EXERCISE 6-8

(a)

Cost of Goods

Available for Sale

$5,500

÷

Total Units

Available for Sale

900

=

Weighted Average

Unit Cost

$6.11

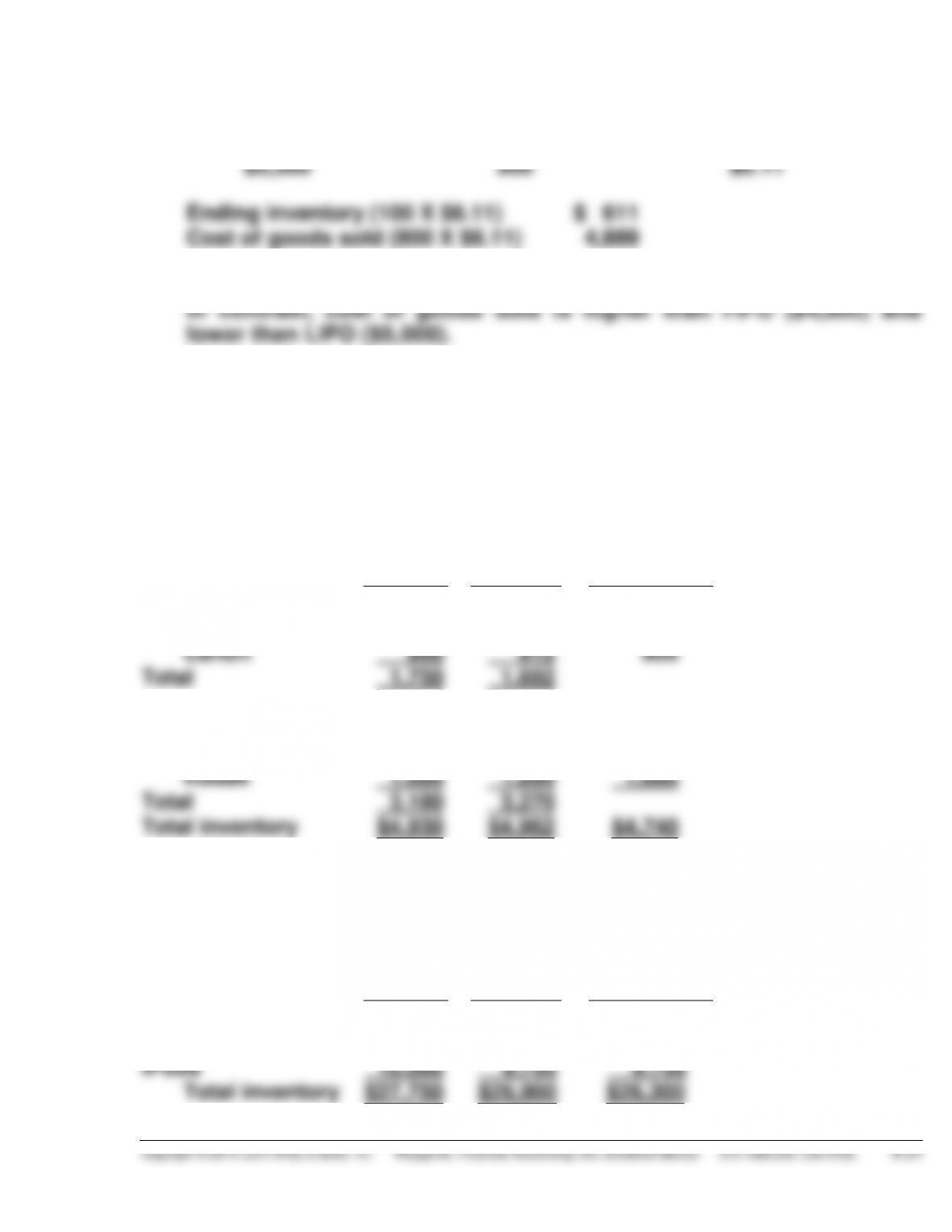

Ending inventory (100 X $6.11) $ 611

Cost of goods sold (800 X $6.11) 4,889

(b) Ending inventory is lower than FIFO ($700) and higher than LIFO ($500).

(c) The average-cost method uses a weighted-average unit cost, not a simple

average of unit costs.

