*PROBLEM 6-8B (Continued)

(b)

Gross profit:

LIFO

FIFO

Moving-Average

Sales

$13,800

$13,800

$13,800

Cost of goods sold

7,260

6,020

6,446

Gross profit

$ 6,540

$ 7,780

$ 7,354

Ending inventory

$ 2,040

$ 3,280

$ 2,854

On the balance sheet, FIFO gives the highest ending inventory (represent–

ing the most current costs); LIFO gives the lowest ending inventory

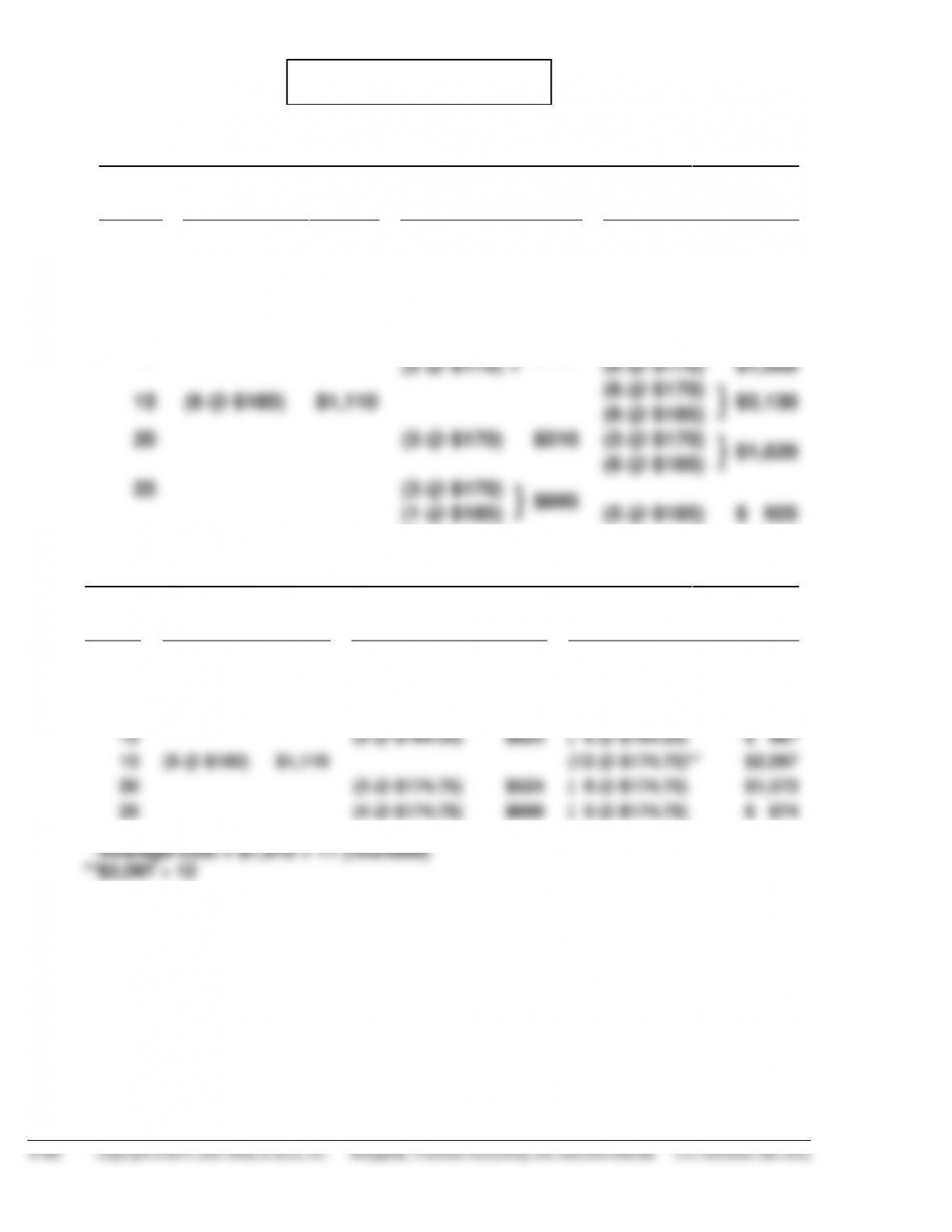

*PROBLEM 6-9B

(a)

