PROBLEM 6-1A

(a) The sale will be recorded on February 26. The goods (cost, $800) should

PROBLEM 6-2A

(a)

COST OF GOODS AVAILABLE FOR SALE

Date

Explanation

Units

Unit Cost

Total Cost

Oct. 1

Beginning Inventory

2,000

$7

$ 14,000

3

Purchase

2,500

8

20,000

9

Purchase

3,500

9

31,500

19

Purchase

3,000

10

30,000

25

Purchase

4,000

11

44,000

Total

15,000

$139,500

(b)

FIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$139,500

Oct. 25

4,000

$11

$44,000

Less: Ending

inventory

45,000

19

100

10

1,000

4,100*

$45,000

Cost of goods sold

$ 94,500

*15,000 – 10,900 = 4,100

Proof of Cost of Goods Sold

Date

Units

Unit Cost

Total Cost

Oct. 1

2,000

$7

$14,000

3

2,500

8

20,000

9

3,500

9

31,500

19

2,900

10

29,000

10,900

$94,500

LIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$139,500

Oct. 1

2,000

$7

$14,000

Less: Ending

inventory

30,800

3

2,100

8

16,800

4,100

$30,800

Cost of goods sold

$108,700

PROBLEM 6-2A (Continued)

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Oct. 25

4,000

$11

$ 44,000

19

3,000

10

30,000

9

3,500

9

31,500

3

400

8

3,200

10,900

$108,700

AVERAGE COST

(1)

Ending Inventory

(2)

Cost of Goods Sold

$139,500 ÷ 15,000 = $9.30

Cost of goods available

for sale

$139,500

Units

Unit Cost

Total Cost

Less: Ending inventory

38,130

4,100

$9.30

$38,130

Cost of goods sold

$101,370

$45,000.

PROBLEM 6-3A

(a)

COST OF GOODS AVAILABLE FOR SALE

Date

Explanation

Units

Unit Cost

Total Cost

1/1

Beginning Inventory

150

$20

$ 3,000

3/15

Purchase

400

23

9,200

7/20

Purchase

250

24

6,000

9/4

Purchase

350

26

9,100

12/2

Purchase

100

29

2,900

Total

1,250

$30,200

(b)

FIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$30,200

12/2

100

$29

$2,900

Less: Ending

inventory

6,800

9/4

150

26

3,900

250

$6,800

Cost of goods sold

$23,400

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

1/1

150

$20

$ 3,000

3/15

400

23

9,200

7/20

250

24

6,000

9/4

200

26

5,200

1,000

$23,400

LIFO

(1)

Ending Inventory

(2)

Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

Cost of goods

available for sale

$30,200

1/1

150

$20

$3,000

Less: Ending

inventory

5,300

3/15

100

23

2,300

250

$5,300

Cost of goods sold

$24,900

PROBLEM 6-3A (Continued)

Proof of Cost of Goods Sold

Date

Units

Unit

Cost

Total

Cost

12/2

100

$29

$ 2,900

9/4

350

26

9,100

7/20

250

24

6,000

3/15

300

23

6,900

1,000

$24,900

AVERAGE COST

(1)

Ending Inventory

(2)

Cost of Goods Sold

$30,200 ÷ 1,250 = $24.16

Cost of goods available

for sale

$30,200

Units

Unit Cost

Total Cost

Less: Ending inventory

6,040

250

$24.16

$6,040

Cost of goods sold

$24,160

Proof of Cost of Goods Sold

1,000 units X $24.16 = $24,160

(b) above.

