Answers to End of Chapter Questions

1. All of the factors are equally important and interrelated. Without satisfactory answers to

2. Collateral is a back-up source of repayment, and should not be used to approve a loan by

3. In most cases, a request for loans to buy cheese is unacceptable because this should be

financed by normal cash *ows. Also, a loan for the owner to buy a car should be a personal

4. Why would anyone lend to an individual with bad character? Similarly, why lend to a firm or

non-pro)t organization with a bad reputation and senior management o/cials who have

histories of problems? The only answer is that the lender might be able to control all risk and

5. Character of borrowers:

a. Complaints may be a signal of serious internal operating problems and/or poor quality

b. Family businesses often follow ‘expense preference behavior.’ As such, operating

c. Each of these leads to potential accounting problems. Enron’s example of moving debt

d. Stock issued to principals typically arises from stock options. As such, the principals’

e. Inexperienced managers generally make a higher number of mistakes and potentially

6. Liquidity and leverage ratios address a borrower’s ability to repay fixed debt obligations;

liquidity in the near-term and leverage over longer planning periods. Activity and

7. A high current ratio is associated with high cash, receivables and inventory relative to current

liabilities. Consider a case where the high current assets are inventory and receivables. All

8. Many firms report rising profit year to year, but )nd that they need additional working

capital financing. The typical reason is that the firm’s inventory and accounts receivable are

growing at a high rate. While profit are positive and rising, cash *ow from operations is

9. Sources or uses of cash

a. source

b. use

10. Cash *ow from operations should be suffcient to pay cash dividends and principal payments

on outstanding debt. Thus, this ratio should be at least 100%. The fact that it is less than

11. No. A portion of capital expenditures is typically financed long-term. Cash *ow from

12. Primary source of repayment

a. Selling an asset: advantage: typically a predictable value; disadvantage: time and cost to

b. Generating more sales: advantage: high value for an ongoing concern which should lead

c. Issuing stock (equity): advantage: lowers financial leverage and firm does not have to

d. Increasing a liability: advantage: predictable and quick to access funds; disadvantage:

e. Decreasing expense: advantage: long-term effect if successful; disadvantage: difficult to

13. Ratios:

a. Current ratio: $1,280/$980 = 1.31X

b. Days accounts receivable = $700/($9,125/365) = 28 days

14.

a. Debt service requirements with prime at 8% (effective rate at 10%) are:

Cash *ow from operations – (principal + interest + dividends)

b. If prime equals 9%, interest payments increase by:

15. A partial list of questions would include:

a. What is the experience level of the firm’s o/cers?

16. Originators might consider selling a loan to reduce their credit risk exposure. Another

potential benefit of selling a loan is the reduction in capital requirements. Sellers of loans

Financial institutions on the buying side may use loan participations and loan sales to

