Chapter 14

Question 1

$ billion

Initial estimate

Overseas tax

estimate

Revenues 50 50

Cash on balance sheet 60 60

Cash from overseas 40 40

Tax due – (12)

After-tax amount 60 48

Cash needed for operations 1 1

Excess–cash estimate 59 47

Overseas profit tax rate, % 30.00%

Comment: Initially, one might assume that the balance sheet cash was from domestic profits, which have already had taxes collected.

Thus, the estimates might be $1 billion for cash needed for operations and $59 billion for excess cash and marketable securities.

However, once one realizes that this is largely cash from overseas profits, one would want to discount the cash for the impact of taxes.

The choice of a tax rate is not easy. One might choose bounds between the high of the current top corporate tax rate and the low of

some estimated “tax holiday” rate, as has been done in the past. This would lower the estimated value of the firm.

In the case illustrated in this answer, with a tax rate of 30 percent, the estimated value of the firm comes down by $12 billion.

Chapter 14

Questions 2 & 3 Question 2 Question 3

$ million $ million

Valuation, $ million No sale Sale Nonconsolidated subsidiary Contingent claim

Value of operations 2,500 2,500 Nonconsolidated subsidiary 500 Contingent claim 100

Nonconsolidated subsidiary 100 85 Times: % ownership 20% Times: Probability of occurrence, % 10%

Enterprise value 2,600 2,585 Value to MarineCo 100 Expected claim 10

Unfunded pension liabilities (200) Gain on sale After-tax cash to MarineCo

Contingent claim (7) Market value 100 Expected claim 10

Equity value 2,393 Book value (50) Tax deduction (3)

Gain on sale 50 After-tax expected claim 7

Key data After-tax cash to MarineCo

Marginal tax rate, % 30% Market value 100

Taxes on sale at 30% (15)

After-tax cash to MarineCo 85

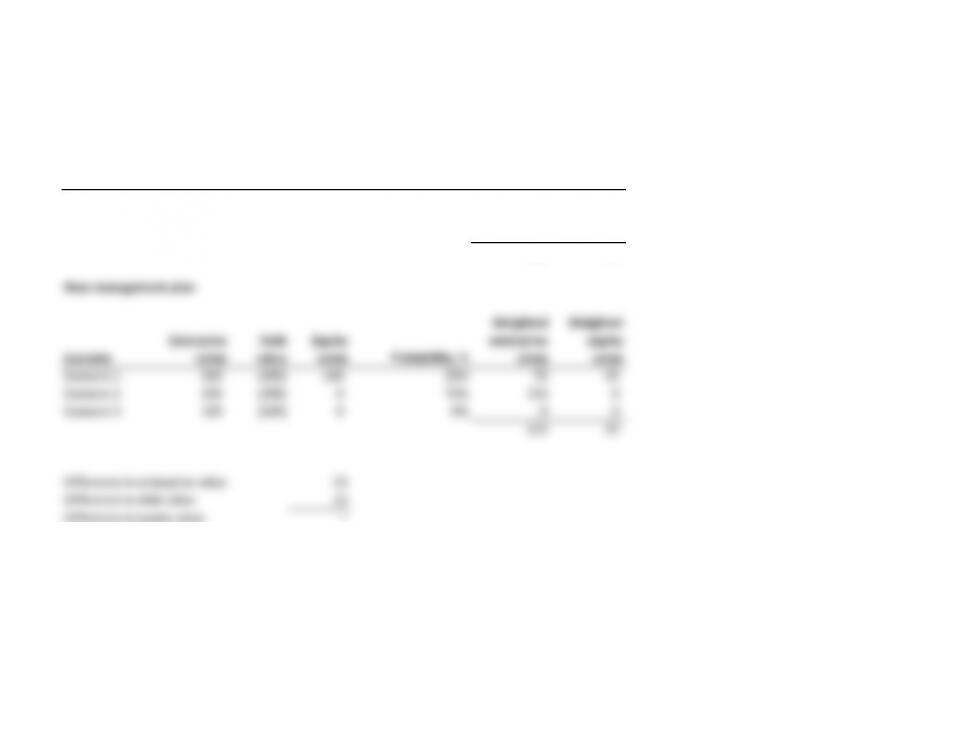

Chapter 14

Question 4

$ million

Debt amount -200

Weighted Weighted

Enterprise Debt Equity enterprise equity

Scenario value value value Probability, %value value

Scenario 1 300 (200) 100 25% 75 25

Scenario 2 200 (200) 0 50% 100 0

Scenario 3 100 (100) 0 25% 25 0

200 25

New management plan

Weighted Weighted

Enterprise Debt Equity enterprise equity

Scenario value value value Probability, %value value

Scenario 1 300 (200) 100 25% 75 25

Scenario 2 200 (200) 0 75% 150 0

Scenario 3 100 (100) 0 0% 0 0

225 25

Difference in enterprise value

25

Difference in debt value 25

Difference in equity value –

The entire value increase accrues to the debt holders, a common problem with distressed companies,

as debt holders now have a 100 percent likelihood of being repaid in full.