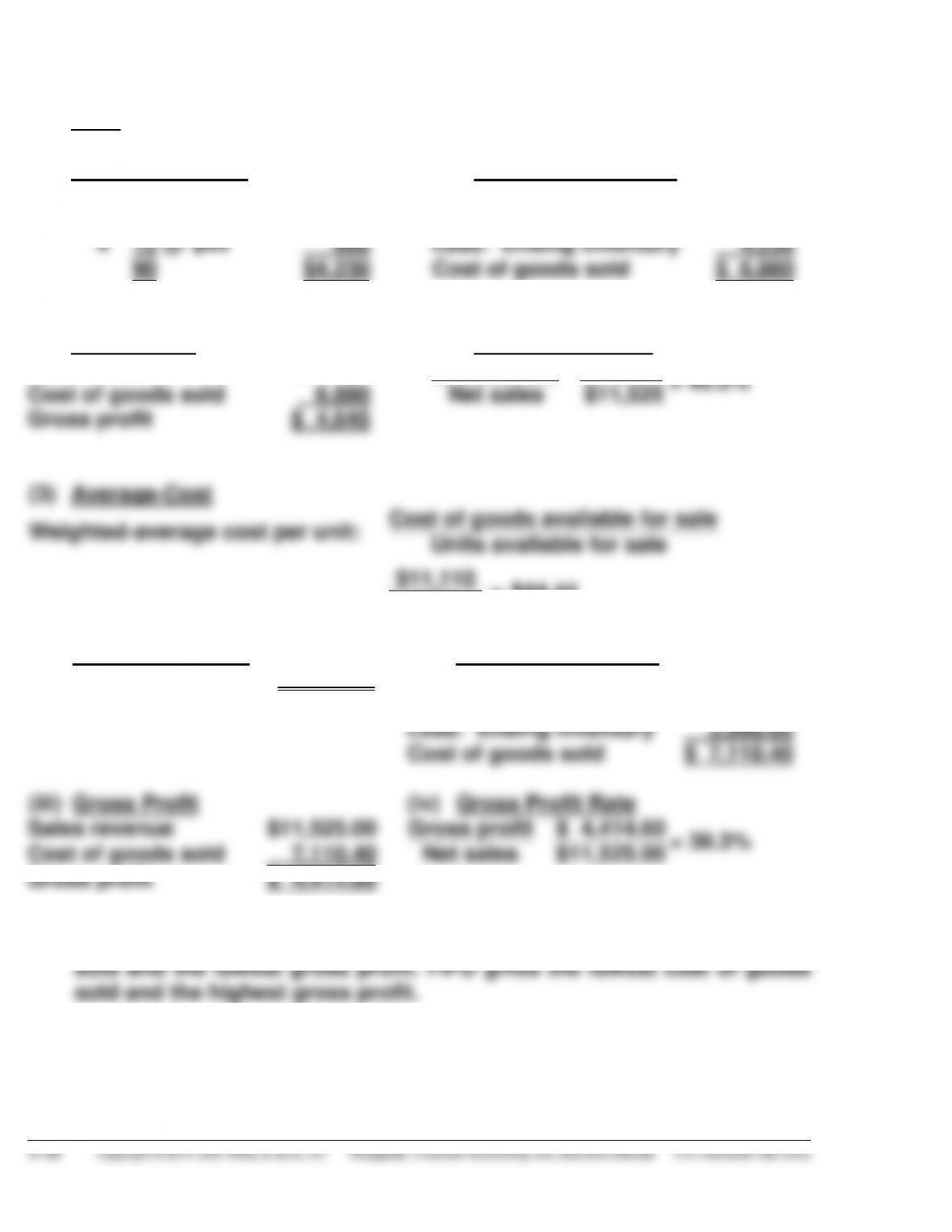

(2) LIFO produces the highest cost of goods sold, $24,900 as shown in

(b) above.

PROBLEM 6-4A

(a) Felipe INC.

Condensed Income Statements

For the Year Ended December 31, 2015

FIFO

LIFO

Sales revenue ………………………………….. $747,000 $747,000

Cost of goods sold

Beginning inventory …………………… 14,000 14,000

Cost of goods purchased ……………. 466,000 466,000

Cost of goods available for sale ….. 480,000 480,000

recent purchase prices.

(2) The LIFO method produces the most meaningful net income because

the cost of the most recent purchases are matched against sales.

spoilage and obsolescence.

(4) There will be $3,960 additional cash available under LIFO because

income taxes are $69,200 under LIFO and $73,160 under FIFO.

FIFO and (b) higher than LIFO.

