CHAPTER 5

ACCOUNTING FOR MERCHANDISING

OPERATIONS

LEARNING OBJECTIVES

1. IDENTIFY THE DIFFERENCES BETWEEN SERVICE AND

MERCHANDISING COMPANIES.

2. EXPLAIN THE RECORDING OF PURCHASES UNDER

A PERPETUAL INVENTORY SYSTEM.

3. EXPLAIN THE RECORDING OF SALES REVENUES

UNDER A PERPETUAL INVENTORY SYSTEM.

A MERCHANDISING COMPANY.

5. DISTINGUISH BETWEEN A MULTIPLE-STEP AND A

SINGLE-STEP INCOME STATEMENT.

*6. PREPARE A WORKSHEET FOR A MERCHANDISING

COMPANY.

*7. EXPLAIN THE RECORDING OF PURCHASES AND

SALES OF INVENTORY UNDER A PERIODIC INVENTORY

SYSTEM.

CHAPTER REVIEW

Merchandising Operations

1. (L.O. 1) A merchandising company is an enterprise that buys and sells merchandise as their

2. The primary source of revenue for a merchandising company is sales revenue. Expenses are divided

3. Sales less cost of goods sold is called the gross profit. For example, if sales are $5,000 and cost

of goods sold is $3,000, gross profit is $2,000.

