity swap could allow Marathon Insurance Company to capitalize

on expectations of a strong stock market performance over the next year without altering its existing

portfolio mix of stocks and bonds.

ANSWER: An equity swap involves the exchange of interest payments (based on a specified interest

rate) for payments linked to the degree of change in a stock index. Marathon Insurance Company

9. Swap Network. Explain how the failure of a large commercial bank could cause a worldwide swap

credit crisis.

ANSWER: Assume the commercial bank has taken positions in numerous swaps and guaranteed

payments on other swaps. As it fails, it will default on its swap payments. The counterparties of these

10. Currency Swaps. Markus Company purchases supplies from France once a year. Would Markus be

favorably affected if it establishes a currency swap arrangement and the dollar strengthens? What if it

establishes a currency swap arrangement and the dollar weakens?

ANSWER: Markus could engage in a currency swap arrangement in which it agrees to swap dollars

11. Basis Risk. Explain basis risk as it relates to a currency swap.

ANSWER: Basis risk would reflect the hedging of a position in a foreign currency with a swap in a

12. Sovereign Risk. Give an example of how sovereign risk is related to currency swaps.

ANSWER: An example of sovereign risk is that the government of a country could suspend the

13. Use of Interest Rate Swaps. Explain why some companies that issue bonds engage in interest rate

swaps in financial markets. Why do they not simply issue bonds that require the type of payments

(fixed or variable) that they prefer to make?

ANSWER: In some cases, the premium paid by a risky firm when issuing fixed-rate bonds may be

higher than if it issues variable-rate bonds. Thus, it may prefer to issue variable-rate bonds even if it

14. Use of Currency Swaps. Explain why some companies that issue bonds engage in currency swaps.

Why do they not simply issue bonds in the currency that they would prefer to use for making

payments?

ANSWER: Companies may not be well known in the country where the bonds denominated in a

particular currency could most easily be placed. Therefore, they may issue bonds in a different

Advanced Questions

15. Rate-Capped Swaps. Bull and Finch Company wants a fixed-for-floating swap. It expects interest

rates to rise far above the fixed rate that it would pay and remain very high until the swap maturity

date. Should it consider negotiating for a rate-capped swap with the cap set at two percentage points

above the fixed rate? Explain.

ANSWER: Bull and Finch should not consider the rate-capped swap because it would restrict the

16. Forward Swaps. Rider Company negotiates a forward swap to begin two years from now, in which it

will swap fixed payments for floating-rate payments. What will be the effect on Rider if interest rates

rise substantially over the next two years? That is, would Rider be better off by using this forward

swap than if it had simply waited two years before negotiating the swap? Explain.

ANSWER: Rider would have been better off with the forward swap, because the fixed rate specified

in the forward swap would be lower than the fixed rate specified two years later (since the fixed rate

17. Swap Options. Explain the advantage of a swap option to a financial institution that wants to swap

fixed payments for floating payments.

ANSWER: A swap option would allow the financial institution to terminate the swap arrangement

18. Callable Swaps. Back Bay Insurance Company negotiated a callable swap involving fixed payments

in exchange for floating payments. Assume that interest rates decline consistently up until the swap

maturity date. Do you think Back Bay might terminate the swap prior to maturity? Explain.

19. Credit Default Swaps. Credit default swaps were once viewed as a great innovation for making

mortgage markets more stable. Yet, the swaps were sometimes criticized for making the credit crisis

worse. Why?

ANSWER: Credit default swaps protect securities against default, but the protection is only as strong

as the seller of the swaps. Some financial institutions that sold credit default swaps were subject to

20. Credit Default Swap Prices. Explain why the failures of Lehman Brothers caused prices

on credit default swap contracts to increase.

ANSWER: The credit crisis illustrated how protection provided to buyers of a CDS is only as

good as the creditworthiness of the CDS seller. Participants recognized that the government

21. Reform of CDS Contracts. Explain how the Financial Reform Act of 2010 attempted

to reduce the risk in the financial system resulting from the use of credit default swaps.

ANSWER: As a result of the Financial Reform Act of 2010, derivative securities such as

swaps are to be traded on an exchange or clearinghouse. One obvious result of having

Interpreting Financial News

Interpret the following statements made by Wall Street analysts and portfolio managers.

a. “The swaps market is another Wall Street-developed house of cards.”