PROBLEM 6-5A

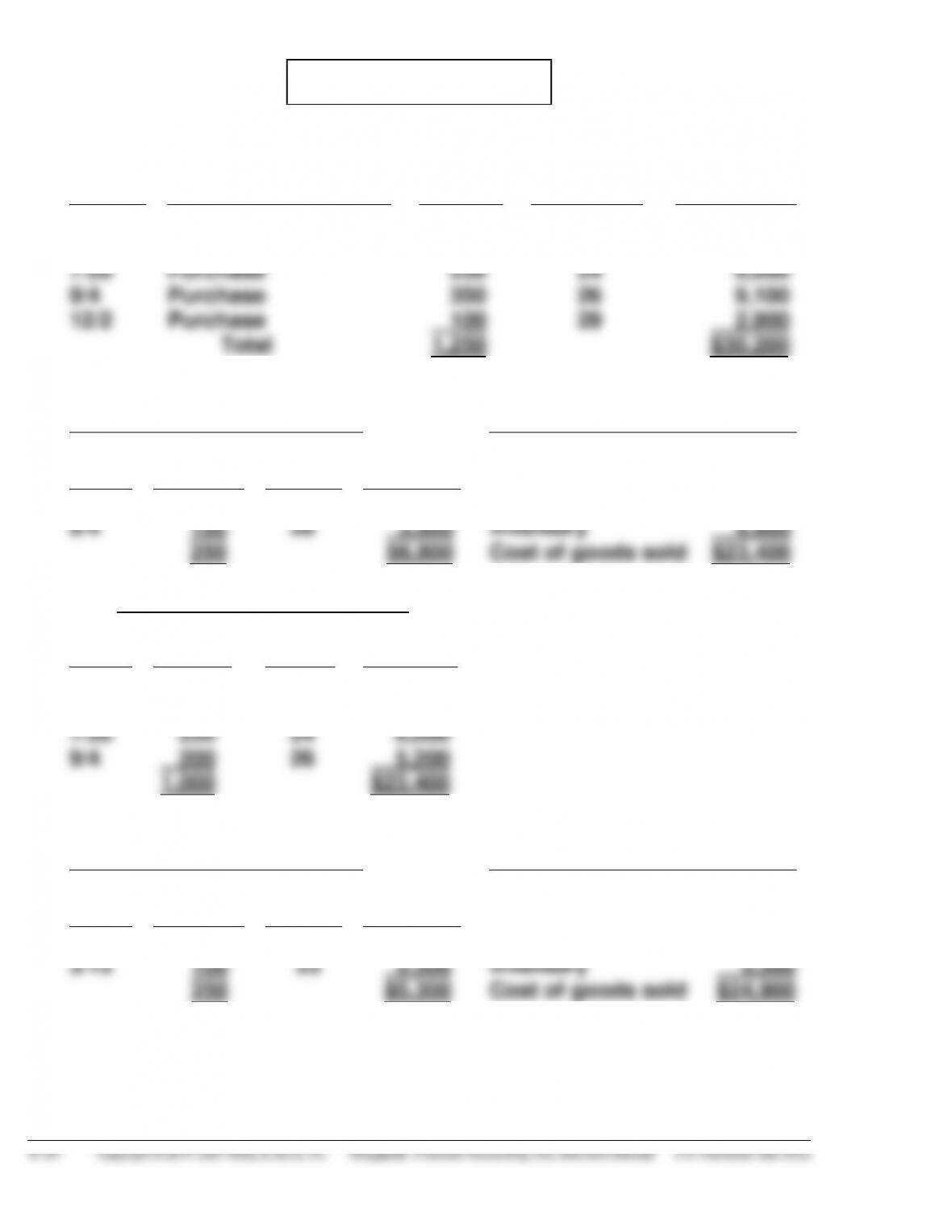

(a)

Cost of Goods Available for Sale

Date

Explanation

Units

Unit Cost

Total Cost

June 1

Beginning Inventory

40

$40

$ 1,600

June 4

Purchase

135

44

5,940

June 18

Purchase

55

46

2,530

June 18

Purchase return

(10)

46

(460)

June 28

Purchase

30

50

1,500

Total

250

$11,110

Ending Inventory in Units:

Sales Revenue

Units available for sale

250

Unit

Sales (110 – 15 + 65)

