12. Evaluation of Internal Controls: The Never Sink Canoe (NSC) Company

Segregations of Duties Issues

Control Weakness 1: Transaction authorization should be separated from transaction

Control Weakness 2: Asset custody should be separate from record keeping responsibility.

The accounting clerk has cash receipts and check writing responsibility and also sets up AP and

AR accounts and updates those accounts.

Control Weakness 3: Asset custody should be separate from record keeping responsibility.

Accounting Records Issues

Control Weakness: Adequate source documents, journals, and ledgers need to be in place to

Fraud Potential:Sales staff need only submit a form to claim reimbursement but no proof of the

Control Weakness: Verification procedures are checks on the accounting system to identify

Fraud Potential: The fraud potential has been previously discussed regarding commissions

Chapter 1 Page 2

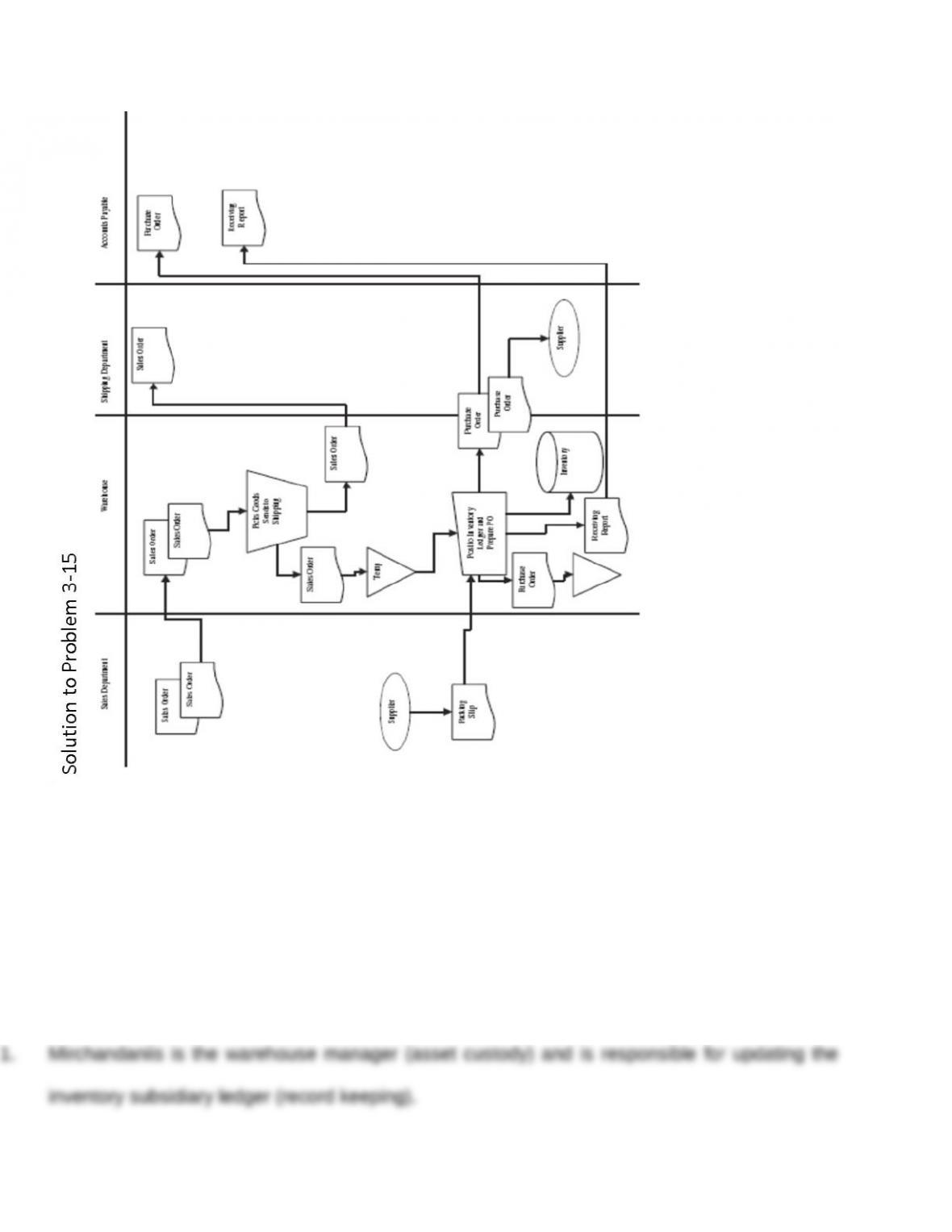

13. Documenting System and Evaluating Controls

a. Flowchart of Process

1. Kickback fraud— The clerk selects the supplier and also places the order. He is thus in position

Chapter 1 Page 3

3. Theft of inventory—the clerk can remove inventory from the warehouse, sell it, and adjust the

14. Analysis of Flowchart, Internal controls

a)

b) The following possible fraud could be committed:

