Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

155

CHAPTER 11

FIXEDINCOME PORTFOLIO

MANAGEMENTPART I

SOLUTIONS

1 . e tracking risk is the standard deviation of the active returns. For the data shown in the

problem, the tracking risk is 28.284 bps, as shown below:

Period

Portfolio

Return

Benchmark

Return Active Return

(AR – Avg.

AR)

2

1 14.10% 13.70% 0.400% 0.00090%

2 . e portfolio is more sensitive to changes in the spread because its spread duration is

3.151 compared with the benchmark’s 2.834. e portfolio’s higher spread duration is

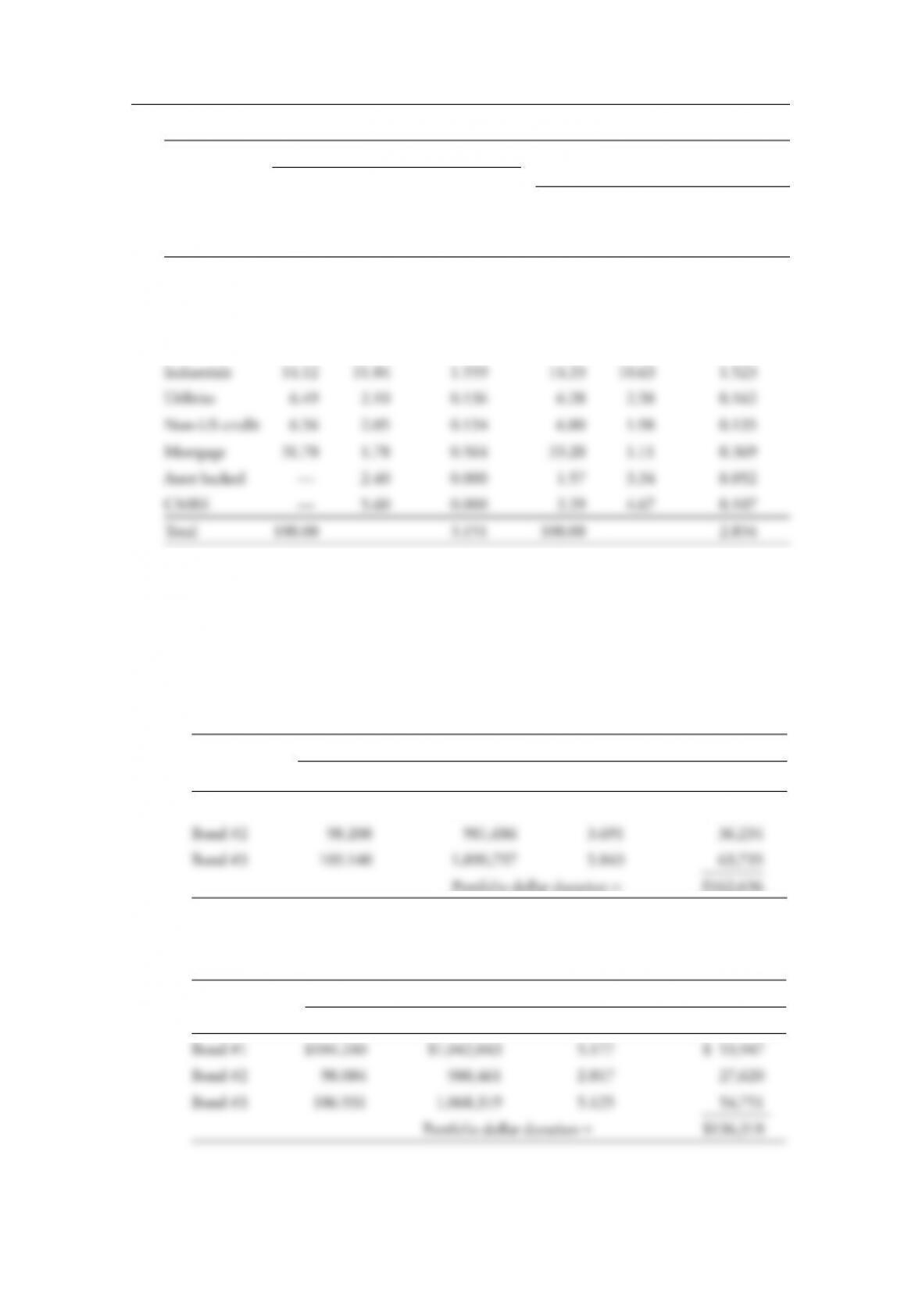

156 Part II: Solutions

Portfolio

Benchmark

Sector

% of

Portfolio

Spread

Duration

Contribution to

Spread

Duration

% of

Portfolio

Spread

Duration

Contribution to

Spread Duration

Treasury 22.70 0.00 0.000 23.10 0.00 0.000

Agencies 12.20 4.56 0.556 6.54 4.41 0.288

Financial

institutions

6.23 3.23 0.201 5.89 3.35 0.197

3 . Dollar duration is a measure of the change in portfolio value for a 100 bps change in

market yields. It is de ned as

Dollar duration = Duration × Dollar value × 0.01

A . A portfolio’s dollar duration is the sum of the dollar durations of the component secu-

rities. e dollar duration of this portfolio at the beginning of the period is $162,636,

which is calculated as

Initial Values

Security Price Market Value Duration Dollar Duration

Bond #1 $106.110 $1,060,531 5.909 $ 62,667

At the end of one year, the portfolio’s dollar duration has changed to $136,318, as

shown below.

After 1 Year

Security Price Market Value Duration Dollar Duration

Chapter 11 Fixed-Income Portfolio Management—Part I 157

B . e rebalancing ratio is a ratio of the original dollar duration to the new dollar

duration:

C . e portfolio requires each position to be increased by 19.3 percent. e cash required

this problem, (0.4774 × 5.50) + (0.1479 × 5.80) + (0.1235 × 4.50) + (0.2512 × 4.65) =

5.20735. Round to 5.21.

result of a change in the spread between the security and a Treasury. e portfolio spread

