33. Techniques for Hedging Receivables. SMU Corp. has future receivables of 4,000,000 New Zealand

dollars (NZ$) in one year. It must decide whether to use options or a money market hedge to hedge

this position. Use any of the following information to make the decision. Verify your answer by

determining the estimate (or probability distribution) of dollar revenue to be received in one year for

each type of hedge.

Spot rate of NZ$ = $.54

One-year call option: Exercise price = $.50; premium = $.07

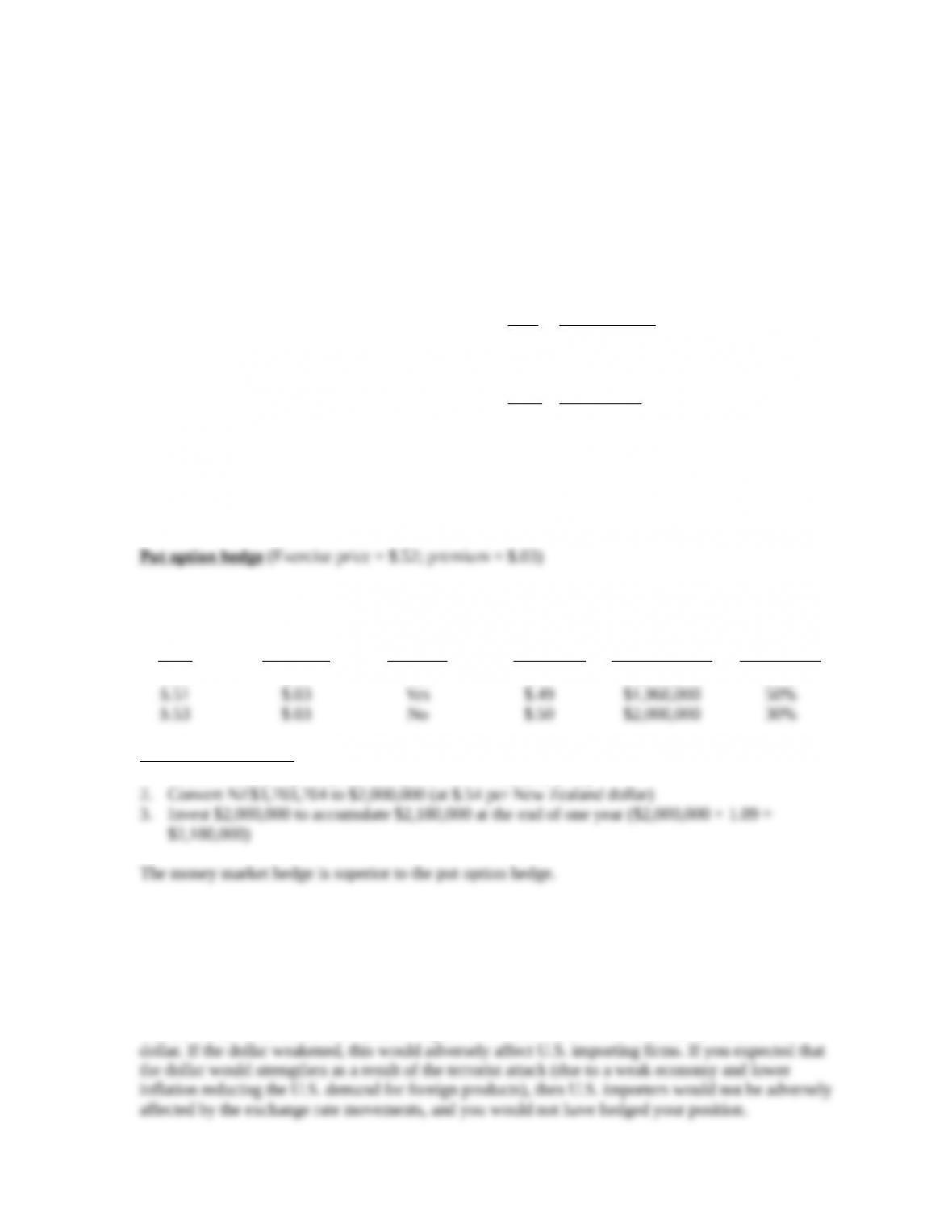

One-year put option: Exercise price = $.52; premium = $.03

U.S. New Zealand

One-year deposit rate 9% 6%

One-year borrowing rate 11 8

Rate Probability

Forecasted spot rate of NZ$ $.50 20%

.51 50

.53 30

ANSWER:

Possible Spot

Rate

Put Option

Premium

Exercise

Option?

Amount per

Unit Received

Accounting

for Premium

Total Amount

Received

for

NZ$4,000,000 Probability

$.50 $.03 Yes $.49 $1,960,000 20%

Money market hedge

1. Borrow NZ$3,703,704 (NZ$4,000,000/1.08 = NZ$3,703,704)

34. Exposure to September 11. If you were a U.S. importer of products from Europe, explain whether

the September 11, 2001 terrorist attack on the U.S. would have caused you to hedge your payables

(denominated in euros) due a few months later. Keep in mind that the attack was followed by a

reduction in U.S. interest rates.

ANSWER: The attack would have caused expectations of weak U.S. stock prices and lowered U.S.

interest rates, which could have reduced capital flows into the U.S. and reduced the value of the

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Managing Transaction Exposure 2

35. Hedging with Forward versus Option Contracts. As treasurer of Tempe Corp., you are confronted

with the following problem. Assume the one-year forward rate of the British pound is $1.59. You

plan to receive 1 million pounds in one year. A one-year put option is available. It has an exercise

price of $1.61. The spot rate as of today is $1.62, and the option premium is $.04 per unit. Your

forecast of the percentage change in the spot rate was determined from the following regression

model:

et = a0 + a1DINFt-1 + a2DINTt + u

where et= percentage change in British pound value over period t

DINFt-1 = differential in inflation between the United States and the United

Kingdom in period t–1

DINTt= average differential between U.S. interest rate and British

interest rate over period t

a0, a1, and a2= regression coefficients

u = error term

The regression model was applied to historical annual data, and the regression coefficients were

estimated as follows:

a0 =0.0

a1 =1.1

a2 =0.6

Assume last year’s inflation rates were 3 percent for the United States and 8 percent for the United

Kingdom. Also assume that the interest rate differential (DINTt) is forecasted as follows for this year:

Forecast of DINTtProbability

1% 40%

2 50

3 10

Using any of the available information, should the treasurer choose the forward hedge or the put

option hedge? Show your work.

ANSWER:

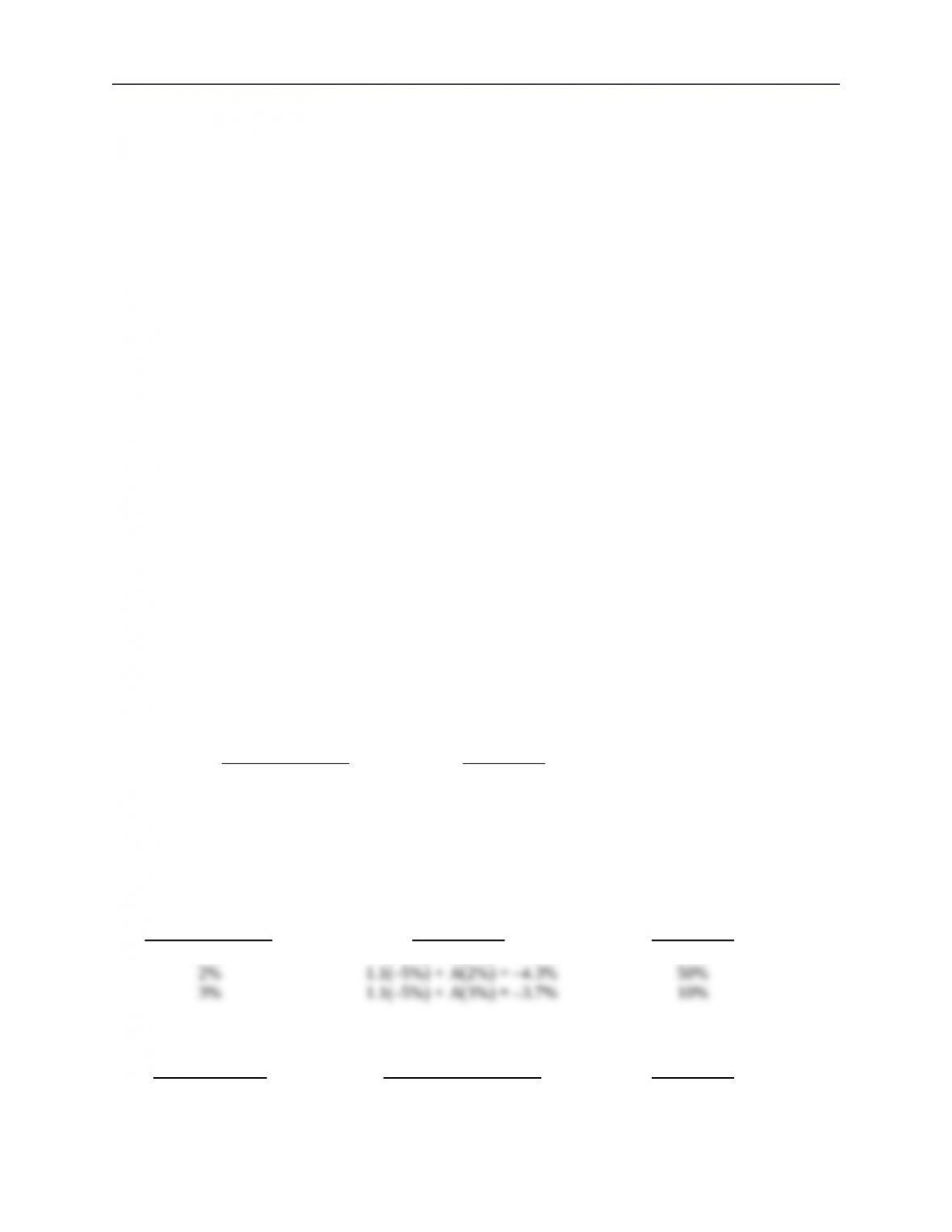

Forecast of DINTtForecast of et Probability

1% 1.1(–5%) + .6(1%) = –4.9% 40%

Approximate

Forecast of etForecasted Spot Rate

(derived above) of Pound in One Year Probability

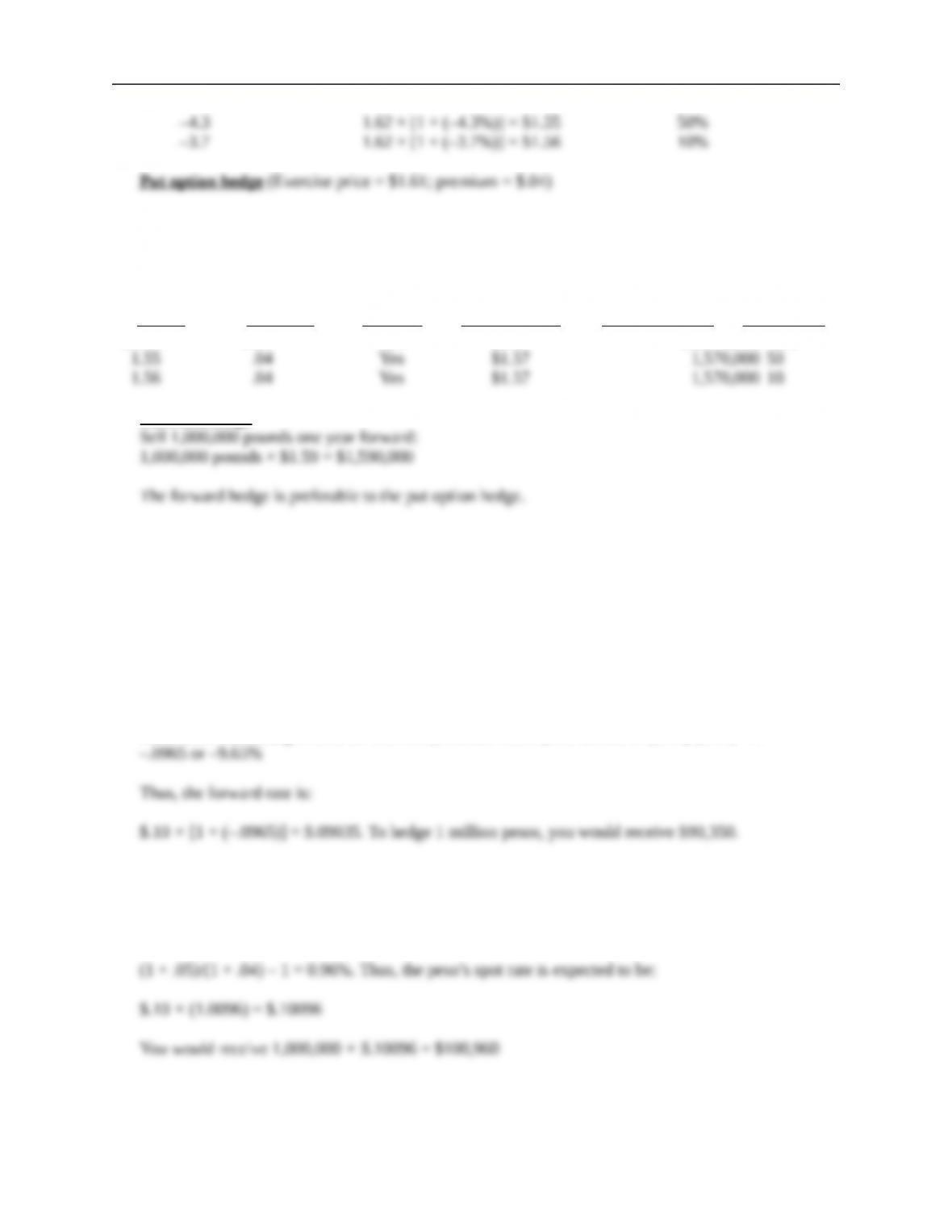

–4.9% 1.62 × [1 + (–4.9%)] = $1.54 40%

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Managing Transaction Exposure 3

Possible

Spot Rate of Amount

Pound in Received

One Year Put per Unit Total Amount

(derived Option Exercise (accounting Received for One

above) Premium Option? for premium) Million Pounds Probability

$1.54 $.04 Yes $1.57 $1,570,000 40%

Forward hedge

36. Hedging Decision. You believe that IRP presently exists. The nominal annual interest rate in Mexico

is 14%. The nominal annual interest rate in the U.S. is 3%. You expect that annual inflation will be

about 4% in Mexico and 5% in the U.S. The spot rate of the Mexican peso is $.10. Put options on

pesos are available with a one-year expiration date, an exercise price of $.1008, and a premium of

$0.014 per unit.

You will receive 1 million pesos in one year.

a. Determine the amount of dollars that you will receive if you use a forward hedge.

ANSWER: According to IRP, the forward premium on the peso should be (1.03)/(1.14) – 1 =

b. Determine the expected amount of dollars that you will receive if you do not hedge and believe in

purchasing power parity (PPP).

ANSWER: The expected percentage change in the Mexican peso according to PPP is:

c. Determine the amount of dollars that you will expect to receive if you use a currency put option

hedge. Account for the premium you would pay on the put option.

