Solution to Continuing Case Problem: Blades, Inc.

1. Given that Blades expects to use the cash flows generated by the Thai subsidiary to pay the interest

and principal of the notes, would the effective financing cost of the baht-denominated notes be

affected by exchange rate movements? Would the effective financing cost of the yen-denominated

notes be affected by exchange rate movements? How?

ANSWER: No, the effective financing cost of the baht-denominated notes would not be affected by

The effective financing cost of the yen-denominated notes will be affected by exchange rate

movements, since Blades would convert baht into yen in order to pay the interest and principal on

2. Construct a spreadsheet to determine the annual effective financing percentage cost of the

yen-denominated notes issued in each of the three scenarios for the future value of the yen. What is

the probability that the financing cost of issuing yen-denominated notes is lower than the cost of

issuing baht-denominated notes?

ANSWER: (See spreadsheet below.) The annual effective financing percentage costs for the three

scenarios of no change in the value of the yen, an appreciation of 2 percent, and an appreciation of 3

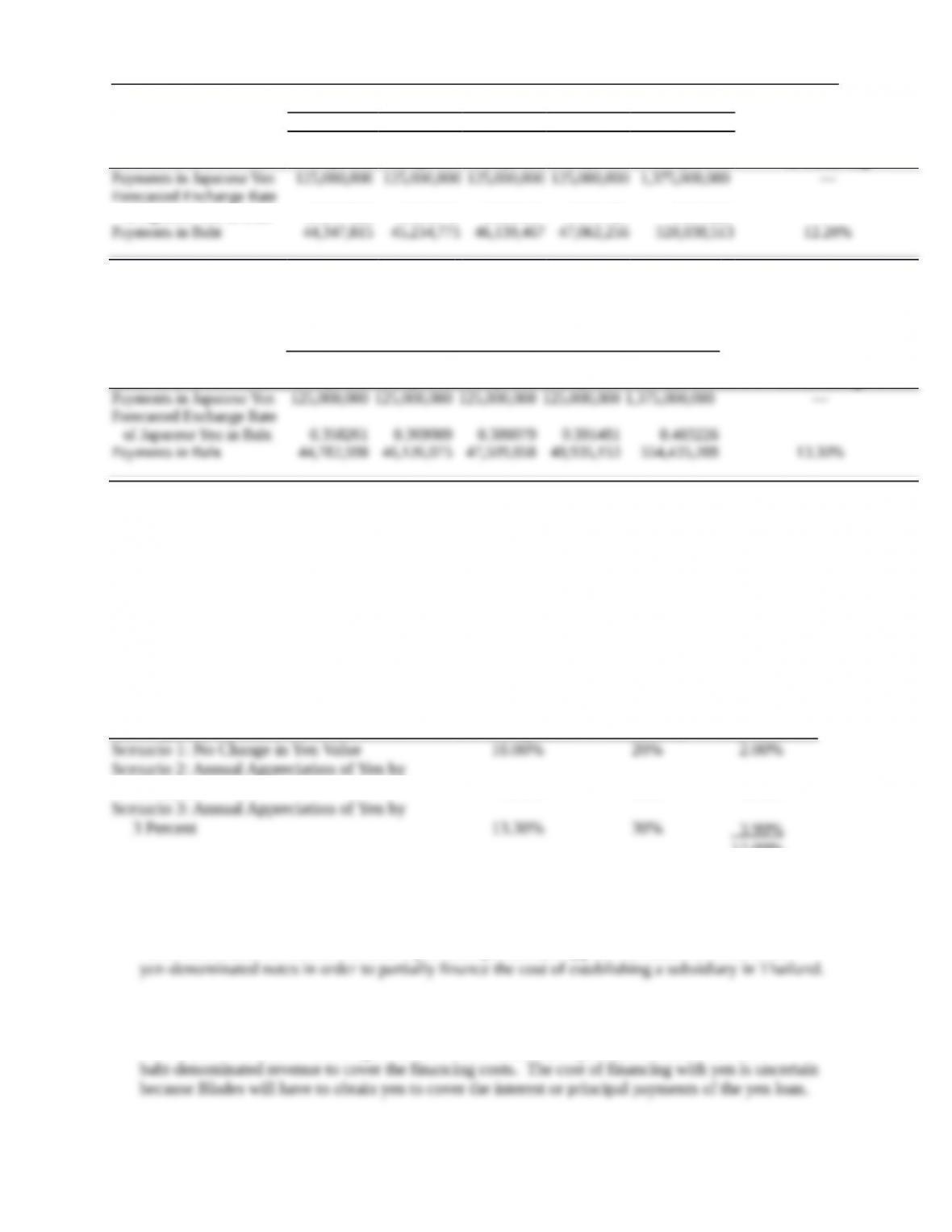

Calculation of Interest Expense:

(1) Yen Value Changes

by 0 Percent Annually

Relative to the Baht

End of Year:

Annual Cost

1 2 3 4 5 of Financing

Forecasted Exchange Rate

of Japanese Yen in Baht 0.347826 0.347826 0.347826 0.347826 0.347826 —

(2) Yen Value Changes

by 2 Percent

Annually Relative

to the Baht

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Long-Term Debt Financing 2

End of Year:

Annual Cost

1 2 3 4 5 of Financing

Forecasted Exchange Rate

of Japanese Yen in Baht 0.3547825 0.361878 0.369116 0.376498 0.384028 —

(3) Yen Value Changes

by 3 Percent Annually

Relative to the Baht

End of Year:

Annual Cost

1 2 3 4 5 of Financing

3. Using a spreadsheet, determine the expected annual effective financing percentage cost of issuing

yen-denominated notes. How does this expected financing cost compare with the expected financing

cost of the baht-denominated notes?

ANSWER: (See spreadsheet below.) The expected annual effective financing cost of issuing

yen-denominated notes is 12.09 percent, which is lower than the cost associated with issuing

