Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 18

Question 1

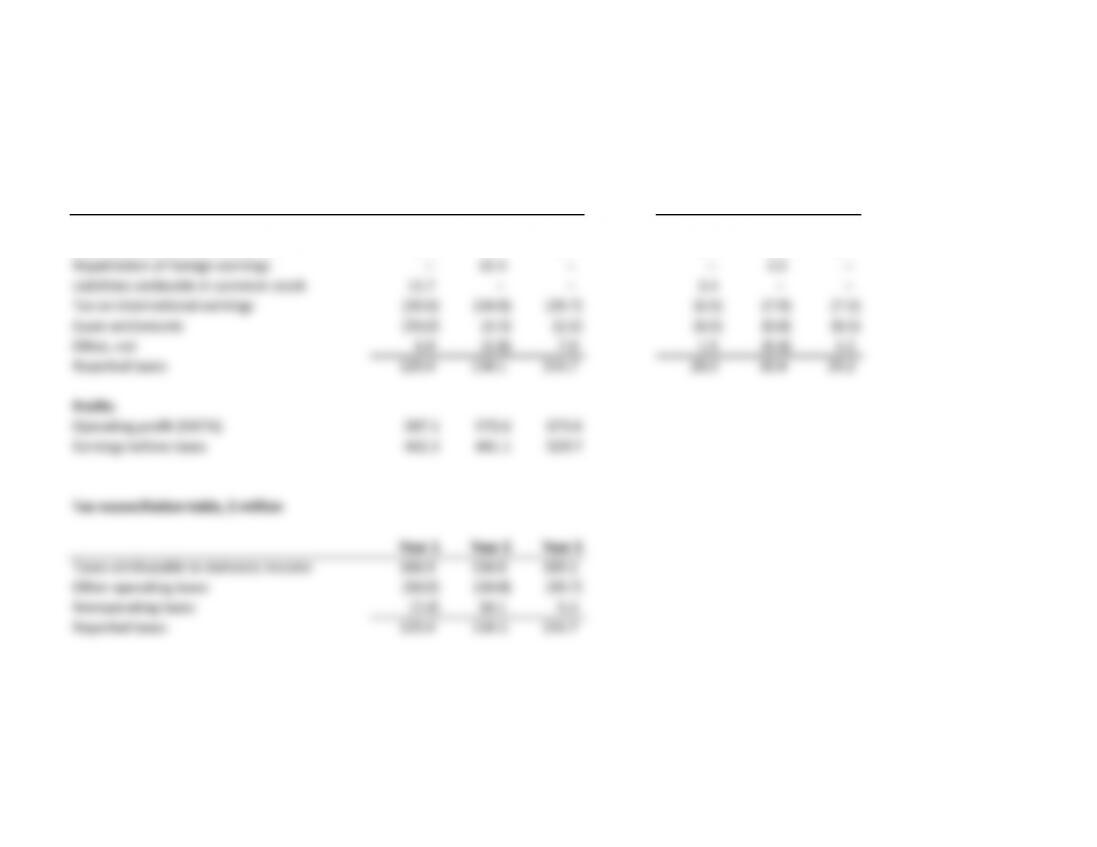

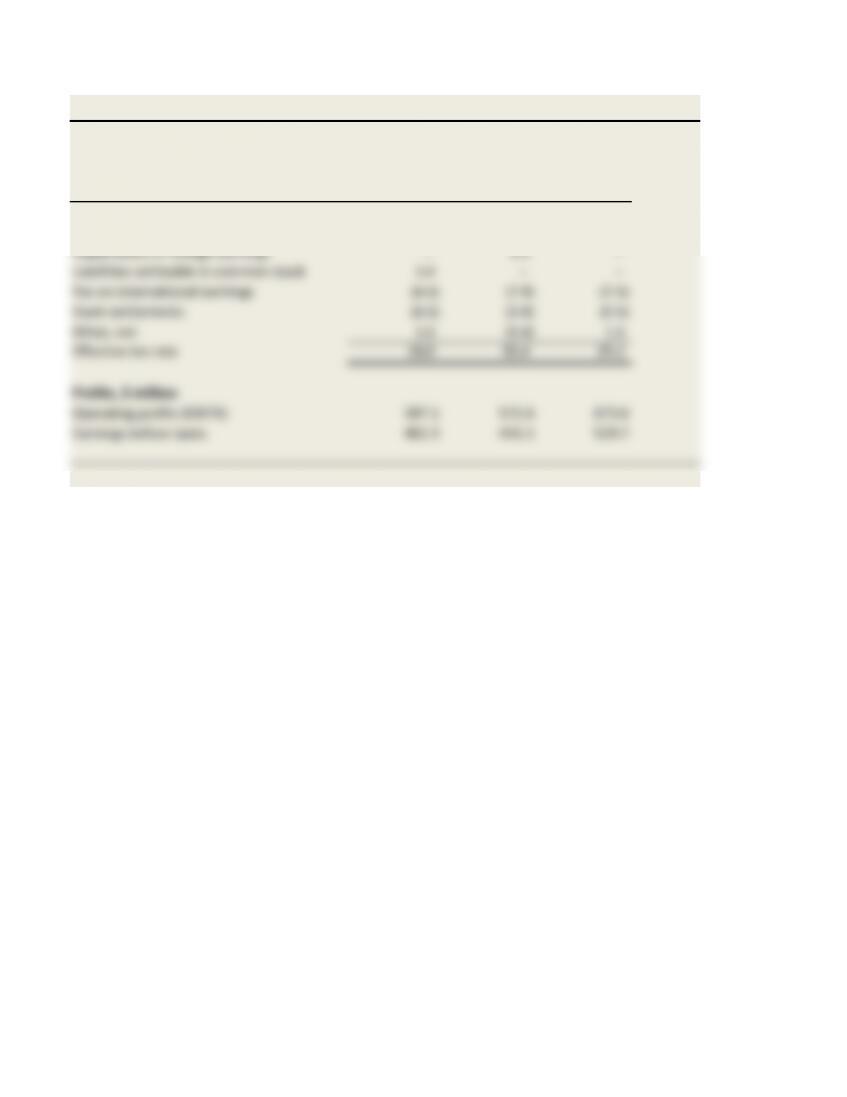

Tax reconciliation table, $ million Tax reconciliation table, %

Year 1 Year 2 Year 3 Year 1 Year 2 Year 3

Statutory income tax rate 161.8 154.4 185.4 35.0 35.0 35.0

State and local income taxes, net 5.1 4.4 3.7 1.1 1.0 0.7

Repatriation of foreign earnings – 15.4 – – 3.5 –

Liabilities settleable in common stock 15.7 – – 3.4 – –

Tax on international earnings (30.0) (34.8) (39.7) (6.5) (7.9) (7.5)

Exam settlements (30.0) (3.5) (2.6) (6.5) (0.8) (0.5)

Other, net 6.9 (1.8) 7.9 1.5 (0.4) 1.5

Reported taxes 129.4 134.1 154.7 28.0 30.4 29.2

Profits

Operating profit (EBITA) 587.1 572.6 673.6

Earnings before taxes 462.3 441.1 529.7

Tax reconciliation table, $ million

Year 1 Year 2 Year 3

Taxes attributable to domestic income 166.9 158.8 189.1

Other operating taxes (30.0) (34.8) (39.7)

Nonoperating taxes (7.4) 10.1 5.3

Reported taxes 129.4 134.1 154.7

Chapter 18

Question 2

Panel A Panel B

Assumption: Nonoperating items recognized domestically Assumption: Nonoperating items recognized globally

$ million $ million

Year 1 Year 2 Year 3 Year 1 Year 2 Year 3

