PROBLEM 9-5A (Continued)

Cost $500,000

Accum. depreciation—

(b) Dec. 31 Depreciation Expense ………………… 570,000

31 Depreciation Expense ………………… 4,800,000

(c) GRAND COMPANY

Partial Balance Sheet

December 31, 2016

Plant Assets*

Land …………………………………………….. $ 5,730,000

Buildings ………………………………………. $28,500,000

Less: Accumulated depreciation—

*See T-accounts which follow.

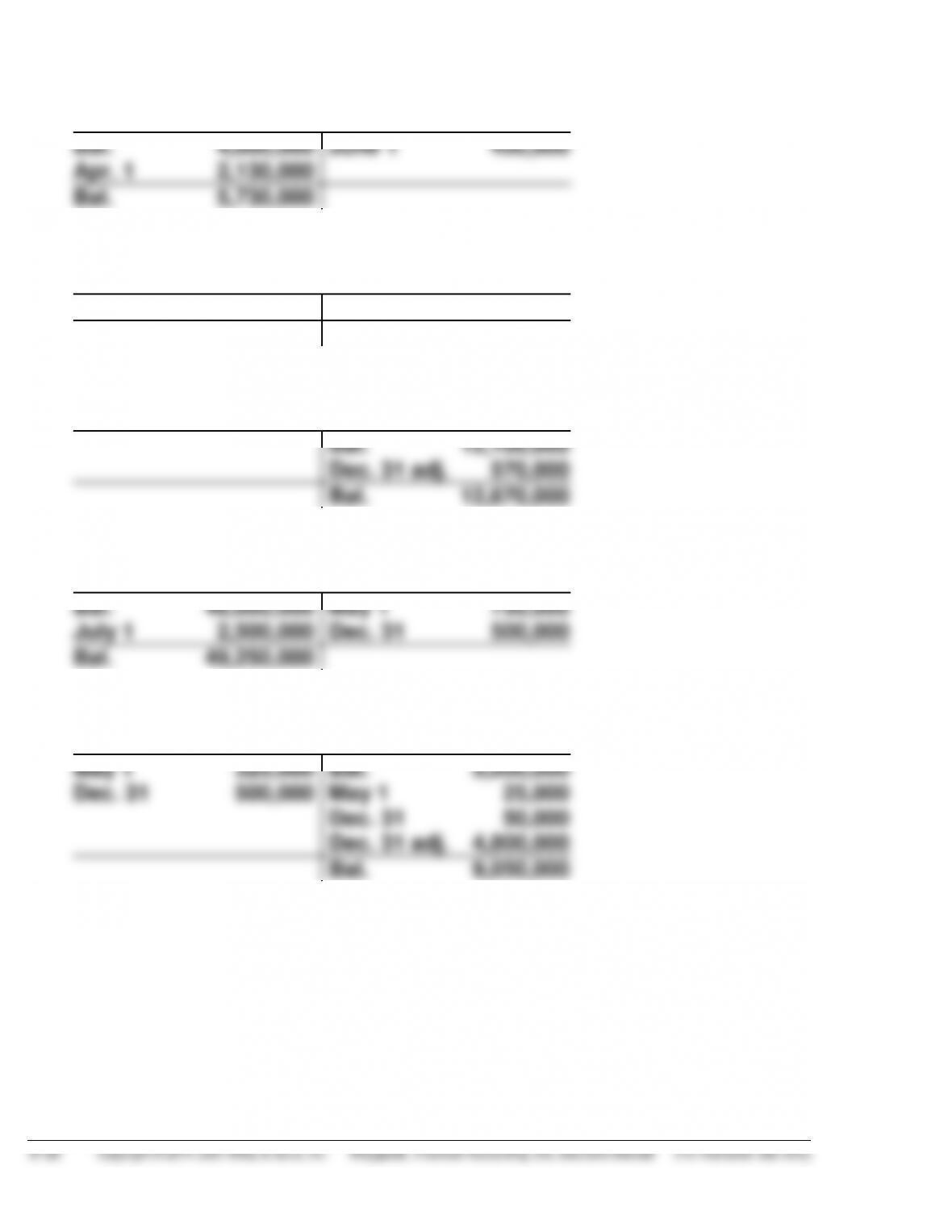

PROBLEM 9-5A (Continued)