baht-denominated notes.

(1) (2) (3) = (1) × (2)

Exchange Rate Scenario

Effective Financing

Percentage Cost Probability Product

Scenario 2: Annual Appreciation of Yen by

2 Percent 12.20% 50% 6.10%

12.09%

4. Based on your answers to the previous questions, do you think Blades should issue yen- or

baht-denominated notes?

ANSWER: Based on the answers to the previous questions, it appears that Blades should issue

5. What is the tradeoff involved?

ANSWER: The cost of financing in baht is known with certainty, because Blades could use

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Long-Term Debt Financing 3

Solution to Supplemental Case: Devil VCR Corporation

a. It can reduce its exposure to exchange rate risk, because it could convert the proceeds of the bond

b. This approach would increase Devil VCR’s exchange rate risk, because it already has expenses in

c. This approach would not reduce the exchange rate risk resulting from the exporting program,

Small Business Dilemma

Long-Term Financing Decision by the Sports Exports Company

The Sports Exports Company continues to focus on producing footballs in the U.S. and exporting them to

the United Kingdom. The exports are denominated in pounds, which has continually exposed the firm to

exchange rate risk. It is now considering a new form of expansion where it would sell specialty sporting

goods in the U.S. If it pursues this U.S. project, it would need to borrow long-term funds. The

dollar-denominated debt has an interest rate that is slightly lower than the pound-denominated debt.

1. Jim Logan, owner of the Sports Exports Company, needs to determine whether dollar-denominated

debt or pound-denominated debt would be most appropriate for financing this expansion, if he does

expand. He is leaning toward financing the U.S. project with dollar-denominated debt, since his goal

is to avoid exchange rate risk. Is there any reason why he should consider using pound-denominated

debt to reduce exchange rate risk?

ANSWER: Yes. Jim’s existing export business results in pound receivables. He could use some of

2. Assume that Jim decides to finance his proposed U.S. business with dollar-denominated debt if he

does implement the U.S. business idea. How could he use a currency swap along with the debt to

reduce the firm’s exposure to exchange rate risk?