Statutory tax rate, % 36.1 36.0 35.7 Blended global rate, % 29.6 28.1 28.2

x EBITA 587.1 572.6 673.6 x EBITA 587.1 572.6 673.6

Statutory taxes on EBITA 211.9 206.1 240.5 Global taxes on EBITA 173.8 160.9 190.0

Tax on international earnings (30.0) (34.8) (39.7) Other operating taxes – – –

Estimated operating taxes 181.9 171.3 200.7 Estimated operating taxes 173.8 160.9 190.0

Tax rates, % Tax rates, %

Statutory tax rate 36.1 36.0 35.7 Statutory tax rate 36.1 36.0 35.7

Effective tax rate 28.0 30.4 29.2 Effective tax rate 28.0 30.4 29.2

Operating tax rate 31.0 29.9 29.8 Operating tax rate 29.6 28.1 28.2

Chapter 18

Question 3

Companies can avoid high domestic tax rates by maintaining earnings in foreign countries indefinitely. For some companies,

this has led to large cash balances abroad. For instance, Apple Corporation held 88 percent of its $155 billion in cash and

equivalents overseas as of 2014, according to the Financial Times . If a company repatriates earnings, tax law requires that

the company pay the difference between local and foreign taxes. But will it? In 2004, the United States passed a temporary

law allowing companies to repatriate earnings at just 5.25 percent, which is less than most cross-country differentials.