Land

Bal. 4,000,000

Apr. 1 2,130,000

June 1 400,000

Bal. 5,730,000

Buildings

Bal. 28,500,000

Bal. 28,500,000

Accumulated Depreciation—Buildings

Bal. 12,100,000

Dec. 31 adj. 570,000

Bal. 12,670,000

Equipment

Bal. 48,000,000

July 1 2,500,000

May 1 750,000

Dec. 31 500,000

Bal. 49,250,000

Accumulated Depreciation—Equipment

May 1 325,000

Dec. 31 500,000

Bal. 5,000,000

May 1 25,000

Dec. 31 50,000

Dec. 31 adj. 4,800,000

Bal. 9,050,000

PROBLEM 9-6A

(a) Accumulated Depreciation—Equipment ……………… 50,000

(b) Cash ……………………………………………………….………… 21,000

(c) Cash ……………………………………………………….………… 31,000

PROBLEM 9-7A

(a) Jan. 2 Patents …………………………………………….. 27,000

Jan.– Research and Development

June Expense ……………………………………….. 140,000

Sept. 1 Advertising Expense …………………………. 50,000

Oct. 1 Franchises ……………………………………….. 140,000

(b) Dec. 31 Amortization Expense ……………………….. 10,000

31 Amortization Expense ……………………….. 5,500

(c) Intangible Assets

Patents ($97,000 cost – $17,000 amortization) (1) …………… $ 80,000

PROBLEM 9-8A

1. Research and Development Expense ………………. 136,000

Patents ………………………………………………………….. 13,600

Amortization Expense

2. Goodwill ………………………………………………………… 920

Note: Goodwill should not be amortized because it has an indefinite life unlike

Patents.

PROBLEM 9-9A

(a)

LaPorta

Lott

Asset turnover

$1,300,000

$2,500,000

= .52 times

$1,180,000

$2,000,000

= .59 times

PROBLEM 9-1B

Item

Land

Buildings

Other Accounts

1

2

3

4

5

6

7

8

9

10

($ 5,000)

100,000

( 27,000)

( (3,500)

($128,500)

$490,000

19,000

9,000

$518,000

$ 7,500 Property Tax Expense

18,000 Land Improvements

6,000 Land Improvements

PROBLEM 9-2B

(a)

Year

Computation

Accumulated

Depreciation

12/31

MACHINE 1

2012

2013

2014

2015

$100,000 X 10% = $10,000

$100,000 X 10% = $10,000

$100,000 X 10% = $10,000

$100,000 X 10% = $10,000

$ 10,000

20,000

30,000

40,000

MACHINE 2

2013

2014

2015

$180,000 X 25% = $45,000

$135,000 X 25% = $33,750

$101,250 X 25% = $25,313

$ 45,000

78,750

104,063

MACHINE 3

2015

2,000 X ($110,000 ÷ 25,000) = $8,800

$ 8,800

(b)

Year

Depreciation Computation

Expense

MACHINE 2

(1)

(2)

2013

2014

$180,000 X 25% X 8/12 = $30,000

$150,000 X 25% = $37,500

$30,000

$37,500

PROBLEM 9-3B

(a) (1) Purchase price ……………………………………………………….. $ 58,000

Sales tax ………………………………………………………………… 2,750

Shipping costs ……………………………………………………….. 100

Equipment …………………………..…………………….. 61,000

(2) Recorded cost ………………………………………………………… $ 61,000

Less: Salvage value ……………………………………………….. 5,000

Depreciation Expense …………………………………. 14,000

Accumulated Depreciation—

(b) (1) Recorded cost ………………………………………………………… $120,000

Less: Salvage value ……………………………………………….. 10,000

(2)

Year

Book Value at

Beginning of

Year

DDB Rate

Annual

Depreciation

Expense

Accumulated

Depreciation

2015

2016

2017

2018

$120,000

60,000

30,000

15,000

*50%*

*50%*

*50%*

*50%*

$60,000

30,000

15,000

5,000**

$60,000

90,000

105,000

110,000

PROBLEM 9-3B (Continued)

$4.40 per unit.

Annual Depreciation Expense

2015: $4.40 X 5,500 = $24,200

reports the highest.

These facts occur because the declining-balance method is an accelerated

depreciation method in which the largest amount of depreciation is

recognized in the early years of the asset’s life. If the straight–line method

The amount of depreciation expense recognized using the units–of–activity