There is a concern that the swaps market could overexpose some banks so if swap arrangements

b. “As a dealer in interest rate swaps, our bank takes various steps to limit our exposure.”

Any provisions that could force clients to meet their swap obligations would help protect banks.

c. “The regulation of commercial banks, securities firms, and other financial institutions that

participate in the swaps market could create a regulatory war.”

Managing in Financial Markets

As a manager of a commercial bank, you have just purchased a three-year interest rate collar, with LIBOR

as the interest rate index. The interest rate cap specifies a fee of 2 percent of notional principal valued at

$100 million and an interest rate ceiling of 9 percent. The interest rate floor specifies a fee of 3 percent of

the $100 million notional principal and an interest rate floor of 7 percent. Assume that LIBOR is expected

to be 6 percent, 10 percent, and 11 percent, respectively, at the end of each of the next three years.

a. Determine the net fees paid, and also determine the expected net payments to be received as a

result of purchasing the interest rate collar.

The net payments are derived as follows:

End of Year:

0 1 2 3

LIBOR 6% 10% 11%

Purchase of

Interest Rate

Sale of Interest

Rate Floor:

Interest Rate

Floor 7% 7% 7%

LIBOR’s

Percentage

Points Below

b. Assuming you are very confident that interest rates will rise, should you consider purchasing a

callable swap instead of the collar? Explain.

The interest collar is most appropriate if you are confident that interest rates will rise. The

callable swap allows you flexibility to terminate the swap agreement in the event that interest

c. Explain the conditions under which your purchase of an interest rate collar could backfire.

If interest rates decline rather than rise, you will not receive any payments on the interest rate

