22. Factors that Affect the NPV of a Divestiture. Clemson Co. (a U.S. firm) has a subsidiary in

Germany that generates substantial earnings in euros each year. One week ago, it received an offer

from a company to purchase it, and it has not yet responded to this offer.

a. Since last week, the expected stream of euro cash flows has not changed, but the forecasts of the

euro’s value in future periods have been revised downward. Will the NPV of the divestiture be larger

or smaller or the same as it was last week? Briefly explain.

b. Since last week, the expected stream of euro cash flows has not changed, but the long-term interest

rate in the U.S. has declined. Will the NPV of the divestiture be larger or smaller or the same as it was

last week? Briefly explain.

ANSWER:

23. Impact of Country Perspective on Target Valuation. Targ Co. of the U.S. has been targeted by

3 firms that consider acquiring it: (1) Americo (from the U.S.), Japino (of Japan), and Canzo (of

Canada). These 3 firms do not have any other international business, have similar risk levels, and

have a similar capital structure. Each of the 3 potential acquirers has derived similar expected dollar

cash flow estimates for Targ Co. The long-term risk free interest rate is 6% in the U.S.. 9% in Canada,

and 3% in Japan. The stock market conditions are similar in each of the countries. There are no

potential country risk problems that would result from acquiring Targ Co. All potential acquirers

expect that the Canadian dollar will appreciate by 1 percent a year against the U.S. dollar and will be

stable against the Japanese yen. Which firm will likely have the highest valuation of Targ Co.?

Explain.

ANSWER: Japan firm has lowest cost of capital, so the present value of cash flows will be highest

24. Valuation of a Foreign Target. Gaston Co. (a U.S. firm) is considering the purchase of a target

company based in Mexico. The net cash flows to be generated by this target firm are expected to be

300 million pesos at the end of one year. The existing spot rate of the peso is $.14, while the expected

spot rate in one year is $.12. All cash flows will be remitted to the parent at the end of one year. In

addition, Gaston hopes to sell the company for 800 million pesos (after taxes) at the end of one year.

The target has 10 million shares outstanding. If Gaston purchases this target, it would require a 25

percent return. The maximum value that Gaston should pay for this target company today is ____

pesos per share. Show your work.

ANSWER:

Cash flows generated by target in one year = 1,100 million pesos x $.12 = $132 million.

25. Divestiture of a Foreign Subsidiary. Rudecki Co. (a U.S. firm) has a Polish subsidiary that is

considering divesting. This subsidiary is completely focused on research and development for

Rudecki’s other business. Rudecki has cash outflows (paid in zloty, the Polish currency) for the

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Corporate Governance and Control 2

laboratories and scientists in Poland. Although the subsidiary does not generate any sales, its research

and development lead to new products and higher sales of products that are solely in the U.S. and are

denominated in dollars. There is no foreign competition. Last week, a firm offered to purchase the

subsidiary for $10 million, and the offer is still available. Today Rudecki has revised its forecasts of

the zloty upward for all future periods. Will today’s adjustment in exchange rate forecasts increase,

decrease, or have no effect on the net present value of a divestiture of this subsidiary from Rudecki’s

perspective? Briefly explain. [Keep in mind that the NPV of the divestiture is not the same as the

NPV that results from acquiring a project.]

ANSWER: The expected appreciation of the zloty makes the subsidiary more expensive to operate.

26. Poison Pills and Takeovers. Explain how a foreign target could use poison pills to prevent a

takeover or change the terms of a takeover.

ANSWER: A poison pill does not require the approval of other shareholders so it can be easily

27. Governance of MNCs by Shareholders. Explain the various ways in which large shareholders

can attempt to govern an MNC and improve its management.

ANSWER: If large shareholders dislike a new policy by management, they may contact the board

and voice their opinion. They may also engage in proxy contests, in which they attempt to change the

28. Divestiture of a Foreign Subsidiary. Ved Co. (a U.S. firm) has a subsidiary in Germany that

generates substantial earnings in euros each year. It will soon decide whether to divest the subsidiary.

