Chapter 20

Questions 1 & 2

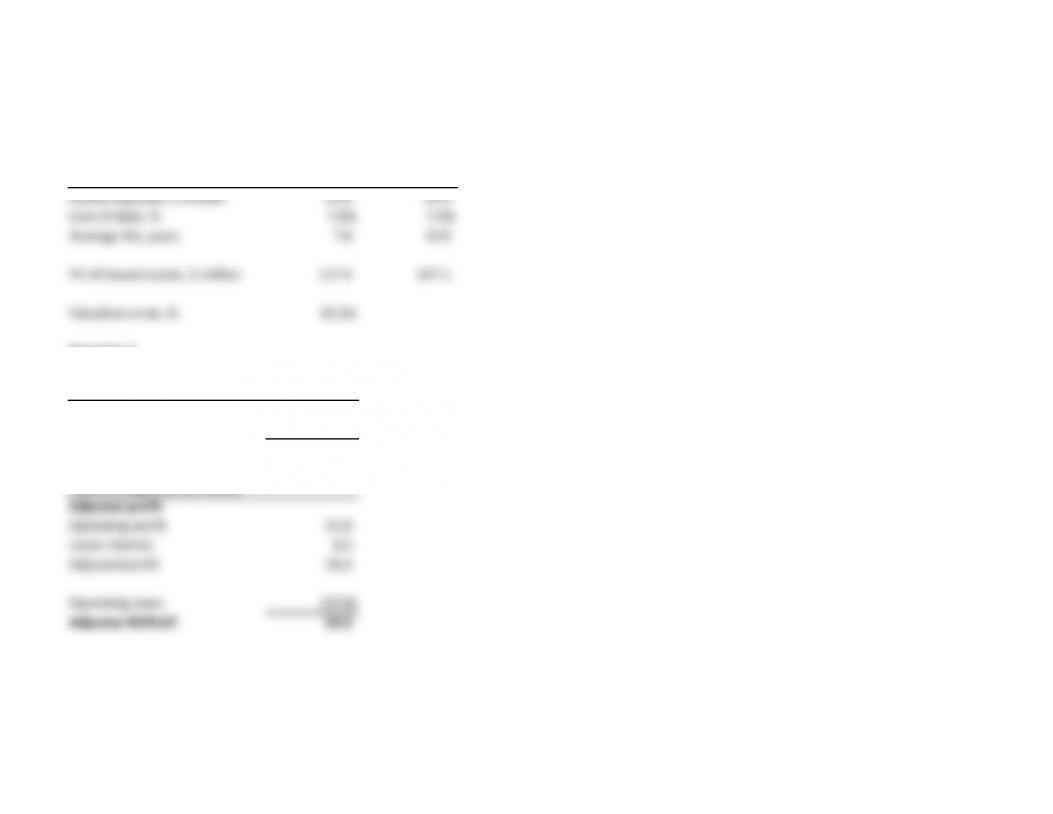

PV of leased assets Correct Misestimated

Rental expenses, $ million 25.0 25.0

Cost of debt, % 7.0% 7.0%

Average life, years 7.0 10.0

PV of leased assets, $ million 117.4 147.1

Valuation error, % 25.2%

Question 2

$ million

NOPLAT, direct from financial statements Operating

Operating profit 25.0 tax rate, %

Operating taxes (7.5) 30.0%

NOPLAT 17.5

NOPLAT, adjusted for leases

Adjusted profit

Operating profit 25.0

Lease interest 8.2

Adjusted profit 33.2

Operating taxes (10.0)

Adjusted NOPLAT 23.3

Chapter 20

Question 3

Using the present value of reported rental expenses systematically undervalues the asset, since it ignores the residual value returned at

the end of the lease contract. As stated in the text, most would agree that a $1 million asset leased for two years is worth more than the

present value of two payments of $100,000 per year.

Chapter 20

Question 4

Due to liberal accounting policies, if a firm sold its receivables, they were taken off of the balance sheet. This improved closely scrutinized operating

metrics like operating cash flow and ROIC.

After the financial crisis, accounting policies became stricter, and securitized receivables were classified as secured borrowing. Coupled with tighter

credit policies from banks, this substantially reduced the receivables securitization programs.

Chapter 20

Question 5

AutoCo

Income statement

$ million

Year 1 Year 2 Year 3

Operating income 15,000 15,500 16,000

Pension expense 5 45 (40)

Service expense (300) (365) (365)