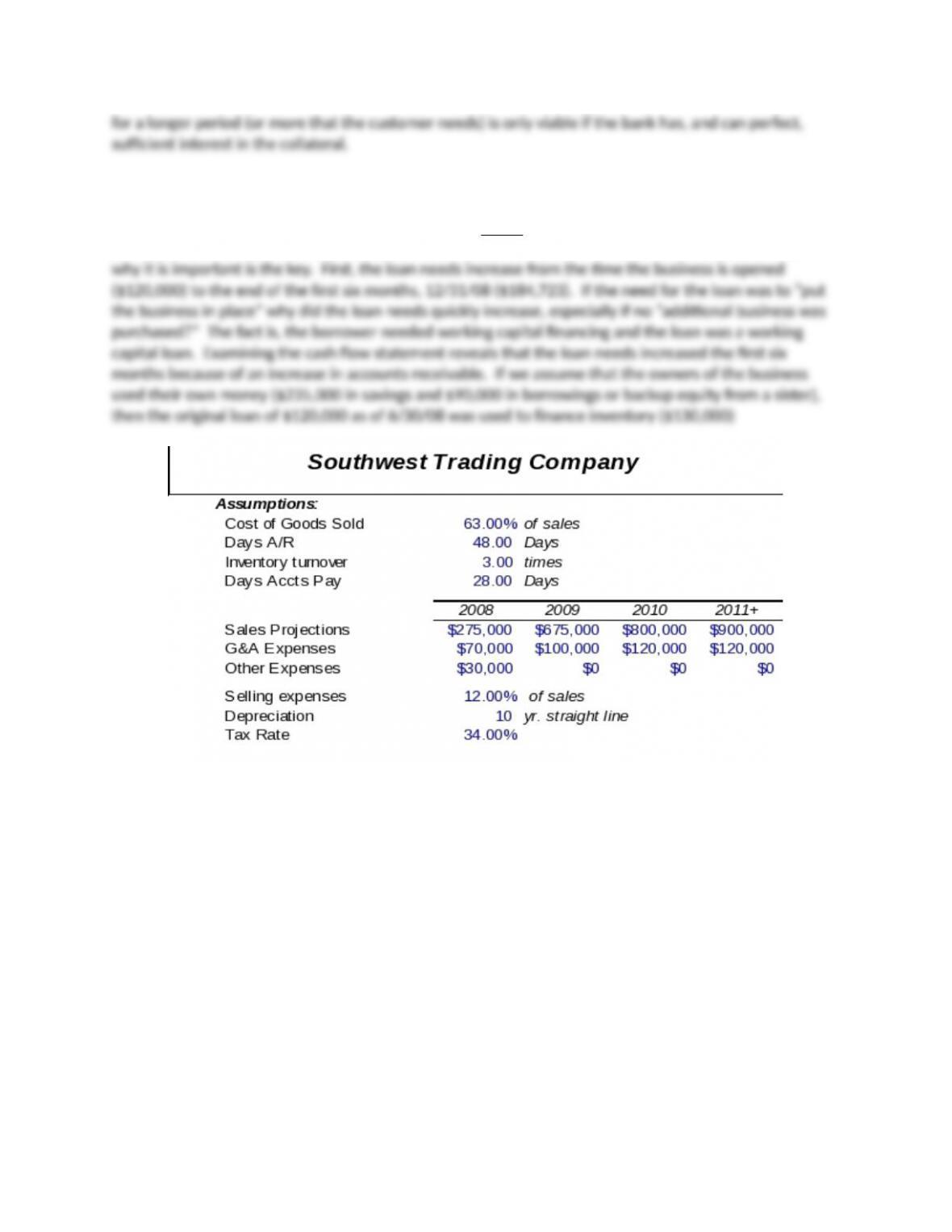

Problem I: Southwest Trading Company

Teaching Objectives

It is often difficult to teach students the importance of cash *ow and how this determines the borrower’s

ability to repay the loan. often, students get involved in calculating ratios, cash *ow statements and

even pro forma statements and lose sight of the objectives of the analysis. The Southwest Trading

Company case requires the student to evaluate the loan request based on the Company’s ability to repay

the loan. The four fundamental questions:

What are the loan proceeds needed for?

How much does the borrower need?

What is the primary source of repayment and when?

What is the secondary source of repayment?

are emphasized in this case.

Typical mistakes

The mistake made most often by the student and even by the lender of the original case

(although this case is far removed from the original), is a failure to clearly determine what the loan

proceeds are to be used for. Originally, the loan was made as a 15-year mortgage for the building. This

type of loan was inappropriate for at least two reasons. The first is that the loan can be paid o: much

The second reason a mortgage is inappropriate is that if the loan o/cer determines that the loan

that “best matches” the need is a mortgage, this is not a loan – rather it is venture capital. The

distinction here is an important one. If the borrower needs a loan to “put the business in place” and the

primary source of repayment is the business, this is venture capital. So, “what’s the di:erence?” and

Answers to the questions:

1. First how much was needed? To open the doors, they needed $120,000.

2. The loan needs increased to a maximum of $184,723 on 12/31/2008.

Southwest Trading Company

Pro Forma Balance Sheet

06/01/08 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13

Cash $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000

Accounts Receivables $0 $72,329 $88,767 $105,205 $118,356 $118,356 $118,356

Inventory $130,000 $115,500 $141,750 $168,000 $189,000 $189,000 $189,000

Gross Fixed Assets $295,000 $295,000 $295,000 $295,000 $295,000 $295,000 $295,000

less Accumulated Dep. $0 $14,750 $44,250 $73,750 $103,250 $132,750 $162,250

Net Plant and Equipment $295,000 $280,250 $250,750 $221,250 $191,750 $162,250 $132,750

Total Assets $445,000 $488,079 $501,267 $514,455 $519,106 $489,606 $460,106

Accounts Payable $0 $24,356 $34,636 $40,677 $45,107 $43,496 $43,496

Notes Payable $90,000 $90,000 $90,000 $90,000 $90,000 $90,000 $90,000

Equity $235,000 $189,000 $228,250 $263,875 $313,705 $363,535 $413,365

Total Liabs & Eq. $325,000 $303,356 $352,886 $394,552 $448,812 $497,031 $546,861

Loan Needs (mkt. sec’s.) $120,000 $184,723 $148,382 $119,904 $70,294 ($7,425) ($86,755)

Total Liabs & Eq. $445,000 $488,079 $501,267 $514,455 $519,106 $489,606 $460,106

including new loan needs

Change in Loan Needs $120,000 $64,723 ($36,341) ($28,478) ($49,609) ($77,719) ($79,330)

Note: Sales ending 12/31/2008 are for 6 months.

Southwest Trading Company

Pro Forma Income Statement

06/30/08 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13

Sales $0 $275,000 $675,000 $800,000 $900,000 $900,000 $900,000

Cost of Goods Sold $0 $173,250 $425,250 $504,000 $567,000 $567,000 $567,000

Gross Margin $0 $101,750 $249,750 $296,000 $333,000 $333,000 $333,000

Selling & Administrative $0 $33,000 $81,000 $96,000 $108,000 $108,000 $108,000

G&A Expenses $0 $70,000 $100,000 $120,000 $120,000 $120,000 $120,000

Depreciation $0 $14,750 $29,500 $29,500 $29,500 $29,500 $29,500

Other $0 $30,000 $0 $0 $0 $0 $0

Total Operating Expenses $0 $147,750 $210,500 $245,500 $257,500 $257,500 $257,500

