31. Currency Strangles. (See Appendix B in this chapter.) Assume the following options are currently

available for British pounds (₤):

Call option premium on British pounds = $.04 per unit

Put option premium on British pounds = $.03 per unit

Call option strike price = $1.56

Put option strike price = $1.53

One option contract represents ₤31,250.

a. Construct a worksheet for a long strangle using these options.

b. Determine the break-even point(s) for a strangle.

c. If the spot price of the pound at option expiration is $1.55, what is the total profit or loss to the

strangle buyer?

d. If the spot price of the pound at option expiration is $1.50, what is the total profit or loss to the

strangle writer?

ANSWER:

a. Many different worksheets are possible, but one worksheet is shown below.

Value of Pound at Option Expiration

$1.40 $1.53 $1.56 $1.65

Call –$.04 –$.04 –$.04 +$.05

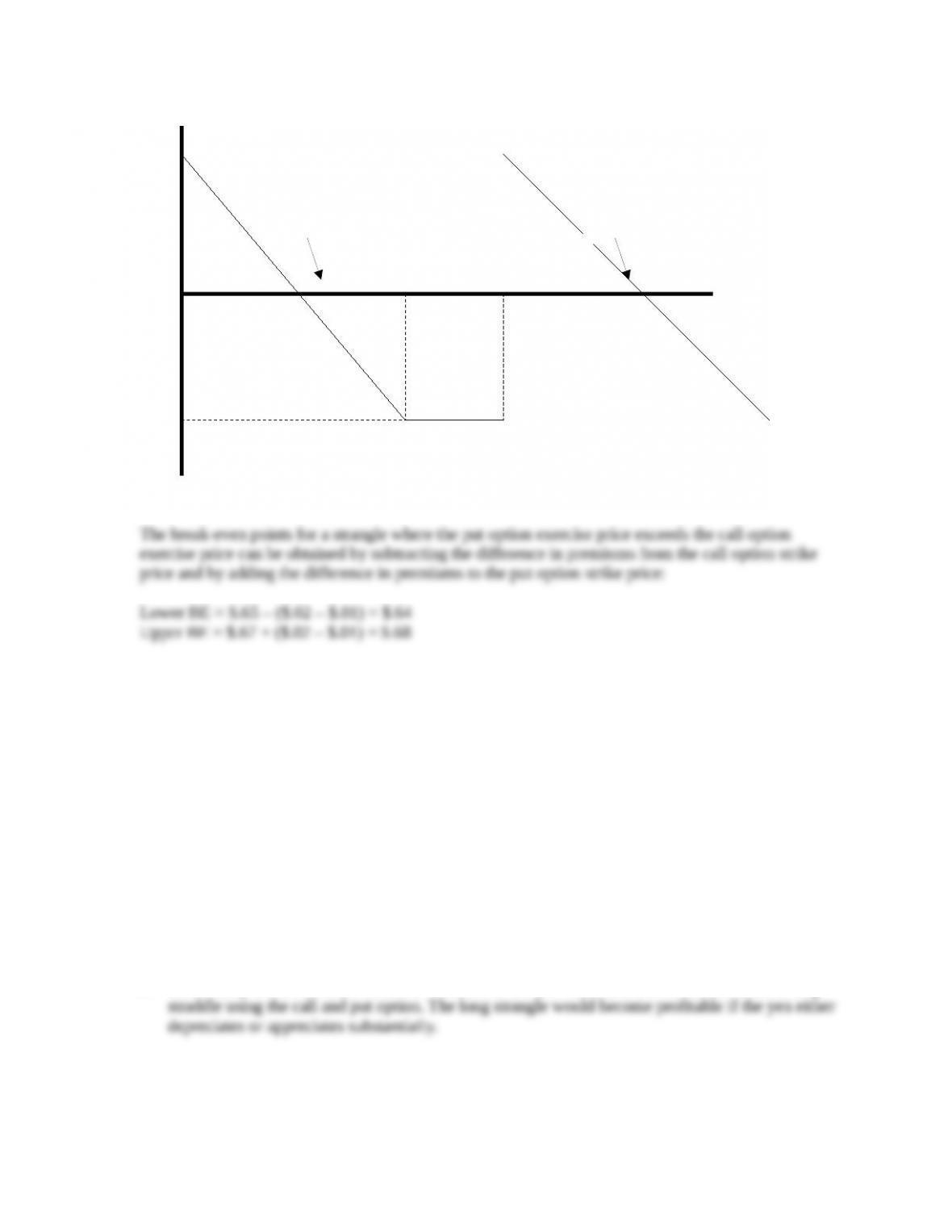

b. The break-even points for a strangle are located below the lower exercise price and above the

higher exercise price. The lower break-even point is located at $1.46 = $1.53 – ($.04 + $.03). The

c. Since $1.55 is between the two exercise prices, neither option will be exercised, and the strangle

d. If the spot price is $1.50, the put option will be exercised, but the call option will expire. On the

put option, the strangle writer will lose $.03 = $1.53 – $1.50. The writer will also collect the

32. Currency Strangles. Refer to the previous question, but assume that the call and put option

