PROBLEM 7-6B

(a) GAMEL COMPANY

Bank Reconciliation

October 31, 2015

Cash balance per bank statement ……………………………… $15,313.00

Less: Outstanding checks

No.

Amount

No.

Amount

62

183

284

$107.74

127.50

215.26

862

863

864

$132.10

192.78

140.49

……………….

915.87

Adjusted cash balance per bank ……………………………….. $17,623.31

Cash balance per books……………………………………………. $18,608.81

Add: Bank credit (collection of note receivable) ……….. 460.00

Adjusted balance per books (before theft) …………………. 19,068.81

Less: Theft ……………………………………………………………… 1,445.50*

Adjusted cash balance per books ……………………………… $17,623.31

*$19,068.81 – $17,623.31

(b) The cashier attempted to cover the theft of $1,445.50 by:

PROBLEM 7-6B (Continued)

(c) 1. The principle of independent internal verification has been violated

2. The principle of segregation of duties has been violated because

COMPREHENSIVE PROBLEM SOLUTION

(a)

Dec. 7

Cash …………………………………………………….

Accounts Receivable ……………………..

3,600

3,600

12

Inventory ……………………………………………...

Accounts Payable ………………………….

12,000

12,000

17

Accounts Receivable …………………………..

Sales Revenue ……………………………….

Cost of Goods Sold ……………………………...

Inventory ……………………………………….

16,000

10,000

16,000

10,000

19

Salaries and Wages Expense ………………...

Cash ……………………………………………..

2,200

2,200

22

Accounts Payable ………………………………...

Cash ($12,000 X .99) ……………………….

Inventory ……………………………………….

12,000

11,880

120

26

Cash ($16,000 X .98) ……………………………..

Sales Discounts …………………………………...

Accounts Receivable ……………………..

15,680

320

16,000

31

Cash …………………………………………………….

Accounts Receivable ……………………..

2,700

2,700

COMPREHENSIVE PROBLEM SOLUTION (Continued)