(1)

FIFO

Date

Purchases

Cost of

Goods Sold

Balance

May 1

(7 @ $150)

$1,050

(7 @ $150)

$1,050

4

(4 @ $150)

$600

(3 @ $150)

$ 450

8

(8 @ $170)

$1,360

(3 @ $150)

}

$1,810

(8 @ $170)

12

(3 @ $150)

}

$790

(2 @ $170)

(6 @ $170)

$1,020

15

(6 @ $185)

$1,110

(6 @ $170)

}

$2,130

(6 @ $185)

20

(3 @ $170)

$510

(3 @ $170)

}

$1,620

(6 @ $185)

25

(3 @ $170)

}

$695

(1 @ $185)

(5 @ $185)

$ 925

(2)

MOVING-AVERAGE COST

Date

Purchases

Cost of

Goods Sold

Balance

May 1

(7 @ $150)

$1,050

( 7 @ $150)

$1,050

4

(4 @ $150)

$600

( 3 @ $150)

$ 450

8

(8 @ $170)

$1,360

(11 @ $164.55)*

$1,810

12

(5 @ $164.55)

$823

( 6 @ $164.55)

$ 987

15

(6 @ $185)

$1,110

(12 @ $174.75)**

$2,097

20

(3 @ $174.75)

$524

( 9 @ $174.75)

$1,573

25

(4 @ $174.75)

$699

( 5 @ $174.75)

$ 874

*PROBLEM 6-9B (Continued)

(3)

LIFO

Date

Purchases

Cost of

Goods Sold

Balance

May 1

(7 @ $150)

$1,050

(7 @ $150)

$1,050

4

(4 @ $150)

$600

(3 @ $150)

$ 450

8

(8 @ $170)

$1,360

(3 @ $150)

}

$1,810

(8 @ $170)

12

(5 @ $170)

$850

(3 @ $150)

}

$ 960

(3 @ $170)

15

(6 @ $185)

$1,110

(3 @ $150)

}

$2,070

(3 @ $170)

(6 @ $185)

20

(3 @ $185)

$555

(3 @ $150)

}

$1,515

(3 @ $170)

(3 @ $185)

25

(3 @ $185)

}

$725

(3 @ $150)

}

$ 790

(1 @ $170)

(2 @ $170)