Earnings Before Taxes $0 ($46,000) $39,250 $50,500 $75,500 $75,500 $75,500

Taxes @ 34% $0 $0 $0 $14,875 $25,670 $25,670 $25,670

Net Income $0 ($46,000) $39,250 $35,625 $49,830 $49,830 $49,830

Taxable Income $0 ($46,000) ($6,750) $43,750 $75,500 $75,500 $75,500

Average Daily Sales $1,507 $1,849 $2,192 $2,466 $2,466 $2,466

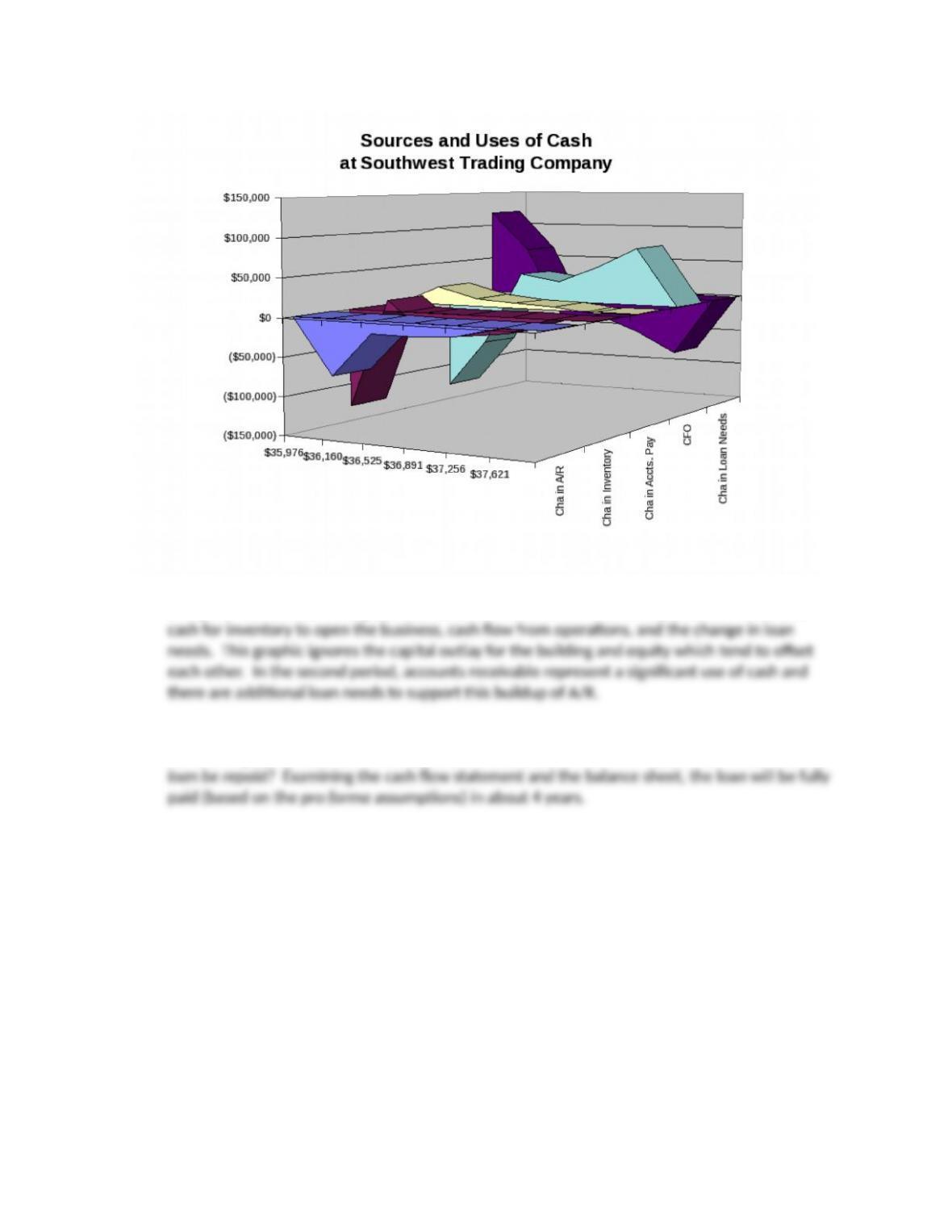

3. What was the loan need for? This was a working capital loan and the original $120,000 was

Using the Sources and Uses graph above, one will notice the relationship between the use of

What is the primary source of repayment and when? Examining the cash *ow statement and

the above graphic, cash *ow from operations is clearly the source of repayment. When will the

4. Pro Forma Cash Budget

Southwest Trading Company

Pro Forma Cash Budget

06/30/08 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13

Cash Sales

Net Sales $0 $275,000 $675,000 $800,000 $900,000 $900,000 $900,000

less Change in A/R $0 ($72,329) ($16,438) ($16,438) ($13,151) $0 $0

Total Cash Receipts $0 $202,671 $658,562 $783,562 $886,849 $900,000 $900,000

Cash disbursements

COGS $0 ($173,250) ($425,250) ($504,000) ($567,000) ($567,000) ($567,000)

less change in Inventory ($130,000) $14,500 ($26,250) ($26,250) ($21,000) $0 $0

plus change in A/P $0 $24,356 $10,279 $6,041 $4,430 ($1,611) $0

Total Cash Purchases ($130,000) ($134,394) ($441,221) ($524,209) ($583,570) ($568,611) ($567,000)