duration is the weighted average duration of those securities in the portfolio that have a

yield above the default-free yield (i.e., non-Treasuries). In this problem, the agencies, cor-

porates, and mortgage-backed securities have a spread. Using their original weights in the

2.58165. Round to 2.58.

dramatically from those of the index and that the durations of the portfolio components

di er from their respective durations in the index. us the manager is using active manage-

ment because he had both duration and sector mismatches and not on a small scale.

that for equities. Alonso is incorrect in identifying this as a limiting factor. Information

(data) for the other two factors can be impossible to acquire.

by using the current price of 100.40625 ( Exhibit 2 ), Alonso’s forecast of 99.50, and a

semi-annual coupon of 2.0625. e problem informs that there is zero accrued interest.

10-year Treasuries because his stated desire is to maintain the dollar duration of the port-

folio. e sale price of $10 million par value of the 5-year bond is found by multiplying

duration of the 10-year and its quoted price and 0.01 to get the par value of the 10-year.

e result is $454,840.31/(8.22 × 1.0909375 × 0.01) = $5,072,094.

all risks. Credit risk destroys the immunization match; therefore, the statement is incor-

rect. e risk to immunization comes from non-parallel shifts in the yield curve.

more reinvestment rate risk than Portfolio B.

pounding). Find the time ten future value of $100 million at this rate. e answer is

versus multiple liabilities immunization.

158 Part II: Solutions

bilities, the durations of the assets after a parallel yield curve shift (whether up or down)

will envelope the durations of the liabilities after the shift. e immunization can be

maintained, although rebalancing may be necessary.

straint that it be cash- ow-matched in the rst few years. Cash ow matching the initial

portion of the liability stream reduces the risk associated with nonparallel shifts of the

yield curve.