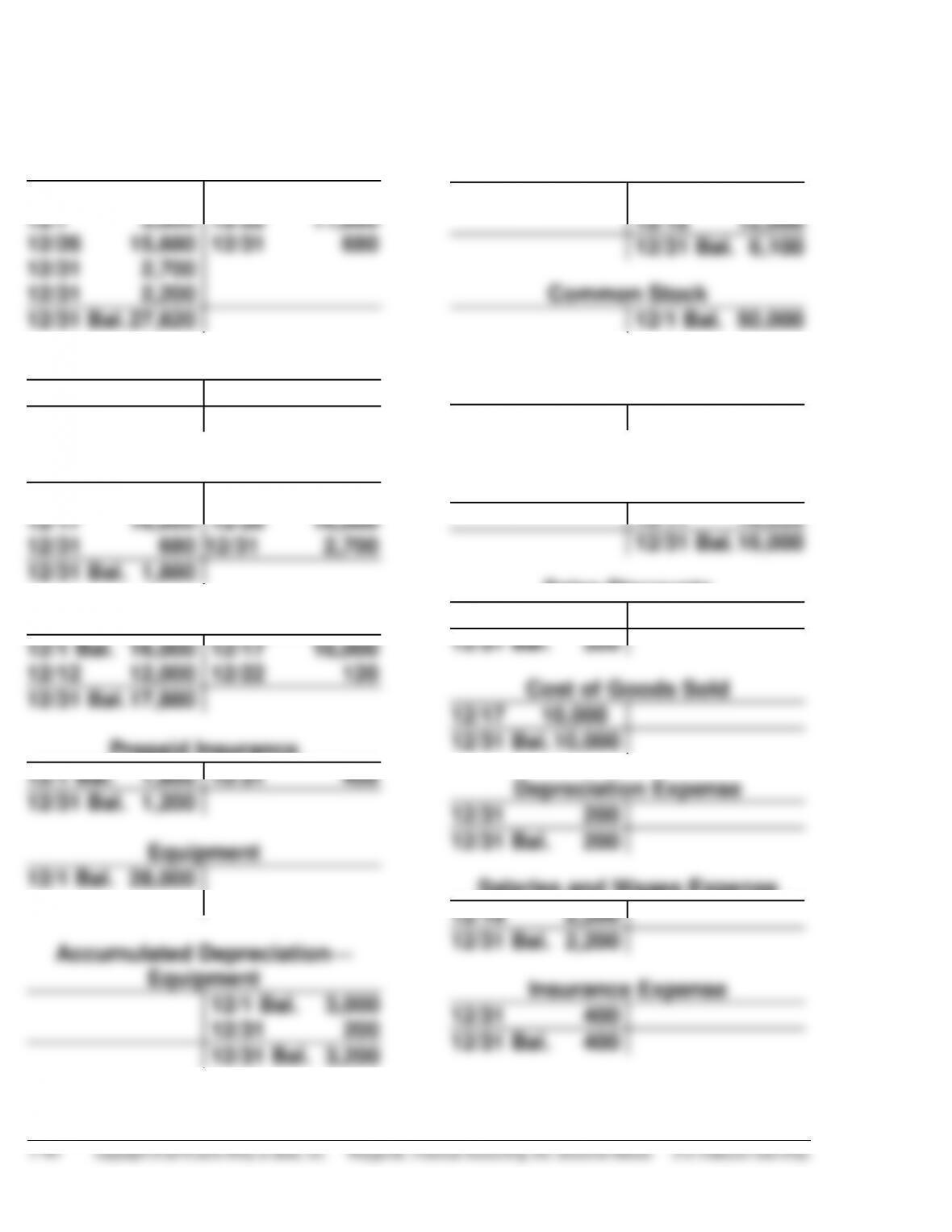

(b) & (e) General Ledger

Cash

12/1 Bal. 18,200

12/7 3,600

12/26 15,680

12/31 Bal. – 0 –

12/31 680

12/1 Bal. 16,000

12/12 12,000

12/17 10,000

12/22 120

12/31 Bal. 17,880

Prepaid Insurance

12/31 Bal. 1,200

12/26 320

12/31 Bal. 10,000

12/19 2,200

12/22 11,880

12/31 680

Accounts Payable

12/22 12,000

12/1 Bal. 6,100

12/12 12,000

12/31 Bal. 6,100

12/19 2,200

COMPREHENSIVE PROBLEM SOLUTION (Continued)