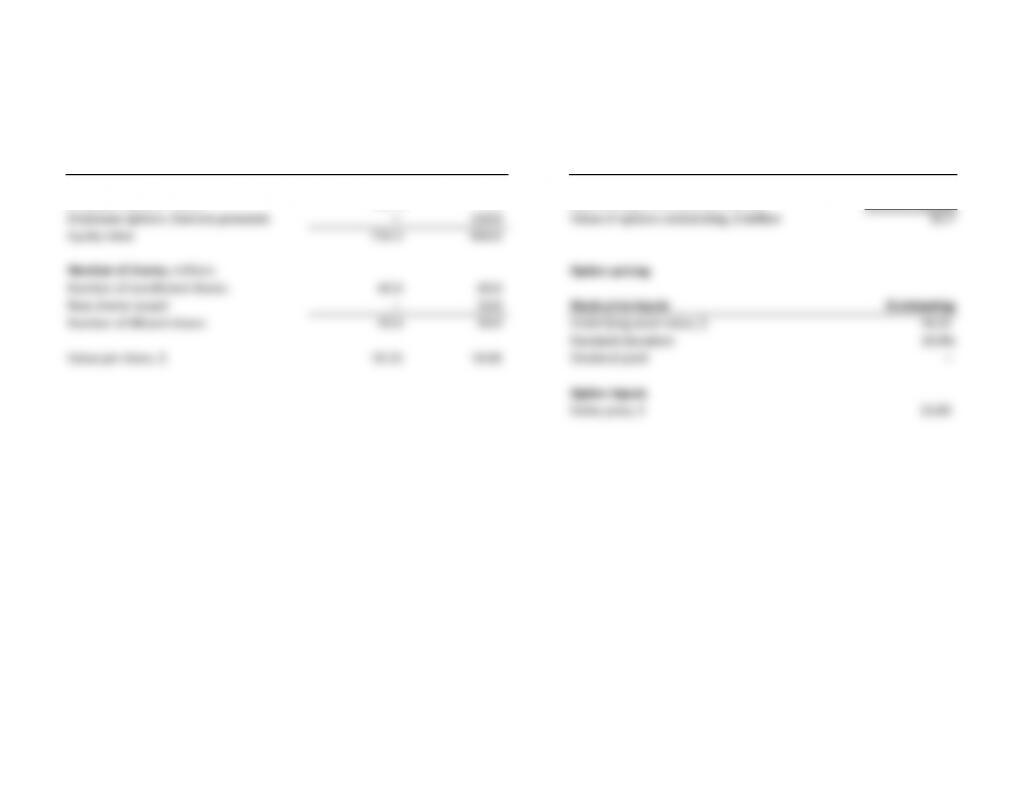

Chapter 14

Question 5

Value of Exercise

outstanding value

$ million options approach Option data Outstanding

Enterprise value 800.0 800.0 European call value, $ 6.67

Employee options: Value (66.7) – Outstanding at end of year, millions 10.00

Employee options: Exercise proceeds – 150.0 Value of options outstanding, $ million 66.7

Equity value 733.3 950.0

Number of shares, millions Option pricing

Number of nondiluted shares 40.0 40.0

New shares issued – 10.0 Stock price inputs Outstanding

Number of diluted shares 40.0 50.0 Underlying asset value, $ 18.33

Standard deviation 10.0%

Value per share, $ 18.33 19.00 Dividend yield –

Option inputs

Strike price, $ 15.00

Comment: Note that the exercise method will understate the value of the options, as it ignores the time value of the options.

Understating the value of the options will overstate the value of the firm’s equity.

Chapter 14

Question 6

Market Conversion

value value

$ million approach approach Option data Outstanding

Enterprise value 10,000 10,000 Convertible bond value, $ 1,150

Convertible debt (115) – Outstanding at end of year 100,000

Value of outstanding convertible debt, $ 115,000,000

Equity value 9,885 10,000

Number of shares, millions

Number of nondiluted shares 500.0 500.0

New shares issued – 0.1

Number of diluted shares 500.0 500.1

Value per share, $ 19.77 20.00

Comment: Note that the conversion method will understate the value of the bond, ignoring the time value of the option feature.

Understating the value of the bonds will overstate the value of the firm‘s equity.