One week ago, a company offered to purchase the subsidiary from Ved Co., and Ved has not yet

responded to this offer.

a. Since last week, the expected stream of euro cash flows has not changed, but the forecasts of the

euro’s value in future periods have been revised downward. When deciding whether a divestiture is

feasible, Ved Co. estimates the NPV of the divestiture. Will Ved’s estimated NPV of the divestiture be

larger or smaller or the same as it was last week? Briefly explain.

b. If the long-term interest rate in the U.S. suddenly declines, and all other factors are unchanged, will

the NPV of the divestiture be larger or smaller or the same as it was last week? Briefly explain.

ANSWER:

a. Since the euro is depreciating, then the PVs for the divesture will lower, because the values of the

b. Since the interest rate in U.S. declines then Cost of Debt (kd) will be lower too. It will affect the

required rate of return used to estimate the PVs of the net cash flows. The rate is inversely

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Corporate Governance and Control 3

29. Valuation of a Planned Divestiture. Dallen Co. has a subsidiary in Mexico that does research and

development and produces prescription pills that are transported to and sold in the U.S. The parent

used its own funds to build the subsidiary. Dallen Co. pays for the operations in Mexico in Mexican

pesos, but all of its revenue from selling the pills in the U.S. is in dollars. It has no other international

business. Dallen’s competitors are local firms in the U.S. that have no international operations. Two

days ago, Dallen received an offer from a firm to buy Dallen’s subsidiary, and the offer is in effect for

a few days.

a. Yesterday, an event occurred that makes the parent of Dallen Co. believe that the Mexican peso will

weaken substantially in the future. Do you think the event that occurred yesterday will increase,

decrease, or have no impact on the likelihood that Dallen will accept the offer and sell its subsidiary

at the existing offer price? Briefly explain.

ANSWER: The weaker peso reduces the cost to the Dallen parent when Dallen pays for the

b. Today, an event occurred that caused the risk-free interest rate in the U.S. to increase. Do you think

the event that just occurred today will increase, decrease, or have no impact on the likelihood that

Dallen will accept the offer and sell its subsidiary at the existing offer price? Briefly explain.

ANSWER: The parent’s cost of equity increases because the U.S. risk-free interest rate increased,

30. Divestiture Decision. Kylee Co. (a U.S. firm) has a British subsidiary that will generate cash flows of

3 million pounds at the end of each of the next two years. It uses the prevailing spot rate of the British

pound of $1.80 as a forecast of the future value of the pound. Its required rate of return on this

business is 16 percent. Kylee just received an offer from a British company who wants to buy the

subsidiary for $8,000,000. Assume that Kylee would not be subject to any tax on the sale.

a. Should Kylee Co. sell the business? Show your work.

ANSWER:

Year 1 Year 2

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Corporate Governance and Control 4

b. Assume that there is news today that causes Kylee to think that the British pound will strengthen

substantially the next two years. Assume the offer price remains unchanged. If Kylee reassesses

whether to divest based on this information, do you think the potential news will increase the net

present value of the divestiture (make the divestiture more beneficial for Kylee), reduce the net

present value of the divestiture, or have no impact on the estimated net present value of the

divestiture? Briefly explain.

ANSWER: A stronger pound increases the value of the subsidiary, so the NPV of the divestiture

c. Assume that today the prevailing long-term U.S. risk-free interest rate decreased, and that this has

no effect on Kylee’s cash flows from operations. Assume the offer price remains unchanged. Do you

think this information about the decline in the U.S. risk-free interest rate will increase the net present

value of the divestiture, reduce the net present value of the divestiture, or have no impact on the

estimated net present value of the divestiture? Briefly explain.

ANSWER: A decrease in the prevailing risk-free rate results in a lower required rate of return on the

Solution to Continuing Case Problem: Blades, Inc.