premiums are $.035 per unit and $.025 per unit, respectively. (See Appendix B in this chapter.)

a. Construct a contingency graph for a long pound strangle.

b. Construct a contingency graph for a short pound strangle.

ANSWER:

a. The plotted points should create a U shape that cuts through the horizontal (break-even) axis at

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Future spot rate

$1.47 $1.62

$1.53 $1.56

Future spot rate

$1.47 $1.62

$1.53 $1.56

Net profit per unit

b. The plotted points should create an upside down U shape that cuts through the horizontal

Net profit per unit

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

$1.47

-$.06

-$1.47

$.06

33. Currency Strangles. The following information is currently available for Canadian dollar (C$)

options (see Appendix B in this chapter):

Put option exercise price = $.75

Put option premium = $.014 per unit

Call option exercise price = $.76

Call option premium = $.01 per unit

One option contract represents C$50,000

a. What is the maximum possible gain the purchaser of a strangle can achieve using these options?

b. What is the maximum possible loss the writer of a strangle can incur?

c. Locate the break-even point(s) of the strangle.

ANSWER:

a. The maximum gain of a long strangle is unlimited for currency appreciation. For currency

b. The maximum loss of a short strangle is unlimited for currency appreciation. For currency

c. The lower break-even point is obtained by subtracting both premiums from the put option