Prior service cost (credit) amortization 20 020

Adjusted operating income 14,705 15,180 15,595

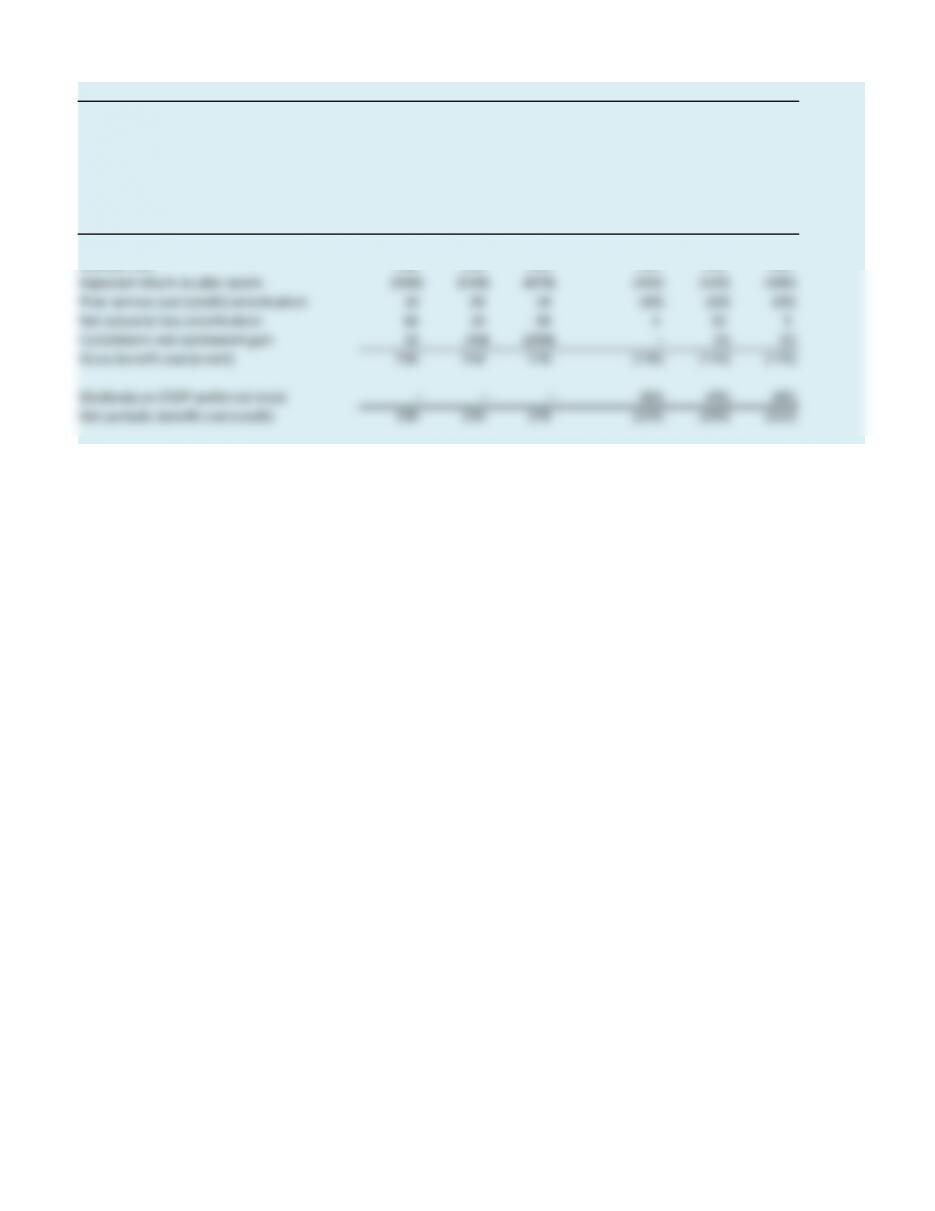

AutoCo, annual report, Note 10

Postretirement benefits and employee stock ownership plan

$ million

Year 1 Year 2 Year 3 Year 1 Year 2 Year 3

Service cost 210 270 280 90 95 85

Interest cost 450 520 500 250 230 220

Expected return on plan assets (500) (530) (470) (450) (420) (400)

Prior service cost (credit) amortization 10 20 10 (30) (20) (30)

Net actuarial loss amortization 50 10 50 510 5

Curtailment and settlement gain 10 (40) (200) –(5) (5)

Gross benefit cost (credit) 230 250 170 (135) (110) (125)

Dividends on ESOP preferred stock ––– (90) (95) (85)

Net periodic benefit cost (credit) 230 250 170 (225) (205) (210)

Other retiree benefits

Pension benefits

Chapter 20

Question 5

No, this does not mean that the plan is fully funded. Many firms will consolidate prepaid pension assets into accounts like “other long-term assets.”

Unfunded pension liabilities are often included in “other long-term liabilities.” This points to the importance of reading the pension footnote to

find the true nature of pension obligations and to remove nonoperating assets or liabilities from accounts on the balance sheet that might be deemed part

of invested capital.

Exhibit 20.10 AutoCo Annual Report

AutoCo: Annual report, Note 10

Postretirement benefits and employee stock ownership plan

Year 1 Year 2 Year 3 Year 1 Year 2 Year 3

Service cost 210 270 280 90 95 85

Interest cost 450 520 500 250 230 220

Expected return on plan assets (500) (530) (470) (450) (420) (400)

Prior service cost (credit) amortization 10 20 10 (30) (20) (30)

Net actuarial loss amortization 50 10 50 510 5

Curtailment and settlement gain 10 (40) (200) –(5) (5)

Gross benefit cost (credit) 230 250 170 (135) (110) (125)

Dividends on ESOP preferred stock – – – (90) (95) (85)

Net periodic benefit cost (credit) 230 250 170 (225) (205) (210)

Pension benefits

Other retiree benefits