EXERCISE 6-9

Cost

Market

Lower

–of-Cost

–or-Market:

Cameras

Minolta

$ 850

$ 780

$ 780

Canon

900

912

900

Total

1,750

1,692

Light meters

Vivitar

1,500

1,380

1,380

Kodak

1,680

1,890

1,680

Total

3,180

3,270

Total inventory

$4,930

$4,962

$4,740

EXERCISE 6-10

Cost

Market

Lower

–of-Cost-

or-Market:

Cameras

$ 6,500

$ 7,100

$ 6,500

DVD players

11,250

10,050

10,050

iPods

10,000

9,750

9,750

Total inventory

$27,750

$26,900

$26,300

EXERCISE 6-11

2014

2015

Beginning inventory …………………………………….. $ 20,000 $ 27,000

Cost of goods purchased …………………………….. 150,000 175,000

a$30,000 – $3,000 = $27,000. b$35,000 + $6,000 = $41,000.

EXERCISE 6-12

(a)

2014

2015

Sales revenue ………………………………………….. $220,000 $250,000

Cost of goods sold

Beginning inventory …………………………... 32,000 38,000

Cost of goods purchased …………………… 173,000 202,000

shown below:

Difference $ 0

(c) Dear Mr./Ms. President:

Because your ending inventory of December 31, 2014 was overstated

In a periodic system, the cost of goods sold is calculated by deducting

the cost of ending inventory from the total cost of goods you have

EXERCISE 6-12 (Continued)

The error also affects the balance sheet at the end of 2014. The inven-

tory reported in the balance sheet is overstated; therefore, total assets

are overstated. The overstatement of the 2014 net income results in the

EXERCISE 6-13

2013

2014

2015

Inventory

turnover

$900,000

$1,120,000

$1,300,000

($100,000 + $300,000) ÷ 2

($300,000 + $400,000) ÷ 2

($400,000 + $480,000) ÷ 2

$900,000

= 4.5

$1,120,000

= 3.2

$1,300,000

= 2.95

$200,000

$350,000

$440,000

Days in

inventory

365

= 81.1 days

365

= 114.1 days

365

= 123.7 days

4.5

3.2

2.95

Gross

profit rate

$1,200,000 – $900,000

= 25%

$1,600,000 – $1,120,000

= 30%

$1,900,000 – $1,300,000

= 32%

$1,200,000

$1,600,000

$1,900,000

The inventory turnover decreased by approximately 34% from 2013 to 2015

while the days in inventory increased by almost 53% over the same time

EXERCISE 6-14

(a)

Alpha Company

Omega Company

Inventory Turnover

$190,000

$292,000

($45,000 + $55,000)/2

= 3.80

($71,000 + $69,000)/2

= 4.17

Days in Inventory

365/3.80 = 96 days

365/4.17 = 88 days

(b) Omega Company is moving its inventory more quickly, since its inven-

tory turnover is higher, and its days in inventory is lower.

*EXERCISE 6-15

(1)

FIFO

Date

Purchases

Cost of Goods Sold

Balance

Jan. 1

(3 @ $600)

$1,800

8

(2 @ $600) $1,200

(1 @ $600)

600

10

(6 @ $660) $3,960

(1 @ $600)

4,560

(6 @ $660)

15

(1 @ $600)

(3 @ $660) $2,580

(3 @ $660)

1,980

(2)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

Jan. 1

(3 @ $600)

$1,800

8

(2 @ $600) $1,200

(1 @ $600)

600

10

(6 @ $660) $3,960

(1 @ $600)

4,560

(6 @ $660)

15

(4 @ $660) $2,640

(1 @ $600)

1,920

(2 @ $660)

*EXERCISE 6-15 (Continued)

(3)