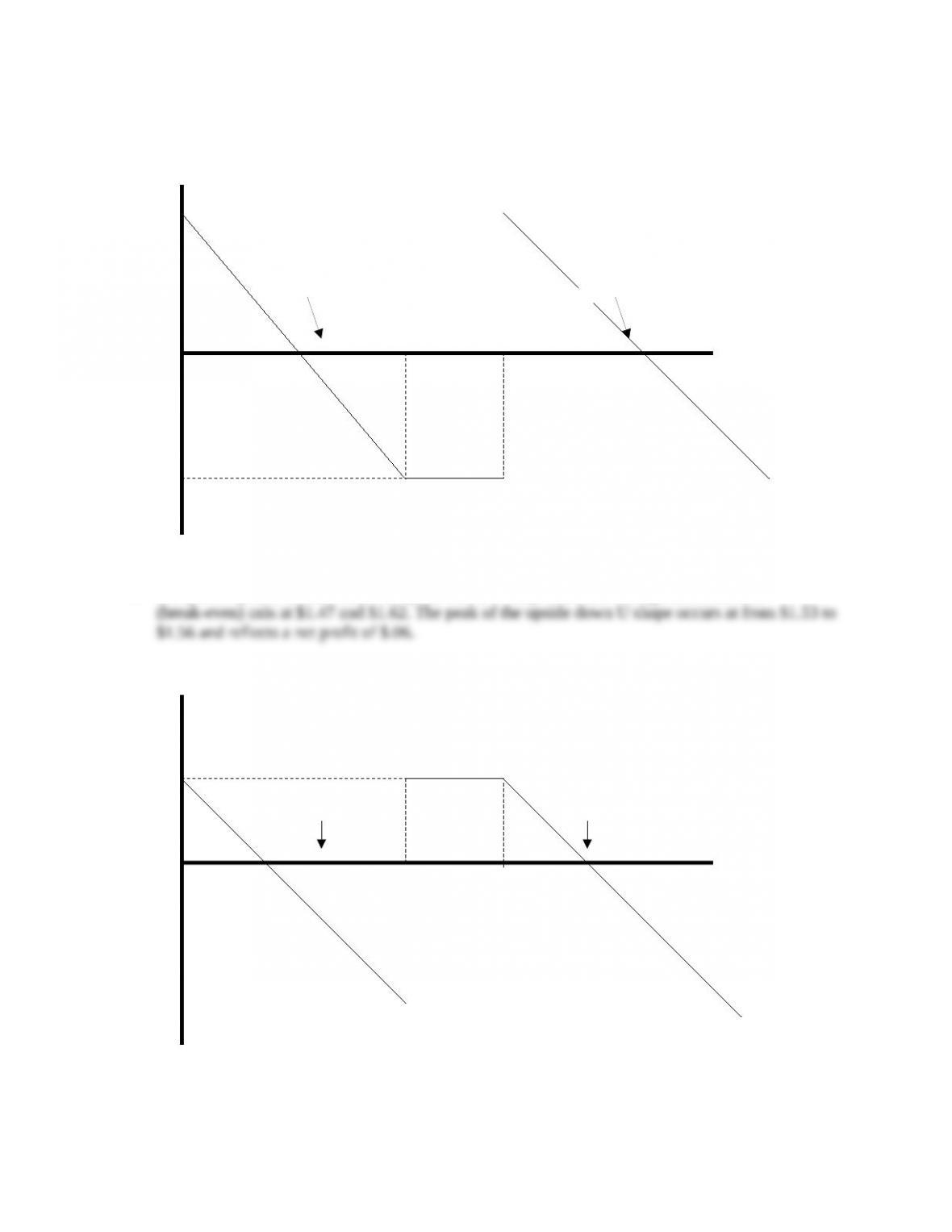

34. Currency Strangles. For the following options available on Australian dollars (A$), construct a

worksheet and contingency graph for a long strangle. Locate the break-even points for this strangle.

(See Appendix B in this chapter.)

Put option strike price = $.67

Call option strike price = $.65

Put option premium = $.01 per unit

Call option premium = $.02 per unit

ANSWER:

Note that the put strike price exceeds the call strike price in this case.

Value of Australian dollar at Option Expiration

$.60 $.65 $.67 $.70

Own a Call –$.02 –$.02 $.00 +$.03

Net profit per unit

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Future spot rate

$.64 $.68

$.65 $.67

35. Speculating with Currency Options. Barry Egan is a currency speculator. Barry believes that the

Japanese yen will fluctuate widely against the U.S. dollar in the coming month. Currently, one-month

call options on Japanese yen (¥) are available with a strike price of $.0085 and a premium of $.0007

per unit. One-month put options on Japanese yen are available with a strike price of $.0084 and a

premium of $.0005 per unit. One option contract on Japanese yen contains 6.25 million yen. (See

Appendix B in this chapter.)

a. Describe how Barry Egan could utilize these options to speculate on the movement of the

Japanese yen.

b. Assume Barry decides to construct a long strangle in yen. What are the break-even points of this

strangle?

c. What is Barry’s total profit or loss if the value of the yen in one month is $.0070?

d. What is Barry’s total profit or loss if the value of the yen in one month is $.0090?

ANSWER:

a. Since Barry seems uncertain as to the direction of the yen fluctuation, he could construct a long

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

$.64

-$.01

b. Lower BE point = $.0084 – ($.0007 + $.0005) = $.0072

c.

Per Unit Per Contract

Selling Price of ¥ $.0084 $52,500 ($.0084 × 6.25 million units)

– Purchase price of ¥ –.0070 –43,750 ($.0070 × 6.25 million units)

d.