5. Operating expenses are expenses incurred in the process of recognizing sales revenue.

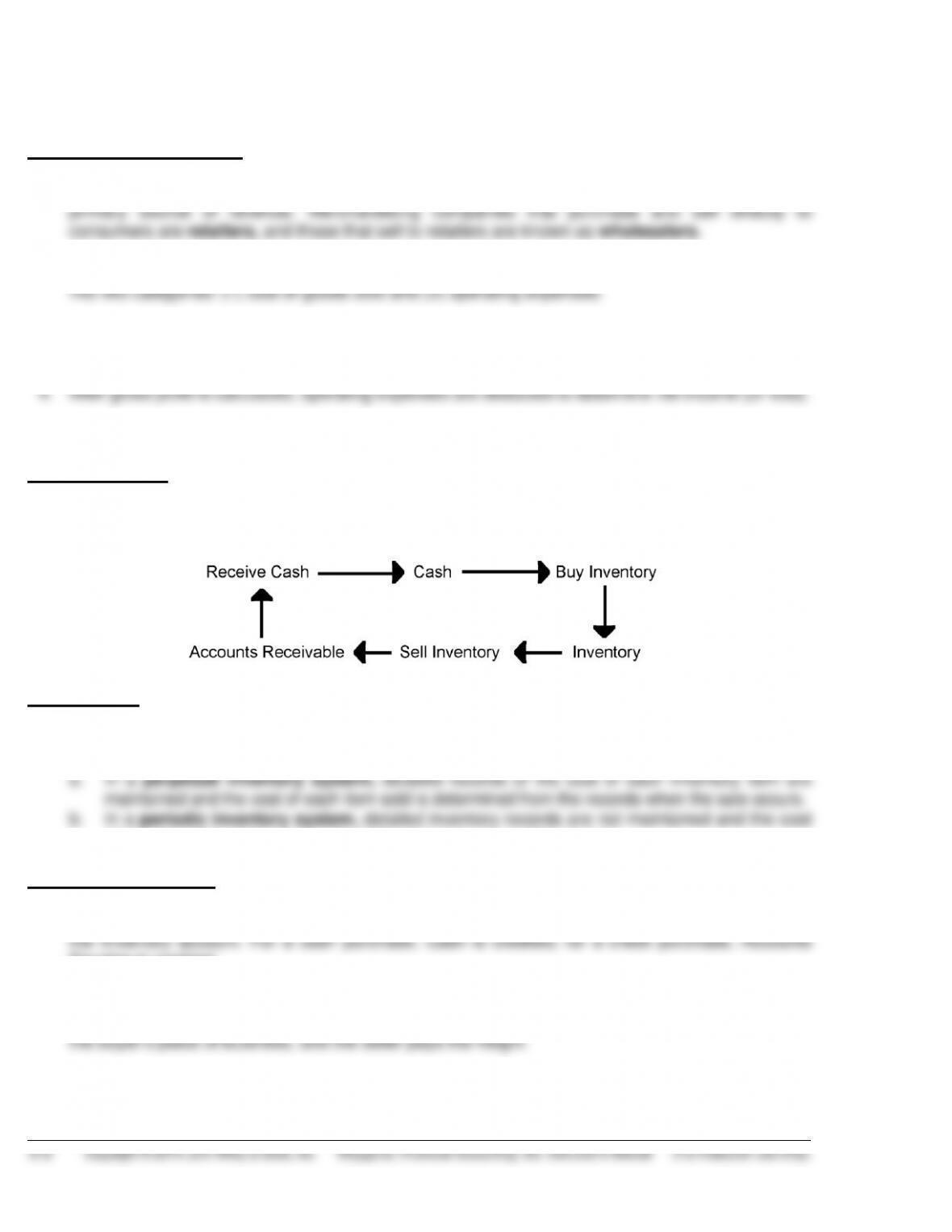

Operating Cycles

6. The operating cycle of a merchandising company is as follows:

Flow of Costs

7. A merchandising company may use either a perpetual or a periodic inventory system in deter–

mining cost of goods sold.

of goods sold is determined only at the end of an accounting period.

Purchase Transactions

8. (L.O. 2) Under the perpetual inventory system, purchases of merchandise for sale are recorded in

Payable is credited.

9. FOB shipping point means that goods are placed free on board the carrier by the seller, and the

buyer must pay the freight costs. FOB destination means that goods are placed free on board at

Copyright © 2014 John Wiley & Sons, Inc. Weygandt, Financial Accounting, 9/e, Instructor’s Manual (For Instructor Use Only) 5-3

10. When the purchaser pays the freight, Inventory is debited and Cash is credited. When the seller

pays the freight, Freight-Out (Delivery Expense) is debited and Cash is credited. This account is

classified as an operating expense by the seller.

11. A purchaser may be dissatisfied with the merchandise received because the goods may be

Inventory is credited.

12. When the credit terms of a purchase on account permit the purchaser to claim a cash discount for

is no purchase discount, and the net amount of the bill is due within 30 days.

13. When an invoice is paid within the discount period, the amount of the discount is credited to

Sales Transactions

14. (L.O. 3) In accordance with the revenue recognition principle, companies record sales

15. All sales transactions should be supported by a business document. Cash register documents

16. A sale on credit is recorded as follows:

Accounts Receivable ……………………………………………………………. XXXX

Sales Revenue ……………………………………………………………… XXXX

Cost of Goods Sold ……………………………………………………………… XXXX

Inventory ……………………………………………………………………… XXXX

Cash ………………………………………………………………………………….. XXXX

Accounts Receivable ……………………………………………………. XXXX

Sales Returns and Allowances

17. A sales return results when a customer is dissatisfied with merchandise and is allowed to return

selling price.

18. To give the customer a sales return or allowance, the seller normally makes the following entry if

the sale was a credit sale (the second entry is made only if the goods are returned):

Sales Returns and Allowances ……………………………………………. XXXX

Accounts Receivable …………………………………………………… XXXX

Inventory ………………………………………………………………………….. XXXX

Cost of Goods Sold …………………………………………………….. XXXX

19. Sales Returns and Allowances is a contra revenue account and the normal balance of the

account is a debit.

Sales Discounts

within 30 days. Sales Discounts is a contra revenue account and the normal balance of this

account is a debit.

21. Both Sales Returns and Allowances and Sales Discounts are subtracted from Sales Revenue in

The Accounting Cycle

22. (L.O. 4) Each of the required steps in the accounting cycle for a service company applies to a

merchandising company.

Adjusting Entries and Closing Entries

23. A merchandising company generally has the same types of adjusting entries as a service com-

income to Income Summary.

Multiple-Step vs. Single-Step Income Statement

24. (L.O. 5) A multiple-step income statement shows several steps in determining net income:

(1) cost of goods sold is subtracted from net sales to determine gross profit and (2) operating

nonoperating sections for:

a. Revenues and expenses that result from secondary or unrelated operations, and

b. Gains and losses that are unrelated to the company’s operations.

Gross Profit and Operating Expenses

25. Gross profit is net sales less cost of goods sold. The gross profit rate is expressed as a

26. Nonoperating sections are reported in the income statement after income from operations and are

27. In a single-step income statement all data is classified into two categories: (a) Revenues (both

Classified Balance Sheet

28. A merchandising company generally has the same type of balance sheet as a service company

except inventory is reported as a current asset.