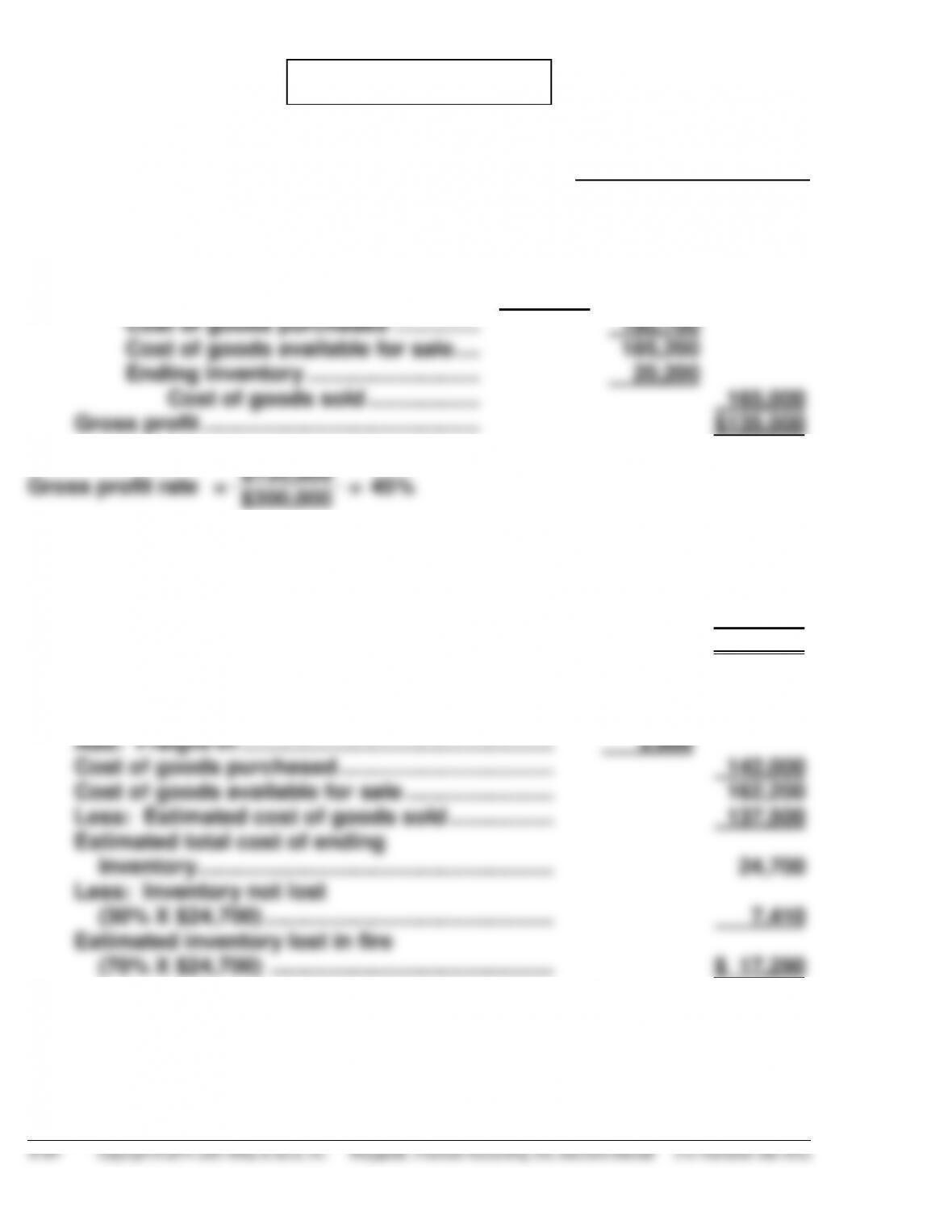

*PROBLEM 6-10B

(a)

February

Net sales ………………………………………….. $300,000

Cost of goods sold

Beginning inventory ………………….. $ 4,500

Net purchases …………………………... $176,800

Add: Freight-in …………………………. 3,900

Gross profit rate

=

$135,000

=

45%

$300,000

(b) Net sales …………………………………………………….. $250,000

Less: Estimated gross profit

(45% X $250,000) ………………………………. 112,500

Estimated cost of goods sold ………………………. $137,500

Beginning inventory ……………………………………. $ 20,200

Net purchases …………………………………………….. $139,000

*PROBLEM 6-11B

(a)

Sporting

Goods

Jewelry

and Cosmetics

Cost

Retail

Cost

Retail

Beginning inventory $ 47,360 $ 74,000 $ 39,440 $ 62,000

Purchases 675,000 1,066,000 741,000 1,158,000

Purchase returns (26,000) (40,000) (12,000) (20,000)

Cost-to-retail ratio:

Estimated ending inventory at cost:

COMPREHENSIVE PROBLEM SOLUTION

(a)

Dec. 3

Inventory (4,000 X $0.72) ………………………

Accounts Payable ………………………….

2,880

2,880

5

Accounts Receivable (4,400 X $0.90) ……..

Sales Revenue ………………………………

Cost of Good Sold ………………………………..

Inventory (3,000 X $0.60) +

(1,400 X $0.72) …………………………….