ANSWER: The Sports Exports Company could borrow long-term funds denominated in dollars to

Part 4 — Integrative Problem

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Long-Term Debt Financing 4

Long-Term Asset and Liability Management

Gandor Company is a U.S. firm that is considering a joint venture with a Chinese firm to produce and sell

DVDs. Gandor will invest $12 million in this project, which will help to finance the Chinese firm’s

production. For each of the first three years, 50 percent of the total profits will be distributed to the

Chinese firm, while the remaining 50 percent will be converted to dollars to be sent to the U.S. The

Chinese government intends to impose a 20 percent income tax on the profits distributed to Gandor. The

Chinese government has guaranteed that the after-tax profits (denominated in yuan, the Chinese currency)

can be converted to U.S. dollars at an exchange rate of CHY1 = $.20 per unit and sent to Gandor

Company each year. At the present time, no withholding tax is imposed on profits sent to the U.S. as a

result of joint ventures in China. Assume that even after considering the taxes paid in China, an

additional 10 percent tax imposed by the U.S. government on profits received by Gandor Company. After

the first three years, all profits earned are allocated to the Chinese firm.

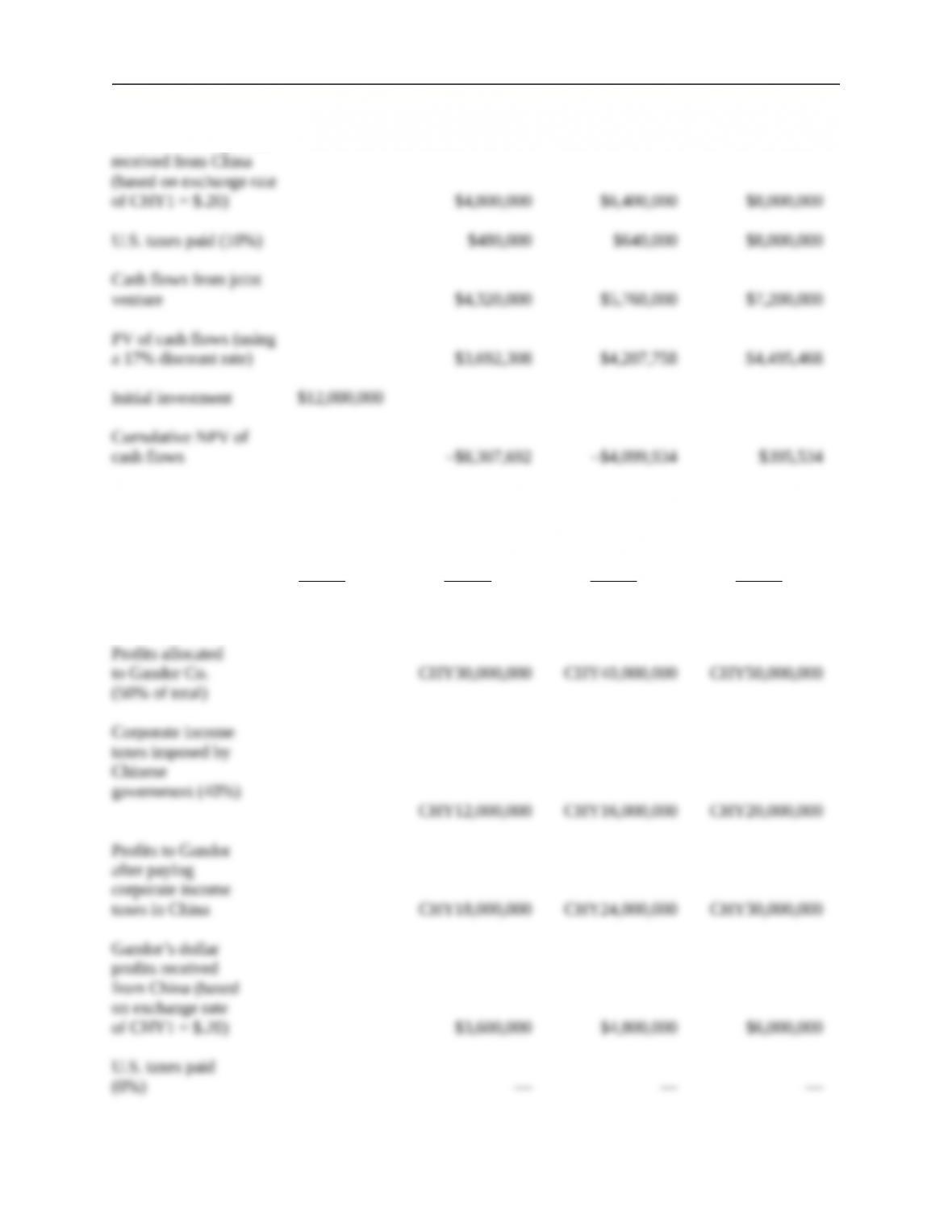

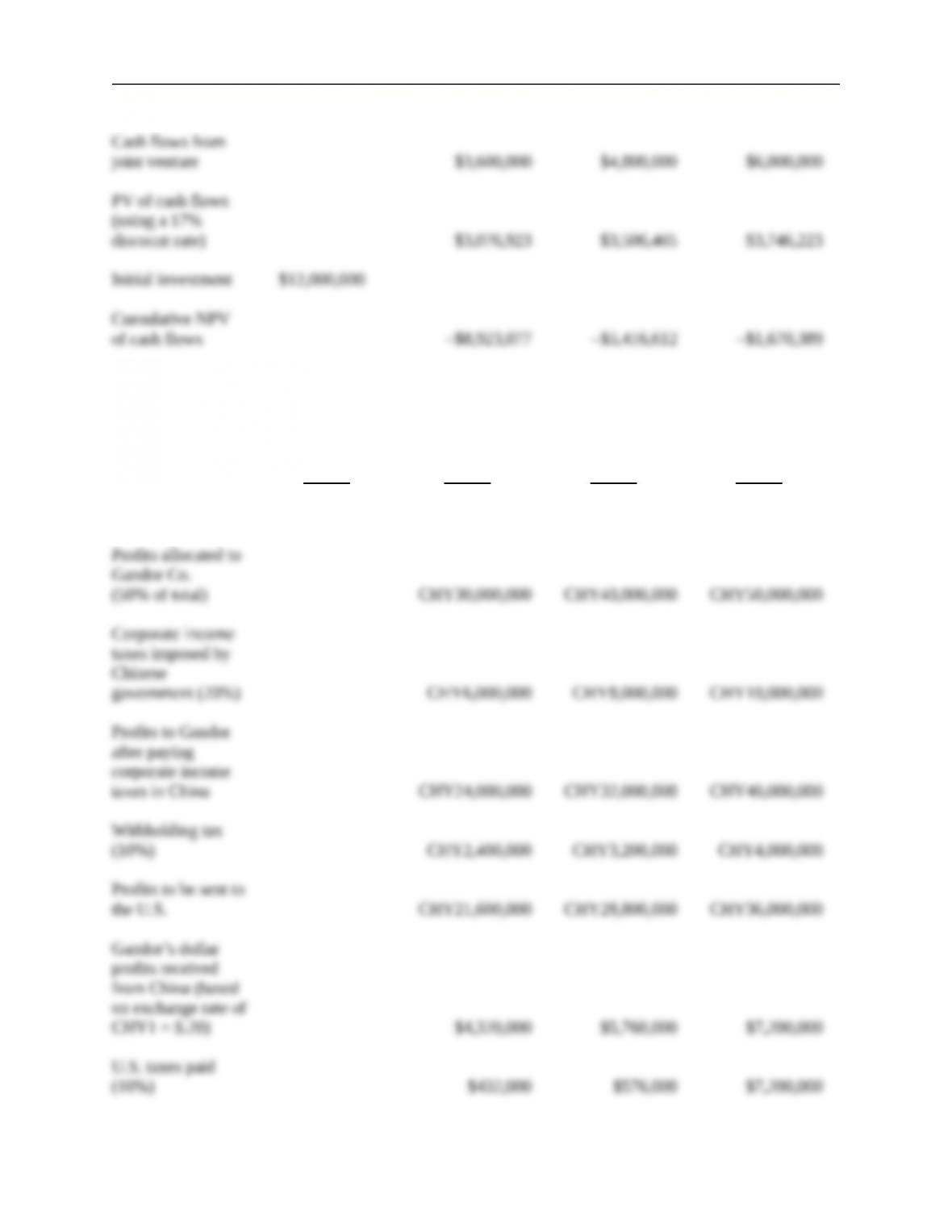

The expected total profits resulting from the joint venture per year are as follows:

Year

Total Profits from Joint

Venture (in yuan, CHY)

1 CHY60 million

2 CHY80 million

3 CHY100 million

Gandor’s average cost of debt is 13.8 percent before taxes. Its average cost of equity is 18 percent.

