BRIEF EXERCISE 7-9

Mar. 20 Postage Expense …………………………………………………. 52

Freight-Out ………………………………………………………….. 26

BRIEF EXERCISE 7-10

BRIEF EXERCISE 7-11

BRIEF EXERCISE 7-12

BRIEF EXERCISE 7-13

Cash balance per bank …………………………..………………………………. $7,420

BRIEF EXERCISE 7-14

Cash balance per books …………………………………………………………. $9,500

BRIEF EXERCISE 7-15

the next year.

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 7-1

1. Violates the control activity of documentation procedures. Source docu-

ments should be promptly forwarded to the accounting department so

DO IT! 7-1 (Continued)

2. Violates the control activity of segregation of duties. Different individuals

tions of delivered goods; approving fictitious invoices for payment.

3. Violates the control activity of establishment of responsibility. Great

DO IT! 7-2

used to confirm that all receipts were deposited and recorded. The clerks

also keep a copy.

DO IT! 7-3

Cash ………………………………………………. 100

31 Postage Expense ………………………………….. 31

DO IT! 7-4

Roger should treat the reconciling items as follows:

SOLUTIONS TO EXERCISES

EXERCISE 7-1

2. Segregation of duties. Employees who make the pizzas do not handle cash.

produces a tape of all sales.

5. Independent internal verification. The counter clerk, in handling the pizza,

EXERCISE 7-2

(a)

(b)

Procedure

Weakness

Principle

Recommended

Change

1.

Cash is not

adequately

protected

from theft.

Physical

controls.

Cash should be

stored in a safe

until it is deposited

in bank.

2.

Inability to

establish

responsibility

for cash with

a specific clerk.

Establishment

of responsibility.

There should be

separate cash

drawers and

register codes

for each clerk.

EXERCISE 7-2 (Continued)

(a)

(b)

Procedure

Weakness

Principle

Recommended

Change

3.

The accountant

should not

handle cash.

Segregation

of duties.

The cashier’s

department should

make the deposits.

4.

Cash is not

independently

counted.

Independent

internal

verification.

A cashier office

supervisor should

count cash.

5.

Cashiers are

not bonded.

Human resource

controls.

All cashiers should

be bonded.

EXERCISE 7-3

(a)

(b)

Procedure

Weakness

Principle

Recommended

Change

1.

The bank

reconciliation

is not

independently

prepared.

Independent

internal

verification.

Someone with no

other cash

responsibilities

should prepare the

bank reconciliation.

2.

The approval

and payment

of bills is done

by the same

individual.

Segregation

of duties.

The store manager

should approve bills

for payment and the

treasurer should sign

and issue checks.

3.

Checks are

not stored in

a secure area.

Physical

controls.

Checks should be

stored in a safe or

locked file drawer.

EXERCISE 7-3 (Continued)

(a)

(b)