Problems

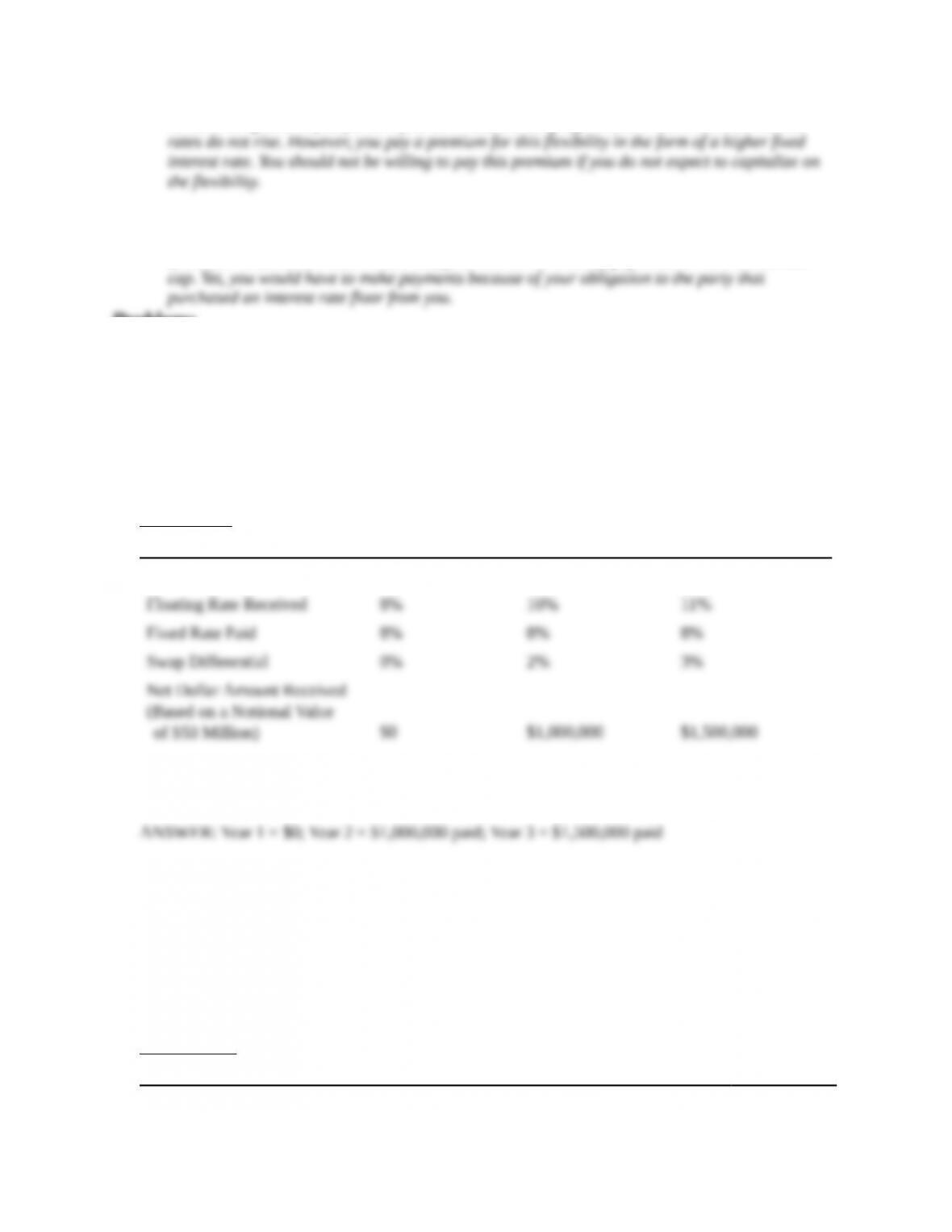

1. Vanilla Swaps. Cleveland Insurance Company has just negotiated a three-year plain vanilla swap in

which it will exchange fixed payments of 8 percent for floating payments of LIBOR + 1 percent. The

notional principal is $50 million. LIBOR is expected to 7 percent, 9 percent, and 10 percent,

respectively, at the end of each of the next three years.

a. Determine the net dollar amount to be received (or paid) by Cleveland each year.

ANSWER:

End of Year:

1 2 3

LIBOR 7% 9% 10%

b. Determine the dollar amount to be received (or paid) by the counterparty on this interest rate

swap each year based on the assumed forecasts of LIBOR.