160

Date

Units

Price

Total Sales

Units remaining in ending inventory

90

June 10

110

$70

$ 7,700

11

(15)

70

(1,050)

25

65

75

4,875

160

$11,525

(1)

LIFO

(i)

Ending Inventory

(ii)

Cost of Goods Sold

June 1

4

40 @ $40

50 @ 44

$1,600

2,200

Cost of goods available

for sale

$11,110

90

$3,800

Less: Ending inventory

3,800

Cost of goods sold

$ 7,310

(iii)

Gross Profit

(iv)

Gross Profit Rate

Sales revenue

$11,525

Gross profit

$ 4,215

=

36.6%

Cost of goods sold

7,310

Net sales

$11,525

Gross profit

$ 4,215

PROBLEM 6-5A (Continued)

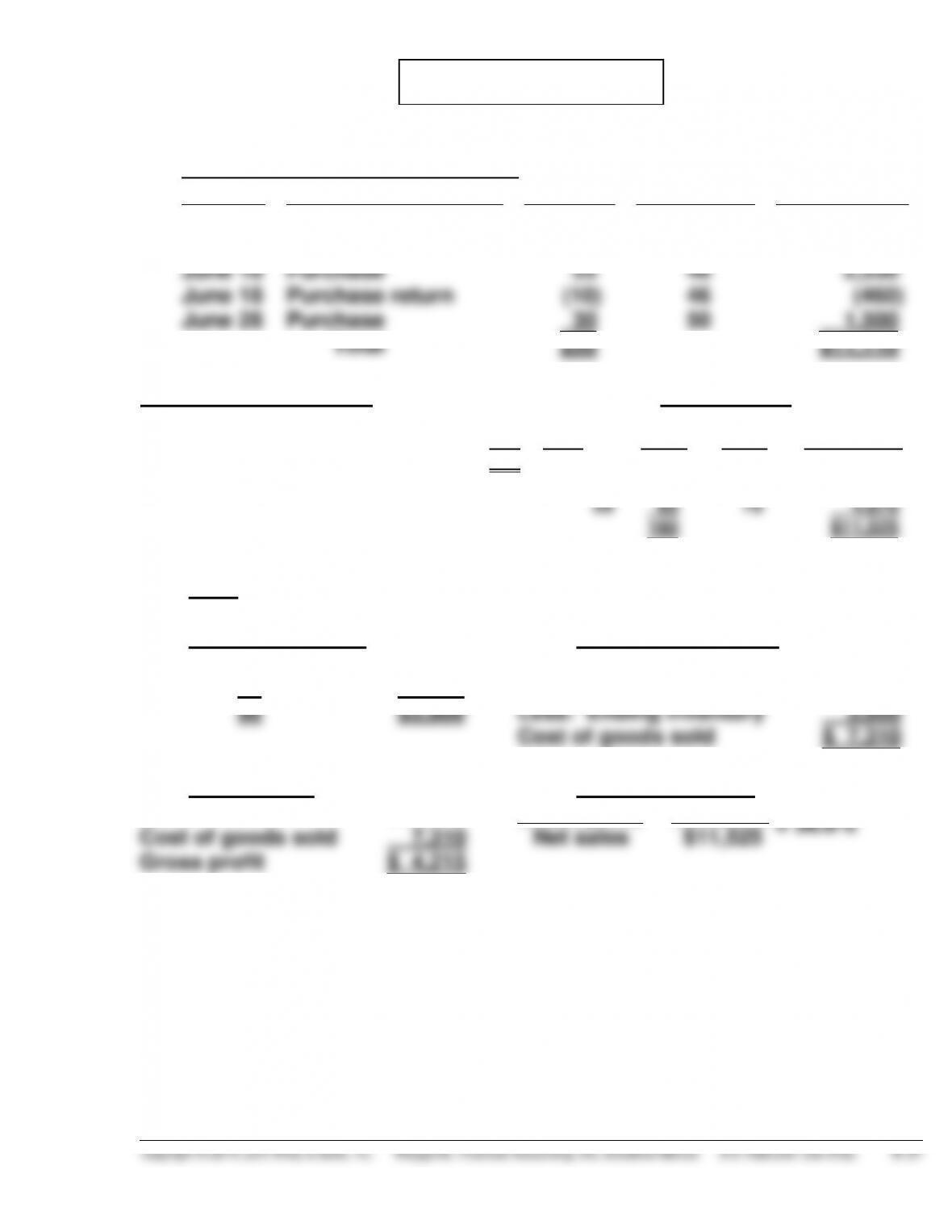

(2)