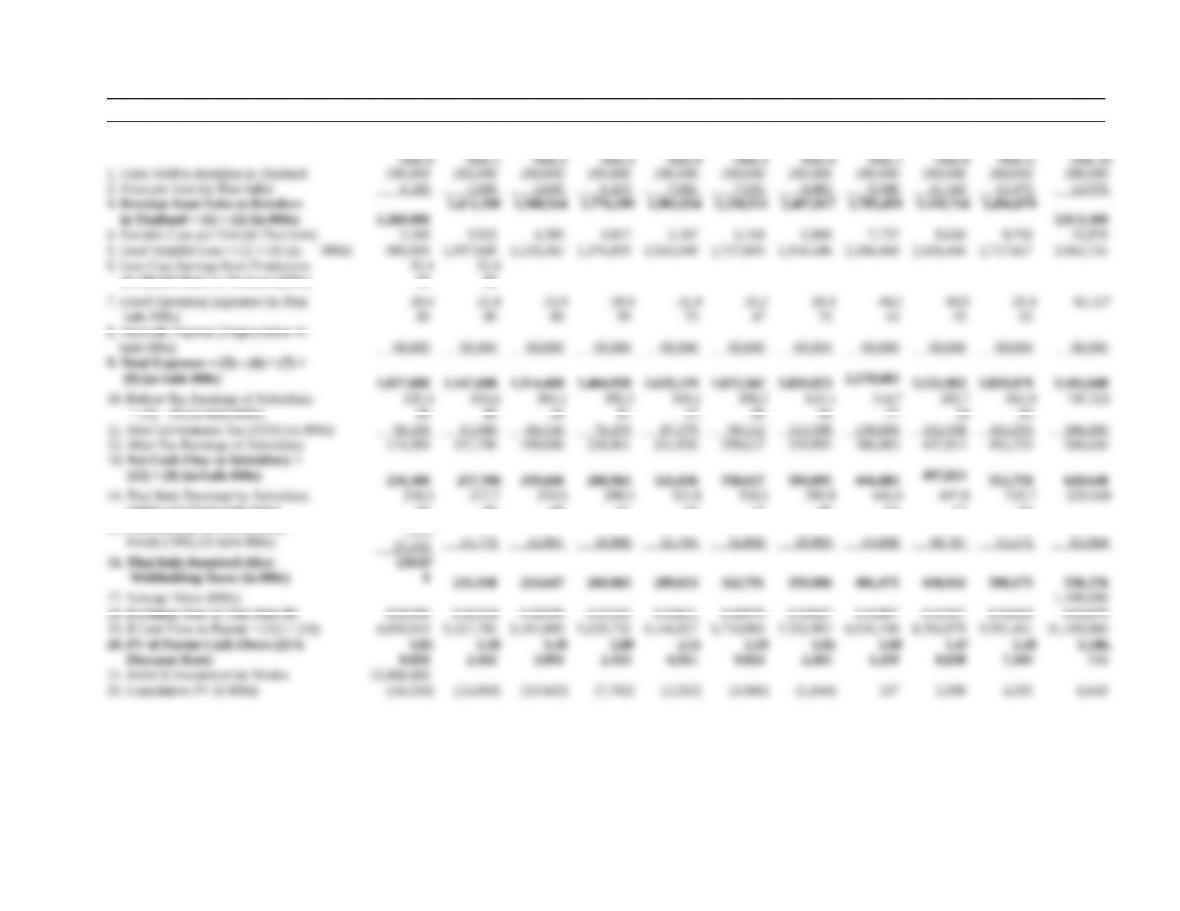

1. Using a spreadsheet, determine the NPV of the acquisition of Skates’n’Stuff. Based on your

numerical analysis, should Blades establish a subsidiary in Thailand or acquire Skates’n’Stuff?

ANSWER: (See spreadsheet attached.) The analysis indicates that the acquisition will result in a net

2. If Blades negotiates with Skates’n’Stuff, what is the maximum amount (in Thai baht) Blades should

be willing to pay?

ANSWER: If Blades, Inc. were to negotiate with Skates’n’Stuff, it should attempt to pay a price that

3. Are there any other factors Blades should consider in making its decision? In your answer, you should

consider the price Skates’n’Stuff is asking relative to your analysis in question 1, other potential

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

251,668$

)079,013,4$172,655,4($000,000,8$

d

NPV

Third, the assumptions gathered by Ben Holt rely on information from unaudited financial statements,

and the accuracy of these numbers may be questionable. Fourth, Blades should consider whether the

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Corporate Governance and Control 6

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

2. Price per Unit (in Thai baht) 4,500 5,040 5,645 6,322 7,081 7,931 8,882 9,948 11,142 12,479 13,976

3. Revenue from Sales to Retailers

1,411,200 1,580,544 1,770,209 1,982,634 2,220,551 2,487,017 2,785,459 3,119,714 3,494,079