3,960

2,808

3,960

2,808

7

Sales Returns and Allowances ……………..

Accounts Receivable……………………..

Inventory …………………………..…………………

Cost of Good Sold …………………………

180

120

180

120

17

Inventory (2,200 X $0.80) ………………………

Cash …………………………..………………..

1,760

1,760

22

Accounts Receivable (2,000 X $0.95) ……..

Sales Revenue ………………………………

Cost of Goods Sold (2,000 X $0.72) ……….

Inventory ………………………………………

1,900

1,440

1,900

1,440

31

Salaries and Wages Expense ………………..

Salaries and Wages Payable …………..

Depreciation Expense …………………………..

Accumulated Depreciation—

Equipment ………………………………….

400

200

400

200

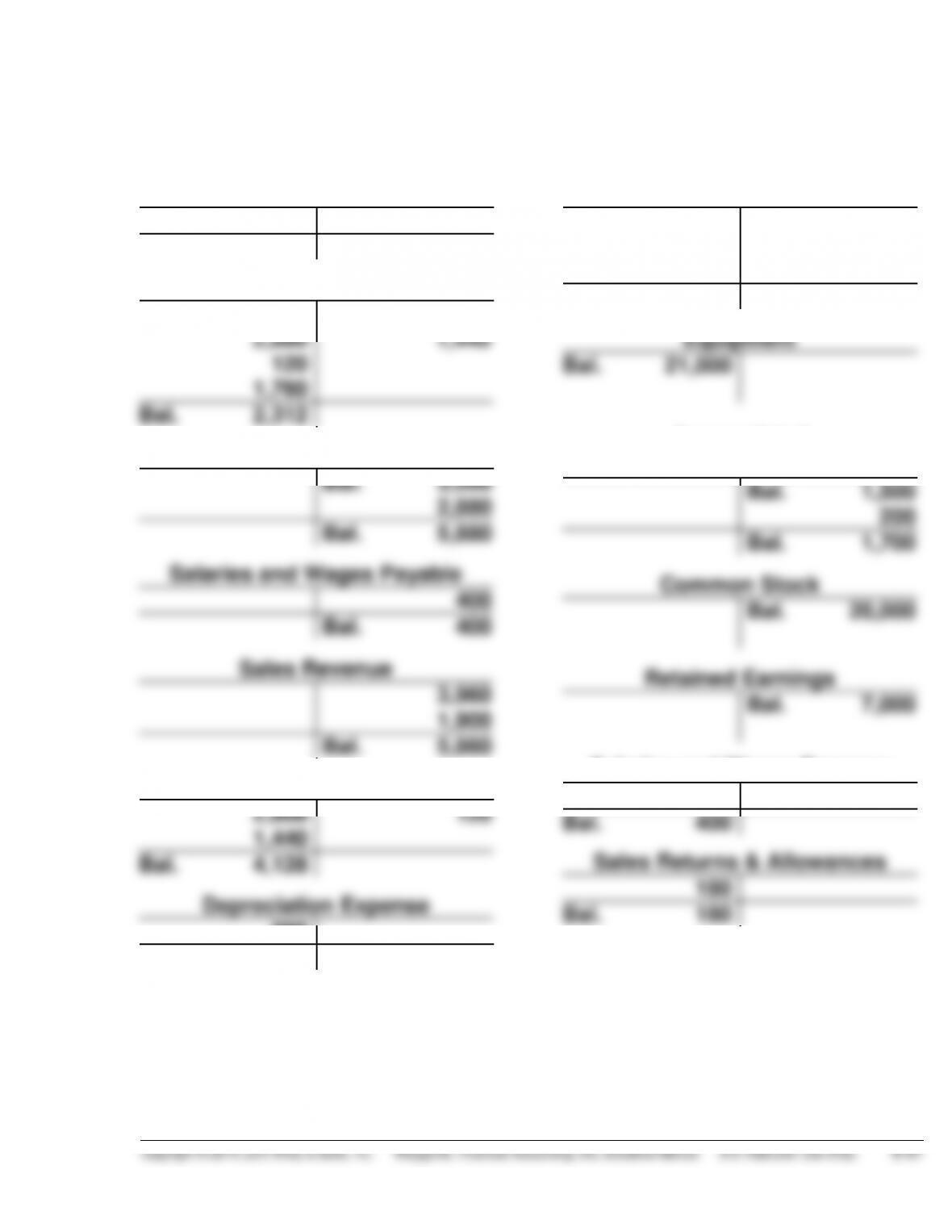

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(b) General Ledger

Cash

Bal. 4,800

1,760

Bal. 3,040

Inventory

Bal. 2,312

Bal. 5,880

Bal. 21,000

Bal. 1,700

Accounts Receivable

Bal. 3,900

3,960

1,900

180

Bal. 9,580

Bal. 400

Bal. 5,860

Bal. 4,128

Bal. 200

Bal. 20,000

Bal. 7,000

Bal. 400

Bal. 180

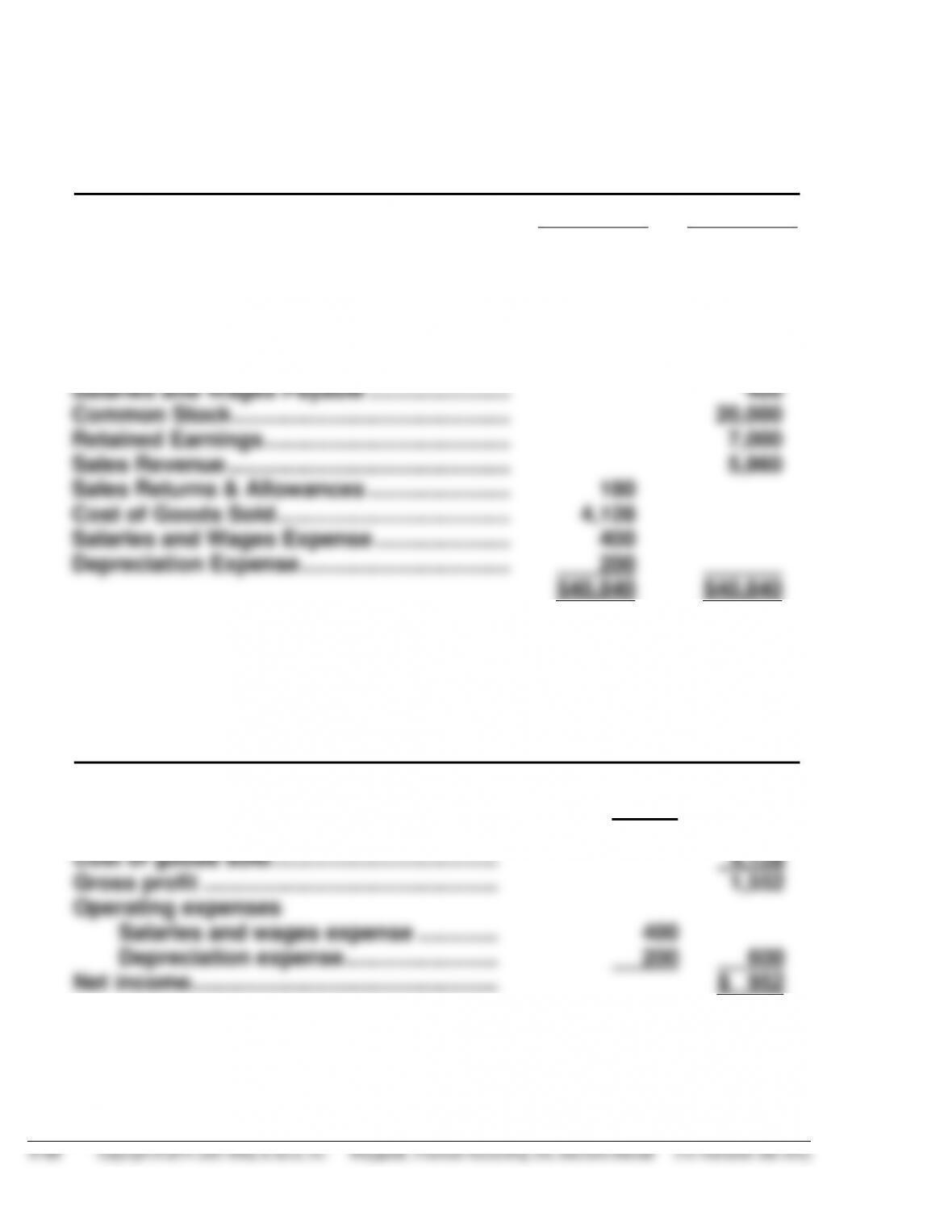

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(c) Matthias COMPANY

Adjusted Trial Balance

December 31, 2015

DR.

CR.

Cash ……………………………………………………..

$ 3,040