FIFO

(i)

Ending Inventory

(ii)

Cost of Goods Sold

June 28

18

30 @ $50

45 @ $46

$1,500

2,070

Cost of goods available

for sale

$11,110

4

15 @ $44

660

Less: Ending inventory

4,230

90

$4,230

Cost of goods sold

$ 6,880

(iii)

Gross Profit

(iv)

Gross Profit Rate

Sales revenue

$11,525

Gross profit

$ 4,645

=

40.3%

Cost of goods sold

6,880

Net sales

$11,525

Gross profit

$ 4,645

(3)

Average-Cost

Weighted-average cost per unit:

Cost of goods available for sale

Units available for sale

$11,110

=

$44.44

250

(i)

Ending Inventory

(ii)

Cost of Goods Sold

90 units @$44.44

$3,999.60

Cost of goods available

for sale

$11,110.00

Less: Ending inventory

3,999.60

Cost of goods sold

$ 7,110.40

(iii)

Gross Profit

(iv)

Gross Profit Rate

Sales revenue

$11,525.00

Gross profit

$ 4,414.60

=

38.3%

Cost of goods sold

7,110.40

Net sales

$11,525.00

Gross profit

$ 4,414.60

(b) In this period of rising prices, LIFO gives the highest cost of goods

PROBLEM 6-6A

(a) BARTON INC.

Income Statement (partial)

For the Year Ended December 31, 2015

Specific Identification

FIFO

LIFO

Sales revenuea

$8,915

$8,915

$8,915

Beginning inventory

1,200

1,200

1,200

Purchasesb

6,505

6,505

6,505

Cost of goods available

for sale

7,705

7,705

7,705

Ending inventoryc

2,505

2,720

2,175

Cost of goods sold

5,200

4,985

5,530

Gross profit

$3,715

$3,930

$3,385

(a)(2,300 @ $1.05) + (5,200 @ $1.25)

(b)(2,500 @ $ .65) + (4,000 @ $.72) + (2,500 @ $.80)

(c)Specific identification ending inventory consists of:

Beginning inventory (2,000 liters – 1,000 – 450)

550 @ $.60

$ 330.00

March 3 purchase (2,500 liters – 1,300 – 550)

650 @ $.65

422.50

March 10 purchase (4,000 liters – 2,900)

1,100 @ $.72

792.00

March 20 purchase (2,500 liters – 1,300)

1,200 @ $.80

960.00

3,500 liters

$2,504.50

FIFO ending inventory consists of:

March 20 purchase

2,500 @ $.80

$2,000

March 10 purchase

1,000 @ $.72

720

3,500 liters

$2,720

LIFO ending inventory consists of:

Beginning inventory

2,000 @ $.60

$1,200

March 3 purchase

1,500 @ $.65

975

3,500 liters

$2,175

best support to increase selling prices.

PROBLEM 6-7A

(a) Sherlynn CO.

Condensed Income Statement

For the Year Ended December 31, 2015

FIFO

LIFO

Sales revenue …………………………………….. $700,000 $700,000

Cost of goods sold

Beginning inventory ……………………… 45,000 45,000

Cost of goods purchased ……………… 532,000 532,000

Cost of goods available for sale …….. 577,000 577,000

Ending inventory ………………………….. 168,000a 147,000b

(b) Answers to questions:

(1) The FIFO method produces the most meaningful inventory amount

(2) The LIFO method produces the most meaningful net income

because the costs of the most recent purchases are matched

against sales.

and obsolescence.

(4) There will be $6,300 additional cash available under LIFO because

income taxes are $39,000 under LIFO and $45,300 under FIFO.

(5) The illusionary gross profit is $21,000 or ($291,000 – $270,000).

to replace the units used.