Total Operating Expenses $0 ($147,750) ($210,500) ($245,500) ($257,500) ($257,500) ($257,500)

plus Depreciation $0 $14,750 $29,500 $29,500 $29,500 $29,500 $29,500

less Taxes Paid $0 $0 $0 ($14,875) ($25,670) ($25,670) ($25,670)

Total Cash Disbursements

($130,000) ($267,394) ($622,221) ($755,084) ($837,240) ($822,281) ($820,670)

Cash Flow from Operations

($130,000) ($64,723) $36,341 $28,478 $49,609 $77,719 $79,330

Capital Expenditures ($295,000) $0 $0 $0 $0 $0 $0

Change in Stock and LTD $325,000 $0 $0 $0 $0 $0 $0

Change in loan needs $120,000 $64,723 ($36,341) ($28,478) ($49,609) ($77,719) ($79,330)

Change in Cash $20,000 $0 $0 ($0) $0 $0 $0

5. What is the secondary source of repayment? Since this is a startup company, the bank will

require all the collateral they can get. They will place a lien on the building (might even structure

this as a short-term mortgage to avoid a business homestead law), inventory and A/R. Even at a

substantial discount, there would be suffcient collateral.

Southwest Trading Company

Pro Forma Collateral Schedule

06/30/08 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13

Collateral Schedule

Cash $20,000 $20,000 $20,000 $20,000 $20,000 $20,000 $20,000

Accounts Receivable @ 75%

$0 $54,247 $66,575 $78,904 $88,767 $88,767 $88,767

Inventory @ 75% $97,500 $86,625 $106,313 $126,000 $141,750 $141,750 $141,750

Building (historical cost 80%)

$236,000 $236,000 $236,000 $236,000 $236,000 $236,000 $236,000

Total available $353,500 $396,872 $428,888 $460,904 $486,517 $486,517 $486,517

Loan from the bank $120,000 $184,723 $148,382 $119,904 $70,294 ($7,425) ($86,755)

Excess over loan (deficit) $233,500 $212,149 $280,506 $341,000 $416,223 $493,942 $573,272

Coverage Ratio 2.95 x 2.15 x 2.89 x 3.84 x 6.92 x #N/A #N/A

6.

a. The bank would want perfect its security interest in the collateral. In addition, the bank will

b. The bank’s biggest risk is default risk. Given that new firms have a high failure rate, the

c. The structure of the loan might be a revolving line that converted to a four-year term note at the

d. If the character of the borrower and other conditions were good, the loan would be approved.

Problem II: Performance of Chem-Co Coatings

1. Cash-Based Income Statement

Net sales $861

COGS -680

Cash margin $46

Cash operating pro)t – 68

Cash #ow from operations – 84

2. Note: The problem states that sales increased by 30% from 2007 to 2008. Thus, 2007 sales =

Days Accounts Receivable = Accounts Receivable/Average Daily Sales

The Days Accounts Receivable increased signiticantly. It is taking customers 35 additional days

to pay. This deterioration results in a use of cash and may be a reflection of a more lenient

credit policy.

Inventory Turnover = COGS/Inventory

The Inventory Turnover has decreased. Inventory is not selling as quickly in 2008 as it did in

2007. This deterioration results in a use of cash and may reflect a change in inventory policy.

Days Accounts Payable = Accounts Payable/[(COGS + ΔInventory)/365]

The Days Accounts Payable has increased. The firm is taking about )ve days longer to pay its

suppliers. This change results in a source of cash and may reflect a change in trade credit

policy.

The overall decrease in cash was caused by a combination of a change in credit policy,

3. Because cash *ow from operations is negative, the firm is in trouble. It borrowed an

additional $117 from the bank and essentially used the proceeds to cover an operating cash

4. The firm appears to have increased its accounts receivable and inventory too much as these