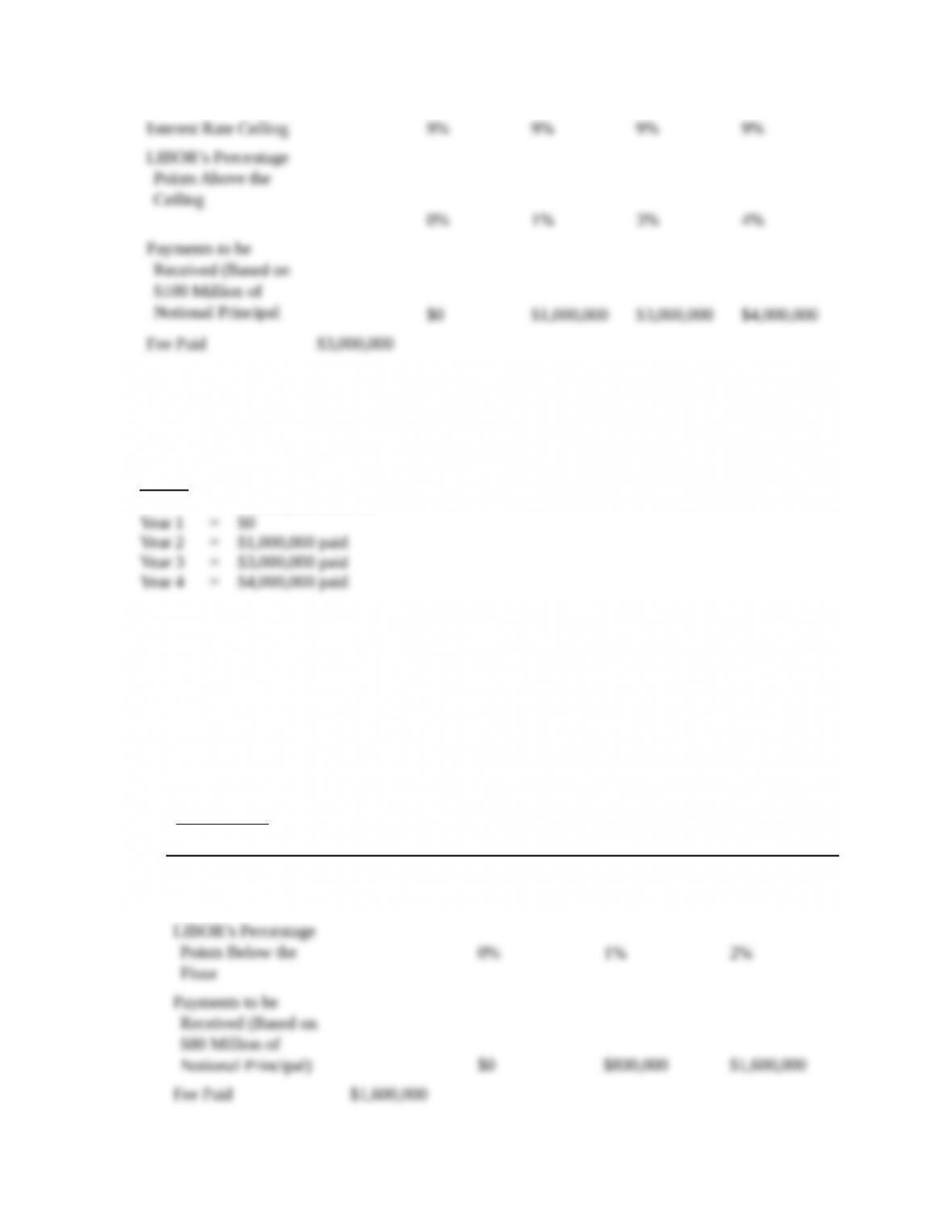

2. Interest Rate Caps. Northbrook Bank purchases a four-year cap for a fee of 3 percent of notional

principal valued at $100 million, with an interest rate ceiling of 9 percent, and LIBOR as the index

representing the market interest rate. Assume that LIBOR is expected to be 8 percent, 10 percent, 12

percent, and 13 percent, respectively, at the end of each of the next four years.

a. Determine the initial fee paid, and also determine the expected payments to be received by

Northbrook if LIBOR moves as forecasted.

ANSWER:

End of Year:

0 1 2 3 4

LIBOR 8% 10% 12% 13%

b. Determine the dollar amount to be received (or paid) by the seller of the interest rate cap based on

the assumed forecasts of LIBOR.

ANSWER:

End of

Year 0 = $3,000,000 received

3. Interest Rate Floors. Iowa City Bank purchases a three-year interest rate floor for a fee of 2 percent

of notional principal valued at $80 million, with an interest rate floor of 6 percent, and LIBOR

representing the interest rate index. The bank expects LIBOR to be 6 percent, 5 percent, and 4 percent

respectively at the end of each of the next three years.

a. Determine the initial fee paid, and also determine the expected payments to be received by Iowa

City if LIBOR moves as forecasted.

ANSWER:

End of Year:

0 1 2 3

LIBOR 6% 5% 4%

Interest Rate Floor 6% 6% 6%

b. Determine the dollar amounts to be received (or paid) by the seller of the interest rate based on

the assumed forecasts of LIBOR.

ANSWER:

End of

Year 0 = $3,000,000 received

Flow of Funds Exercise

Hedging with Interest Rate Derivatives

Recall that if the economy continues to be strong, Carson Company may need to increase its production

capacity by about 50 percent over the next few years to satisfy demand. It would need financing to

expand and accommodate the increase in production. Recall that the yield curve is currently upward

sloping. Also recall that Carson is concerned about a possible slowing of the economy because of

potential Fed actions to reduce inflation. Carson currently relies mostly on commercial loans with floating

interest rates for its debt financing. It has contacted Blazo Bank about the use of interest rate derivatives

to hedge the risk.

a. How could Carson use interest rate swaps to reduce the exposure of its cost of debt to

interest rate movements?

Carson could engage in a swap of fixed interest rates in exchange for floating interest rates. If

b. What is a possible disadvantage of Carson using the interest rate swap hedge as opposed to no

hedge?

If interest rates decline, Carson would incur lower debt financing costs on its floating-rate loans.

c. How could Carson use an interest rate cap to reduce the exposure of its cost of debt to interest

rate movements?

Carson could purchase an interest rate cap, in which it would receive payments if market interest

d. What is a possible disadvantage of Carson using the interest cap hedge as opposed to no hedge?

If interest rates decline, Carson would still incur a cost from the interest rate cap, but would not

e. Explain the tradeoff from using an interest rate swap versus an interest rate cap.

The profit from an interest rate swap would be more closely matched to the increase in debt