Per Unit Per Contract

Selling Price of ¥ $.0090 $56,250 ($.0090 × 6.25 million units)

36. Currency Bullspreads and Bearspreads. A call option on British pounds (₤) exists with a strike

price of $1.56 and a premium of $.08 per unit. Another call option on British pounds has a strike price

of $1.59 and a premium of $.06 per unit. (See Appendix B in this chapter.)

a. Complete the worksheet for a bullspread below.

Value of British Pound at Option Expiration

$1.50 $1.56 $1.59 $1.65

Call @ $1.56

Call @ $1.59

Net

b. What is the breakeven point for this bullspread?

c. What is the maximum profit of this bullspread? What is the maximum loss?

d. If the British pound spot rate is $1.58 at option expiration, what is the total profit or loss for the

bullspread?

e. If the British pound spot rate is $1.55 at option expiration, what is the total profit or loss for a

bearspread?

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

ANSWER:

a.

Value of British Pound at Option Expiration

$1.50 $1.56 $1.59 $1.65

Call @ $1.56 –$.08 –$.08 –$.05 +$.01

b. The breakeven point of a bullspread occurs at the lower exercise price plus the difference in

c. The maximum gain for the bullspread is limited to the difference between the strike prices less

d.

Per Unit Per Contract

Selling Price of ₤ $1.58 $49,375 ($1.58 × 31,250 units)

e. A bearspread using these options involves writing the call option with the $1.56 exercise price and

buying the call option with the $1.59 exercise price. At a spot price of $1.55, neither call option

will be exercised, so the bearspreader nets the difference in options premiums.

Per Unit Per Contract

+ Premium paid for call option +.08 +2,500 ($.08 × 31,250 units)

37. Bullspreads and Bearspreads. Two British pound (₤) put options are available with exercise prices

of $1.60 and $1.62. The premiums associated with these options are $.03 and $.04 per unit,

respectively. (See Appendix B in this chapter.)

a. Describe how a bullspread can be constructed using these put options. What is the difference

between using put options versus call options to construct a bullspread?

b. Complete the following worksheet.

Value of British Pound at Option Expiration

$1.55 $1.60 $1.62 $1.67

Put @ $1.60

Put @ $1.62

Net

c. At option expiration, the spot rate of the pound is $1.60. What is the bullspreader’s total gain or

loss?

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

d. At option expiration, the spot rate of the pound is $1.58. What is the bearspreader’s total gain or

loss?

ANSWER:

a. Using put options to construct a bullspread involves exactly the same actions as constructing a

b.

Value of British Pound at Option Expiration

$1.55 $1.60 $1.62 $1.67

Put @ $1.60 +$.02 –$.03 –$.03 –$.03

c.

Per Unit Per Contract

Selling price of ₤ $1.60 $50,000 ($1.60 × 31,250 units)

d. A bearspread using these put options would be constructed by writing the $1.60 put option and

buying the $1.62 put option.

Per Unit Per Contract

Selling price of ₤ $1.58 $49,375 ($1.58 × 31,250 units)

– Purchase price of ₤ –1.60 –50,000 ($1.60 × 31,250 units)

+ Premium received for put option +.03 +937.50 ($.03 × 31,250 units)

38. Profits from Using Currency Options and Futures. On July 2, the two-month futures rate of the

Mexican peso contained a 2 percent discount (unannualized). There was a call option on pesos with

an exercise price that was equal to the spot rate. There was also a put option on pesos with an exercise

price equal to the spot rate. The premium on each of these options was 3 percent of the spot rate at

that time. On September 2, the option expired. Go to the oanda.com website (or any site that has

foreign exchange rate quotations) and determine the direct quote of the Mexican peso. You exercised

the option on this date if it was feasible to do so.

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

a. What was your net profit per unit if you had purchased the call option?

b. What was your net profit per unit if you had purchased the put option?

c. What was your net profit per unit if you had purchased a futures contract on July 2 that had a

settlement date of September 2?

d. What was your net profit per unit if you sold a futures contract on July 2 that had a settlement

date of September 2?