For companies that repatriate in a given year, we do not recommend treating the repatriation as operating. This will distort

the ongoing tax rate for use in performance appraisal and forecasting. If you decide to treat the repatriation as operating, the

tax should be spread over the years incurred.

Chapter 18

Question 4

Reorganizing deferred taxes Cash tax rate

$ million

Year 1 Year 2 Year 3 Operating cash taxes, $ million Year 2 Year 3

Operating DTAs, net of operating DTLs

Accounts receivable 20.5 16.8 17.3 Operating taxes 171.3 200.7

Inventories 24.6 20.2 15.9 Deferred taxes (81.9) (2.6)

Depreciation of long-lived assets (47.7) (121.5) (120.3) Operating cash taxes 89.4 198.1

Operating DTAs, net of operating DTLs (2.6) (84.5) (87.1)

Operating profit 572.6 673.6

Nonoperating DTAs, net of nonoperating DTLs Tax rates, %

Losses and tax credit carryforwards 39.1 34.4 29.6 Operating tax rate 29.9% 29.8%

Pension 10.0 34.1 26.6 Percent deferred 47.8% 1.3%

Convertible debentures (40.2) (47.6) (56.8) Operating cash tax rate 15.6% 29.4%

Equity method investment - - (26.9)

Nonoperating DTAs, net of nonoperating DTLs 8.9 20.9 (27.5)

Deferred-tax assets, net of liabilities 6.3 (63.6) (114.6)

Check 6.3 (63.6) (114.6)

Chapter 18

Question 5

ToyCo: Total funds invested

$ million

Total funds invested: Uses

Working capital 400.0

Fixed assets 800.0

Invested capital 1,200.0

Tax credit carryforwards 29.6

Total funds invested 1,229.6

Total funds invested: Sources

Debt 600.0

Pension obligations (26.6)

Debt and debt equivalents 573.4

Operating DTLs, net of DTAs 87.1

Nonoperating DTLs, net of DTAs 83.7

Equity 485.4

Equity and equity equivalents 656.2

Total funds invested 1,229.6

Chapter 18

Question 6

When companies grow, they add fixed assets. By using accelerated depreciation on the tax books for new assets, companies can defer taxes.

These deferrals are likely to be highest when organic growth is high. As growth falls and new equipment merely replaces old equipment,

deferrals will drop. In fact, cash taxes can be higher than reported taxes when growth is negative. The company may not pay this higher

rate, however, as shrinking companies often generate losses and consequently do not pay taxes.

EXHIBIT 18.10 ToyCo: Tax Reconciliation Table

%

Year 1 Year 2 Year 3

Statutory income tax rate 35.0 35.0 35.0

State and local income taxes, net 1.1 1.0 0.7

Repatriation of foreign earnings – 3.5 –

Liabilities settleable in common stock 3.4 – –

Tax on international earnings (6.5) (7.9) (7.5)

Exam settlements (6.5) (0.8) (0.5)

Other, net 1.5 (0.4) 1.5

Effective tax rate 28.0 30.4 29.2

Profits, $ million

Operating profits (EBITA) 587.1 572.6 673.6

Earnings before taxes 462.3 441.1 529.7

EXHIBIT 18.11 ToyCo: Deferred-Tax Assets and Liabilities

$ million

Year 1 Year 2 Year 3

Deferred-tax assets

Accounts receivable 20.5 16.8 17.3

Inventories 24.6 20.2 15.9

Losses and tax credit carryforwards 39.1 34.4 29.6

Pension 10.0 34.1 26.6

Deferred-tax assets 94.2 105.5 89.4

Deferred-tax liabilities

Convertible debentures 40.2 47.6 56.8

Depreciation of long-lived assets 47.7 121.5 120.3

Equity method investment - - 26.9

Deferred-tax liabilities 87.9 169.1 204.0