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Managing Transaction Exposure 4

ANSWER: Since the expected spot rate is $.10096 based on PPP, you could receive $.10096 per unit

when you receive the pesos. This amount is higher than the exercise price, so you would sell the pesos

37. Forecasting with IFE and Hedging. Assume that Calumet Co. will receive 10 million pesos in

15 months. It does not have a relationship with a bank at this time, and therefore can not obtain a

forward contract to hedge its receivables at this time. However, in three months, it will be able to

obtain a one-year (12-month) forward contract to hedge its receivables. Today the three-month U.S.

interest rate is 2% (not annualized), the 12-month U.S. interest rate is 8%, the three-month Mexican

peso interest rate is 5% (not annualized), and the 12-month peso interest rate is 20%. Assume that

interest rate parity exists. Assume the international Fisher effect exists. Assume that the existing

interest rates are expected to remain constant over time. The spot rate of the Mexican peso today is

$.10. Based on this information, estimate the amount of dollars that Calumet Co. will receive in 15

months.

ANSWER

Expected Peso value in 3 months = 1.02/1.05 = .9714 .9714 x $.10 = $.09714

38. Forecasting from Regression Analysis and Hedging. You apply a regression model to annual

data in which the annual percentage change in the British pound is the dependent variable, and INF

(defined as annual U.S. inflation minus U.K. inflation) is the independent variable. Results of the

regression analysis show an estimate of 0.0 for the intercept and +1.4 for the slope coefficient. You

believe that your model will be useful to predict exchange rate movements in the future.

You expect that inflation in the U.S. will be 3%, versus 5% in the U.K. There is an 80% chance of

that scenario. However, you think that oil prices could rise, and if so, the annual U.S. inflation rate

will be 8% instead of 3% (and the annual U.K. inflation will still be 5%). There is a 20% chance that

this scenario will occur. You think that the inflation differential is the only variable that will affect the

British pound’s exchange rate over the next year.

The spot rate of the pound as of today is $1.80. The annual interest rate in the U.S. is 6% versus an

annual interest rate in the U.K. of 8%. Call options are available with an exercise price of $1.79, an

expiration date of one year from today, and a premium of $.03 per unit.

Your firm in the U.S. expects to need 1 million pounds in one year to pay for imports. You can use

any one of the following strategies to deal with the exchange rate risk:

a. unhedged strategy

b. money market hedge

c. call option hedge

Estimate the dollar cash flows you will need as a result of using each strategy. If the estimate for a

particular strategy involves a probability distribution, show the distribution. Which hedge is optimal?

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Managing Transaction Exposure 5

ANSWER:

The results of the regression analysis and the forecasts of the future inflation rates can be used to

Unhedged strategy:

Possible spot

rate in one year Probability Cost of payables

$1.7496 80.00% $1,496,600

$1.8756 20.00% $1,875,600

Money market hedge:

Call option hedge

Scenario 1: Call options will not be exercised. When including the premium of $.03 per unit, the cost

is $1.7796 per unit.

Possible spot rate

in one year Probability

Cost of hedging

£1,000,000 (including

the option premium)

39. Forecasting Cash Flows and Hedging Decision. Virginia Co. has a subsidiary in Hong Kong

and in Thailand. Assume that the Hong Kong dollar is pegged at $.13 per Hong Kong dollar and it

will remain pegged. The Thai baht fluctuates against the dollar, and is presently worth $.03. Virginia

Co. expects that during this year, the U.S. inflation rate will be 2%, the Thailand inflation rate will be

11%, while the Hong Kong inflation rate will be 3%. Virginia Co. expects that purchasing power

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Managing Transaction Exposure 6

parity will hold for any exchange rate that is not fixed (pegged). The parent of Virginia Co. will

receive 10 million Thai baht and 10 million Hong Kong dollars at the end of one year from its

subsidiaries.