ANSWER: The answer depends on exchange rates on the specified dates. This question forces

39. Uncertainty and Option Premiums. This morning, a Canadian dollar call option contract has a

$.71 strike price, a premium of $.02, and expiration date of one month from now. This afternoon,

news about international economic conditions increased the level of uncertainty surrounding the

Canadian dollar. However, the spot rate of the Canadian dollar was still $.71. Would the premium of

the call option contract be higher than, lower than, or equal to $.02 this afternoon? Explain.

ANSWER: The premium will be higher than $.02. The call option premium is positively related to

40. Uncertainty and Option Premiums. At 10:30 a.m., the media reported news that the Mexican

government’s political problems were reduced, which reduced the expected volatility of the Mexican

peso against the dollar over the next month. The spot rate of the Mexican peso was $.13 as of 10 a.m.

and remained at that level all morning. At 10 a.m., Hilton Head Co. purchased a call option at the

money on 1 million Mexican pesos with an expiration date one month from now. At 11:00 a.m.,

Rhode Island Co. purchased a call option at the money on 1 million pesos with a December expiration

date one month from now. Did Hilton Head Co. pay more, less, or the same as Rhode Island Co. for

the options? Briefly explain.

ANSWER: Hilton Head Co. paid a higher premium than Rhode Island Co. because the by the time

41. Speculating with Currency Futures. Assume that one year ago, the spot rate of the British

pound was $1.70. One year ago, the one-year futures contract of the British pound exhibited a

discount of 6%. At that time, you sold futures contracts on pounds, representing a total of 1,000,000

pounds. From one year ago to today, the pound’s value depreciated against the dollar by 4 percent.

Determine the total dollar amount of your profit or loss from your futures contract.

ANSWER: Spot rate 1 year ago = $1.70

Forward rate 1 year ago = $1.70 x (1– .06) = $1.598

42. Speculating with Currency Options. The spot rate of the New Zealand dollar is $.77. A call option

on New Zealand dollars with a one-year expiration date has an exercise price of $.78 and a premium

of $.04. A put option on New Zealand dollars at the money with a one-year expiration date has a

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

premium of $.03. You expect that the New Zealand dollar’s spot rate will decline over time and will

be $.71 in one year.

a. Today, Dawn purchased call options on New Zealand dollars with a one-year expiration date.

Estimate the profit or loss per unit at the end of one year. [Assume that the options would be

exercised on the expiration date or not at all.]

b. Today, Mark sold put options on New Zealand dollars at the money with a one-year

expiration date. Estimate the profit or loss per unit for Mark at the end of one year. [Assume

that the options would be exercised on the expiration date or not at all.]

ANSWER:

43. Impact of Expected Volatility on Currency Option Premiums. Assume that Australia’s

central bank announced plans to stabilize the Australian dollar (A$) in the foreign exchange

markets. In response to this announcement, the expected volatility of the A$ declined

immediately. However, the spot rate of the A$ remained at $.89 on this day, and was not

affected by the announcement. The one-year forward rate of the A$ remained at $.89 on this

day and was not affected by the announcement. Do you think the premium charged on a

one-year A$ currency option increased, decreased, or remained the same on this day in

response to the announcement? Briefly explain.

ANSWER: The premium should have declined because of a reduction in expected volatility

Solution to Continuing Case Problem: Blades, Inc.

1. If Blades uses call options to hedge its yen payables, should it use the call option with the exercise

price of $0.00756 or the call option with the exercise price of $0.00792? Describe the tradeoff.

ANSWER: The table shows how the option choices have changed for Blades. If it wants to ensure

paying no more than 5 percent above the spot rate, the option with the exercise price of $0.00756

should be considered, although the premium on that option now has increased to be worth 2 percent

of the exercise price (more expensive). The option premium is higher than what the firm normally

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

2. Should Blades allow its yen position to be unhedged? Describe the tradeoff.

ANSWER: Blades could also remain unhedged, but given its previous desire to hedge because of the

volatile movements even before the event, it would have an even stronger desire to hedge once the

3. Assume there are speculators who attempt to capitalize on their expectation of the yen’s movement

over the two months between the order and delivery dates by either buying or selling yen futures now

and buying or selling yen at the future spot rate. Given this information, what is the expectation on

the order date of the yen spot rate by the delivery date? (Your answer should consist of one number.)