MOVING-AVERAGE COST

Date

Purchases

Cost of Goods Sold

Balance

Jan. 1

(3 @ $600) $1,800

8

(2 @ $600) $1,200

(1 @ $600) 600

10

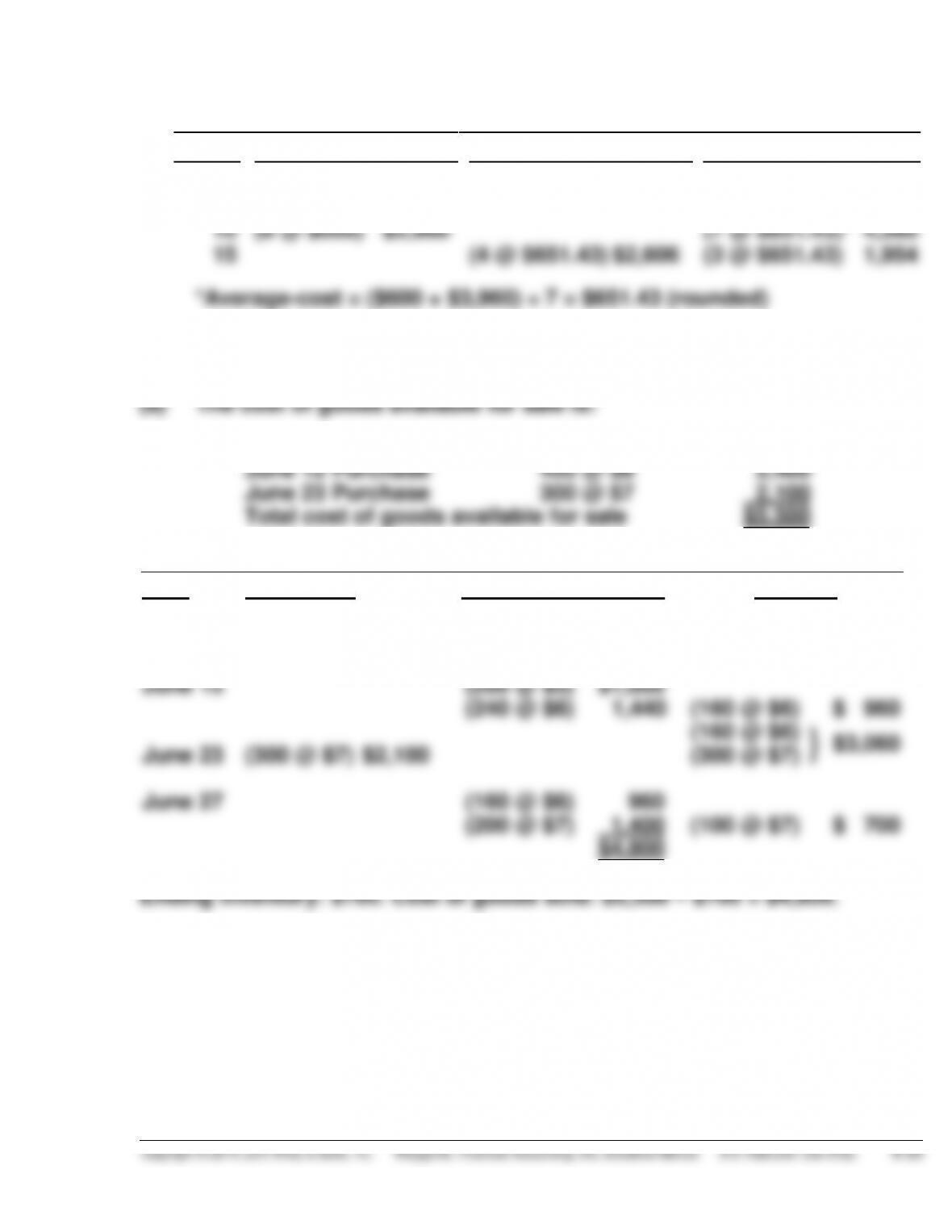

(6 @ $660) $3,960

(7 @ $651.43)* 4,560

15

(4 @ $651.43) $2,606

(3 @ $651.43) 1,954

*EXERCISE 6-16

June 1 Inventory

200 @ $5

$1,000

June 12 Purchase

400 @ $6

2,400

June 23 Purchase

300 @ $7

2,100

Total cost of goods available for sale

$5,500

FIFO

Date

Purchases

Cost of Goods Sold

Balance

June 1

(200 @ $5)

$1,000

June 12

(400 @ $6) $2,400

(200 @ $5)

}

$3,400

(400 @ $6)

June 15

(200 @ $5)

$1,000

(240 @ $6)

1,440

(160 @ $6)

$ 960

(160 @ $6)

}

$3,060

June 23

(300 @ $7) $2,100

(300 @ $7)

June 27

(160 @ $6)

960

(200 @ $7)

1,400

(100 @ $7)

$ 700

$4,800

*EXERCISE 6-16 (Continued)

