BRIEF EXERCISE 6-4

Average unit cost is $6.89 computed as follows:

BRIEF EXERCISE 6-5

(a) FIFO would result in the highest net income.

(b) FIFO would result in the highest ending inventory.

BRIEF EXERCISE 6-6

Cost of good sold under:

LIFO

FIFO

Purchases

$6 X 120

$6 X 120

$7 X 200

$7 X 200

$8 X 140

$8 X 140

Cost of goods available for sale

$ 3,240

$ 3,240

Less: Ending inventory

1,140

1,400

Cost of goods sold

$ 2,100

$ 1,840

the company can expect to earn in future periods.

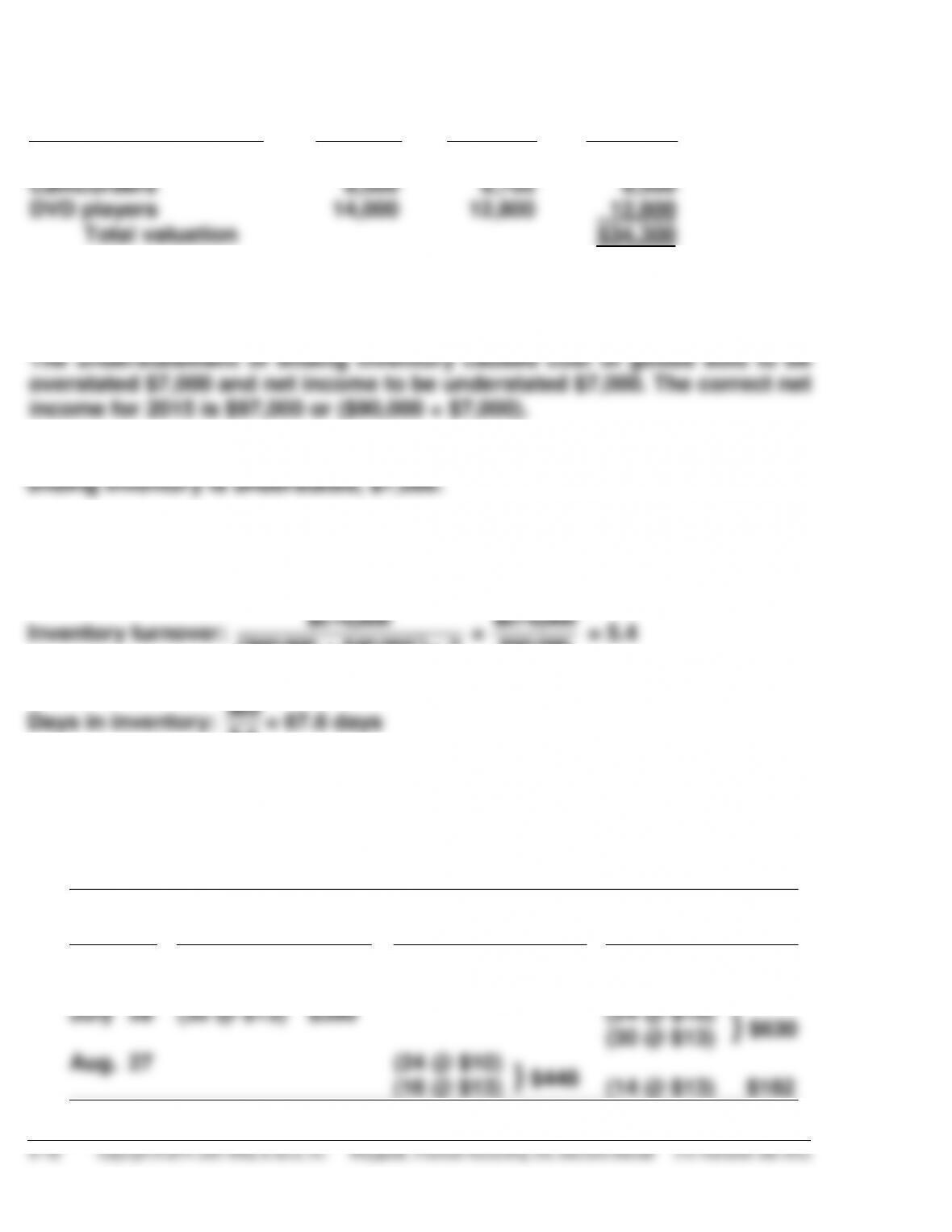

BRIEF EXERCISE 6-7

Inventory Categories

Cost

Market

LCM

Cameras

$12,000

$12,100

$12,000

Camcorders

9,500

9,700

9,500

DVD players

14,000

12,800

12,800

Total valuation

$34,300

BRIEF EXERCISE 6-8

Total assets in the balance sheet will be understated by the amount that

BRIEF EXERCISE 6-9

Inventory turnover:

$270,000

$60,000 + $40,000

÷ 2

=

$270,000

$50,000

= 5.4

Days in inventory:

365

5.4

= 67.6 days

*BRIEF EXERCISE 6-10

(a) FIFO Method

Product E2-D2

Date

Purchases

Cost of

Goods Sold

Balance

May 7

(50 @ $10) $500

(50 @ $10) $500

June 1

(26 @ $10) $260

(24 @ $10) $240

July 28

(30 @ $13) $390

(24 @ $10)

} $630

(30 @ $13)

Aug. 27

(24 @ $10)

} $448

(16 @ $13)

(14 @ $13) $182

*BRIEF EXERCISE 6-10 (Continued)

(b) LIFO Method

Product E2-D2

Date

Purchases

Cost of

Goods Sold

Balance

May 7

(50 @ $10) $500

(50 @ $10) $500

June 1

(26 @ $10) $260

(24 @ $10) $240

July 28

(30 @ $13) $390

(24 @ $10)

} $630

(30 @ $13)

Aug. 27

(30 @ $13)

} $490

(10 @ $10)

(14 @ $10) $140

(c) Average-Cost

Product E2-D2

Date

Purchases

Cost of

Goods Sold

Balance

May 7

(50 @ $10) $500

(50 @ $10) $500

June 1

(26 @ $10) $260

(24 @ $10) $240

July 28

(30 @ $13) $390

(54 @ $11.67)* $630

Aug. 27

(40 @ $11.67) $467

(14 @ $11.67) $163

*($240 + $390) ÷ 54

*BRIEF EXERCISE 6-11

(1) Net sales ………………………………………………………………….. $330,000

(2) Cost of goods available for sale ………………………………… $230,000

*BRIEF EXERCISE 6-12

At Cost

At Retail

Goods available for sale

$38,000

$50,000

Net sales

40,000

Ending inventory at retail

$10,000

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 6-1

Inventory per physical count ……………………………………………. $300,000

Inventory out on consignment …………………………………………. 26,000

DO IT! 6-2

Cost of goods available for sale = (3,000 X $5) + (8,000 X $7) = $71,000

(a) FIFO: $71,000 – (1,600 X $7) = $59,800

DO IT! 6-3

these figures, $476,000.

(b)

2014

2015

Ending inventory

$31,000 understated

No effect

Cost of goods sold

$31,000 overstated

$31,000 understated

Stockholders’ equity

$31,000 understated

No effect

DO IT! 6-4

2014

2015

Inventory turnover

$1,200,000

=

6

$1,425,000

=

8.9

($180,000 + $220,000)/2

($220,000 + $100,000)/2

Days in inventory

365 ÷ 6 = 60.8 days

365 ÷ 8.9 = 41 days

The company experienced a very significant decline in its ending inventory

as a result of the just-in-time inventory. This decline improved its inventory

SOLUTIONS TO EXERCISES

EXERCISE 6-1

EXERCISE 6-2

Ending inventory—as reported …………………………………………….. $740,000

1. Subtract from inventory: The goods belong to

Harmon Corporation. Schuda is merely holding

5. Add to inventory: Reza Sales ordered goods

with a cost of $8,000. Schuda should record the

EXERCISE 6-2 (Continued)

6. Subtract from inventory: GAAP require that inventory

be valued at the lower of cost or market. Obsolete parts

EXERCISE 6-3

(a) FIFO Cost of Goods Sold

(b) It could choose to sell specific units purchased at specific costs if it

wished to impact earnings selectively. If it wished to minimize earnings

(c) I recommend they use the FIFO method because it produces a more

appropriate balance sheet valuation and reduces the opportunity to

manipulate earnings.

(The answer may vary depending on the method the student chooses.)