Using a Worksheet

*29. (L.O. 6) As indicated in Chapter 4, a worksheet enables financial statements to be prepared before

the adjusting entries are journalized and posted. The steps in preparing a worksheet for a

merchandising company are the same as they are for a service company except the additional

merchandising accounts are included.

Determining Cost of Goods Sold Under a Periodic System

*30. (L.O. 7) Under a periodic system separate accounts are used to record freight costs, returns,

and discounts. In addition, a running account of changes in inventory is not maintained. Instead, the

balance in ending inventory, as well as cost of goods sold for the period, is calculated at the end

of the period. The determination of cost of goods sold for Tsutsui Co. using a periodic inventory

system, is as follows:

TSUTSUI COMPANY

Cost of Goods Sold

For the Year Ended December 31, 2015

Cost of goods sold

Inventory, January 1 ………………………………. $ 28,000

Purchases…………………………………………….. $234,000

Less: Purchases returns and allowances ….. $8,200

Purchase discounts ………………………. 4,600 12,800

Net purchases ………………………………………. 221,200

Add: Freight-in ……………………………………… 10,800

Cost of goods purchased ………………………… 232,000

Cost of goods available for sale ……………….. 260,000

Inventory, December 31 ………………………….. 30,000

Cost of goods sold …………………………………. 230,000

5-6 Copyright © 2014 John Wiley & Sons, Inc. Weygandt, Financial Accounting, 9/e, Instructor’s Manual (For Instructor Use Only)

*31. To determine the cost of goods sold under a periodic inventory system, three steps are

required: (1) Record purchases of merchandise; (2) Determine the cost of goods purchased; and

(3) Determine the cost of goods on hand at the beginning and end of the accounting period.

*32. In determining cost of goods purchased, (a) contra-purchase accounts (purchase

returns/allowances and purchase discounts) are subtracted from purchases to produce net

purchases, and (b) freight-in is then added to net purchases.

inventory.

*34. Cost of goods sold is determined by two steps:

a. The cost of goods purchased is added to the cost of goods on hand at the beginning of the

period to obtain the cost of goods available for sale.

available for sale.

Recording Purchases and Sales of Merchandise

*35. (S.O. 7) In a periodic inventory system revenues from the sale of merchandise are recorded

*36. Under the periodic inventory system, purchases of merchandise for sale are recorded in the

Purchases account. For a cash purchase, Cash is credited; for a credit purchase, Accounts Payable

is credited.

*38. If payment is made within the discount period, the amount of the discount is credited to the

account Purchases Discounts. When an invoice is not paid within the discount period, then the

usual entry is made with a debit to Accounts Payable and a credit to Cash.

LECTURE OUTLINE

A. Merchandising Operations.

1. The primary source of revenues for merchandising companies is the sale

of merchandise, referred to as sales revenue or sales.

2. A merchandising company has two categories of expenses:

period.

b. Operating expenses are expenses incurred in the process of earning

sales revenues.

3. Gross profit is the difference between sales revenue and cost of goods sold.

4. In a perpetual inventory system, companies keep detailed records of the

INVESTOR INSIGHT

Morrow Snowboards implemented a perpetual inventory system to improve its

control over inventory. It also stated that it would perform a physical inventory

count every quarter until it felt that the perpetual inventory system was reliable.

If a perpetual system keeps track of inventory on a daily basis, why do companies

ever need to do a physical count?

B. Recording Purchases and Sales of Merchandise.

1. Under a perpetual inventory system:

accounts rather than to Inventory.

b. The company debits the Inventory account for all purchases of

merchandise and freight-in, and credits it for purchase discounts and

purchase returns and allowances. Freight terms are expressed as

either FOB shipping point or FOB destination.

Out (Delivery Expense).

c. A purchaser may return goods to the seller for credit because the

goods are damaged or defective, or of inferior quality. The return of

goods to the seller is known as a purchase return.

discount a purchase discount.

(2) In accordance with the revenue recognition principle, companies

record sales revenues when the performance obligation is

satisfied. Typically the performance obligation is satisfied when

goods transfer from the seller to the buyer.

(4) The cost of goods sold is recognized for each sale by debiting

Cost of Goods Sold and crediting Inventory.

returns and allowances.

(6) Companies record the cost of goods returned by decreasing Cost of

Goods Sold and increasing the Inventory account.

(7) A sales discount occurs when the seller offers a cash discount for

prompt payment of the balance due.

debit.