ANSWER: If there are speculators who attempt to capitalize on their expectation of the yen’s future

movement, then the expectation of the future spot rate would be equal to the futures rate. For

example, suppose speculators expect the yen to appreciate. They would buy yen futures now. If the

4. Assume that the firm shares the market consensus of the future yen spot rate. Given this expectation

and given that the firm makes a decision (i.e., option, futures contract, remain unhedged) purely on a

cost basis, what would be its optimal choice?

ANSWER: (See spreadsheet attached.) The optimal choice, given the expected future spot rate in

question 3 and given that the decision is made solely on a cost basis, is to purchase one futures

5. Will the choice you made as to the optimal hedging strategy in question 4 definitely turn out to be the

lowest-cost alternative in terms of actual costs incurred? Why or why not?

ANSWER: No, as mentioned in the case, the yen is very volatile and, therefore, the actual costs

incurred may turn out to be lower had the firm employed either an option to hedge the yen payable or

Alternative 1—Remain Unhedged

Expected Spot Rate $ 0.006912

Amount of Yen

Payables 12,500,000

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Cost in Two Months ($.006912 × 12,500,000 units) $ 86,400.00

Alternative 2—Purchase One Futures Contract

Futures Price per Unit $ 0.006912

Alternative 3—Purchase Two Options

Options Information Option 1 Option 2

Exercise Price $0.0075600 $0.0079200

Calculations Column A Column B Column C Column D

Amount Paid

Total Premium Exercise? for Yen Total Paid

(Premium per (Is Spot Rate > (Exercise Price (Column A +

unit Units) Exercise Price?) Units) Column C)

Two Options, Exercise

Price of $.00756 $1,890.00 No $86,400.00 $88,290.00

6. Now assume that you have determined that the historical standard deviation of the yen is about

$0.0005. Based on your assessment, you believe it is highly unlikely that the future spot rate will be

more than two standard deviations above the expected spot rate by the delivery date. Also assume that

the futures price remains at its current level of $0.006912. Based on this expectation of the future spot

rate, what is the optimal hedge for the firm?

ANSWER: (See spreadsheet attached.) Although the spreadsheet is required, the answer to this

question is intuitive. If the futures rate remains at its current level while the expected spot rate at the

Calculation of Highest Forecasted Spot Rate

Expected Spot $0.006912

Alternative 1—Remain Unhedged

Expected Spot Rate $ 0.007912

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Alternative 2—Purchase One Futures Contract

Futures Price per Unit $ 0.006912

Alternative 3—Purchase Two Options

Options Information Option 1 Option 2

Exercise Price $0.0075600 $0.0079200

Calculations Column A Column B Column C Column D

Amount Paid

Total Premium Exercise? for Yen Total Paid

(Premium per (Is Spot Rate > (Exercise Price (Column A +

unit Units) Exercise Price?) Units) Column C )

Two Options, Exercise

Price of $.00756 $1,890.00 Yes $94,500.00 $96,390.00

Solution to Supplemental Case: Capital Crystal, Inc.

This case is designed to give students more insight on the advantages and disadvantages of currency

futures and options. More comprehensive questions on this subject are offered in Chapter 11.

a. To hedge with futures, the cost of the imports will be $795 million ($1.59 × £500 million). To hedge

b. Since the future spot rate is likely to exceed the futures price, hedging with futures would likely be less

costly than not hedging. Even if it was more costly, it might be wise to hedge in keeping with the

conservative management style of Capital Crystal, Inc.