Accounts Receivable ……………………………..

9,580

Inventory ……………………………………………….

2,312

Equipment……………………………………………..

21,000

Accumulated Depreciation—Equipment ….

$ 1,700

Accounts Payable …………………………..……..

5,880

Salaries and Wages Payable …………………..

400

Common Stock ………………………………………

Retained Earnings ………………………………….

20,000

7,000

Sales Revenue ……………………………………….

5,860

Sales Returns & Allowances …………………..

180

Cost of Goods Sold ………………………………..

4,128

Salaries and Wages Expense ………………….

400

Depreciation Expense …………………………….

200

$40,840

$40,840

(d) Matthias COMPANY

Income Statement

For the Month Ending December 31, 2015

Sales revenue ………………………………………

$5,860

Less: Sales returns and allowances ……..

180

Net sales ……………………………………………..

$5,680

Cost of goods sold ……………………………….

4,128

Gross profit …………………………..…………….

1,552

Operating expenses

Salaries and wages expense ………….

400

Depreciation expense …………………….

200

600

Net income…………………………………………..

$ 952

COMPREHENSIVE PROBLEM SOLUTION (Continued)

Matthias COMPANY

Balance Sheet

December 31, 2015

Assets

Current assets

Cash ……………………………………………….

$ 3,040

Accounts receivable …………………………

9,580

Inventory …………………………………………

2,312