LIFO

Date

Purchases

Cost of Goods Sold

Balance

June 1

(200 @ $5)

$1,000

June 12

(400 @ $6) $2,400

(200 @ $5)

}

$3,400

(400 @ $6)

June 15

(400 @ $6)

$2,400

(40 @ $5)

$ 200

(160 @ $5)

$ 800

(160 @ $5)

}

$2,900

June 23

(300 @ $7) $2,100

(300 @ $7)

June 27

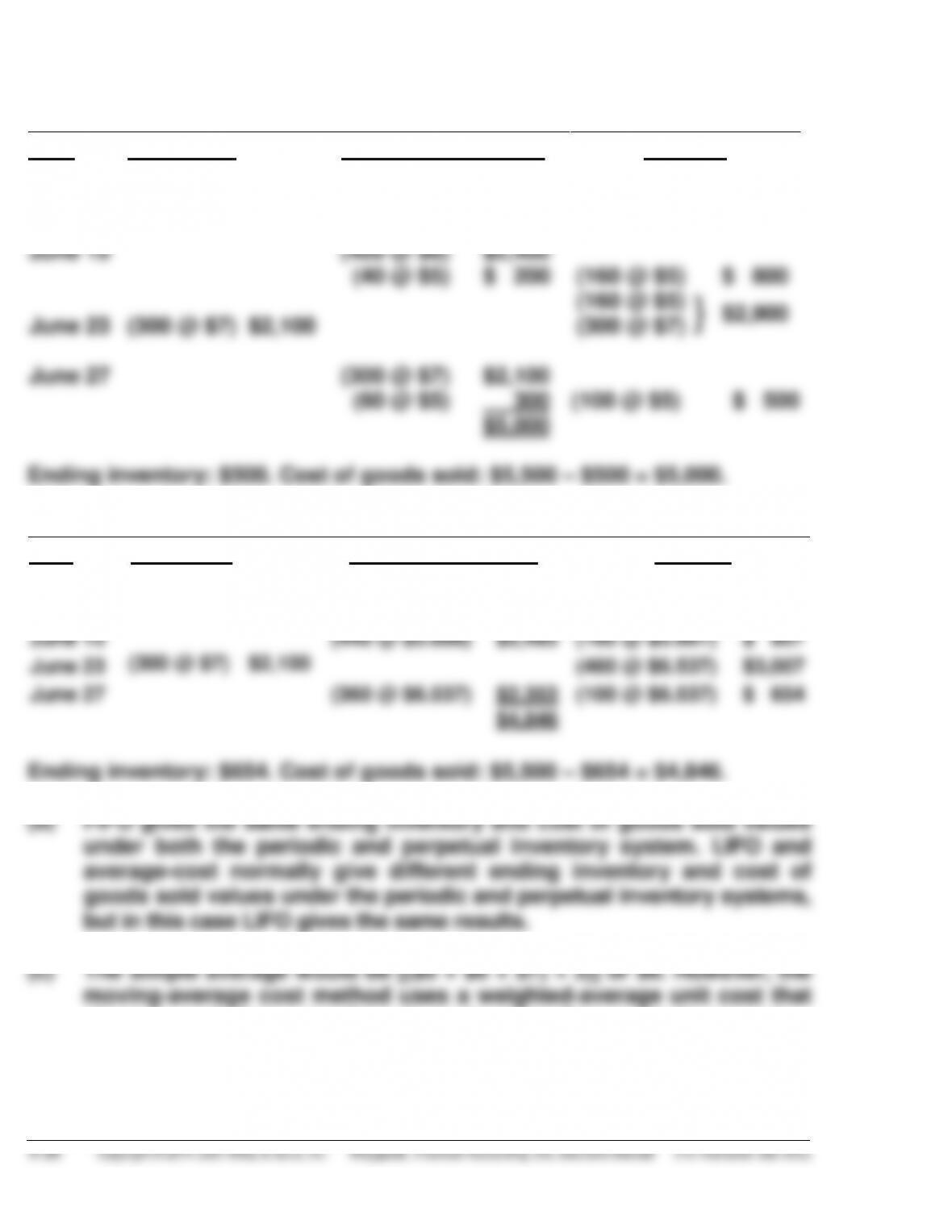

(300 @ $7)

$2,100

(60 @ $5)

300

$5,000

(100 @ $5)

$ 500

Ending inventory: $500. Cost of goods sold: $5,500 – $500 = $5,000.