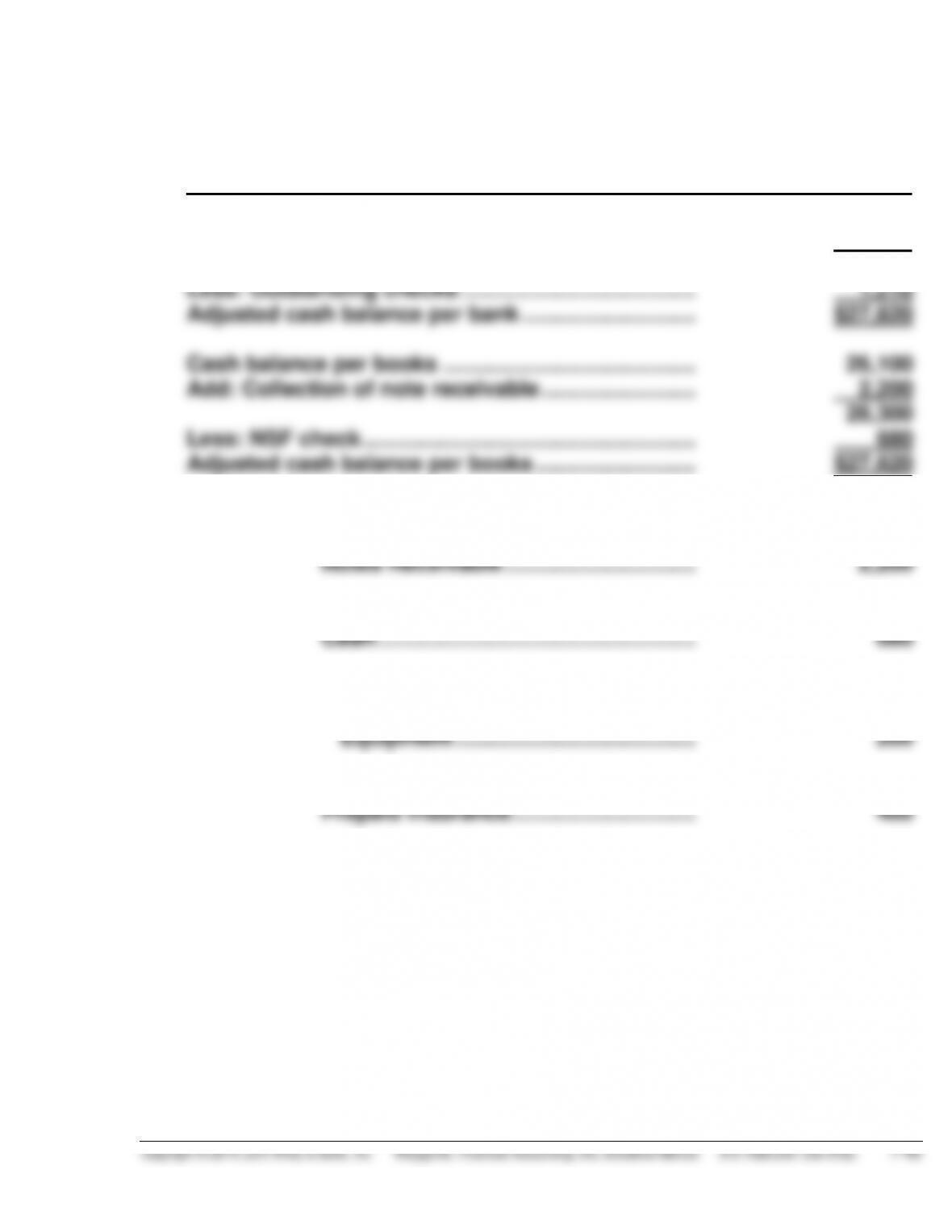

(c) FULLERTON COMPANY

Bank Reconciliation

December 31, 2015

Cash balance per bank statement …………………….. $26,130

Add: Deposits in transit …………………………………… 2,700

28,830

(d) Dec. 31 Cash …………………………………………………. 2,200

31 Accounts Receivable …………………………. 680

31 Depreciation Expense ………………………… 200

Accumulated Depreciation—

31 Insurance Expense …………………………….. 400

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(f) FULLERTON COMPANY

Adjusted Trial Balance

December 31, 2015

DR.

CR.

Cash …………………………………………………….

$27,620

Accounts Receivable …………………………….

1,880

Inventory ………………………………………………

17,880

Prepaid Insurance …………………………………

1,200

Equipment…………………………………………….

28,000

Accumulated Depreciation—Equipment …

$ 3,200

Accounts Payable …………………………………

6,100

Common Stock ……………………………………..

50,000

Retained Earnings …………………………………

14,400

Sales Revenue ………………………………………

16,000

Sales Discounts ……………………………………

320

Cost of Goods Sold ……………………………….

10,000

Depreciation Expense …………………………...

200

Salaries and Wages Expense …………………

2,200

Insurance Expense ………………………………..

400

$89,700

$89,700

(g) FULLERTON COMPANY

Income Statement

For the Month Ending December 31, 2015

Sales revenue ……………………………………….

$16,000

Less: Sales discounts ………………………….

320

Net sales ………………………………………………

15,680

Cost of goods sold ………………………………..

10,000

Gross profit ………………………………………….

5,680

Operating expenses

Salaries and wages expense …………..

$2,200

Insurance expense …………………………

400

Depreciation expense ……………………..

200

2,800

Net income……………………………………………

$ 2,880

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(g) FULLERTON COMPANY

Balance Sheet

December 31, 2015

Assets

Current assets

Cash ……………………………………………….

$27,620

Accounts receivable …………………………

1,880

Inventory …………………………………………

17,880

Prepaid insurance …………………………...

1,200

Total current assets ……………………..

$48,580

Property, plant, and equipment

Equipment ……………………………………….

28,000

Less: Accumulated

depreciation—Equipment ……….

3,200

24,800

Total assets ……………………………………………

$73,380

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable …………………………….

$ 6,100

Stockholders’ equity

Common stock ………………………………..

$50,000

Retained earnings ($14,400 + $2,880) ..

17,280

67,280

Total liabilities and stockholders’ equity ….

$73,380

BYP 7-1 FINANCIAL REPORTING PROBLEM

the United States of America.”

(b) Cash and cash equivalents are reported at $9,815 million for 2011 and

$11,261 million for 2010.

(d) The Company’s management is responsible for establishing and

maintaining adequate internal control over financial reporting (as

defined in Rule 13a–15(f) under the Exchange Act). Management

Report on Form 10–K.

BYP 7-2 COMPARATIVE ANALYSIS PROBLEM

PepsiCo

Coca-Cola

(a)

(1)

$4,067 million

$12,803 million

(2)

$1,876 million decrease

$4,286 million increase

(3)

$8,944 million

$9,474 million

amounts of cash.

BYP 7-3 COMPARATIVE ANALYSIS PROBLEM

Amazon

Wal-Mart

(a)

(1)

$5,269 million

$6,550 million

(2)

$1,492 million increase

$845 million decrease

(3)

$3,903 million

$24,255 million

cash balances at the end of 2011 and are capable of generating huge

amounts of cash.