a. Determine the expected amount of dollars to be received by the U.S. parent from the Thai

subsidiary in one year when the baht receivables are converted to U.S. dollars.

b. The Hong Kong subsidiary will send HK$1 million to make a payment for supplies to the Thai

subsidiary. Determine the expected amount of baht that will be received by the Thai subsidiary

when the Hong Kong dollar receivables are converted to Thai baht.

c. Assume that interest rate parity exists. Also assume that the real one-year interest rate in the U.S.

is 1.0%, while the real interest rate in Thailand is 3.0%. Determine the expected amount of dollars

to be received by the U.S. parent if it uses a one-year forward contract today to hedge the

receivables of 10 million baht that will arrive in one year.

ANSWER:

a. [1.02/1.11] – 1 = -8.11%

b. Cross rate of HK$ = $.13/$.0275675=4.7157baht per HK$ or

40. Hedging Decision. Indiana Company expects to receive 5 million euros in one year from exports.

It can use any one of the following strategies to deal with the exchange rate risk. Estimate the dollar

cash flows received as a result of using the following strategies:

a. unhedged strategy

b. money market hedge

c. option hedge

The spot rate of the euro as of today is $1.10. Interest rate parity exists. Indiana Company uses the

forward rate as a predictor of the future spot rate. The annual interest rate in the U.S. is 8% versus an

annual interest rate of 5% in the eurozone. Put options on euros are available with an exercise price of

$1.11, an expiration date of one year from today, and a premium of $.06 per unit. Estimate the dollar

cash flows it will receive as a result of using each strategy. Which hedge is optimal?

ANSWER

Calculation of Forward Rate

Spot Rate $1.10

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Managing Transaction Exposure 7

Remain Unhedged

Future Spot Rate $1.13

Money Market Hedge

Amount of Receivables 5,000,000

Put Option Hedge

41. Overhedging. Denver Co. is about to order supplies from Canada that are denominated in

Canadian dollars (C$). It has no other transactions in Canada, and will not have any other transactions

in the future. The supplies will arrive in one year and payment is due at that time. There is only one

supplier in Canada. Denver submits an order for 3 loads of supplies, which will be priced at C$3

million. Denver Co. purchases C$3 million one year forward, since it anticipates that the Canadian

dollar will appreciate substantially over the year. The existing spot rate is $.62, while the one-year

forward rate is $.64. The supplier is not sure if it will be able to provide the full order, so it only

guarantees Denver Co. that it will ship one load of supplies, and in this case, the supplies will be

priced at C$1 million. Denver Co. will not know whether it will receive one load or three loads until

the end of the year.

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Managing Transaction Exposure 8

Determine Denver’s total cash outflows in U.S. dollars under the scenario that the Canadian supplier

only provides one load of supplies, and that the spot rate of the Canadian dollar at the end of one year

is $.59. Show your work.

ANSWER

Price per load of supplies (C$) 1,000,000

Loads of supplies needed 3

Total C$ needed 3,000,000

42. Long-term Hedging With Forward Contracts. Tampa Co. will build airplanes and export them

to Mexico for delivery in 3 years. The total payment to be received in 3 years for these exports is 900

million pesos. Today the peso’s spot rate is $.10. The annual U.S. interest rate is 4%, regardless of the

debt maturity. The annual Mexican interest rate is 9% regardless of the debt maturity. Tampa plans to

hedge its exposure with a forward contract that it will arrange today. Assume that interest rate parity

exists. Determine the dollar amount that Tampa will receive in 3 years.