Assume that the corporate income tax rate imposed on Gandor is normally 30 percent. Gandor uses a

capital structure composed of 60 percent debt and 40 percent equity. Gandor automatically adds 4

percentage points to its cost of capital when deriving its required rate of return on international joint

ventures. Though this project has particular forms of country risk that are unique, Gandor plans to

account for these forms of risk within its estimation of cash flows.

Gandor is concerned about two forms of country risk. First, there is the risk that the Chinese government

will increase the corporate income tax rate from 20 percent to 40 percent (20 percent probability). If this

occurs, additional tax credits will be allowed, resulting in no U.S. taxes on the profits from this joint

venture. Second, there is the risk that the Chinese government will impose a withholding tax of 10

percent on the profits that are sent to the U.S. (20 percent probability). In this case, additional tax credits

will not be allowed, and Gandor will still be subject to a 10 percent U.S. tax on profits received from

China. Assume that the two types of country risk are mutually exclusive. This is, the Chinese government

will adjust only one of its taxes (the income tax or the withholding tax), if any.

1. Determine Gandor’s cost of capital. Also, determine Gandor’s required rate of return for the joint

venture in China.

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Long-Term Debt Financing 5

ANSWER: Gandor’s weighted average cost of capital is:

kc

D

D E kd1 t E

D E ke

60% 138% 70% 40% 18%

58% 7 2%

13%

.

. .

2. Determine the probability distribution of Gandor’s net present values for the joint venture.

Capital budgeting analyses should be conducted for these scenarios:

Scenario 1 Based on original assumptions.

Scenario 2 Based on an increase in the corporate income tax by the Chinese government.

Scenario 3 Based on the imposition of a withholding tax by the Chinese government.

SCENARIO 1: BASED ON ORIGINAL ASSUMPTIONS

(Probability = 60%)

Year 0 Year 1 Year 2 Year 3

Total profits

(in CHY) CHY60,000,000 CHY80,000,000 CHY100,000,000

Long-Term Debt Financing 6

Gandor’s dollar profits

SCENARIO 2: BASED ON INCREASE IN CORPORATE INCOME TAX BY CHINESE GOVERNMENT

(Probability = 20%)

Year 0 Year 1 Year 2 Year 3

Total profits

(in CHY) CHY60,000,000 CHY80,000,000 CHY100,000,000

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Long-Term Debt Financing 7

SCENARIO 3: IMPOSITION OF A WITHHOLDING TAX BY CHINESE GOVERNMENT

(Probability = 20%)