Total current assets …………………….

$14,932

Property, plant, and equipment

Equipment ……………………………………….

21,000

Less: Accumulated depreciation—

Equipment …………………………….

1,700

19,300

Total assets ……………………………………………

$34,232

Liabilities and Stockholders’ Equity

Current liabilities

Accounts payable …………………………….

$5,880

Salaries and wages payable ……………..

400

Total current liabilities …………………

$ 6,280

Stockholders’ equity

Common stock ………………………………..

Retained earnings ($7,000 + $952) …….

20,000

7,952

27,952

Total liabilities and stockholders’ equity ….

$34,232

COMPREHENSIVE PROBLEM SOLUTION (Continued)

(e) FIFO Method

Units

Unit Cost

Cost of Goods

Available for Sales

Beg. Inventory

3,000

$0.60

$1,800

Dec. 3 purchase.

4,000

$0.72

2,880

Dec. 17 purchase.

2,200

$0.80

1,760

9,200

$6,440

Ending Inventory

Cost of Goods Sold

Dec. 17

2,200 X $0.80 = $1,760

Cost of goods available for sale

$6,440

Dec. 3

800* X $0.72 = 576

Less: Ending inventory

2,336

3,000 $2,336

Cost of goods sold

$4,104

(f) LIFO Method

Ending Inventory

Cost of Goods Sold

Dec. 1

3,000 X $0.60 = $1,800

Cost of goods available for sale

$6,440

Less: Ending inventory

1,800

Cost of goods sold

$4,640