SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 8-1

The following entry should be prepared to increase the balance in the

Allowance for Doubtful Accounts from $6,100 credit to $15,500 credit (5% X

$310,000):

Bad Debt Expense …………………………………………….. 9,400

(To record estimate of uncollectible

accounts)

DO IT! 8-2

Cash …………………………………………………………………. 194,000

(To record sale of receivables to factor)

DO IT! 8-3

(b) The interest to be received at maturity is $186:

Cash …………………………………………………………… 6,386

DO IT! 8-4

(a)

Net credit sales

÷

Average net

accounts receivable

=

Accounts receivable

turnover

$1,300,000

÷

$101,000 + $107,000

=

12.5 times

2

(b)

Days in year

÷

Accounts receivable

turnover

=

Average collection

period in days

365

÷

12.5 times

=

29.2 days

SOLUTIONS TO EXERCISES

EXERCISE 8-1

March 1 Accounts Receivable—Dodson Company .. 5,000

3 Sales Returns and Allowances ……………….. 500

9 Cash …………………………………………………….. 4,410

Sales Discounts …………………………………….. 90

15 Accounts Receivable …………………………….. 400

31 Accounts Receivable …………………………….. 3

EXERCISE 8-2

(a) Jan. 6 Accounts Receivable—Pryor ………………….. 7,000

16 Cash ($7,000 – $140) ……………………………… 6,860

(b) Jan. 10 Accounts Receivable—Farley…………………. 9,000

Feb. 12 Cash …………………………………………………….. 5,000

Mar. 10 Accounts Receivable—Farley…………………. 40

Interest Revenue

EXERCISE 8-3

(a) Dec. 31 Bad Debt Expense ………………………… 1,400

(b) (1) Dec. 31 Bad Debt Expense

(2) Dec. 31 Bad Debt Expense ………………………… 8,900

(c) (1) Dec. 31 Bad Debt Expense

(2) Dec. 31 Bad Debt Expense ………………………… 6,800

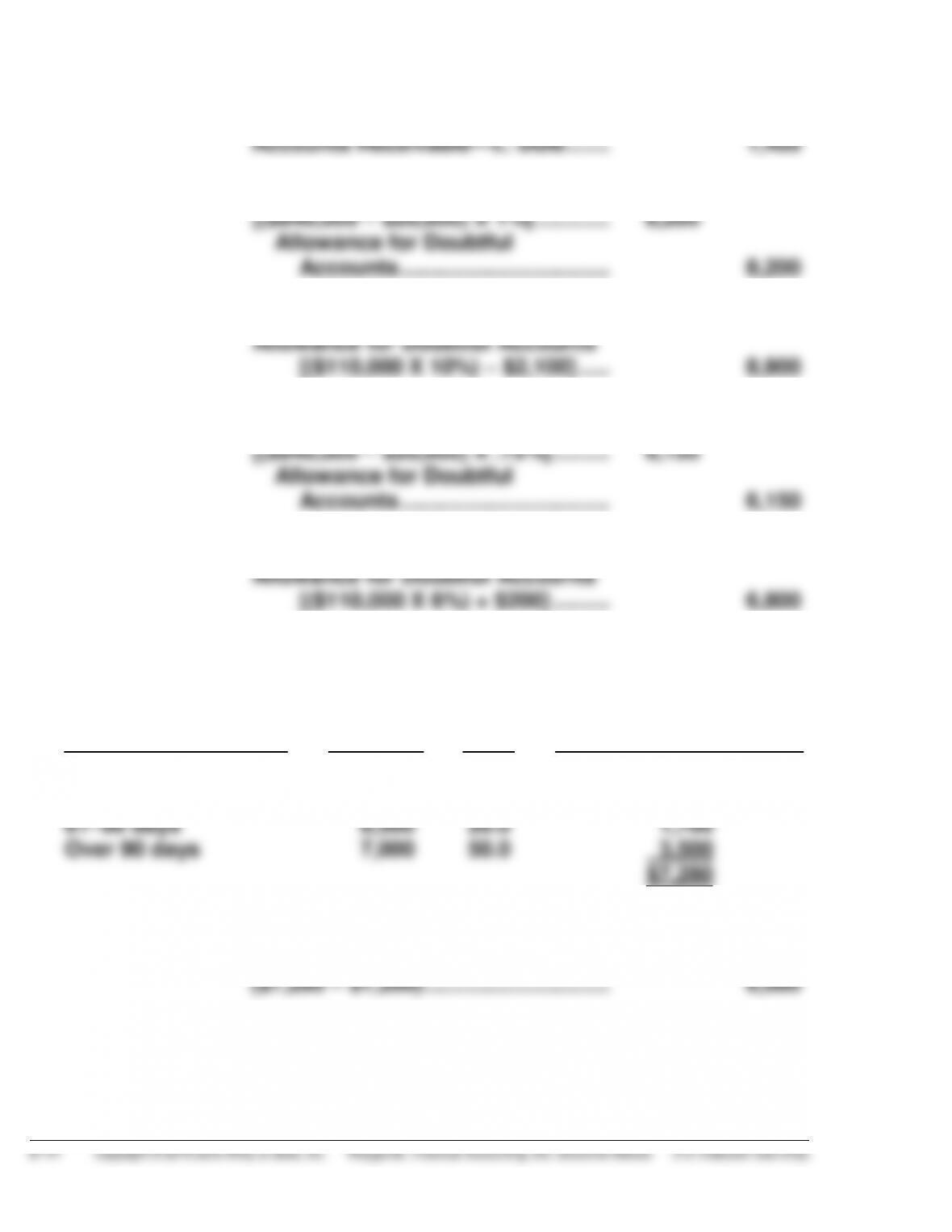

EXERCISE 8-4

(a)

Accounts Receivable

Amount

%

Estimated Uncollectible

1–30 days

31–60 days

61–90 days

Over 90 days