Moving-Average Cost

Date

Purchases

Cost of Goods Sold

Balance

June 1

(200 @ $5) $1,000

June 12

(400 @ $6) $2,400

(600 @ $5.667) $3,400

June 15

(440 @ $5.666)

$2,493

(160 @ $5.667) $ 907

June 23

(300 @ $7) $2,100

(460 @ $6.537) $3,007

June 27

(360 @ $6.537)

$2,353

(100 @ $6.537) $ 654

$4,846

Ending inventory: $654. Cost of goods sold: $5,500 – $654 = $4,846.

changes each time a purchase is made rather than a simple average.

*EXERCISE 6-17

(a)

FIFO

Date

Purchases

Cost of

Goods Sold

Balance

9/1

(26 @ $ 97)

$2,522

9/5

(12 @ $ 97) $1,164

(14 @ $ 97)

$1,358

9/12

(45 @ $102) $4,590

(14 @ $ 97)

$5,948

(45 @ $102)

9/16

(14 @ $ 97)

(36 @ $102) $5,030

( 9 @ $102)

$ 918

9/19

(20 @ $104) $2,080

( 9 @ $102)

$2,998

(20 @ $104)

9/26

(50 @ $105) $5,250

( 9 @ $102)

(20 @ $104)

$8,248

(50 @ $105)

9/29

( 9 @ $102)

(20 @ $104)

(30 @ $105) $6,148

(20 @ $105) $2,100

LIFO

Date

Purchases

Cost of

Goods Sold

Balance

9/1

(26 @ $ 97)

$2,522

9/5

(12 @ $ 97) $1,164

(14 @ $ 97)

$1,358

9/12

(45 @ $102) $4,590

(14 @ $ 97)

$5,948

(45 @ $102)

9/16

(45 @ $102)

( 5 @ $ 97) $5,075

( 9 @ $ 97)

$ 873

9/19

(20 @ $104) $2,080

( 9 @ $ 97)

$2,953

(20 @ $104)

9/26

(50 @ $105) $5,250

( 9 @ $ 97)

$8,203

(20 @ $104)

(50 @ $105)

9/29

(50 @ $105)

( 9 @ $ 97)

$2,017

( 9 @ $104) $6,186

(11 @ $104)

*EXERCISE 6-17 (Continued)