Year 0 Year 1 Year 2 Year 3

Total profits

(in CHY) CHY60,000,000 CHY80,000,000 CHY100,000,000

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Long-Term Debt Financing 8

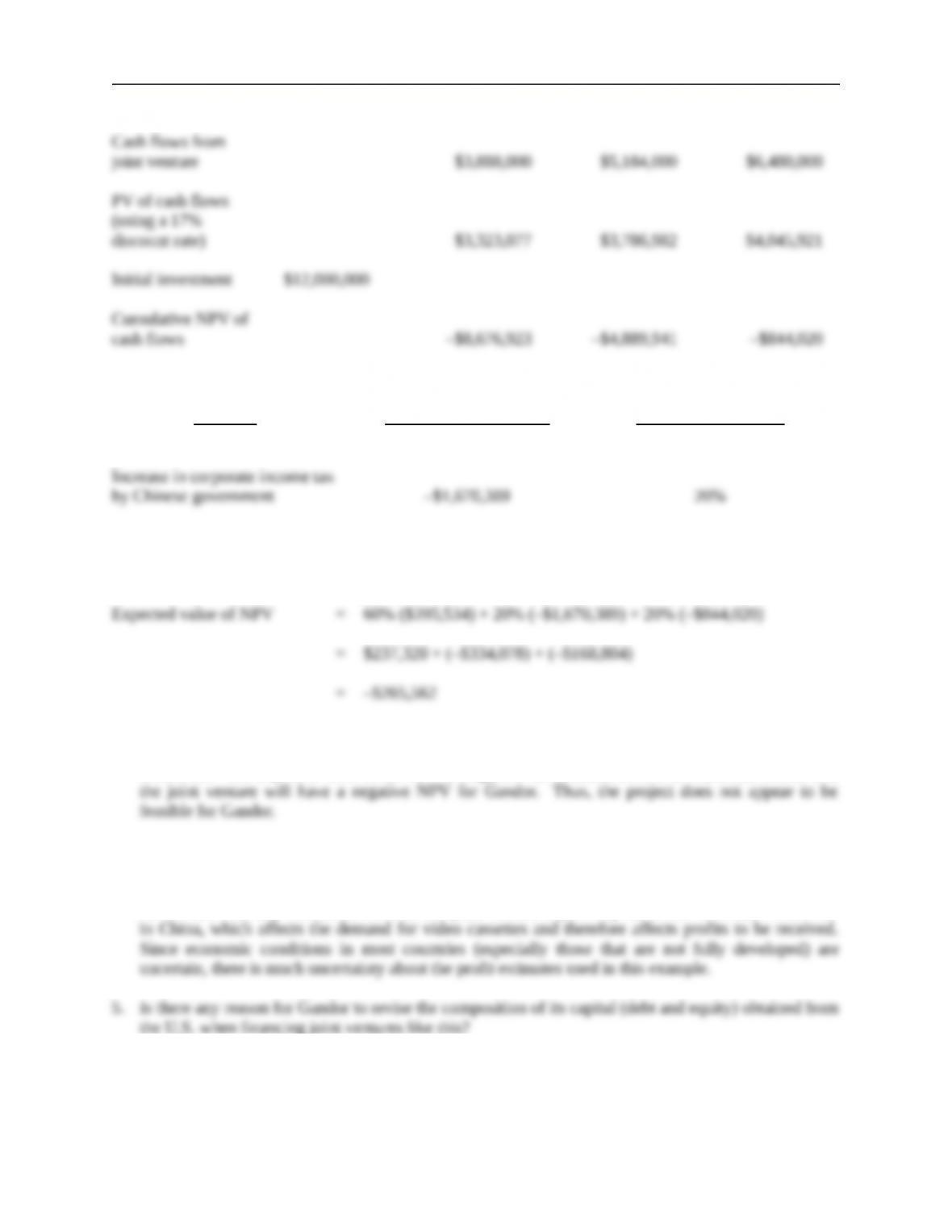

SUMMARY OF SCENARIOS

Scenario NPV for This Scenario

Probability that This

Scenario Will Occur

Original scenario $395,534 60%

Imposition of withholding tax

by Chinese government –$844,020 20%

3. Would you recommend that Gandor participate in the joint venture? Explain.

ANSWER: The expected value of the NPV is negative. In addition, there is a 40 percent chance that

4. What do you think would be the key underlying factor that would have the most influence on the

profits earned in China as a result of the joint venture?

ANSWER: The key influential factor in this joint venture is probably the future economic conditions

the U.S. when financing joint ventures like this?

ANSWER: Gandor may consider using more equity if it believes that the cash flows from joint

ventures like this are very uncertain, in order to ensure that it maintains sufficient cash flows to cover

its debt.

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Long-Term Debt Financing 9

6. When Gandor was assessing this proposed joint venture, some of its managers of recommended that

Gandor borrow the Chinese currency rather than dollars to obtain some of the necessary capital for its

initial investment. They suggested that such a strategy could reduce Gandor’s exchange rate risk. Do

you agree? Explain.

ANSWER: In this case, the exchange rate is guaranteed by the government, so the concept of

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.