$60,000

17,600

8,500

7,000

2.0

5.0

20.0

50.0

$1,200

880

1,700

3,500

$7,280

(b) Mar. 31 Bad Debt Expense ……………………………….. 6,080

Allowance for Doubtful Accounts

EXERCISE 8-5

Allowance for Doubtful Accounts …………………………….. 11,000

Accounts Receivable ………………………………………………. 1,800

Cash ………………………………………………………………………. 1,800

Bad Debt Expense …………………………………………………… 13,200

EXERCISE 8-6

December 31, 2015

Bad Debt Expense (2% X $450,000) ………………………….. 9,000

May 11, 2016

June 12, 2016

Accounts Receivable—Shoemaker …………………………... 1,100

Cash ………………………………………………………………………. 1,100

EXERCISE 8-7

(a) Mar. 3 Cash ($650,000 – $19,500) ………………….. 630,500

(b) May 10 Cash ($3,000 – $120) …………………………. 2,880

EXERCISE 8-8

(a) Apr. 2 Accounts Receivable—J. Elston ………… 1,500

May 3 Cash …………………………………………………. 500

June 1 Accounts Receivable—J. Elston ………… 10

(b) July 4 Cash …………………………………………………. 196

Service Charge Expense

EXERCISE 8-9

(a) Jan. 15 Accounts Receivable …………………………. 18,000

Sales Revenue ……………………………. 18,000

20 Cash ($4,500 – $90) ……………………………. 4,410

Feb. 10 Cash …………………………………………………. 10,000

15 Accounts Receivable ($8,000 X 1.5%) …. 120

EXERCISE 8-10

(a) 2015

Nov. 1 Notes Receivable …………………………………….. 30,000

Dec. 11 Notes Receivable …………………………………….. 6,750

16 Notes Receivable …………………………………….. 4,000

31 Interest Receivable ………………………………….. 545

*Calculation of interest revenue:

Lopez’s note: $30,000 X 10% X 2/12 = $500

(b) 2016

Nov. 1 Cash ……………………………………………………….. 33,000

Interest Receivable ……………………………. 500

*($30,000 X 10% X 10/12)

EXERCISE 8-11

2015

May 1 Notes Receivable ……………………………………… 9,000

Dec. 31 Interest Receivable …………………………………… 600

31 Interest Revenue ………………………………………. 600

EXERCISE 8-11 (Continued)

