Answers to End of Chapter Questions

1. Liquidity risk (low to high):

a. DDAs, NOWs, MMDAs, small time deposits, Federal Home Loan Bank

b. Cost (low to high):

2. Core deposits represent relatively stable sources of funds. When rates change, few deposits

will leave the bank in search of higher yields relative to volatile liabilities. Thus, the interest

elasticity of core deposits is much lower than that for volatile liabilities. The key factor in

Break even deposit balance (X):

When checks are not returned, the account is labeled as ‘truncated.’ Most students will not

keep balances nearly as high as the break-even amount of $1,575. Banks make a profit on

4. Reasonable: there is a cost in officer time to research balance inquiries.

5. Eurodollars

a. TIB: asset: Eurodollar deposit at Barclays; reduces demand deposit at NY Money

Center

b. Barclays Bank:

c. Bank of England:

d. NY Money Center Bank:

6. Variable rate CD over fixed-rate CD: Expect market interest rates to rise, or as a hedger you

7. Insured deposits

a. no uninsured deposits

8. Average (A) or marginal (M)

a. M

9. Loan rates would generally not be set at market rates. If interest rates were rising, the historical rate

10. Servicing costs are highest on transactions accounts because checks are costly to process. The

11. Effective marginal cost of the CD:

1 – .00

12. The marginal weighted average cost of funds reflects the risk of the bank. A loan of average risk

might be of the same risk as the bank and thus need no adjustment for risk. However, it is possible

13. Vault cash: to meet customer withdrawals

Demand deposits held at the Federal Reserve: to meet clearing needs and reserve

14. Absent a substitute check authorized under Check 21, a bank needs to verify that a

deposited check is good in that there are funds supporting it. A hold reduces the risk of loss

15. Core deposits are deposits that a bank can reasonably expect to retain, regardless of changes

in interest rates and general economic activity. Core deposits are often measured as a bank’s

16. Impact on deposit balances

a. decrease

b. decrease

17. Banks pledge collateral against borrowings from Federal Reserve Banks, borrowings from

Federal Home Loan Banks, public deposits (such as Treasury tax and loan accounts), and

securities sold under agreement to repurchase (RPs). The qualifying collateral is determined

18. Banks that assume large amounts of credit or interest rate risk accept greater volatility in

19. Lowest risk to highest risk:

a. local schoolchildren

20. Banks that maintain their deposit base typically offer a full range of quality service so that

moving an account is costly in terms of effort, time, and entails the loss of a personal

21. If bank’s have sufficient capital, failure is not likely. In the extreme, a bank that is entirely

equity financed will not fail. Thus, capital adequacy and asset quality, which affects capital,

are essential to maintaining bank liquidity. The sequence of events leading to failure starts

Problems

Analyzing Profitability

1. Low-balance customer

2. High-balance customer (Personal checking)

a. Monthly expense on the NOW account: $0.1073(21) + $0.2188(13) + $0.16(4) +

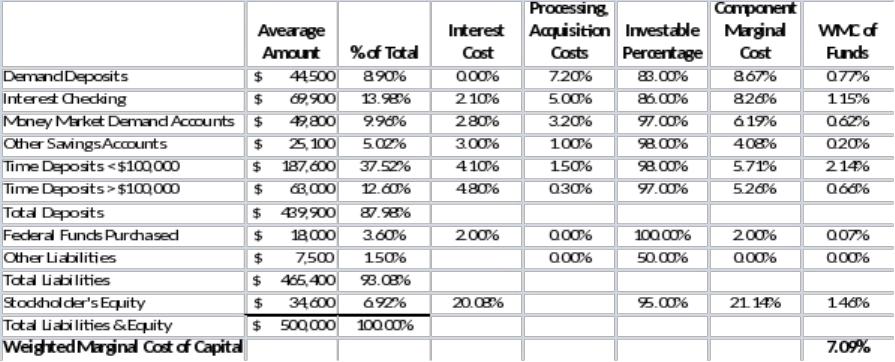

Weighted marginal cost of funds for Northwestern National Bank