Chapter 1 Page 4

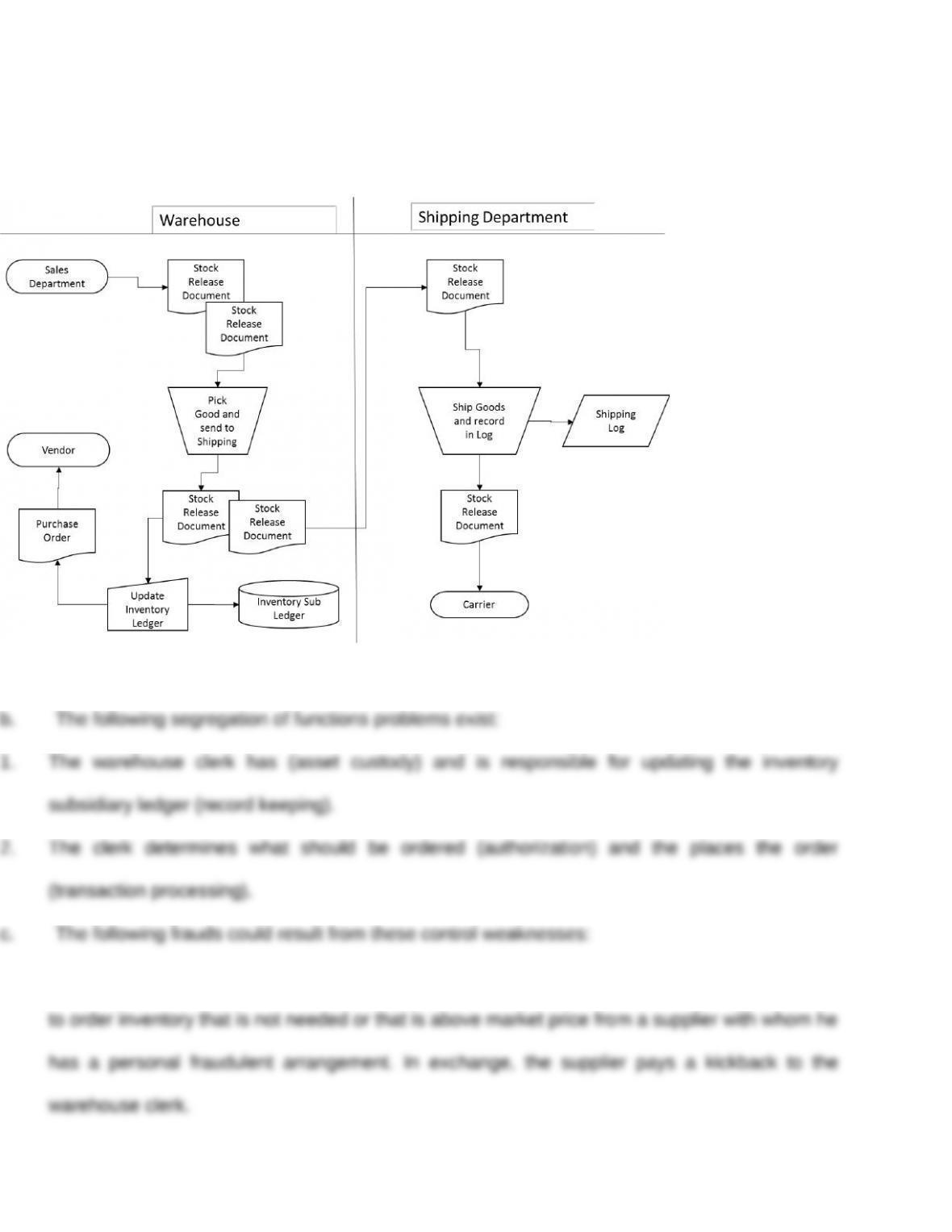

15. Evaluating Internal Controls: Warehouse manager

a) Flowchart

Chapter 1 Page 5

b. The following segregation of functions problems exist:

Chapter 1 Page 6

c. The following frauds could result from these control weaknesses:

1. Kickback fraud—Since Mirchandaniis selects the supplier and also places the order, he could

2. Vendor fraud—Mirchandaniis authorizes, orders, and receives the goods; he could establish

3. Theft of inventory—Mirchandaniis can simply remove the assets from the warehouse, sell them,

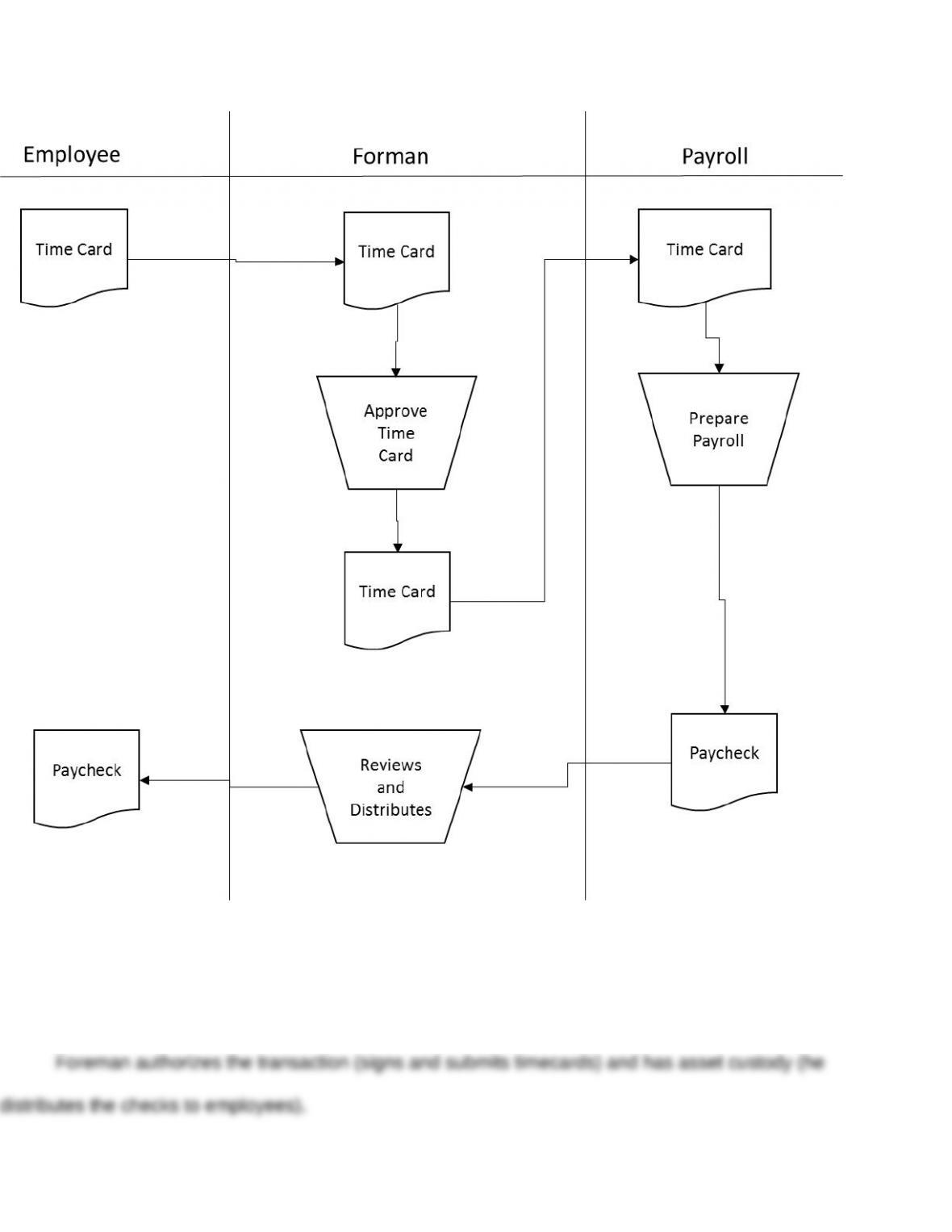

16.EVALUATION OF PAYROLL CONTROLS

a. flowchart 3–16.

Chapter 1 Page 7

b. The following segregation of functions problem exists:

Chapter 1 Page 8

c. The following frauds could result from these control weaknesses:

i. Kickback fraud—the forman permits employees to inflate the hours worked and approves

ii. Nonexistent employee fraud—After an employee leaves the company, the