ANSWER

Since interest rate parity exists, determine the forward rate premium based on existing interest rates:

p = (1+ih)/(1+if) – 1

43. Timing the Hedge. Red River Co. (a U.S. firm) purchases imports that have a price of 400,000

Singapore dollars and it has to pay for the imports in 90 days. It will use a 90-day forward contract to

cover its payables. Assume that interest rate parity exists. This morning, the spot rate of the Singapore

dollar was $.50. At noon, the Federal Reserve reduced U.S. interest rates, while there was no change

in interest rates in Singapore. The Fed’s actions immediately increased the degree of uncertainty

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Managing Transaction Exposure 9

surrounding the value of the Singapore dollar over the next three months. The Singapore dollar’s spot

rate remained at $.50 throughout the day. Assume that the U.S. and Singapore interest rates were the

same as of this morning. Also assume that the international Fisher effect holds. If Red River Co.

purchased a currency call option contract at the money this morning to hedge its exposure, would you

expect that its total U.S. dollar cash outflows be MORE THAN, LESS THAN, or THE SAME AS the

total U.S. dollar cash outflows if it had negotiated a forward contract this morning? Explain.

ANSWER: More than, because there is an option premium on options and the expectation is that the

44. Hedging With Forward Versus Option Contracts. Assume that interest parity exists. Today,

the one-year interest rate in Canada is the same as the one-year interest rate in the U.S. Utah Co. uses

the forward rate to forecast the future spot rate of the Canadian dollar that will exist in one year. It

needs to purchase Canadian dollars in one year. Will the expected cost of its payables be lower if it

hedges its payables with a one-year forward contract on Canadian dollars or a one-year at-the-money

call option contract on Canadian dollars? Explain.

ANSWER: The forward contract does not require an option premium. The forward rate is same as

45. Hedging With a Bullspread. (See the chapter appendix.) Evar Imports Inc. buys chocolate from

Switzerland and resells it in the U.S. It just purchased chocolate invoiced at SF62,500. Payment for

the invoice is due in 30 days. Assume that the current exchange rate of the Swiss franc is $.74. Also

assume that three call options for the franc are available. The first option has a strike price of $.74 and

a premium of $.03; the second option has a strike price of $.77 and a premium of $.01; the third

option has a strike price of $.80 and a premium of $.006. Evar Imports is concerned about a modest

appreciation in the Swiss franc.

a. Describe how Evar Imports could construct a bullspread using the first two options. What is the

cost of this hedge? When is this hedge most effective? When is it least effective?

b. Describe how Evar Imports could construct a bullspread using the first option and the third

option. What is the cost of this hedge? When is this hedge most effective? When is it least

effective?

c. Given your answers to parts (a) and (b), what is the tradeoff involved in constructing a bullspread

using call options with a higher exercise price?

ANSWER:

a. Evar Imports Inc. would buy the first option and write the second option. It would pay SF62,500

b. Evar Imports Inc. would buy the first option and write the third option. It would pay SF62,500 ×

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Managing Transaction Exposure 10

exercise price of $.80. In this case, Imports could have hedged more effectively by only

purchasing options of the first type to hedge, which would minimize its opportunity costs.

c. Constructing a bullspread with a higher exercise price is more expensive. However, the range in

46. Hedging with a Bearspread. (See the chapter appendix.) Marson Inc. has some customers in Canada

and frequently receives payments denominated in Canadian dollars (C$). The current spot rate for the

Canadian dollar is $.75. Two call options on Canadian dollars are available. The first option has an

exercise price of $.72 and a premium of $.03. The second option has an exercise price of $.74 and a

premium of $.01. Marson Inc. would like to use a bearspread to hedge a receivable position of

C$50,000, which is due in one month. Marson is concerned that the Canadian dollar may depreciate

to $.73 in one month.

a. Describe how Marson Inc. could use a bearspread to hedge its position.

b. Assume the spot rate of the Canadian dollar in one month is $.73. Was the hedge effective?

ANSWER:

a. Marson Inc. would construct a bearspread by writing the option with the $.72 exercise price and

b. If the spot rate of the Canadian dollar is $.73 in one month, the hedge would have been

successful. Marson would have received C$50,000 × ($.03 – $.01) = $1,000 from establishing the

47. Hedging with Straddles. (See the chapter appendix.) Brooks, Inc. imports wood from Morocco. The

Moroccan exporter invoices in Moroccan dirham. The current exchange rate of the dirham is $.10.

