CHAPTER 4

Completing the Accounting Cycle

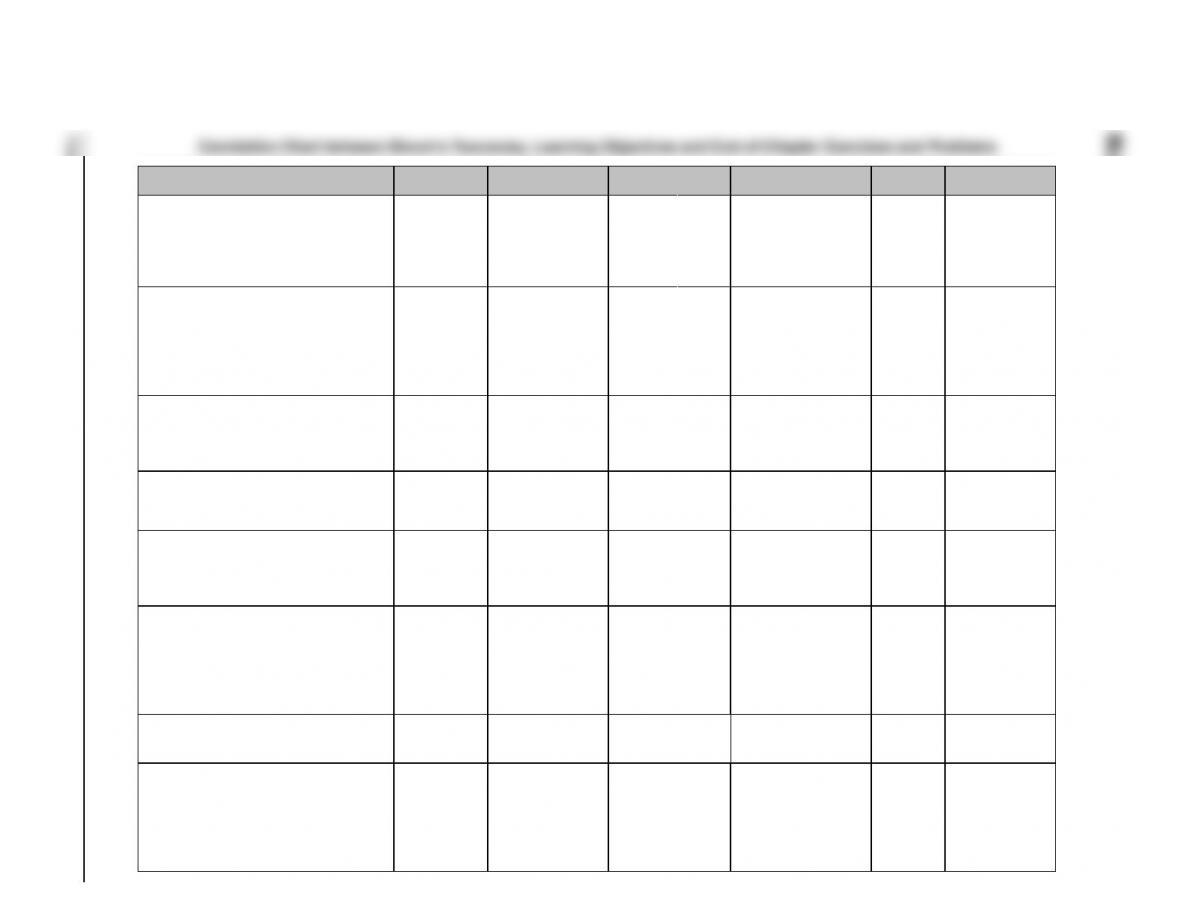

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

B

Problems

*1. Prepare a worksheet.

1, 2, 3,

4, 5

1, 2, 3

1

1, 2, 3,

5, 6

1A, 2A, 3A,

4A, 5A

1B, 2B, 3B,

4B, 5B

*2. Explain the process

of closing the books.