Procedure

Weakness

Principle

Recommended

Change

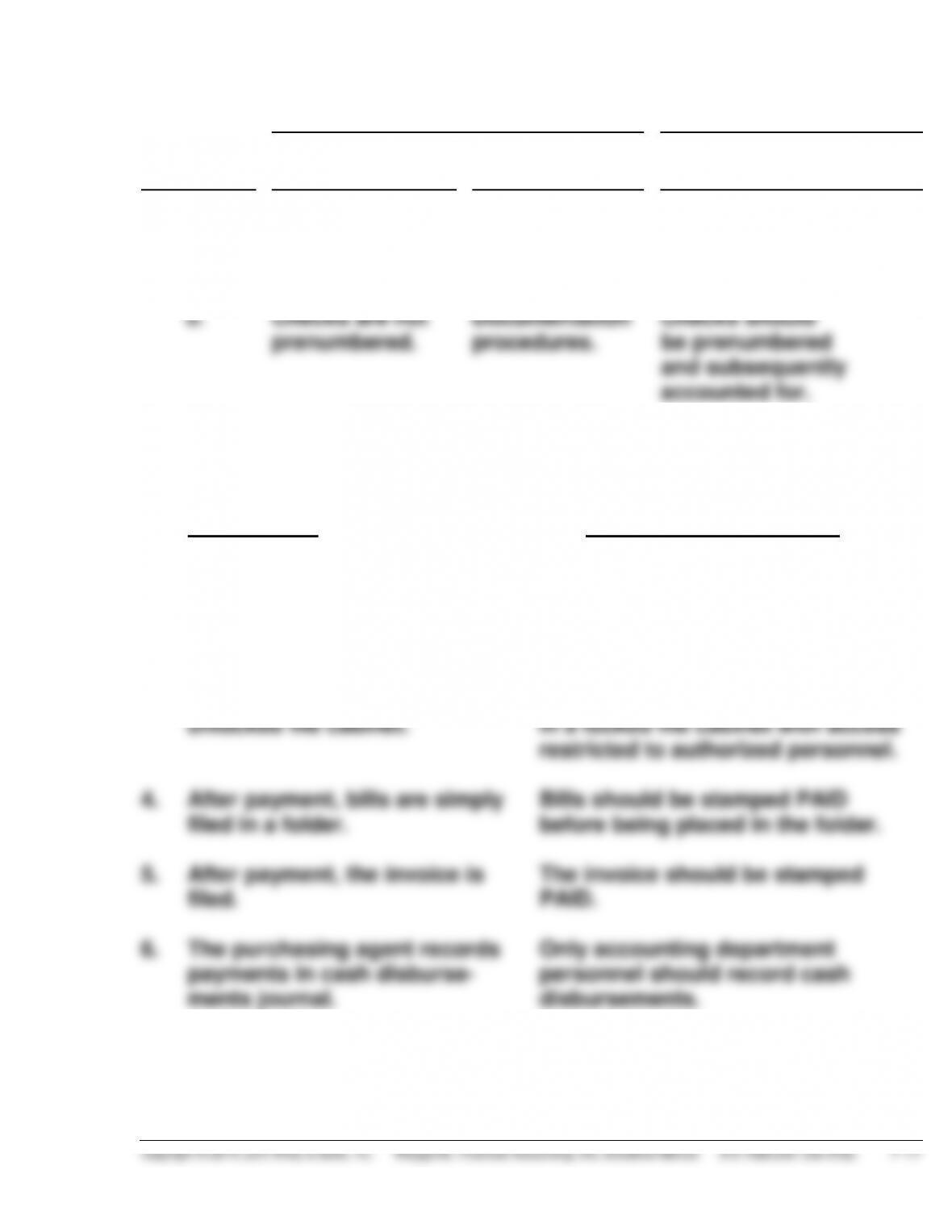

4.

After payment,

bills are simply

filed in a folder.

Documentation

procedures.

Bills should be stamped

PAID before being placed

in the folder.

5.

Checks are not

prenumbered.

Documentation

procedures.

Checks should

be prenumbered

and subsequently

accounted for.

EXERCISE 7-4

(a) Weaknesses

(b) Suggested Improvement

1. Checks are not prenumbered.

Use prenumbered checks.

2. The purchasing agent signs

checks.

Only the treasurer’s department

personnel should sign checks.

3. Unissued checks are stored in

unlocked file cabinet.

Unissued checks should be stored

in a locked file cabinet with access

restricted to authorized personnel.

4. After payment, bills are simply

filed in a folder.

Bills should be stamped PAID

before being placed in the folder.

5. After payment, the invoice is

filed.

The invoice should be stamped

PAID.

6. The purchasing agent records

payments in cash disburse-

ments journal.

Only accounting department

personnel should record cash

disbursements.

EXERCISE 7-4 (Continued)

(a) Weaknesses

(b) Suggested Improvement

7. The treasurer records the

checks in cash disbursements

journal.

Same as answer to No. 6 above.

8. The treasurer reconciles the

bank statement.

An internal auditor should

reconcile the bank statement.

(b) To: Treasurer, Danner Company

From: Accounting Student

1. Danner Company should use prenumbered checks. These should

2. The purchasing department should approve bills for payment. The

3. Only the accounting department personnel should record cash

disbursements.

contact me.

EXERCISE 7-5

Procedure

IC good or weak?

Related internal control principle

1.

Weak

Establishment of Responsibility

2.

Good

Independent Internal Verification

3.

Weak

Segregation of Duties

4.

Good

Segregation of Duties

5.

Weak

Documentation Procedures

EXERCISE 7-6

Procedure

IC good or weak?

Related internal control principle

1.

Good

Human Resource Controls

2.

Weak

Establishment of Responsibility

3.

Weak

Segregation of Duties

4.

Good

Independent Internal Verification

5.

Good

Physical Controls

EXERCISE 7-7

May 1 Petty Cash ……………………………………………… 100.00

June 1 Delivery Expense ……………………………………. 31.25

Postage Expense ……………………………………. 39.00

July 1 Delivery Expense …………………………..……….. 21.00

July 10 Petty Cash ……………………………………………… 30.00

EXERCISE 7-8

Mar. 1 Petty Cash……………………………………………………….. 100

Cash …………………………………………………………. 100

15 Postage Expense………………………………………………. 39

Freight-Out ……………………………………………………….. 21

20 Petty Cash………………………………………………………… 75

EXERCISE 7-9

(a) Cash balance per bank statement ……………… $3,560.20

Add: Deposits in transit …………………………... 530.00

4,090.20

(b) Accounts Receivable ………………………………… 490.00

Miscellaneous Expense …………………………….. 25.00