Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 19

Question 1

The three steps are:

(1) Separate operating from nonoperating items, treating items that grow in line with revenues and are related to the core business as operating.

(2) Search the footnotes for embedded one-time items.

(3) Analyze each nonoperating item to assess how it affects the future operations of the firm.

Chapter 19

Question 2

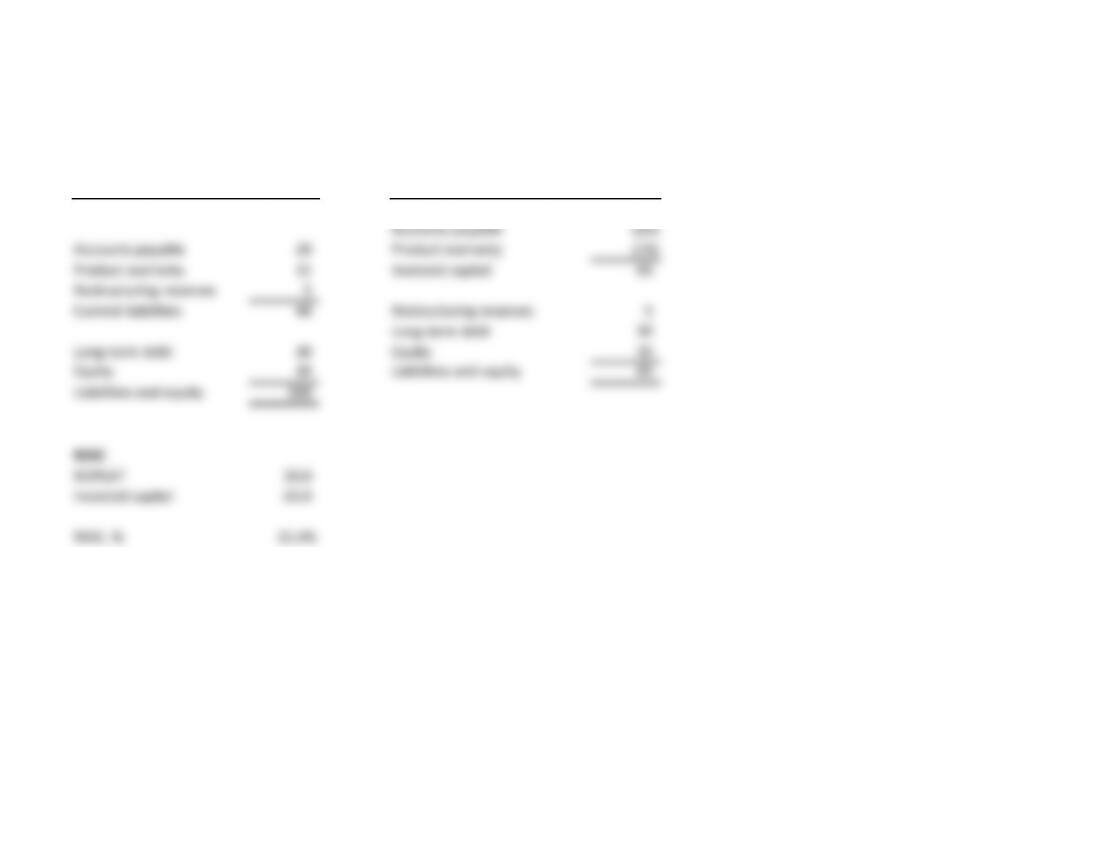

$ million

Balance sheet Reorganized financial statements

Operating assets 100 Operating assets 100

Accounts payable (20)

Accounts payable 20 Product warranty (15)

Product warranty 15 Invested capital 65

Restructuring reserves 5

Current liabilities 40 Restructuring reserves 5

Long-term debt 30

Long-term debt 30 Equity 30

Equity 30 Liabilities and equity 65

Liabilities and equity 100

ROIC

NOPLAT 10.0

Invested capital 65.0

ROIC, % 15.4%

Chapter 19

Question 3

Year 0 Year 1 Year 2

Revenues –100 100

Operating costs –(80) (90)

Litigation provision –(10) 5

Net income –10 15

Today Year 1 Year 2

Cash 50 70 75

Inventory 50 50 50

Total assets 100 120 125

Litigation reserve 10 0

Equity 100 110 125

Liabilities and equity 100 120 125

Return on equity, % –9% 12%

Comment:

The return on equity is distorted by the litigation expense because it doesn't correspond to cash outflows pertaining to the case.

In year 1, there is no cash outflow for the case, yet net income is pulled down by the provision for this litigation. In year 2, net

income is inflated by the gain on the litigation expense, due to the resolution cost being less than expected.

Chapter 19

Question 4

The treatment of consecutive restructuring charges is a judgment call. The key assessment is whether or not the restructuring charges

will continue and whether or not they are cash. For instance, many restructuring charges are layoffs and asset write-offs. To forecast cash

flow, determine the level of future severance and any tax impacts from asset write-offs. These should be included in the valuation.

Chapter 19

Question 5

Some of the more common nonoperating items and one-time charges include amortization of acquired intangibles, asset write-offs

including write-offs of goodwill and purchased R&D, restructuring charges, litigation charges, and gains and losses on asset sales.