4. Variable Cost per Unit (in Thai baht) 3,500 3,920 4,390 4,917 5,507 6,168 6,908 7,737 8,666 9,706 10,870

6. Less Cost Savings from Production

of 108,000 Pairs in Thailand (000s)

32,4

00

32,4

00

—

—

—

—

—

—

—

—

—

baht 000s)

00

00

88

99

70

47

76

14

19

62

8. Noncash Expense (Depreciation in

9. Total Expenses = (5) – (6) + (7) +

10. Before-Tax Earnings of Subsidiary

= (3) – (9) (in baht 000s)

232,4

00

263,6

00

266,1

44

305,2

81

349,1

15

398,2

09

453,1

94

514,7

77

583,7

50

661,0

00

747,521

13. Net Cash Flow to Subsidiary =

14. Thai Baht Remitted by Subsidiary

(100% of CF) (in baht 000s)

234,3

00

257,7

00

259,6

08

288,9

61

321,8

36

358,6

57

399,8

95

446,0

83

497,8

13

555,7

50

620,640

15. Withholding Tax on Remitted

16. Thai Baht Remitted After

210,87

17. Salvage Value (000s) 1,100,000

18. Exchange Rate of Thai Baht ($) 0.02300 0.02254 0.02209 0.02165 0.02121 0.02079 0.02037 0.01997 0.01957 0.01918 0.01879

20. PV of Parent Cash Flows (25%

4,85

4,18

3,30

2,88

2,51

2,19

1,92

1,68

1,47

1,28

3,346,

21. Initial $ Investment by Blades 23,000,000

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as permitted in a license distributed with a certain product or

service or otherwise on a password-protected website for classroom use.

International Corporate Governance and Control 7

Solution to Supplemental Case: Redwing Technology Company

a. The earnings performance translated in dollars is misleading because they are distorted by varying

exchange rates. The actual earnings in each local currency in each subsidiary should be assessed,

since the subsidiary has no control over the exchange rate used for translation. The translation causes

earnings to be overstated when the local currency is strong (against the dollar) and understated when

the local currency is weak. The following table shows the earnings of each subsidiary when

measured in the local currency. Based on this table, the Canadian subsidiary experienced a consistent

growth in earnings over time, averaging about a 14 percent increase per year. Conversely, the South

African subsidiary experienced consistent declines in earnings over time, with an average annual

earnings growth rate of –4.38%. The Japanese subsidiary experienced a decline in earnings in all but

one year, and its average annual earnings growth rate was –1.03%. When measured in this way, the

executive in charge of the Canadian subsidiary appears to have achieved the best performance. The

results are much different when earnings are measured in U.S. dollars for all subsidiaries. The

Canadian performance would not be as high while the South African and Japanese performance

would be higher. Yet, the chief executives of the respective subsidiaries cannot control the translated

exchange rate. It can be argued that they should not be rewarded or penalized because of the

translation effect caused by a volatile exchange rate (although there could be exceptions when they

are personally responsible for hedging any remitted earnings or any inflows of funds coming from

other countries).

Earnings (in millions) Denominated in the Local Currency

Annual Annual Annual

Years Percentage South Percentage Percentage

Ago Canada Increase Africa Increase Japan Increase

5 C$16.80 — R210.00 — Y7,500.00 —

b. Based on its high annual growth rate of earnings, the Canadian subsidiary would likely deserve a cash

c. Even if the earnings are remitted, Canada would still be the best bet. There was an assumption that

d. The earnings of the Canadian and South African subsidiaries only appear to be highly correlated when

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

International Corporate Governance and Control 8

Small Business Dilemma

Multinational Restructuring by the Sports Exports Company

1. Are there any reasons why the business that has been so successful in the United Kingdom might not

be successful in other European countries?

ANSWER: When this business was first created, it was based on a perception that British consumers

2. If the business is diversified throughout Europe, will this substantially reduce the exposure of the

Sports Exports Company to exchange rate risk?

ANSWER: No. The European expansion will result in payments of euros for the exports. So the

3. Now that several countries in Europe participate in a single currency system, will this affect the

performance of new expansion throughout Europe?

ANSWER: It may make it easier for the distributor to deal with stores throughout Europe, but the

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.