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Assuming the forecast is correct, the cost of importing when not hedging is $785 million ($1.57 ×

£500 million), which is less than the cost of either hedge. However, given the conservative

management style of Capital Crystal, Inc., a hedge may still be appropriate. If the pound’s value is just

$.02 higher than forecasted in three months, Capital will have to pay $5 million more than if it had

If students put themselves in the position of the managers (bonus is received if a minimum level of

performance is achieved), they would probably hedge. However, it is questionable whether this

Small Business Dilemma

Use of Currency Futures and Options by the Sports Exports Company

1. How can the Sports Exports Company use currency futures contracts to hedge against exchange rate

risk? Are there any limitations of using currency futures contracts that would prevent the Sports

Exports Company from locking in a specific exchange rate at which it can sell all the pounds it

expects to receive in each of the upcoming months?

ANSWER: The Sports Exports Company can hedge against exchange rate risk by selling futures

contracts on pounds. It could use settlement dates that match up with the receivable dates, or could

2. How can the Sports Exports Company use currency options to hedge against exchange rate risk? Are

there any limitations of using currency options contracts that would prevent the Sports Exports

Company from locking in a specific exchange rate at which it can sell all the pounds it expects to

receive in each of the upcoming months?

ANSWER: The Sports Exports Company can hedge against exchange rate risk by purchasing put

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

3. Jim Logan, owner of the Sports Exports Company, is concerned that the pound may depreciate

substantially over the next month, but he also believes that the pound could appreciate substantially if

specific situations occur. Should Jim use currency futures or currency options to hedge the exchange

rate risk? Is there any disadvantage of selecting this method for hedging?

ANSWER: Jim may consider purchasing put options, which provide a greater degree of flexibility.

The disadvantage of purchasing put options is that a premium must be paid to purchase the options,

Part 1—Integrative Problem

The International Financial Environment

Mesa Company specializes in the production of small fancy picture frames, which are exported from the

U.S. to the United Kingdom. Mesa invoices the exports in pounds and converts the pounds to dollars

when they are received. The British demand for these frames is positively related to economic conditions

in the United Kingdom. Assume that British inflation and interest rates are similar to the rates in the U.S.

Mesa believes that the U.S. balance-of-trade deficit from trade between the U.S. and the United Kingdom

will adjust to changing prices between the two countries, while capital flows will adjust to interest rate

differentials. Mesa believes that the value of the pound is very sensitive to changing international capital

flows, and is moderately sensitive to international trade flows. Mesa is considering the following

information:

The U.K. inflation rate is expected to decline, while U.S. inflation rate is expected to rise.

British interest rates are expected to decline, while U.S. interest rates are expected to increase.

1. Explain how the international trade flows should initially adjust in response to the changes in inflation

(holding exchange rates constant). Explain how the international capital flows should adjust in

response to the changes in interest rates (holding exchange rates constant).

ANSWER: The U.S. balance-of-trade deficit should increase in response to the changes in inflation,

The capital flows from the U.S. to the U.K. should decrease in response to lower British interest rates,

2. Using the information provided, will Mesa expect the pound to appreciate or depreciate in the future?

Explain.

ANSWER: The pound’s equilibrium value will change in response to changes in the capital flows

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

The information on inflation rates suggests that the U.S. will purchase more British goods (increased

U.S. demand for pounds) and will sell less goods to the U.K. (reduced supply of pounds to be

The international capital flow forces will place downward pressure on the pound’s value, while the

3. Mesa believes international capital flows shift in response to changing interest rate differentials. Is

there any reason why the changing interest rate differentials in this example will not necessarily cause

international capital flows to change significantly? Explain.

ANSWER: Given the potential upward pressure placed on the pound by the potential balance of

4. Based on your answer to question 2, how would Mesa’s cash flows be affected by the expected

exchange rate movements? Explain.

ANSWER: Mesa’s cash flows would be adversely affected, because the pounds received by Mesa

5. Based on your answer to question 4, should Mesa consider hedging its exchange rate risk? If so,

explain how it could hedge using forward contracts, futures contracts, and currency options.

ANSWER: Mesa should consider hedging exchange rate risk. It could use forward contracts to sell

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.