Brooks just purchased wood for 2 million dirham and should pay for the wood in three months. It is

also possible that Brooks will receive 4 million dirham in three months from the sale of refinished

wood in Morocco. Brooks is currently in negotiations with a Moroccan importer about the refinished

wood. If the negotiations are successful, Brooks will receive 4 million dirham in three months, for a

net cash inflow of 2 million dirham. The following option information is available:

Call option premium on Moroccan dirham = $.003

Put option premium on Moroccan dirham = $.002

Call and put option strike price = $.098

One option contract represents 500,000 dirham.

a. Describe how Brooks could use a straddle to hedge its possible positions in dirham.

b. Consider three scenarios. In the first scenario, the dirham’s spot rate at option expiration is equal

to the exercise price of $.098. In the second scenario, the dirham depreciates to $.08. In the third

scenario, the dirham appreciates to $.11. For each scenario, consider both the case when the

negotiations are successful and the case when the negotiations are not successful. Assess the

effectiveness of the long straddle in each of these situations by comparing it to a strategy of using

long call options to hedge.

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Managing Transaction Exposure 11

ANSWER:

a. Brooks could construct a long straddle to hedge its positions in dirham. If the negotiations are

b.

Net Cash Flow = +2 million Dirham

Dirham value = $.11 in three

months

* Brooks converts excess

dirham to dollars in the spot

market.

Dirham value = $.08 in three

months

* Brooks converts excess

dirham to dollars at $.098, by

exercising its put options.

Dirham value = $.098 in three

months

*Brooks converts excess

dirham to dollars in the spot

market.

Net Cash Flow = –2 million Dirham

Dirham value = $.11 in three

months

* Brooks converts dollars to

dirham by exercising its call

options.

Dirham value = $.08 in three

months

* Brooks converts dirham to

dollars in the spot market.

* It lets the call option expire.

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.

Managing Transaction Exposure 12

recapture part of the premiums

that were paid for the options.

Dirham value = $.098 in three

months

* Brooks converts dollars to

dirham in the spot market.

48. Hedging with Straddles versus Strangles. (See the chapter appendix.) Refer to the previous

problem. Assume that Brooks believes the cost of a long straddle is too high. However, call options

on with an exercise price of $.105 and a premium of $.002, and put options with an exercise price of

$.09 and a premium of $.001 are also available on Moroccan dirham. Describe how Brooks could use

a long strangle to hedge its possible dirham positions. What is the tradeoff involved in using a long

strangle versus a long straddle to hedge the positions?

ANSWER: Brooks could construct a long strangle in dirham by buying four call options and buying

four put options with different exercise prices. Due to the relationship between the exercise price and

The tradeoff in using a long strangle to hedge is that the strangle does not offer protection until the

spot rate deviates substantially. If the spot rate remains between $.09 and $.105 by the expiration date,

49. Comparison of Hedging Techniques. You own a U.S. exporting firm and will receive 10 million

Swiss francs in one year. Assume that interest parity exists. Assume zero transactions costs. Today,

the one-year interest rate in the U.S. is 7%, and the one-year interest rate in Switzerland is 9%. You

believe that today’s spot rate of the Swiss franc (which is $.85) is the best predictor of the spot rate

one year from now. You consider these alternatives:

*hedge with one-year forward contract,

*hedge with a money market hedge,

*hedge with at-the-money put options on Swiss francs with a one-year expiration date, or

*remain unhedged.

Which alternative will generate the highest expected amount of dollars? If multiple alternatives are

tied for generating the highest expected amount of dollars, list each of them.

ANSWER: Remain unhedged since the future spot rate is expected to be $.85. The forward contract

© 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part, except for use as

permitted in a license distributed with a certain product or service or otherwise on a password-protected website for classroom use.