Moving-Average Cost

Date

Purchases

Cost of

Goods Sold

Balance

9/1

(26 @ $97) $2,522

9/5

(12 @ $97) $1,164

(14 @ $97) $1,358

9/12

(45 @ $102) $4,590

(59 @ $100.81)a $5,948

9/16

(50 @ $100.81) $5,041*

( 9 @ $100.81) $ 907

9/19

(20 @ $104) $2,080

(29 @ $103.00)b $2,987

9/26

(50 @ $105) $5,250

(79 @ $104.27)c $8,237

9/29

(59 @ $104.27) $6,152*

(20 @ $104.27) $2,085

*Rounded

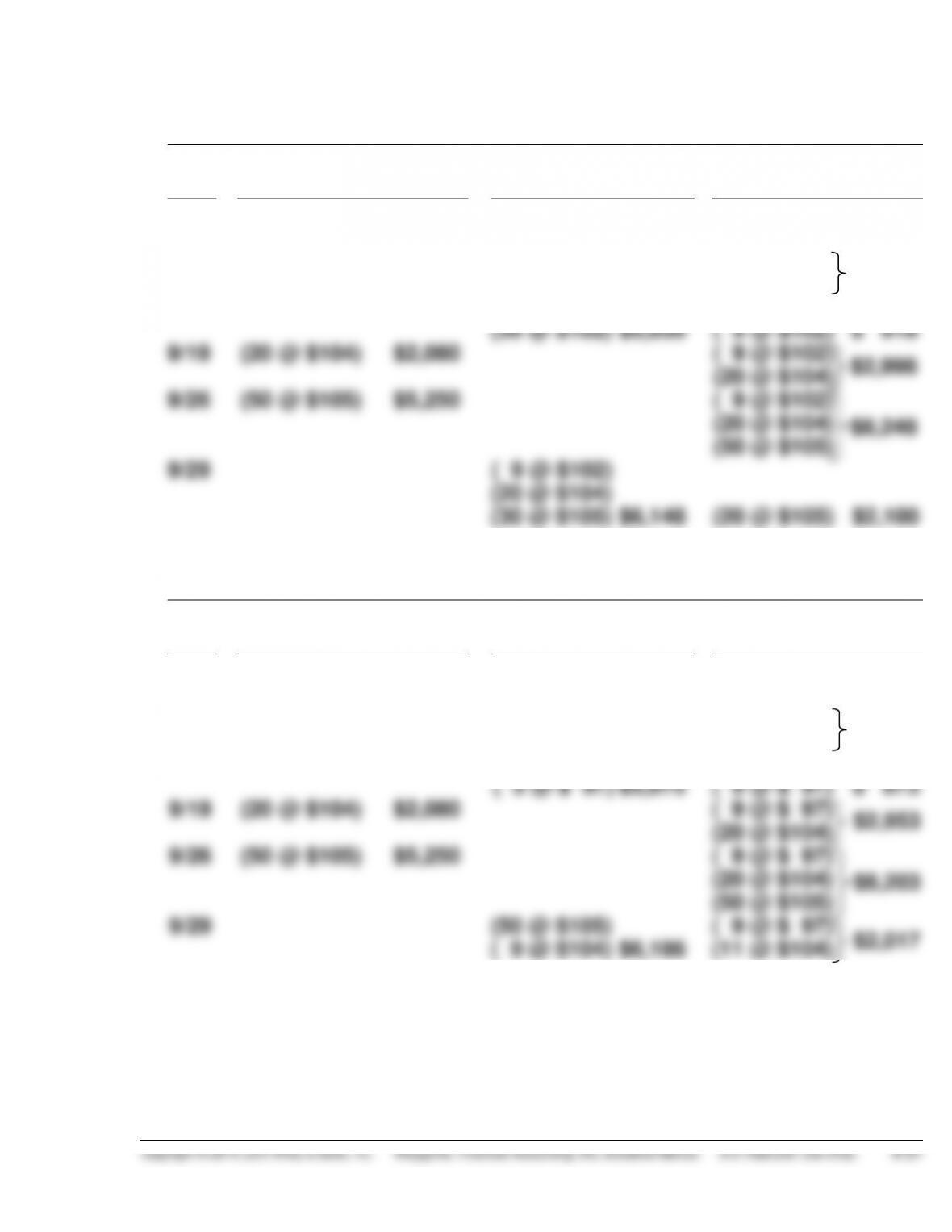

a $5,948 ÷ 59 = $100.81

(b)

Periodic

Perpetual

Ending Inventory FIFO

$2,100

$2,100

Ending Inventory LIFO

$1,940

$2,017

and perpetual inventory system.

LIFO usually yields different ending inventory values when using the

periodic versus perpetual inventory system.

*EXERCISE 6-18

(a) Sales ……………………………………………………………. $840,000

Cost of goods sold

Inventory, November 1 ………………………….. $130,000

Cost of goods purchased ……………………… 536,000

*EXERCISE 6-18 (Continued)

(b) Sales revenue ……………………………………………………………… $1,000,000

Less: Estimated gross profit (35% X $1,000,000) …………… 350,000

Estimated cost of goods sold ……………………………………….. $ 650,000

*EXERCISE 6-19

(a) Net sales ($51,000 – $1,000) ………………………………………….. $50,000

Less: Estimated gross profit (40% X $50,000) ……………….. 20,000

Estimated cost of goods sold ……………………………………….. $30,000

(b) Net sales ……………………………………………………………………… $50,000

Less: Estimated gross profit (30% X $50,000) ……………….. 15,000

Estimated cost of goods sold ……………………………………….. $35,000

*EXERCISE 6-20

Women’s Shoes

Men’s Shoes

Cost

Retail

Cost

Retail

Beginning inventory

$ 25,000

$ 46,000

$ 45,000

$ 60,000

Goods purchased

110,000

179,000

136,300

185,000

Goods available for sale

$135,000

225,000

$181,300

245,000

Less: Net sales

178,000

185,000

Ending inventory at retail

$ 47,000

$ 60,000

Cost-to-retail ratio

$135,000

= 60%

$181,300

= 74%

$225,000

$245,000

Estimated cost of ending