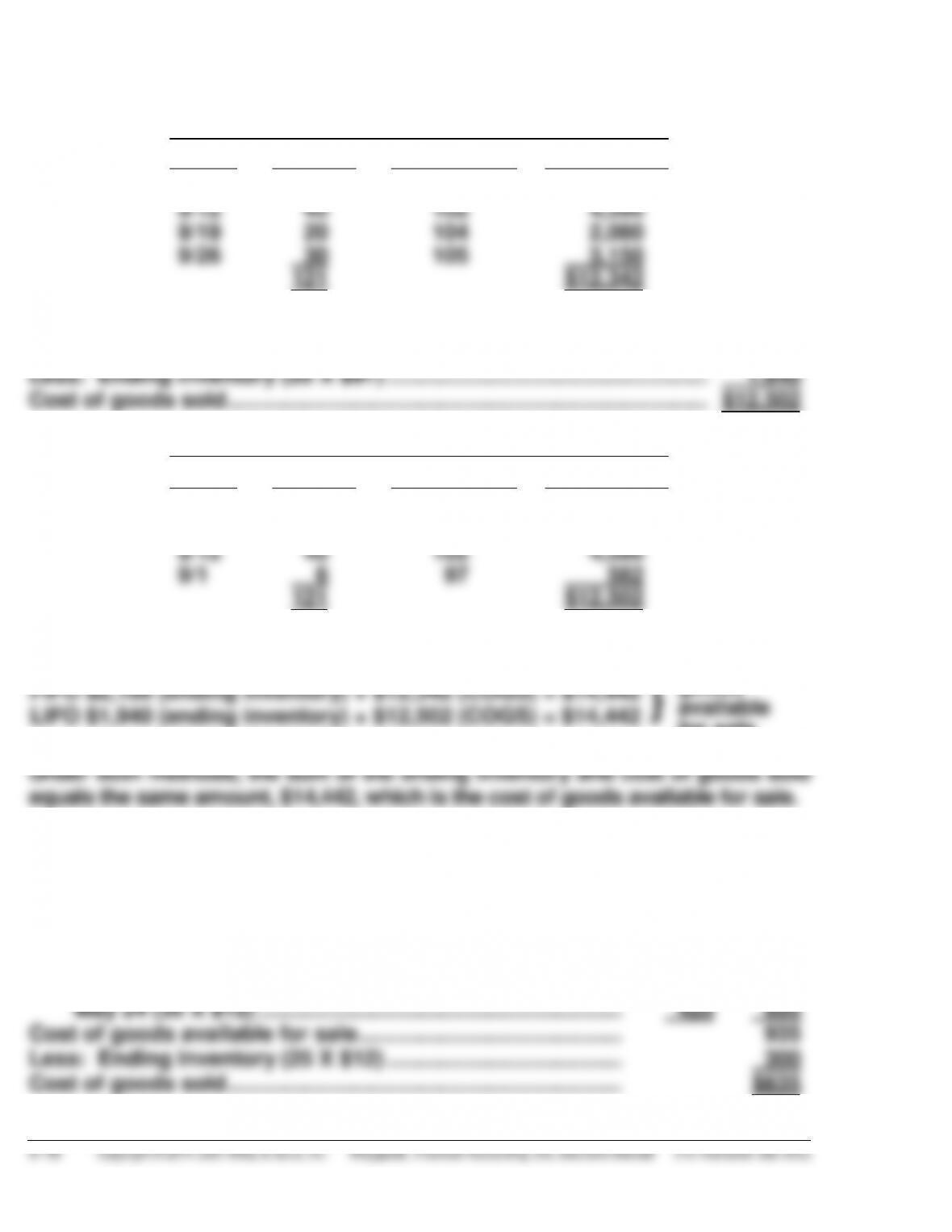

EXERCISE 6-4

(a) FIFO

Beginning inventory (26 X $97) …………………………….. $ 2,522

Purchases

Sept. 12 (45 X $102) ……………………………………….. $4,590

Sept. 19 (20 X $104) ……………………………………….. 2,080

EXERCISE 6-4 (Continued)

Proof

Date

Units

Unit Cost

Total Cost

9/1

26

$ 97

$ 2,522

9/12

45

102

4,590

9/19

20

104

2,080

9/26

30

105

3,150

121

$12,342

LIFO

Cost of goods available for sale………………………………………………… $14,442

Proof

Date

Units

Unit Cost

Total Cost

9/26

50

$105

$ 5,250

9/19

20

104

2,080

9/12

9/1

45

6

102

97

4,590

582

121

$12,502

(b)

FIFO $2,100 (ending inventory) + $12,342 (COGS) = $14,442

}

Cost of

goods

available

for sale

LIFO $1,940 (ending inventory) + $12,502 (COGS) = $14,442

EXERCISE 6-5

FIFO

Beginning inventory (30 X $8) ………………………………………. $240

Purchases

May 15 (25 X $11) ………………………………………………….. $275

EXERCISE 6-5 (Continued)

Proof

Date

Units

Unit Cost

Total Cost

5/1

30

$ 8

$240

5/15

25

11

275

5/24

10

12

120

65

$635

LIFO

Proof

Date

Units

Unit Cost

Total Cost

5/24

35

$12

$420

5/15

25

11

275

5/1

5

8

40

65

$735

EXERCISE 6-6

(a) FIFO

LIFO

Cost of goods available for sale ……………………….. $5,500

EXERCISE 6-6 (Continued)

(b) The FIFO method will produce the higher ending inventory because

costs have been rising. Under this method, the earliest costs are

(c) The LIFO method will produce the higher cost of goods sold for Kaleta

Company. Under LIFO the most recent costs are charged to cost of

EXERCISE 6-7

(a) (1) FIFO

Beginning inventory …………………………………… $10,000

(2) LIFO

Beginning inventory …………………………………… $10,000

(3) AVERAGE-COST

Beginning inventory …………………………………… $10,000

Purchases …………………………………………………. 26,000

lower costs are matched with revenues.

(c) The use of FIFO would result in inventories approximating current cost in

the balance sheet, since the more recent units are assumed to be on hand.

year since income will be lower.