2016

May 1 Cash ……………………………………………………….. 9,900

EXERCISE 8-12

4/1/15 Notes Receivable …………………………………….. 30,000

7/1/15 Notes Receivable …………………………………….. 25,000

12/31/15 Interest Receivable ………………………………….. 2,700

Interest Receivable ………………………………….. 1,250

Interest Revenue

4/1/16 Cash ……………………………………………………….. 33,600

Accounts Receivable ……………………………….. 26,875

EXERCISE 8-13

(a) May 2 Notes Receivable …………………………..……. 9,000

(b) Nov. 2 Accounts Receivable—Chang

Inc.………………………………………………….. 9,405

(c) Nov. 2 Allowance for Doubtful Accounts …………. 9,000

EXERCISE 8-14

(a) Beginning accounts receivable ………………………………… $ 100,000

SOLUTIONS TO PROBLEMS

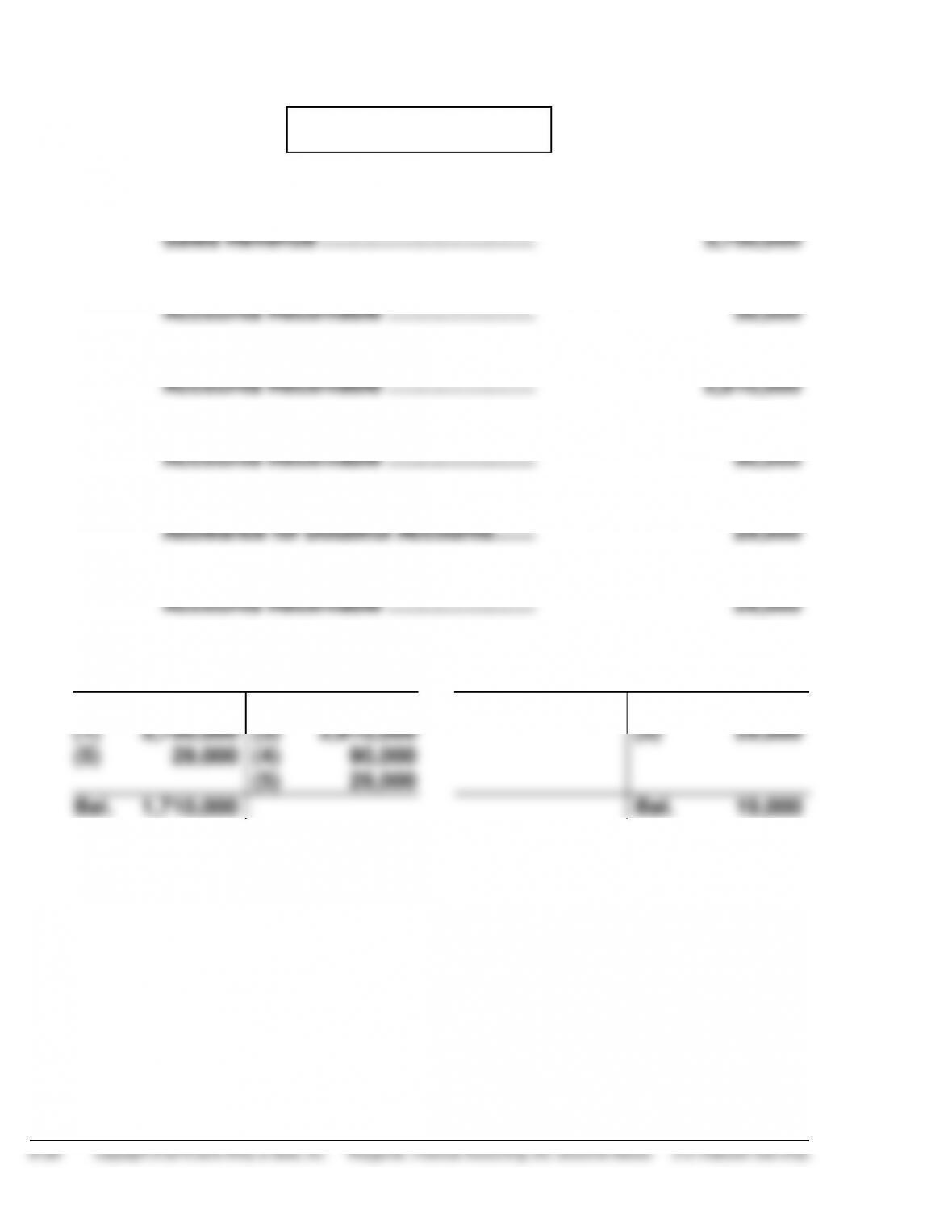

PROBLEM 8-1A

(a) 1. Accounts Receivable ………………………….. 3,700,000

2. Sales Returns and Allowances ……………. 50,000

3. Cash ………………………………………………….. 2,810,000

4. Allowance for Doubtful Accounts ………… 90,000

5. Accounts Receivable ………………………….. 29,000

Cash ………………………………………………….. 29,000

(b)

Accounts Receivable

Allowance for Doubtful Accounts

Bal. 960,000

(1) 3,700,000

(5) 29,000

(2) 50,000

(3) 2,810,000

(4) 90,000

(5) 29,000

(4) 90,000

Bal. 80,000

(5) 29,000

Bal. 1,710,000

Bal. 19,000