6, 7, 11

4, 5, 6

2

4, 7, 8,

11, 19

1A, 2A, 3A,

4A, 5A

1B, 2B, 3B,

4B, 5B

*3. Describe the content and

purpose of a post-closing

trial balance.

8, 9

7

4, 7, 8

1A, 2A, 3A,

4A, 5A

1B, 2B, 3B,

4B, 5B

*4. State the required steps in

the accounting cycle.

10, 11, 12

8

10, 19

5A

5B

*5. Explain the approaches

to preparing correcting

entries.

13

9

12, 13

6A

*6. Identify the sections of a

classified balance sheet.

14, 15, 16,

17, 18, 19

10, 11

3, 4

3, 9, 14, 15,

16, 17

1A, 2A, 3A,

4A, 5A

1B, 2B, 3B,

4B, 5B

*7. Prepare reversing entries.

10, 20, 21

12

18, 19

chapter.

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time Allotted

(min.)

1A

Prepare worksheet, financial statements, and adjusting

and closing entries.

Simple

40–50

2A

Complete worksheet; prepare financial statements,

closing entries, and post-closing trial balance.

Moderate

50–60

3A

Prepare financial statements, closing entries, and post-

closing trial balance.

Moderate

40–50

4A

Complete worksheet; prepare classified balance sheet,

entries, and post-closing trial balance.

Moderate

50–60

5A

Complete all steps in accounting cycle.

Complex

70–90

6A

Analyze errors and prepare correcting entries and trial

balance.

Moderate

40–50

1B

Prepare worksheet, financial statements, and adjusting

and closing entries.

Simple

40–50

2B

Complete worksheet; prepare financial statements,

closing entries, and post-closing trial balance.

Moderate

50–60

3B

Prepare financial statements, closing entries, and post-

closing trial balance.

Moderate

40–50

4B

Complete worksheet; prepare classified balance sheet,

entries, and post-closing trial balance.

Moderate

50–60

5B

Complete all steps in accounting cycle.

Complex

70–90

Comprehensive Problem: Chapters 2 to 4

WEYGANDT FINANCIAL ACCOUNTING 9E

CHAPTER 4

COMPLETING THE ACCOUNTING CYCLE

Number

LO

BT

Difficulty

Time (min.)

BE1

1

K

Simple

2–4

BE2

1

AN

Moderate

6–8

BE3

1

C

Simple

3–5

BE4

2

AP

Simple

3–5

BE5

2

AP

Simple

4–6

BE6

2

AP

Simple

6–8

BE7

3

C

Simple

2–4

BE8

4

K

Simple

3–5

BE9

5

AN

Moderate

4–6

BE10

6

AP

Simple

4–6

BE11

6

C

Simple

3–5

BE12

7

AN

Moderate

4–6

DI1

1

C

Simple

4–6

DI2

2

AP

Simple

2–4

DI3

6

AP

Simple

6–8

DI4

6

C

Simple

4–6

EX1

1

AP

Simple

12–15

EX2

1

AP

Simple

10–12

EX3

1, 6

AP

Simple

12–15

EX4

2, 3

AP

Simple

12–15

EX5

1

AN

Simple

10–12

EX6

1

AN

Moderate

12–15

EX7

2, 3

AP

Simple

8–10

EX8

2, 3

AP

Simple

10–12

EX9

6

AP

Simple

12–15

EX10

4

C

Simple

3–5

EX11

2

AP

Simple

6–8

EX12

5

AN

Moderate

8–10

EX13

5

AN

Moderate

4–6

EX14

6

AP

Moderate

10–12

EX15

6

C

Simple

5–8

EX16

6

AP

Simple

8–10

COMPLETING THE ACCOUNTING CYCLE (Continued)

Number

LO

BT

Difficulty

Time (min.)

EX17

6

AP

Simple

12–15

EX18

7

AN

Moderate

5–7

EX19

2, 4, 7

AN

Moderate

10–12

P1A

1-3, 6

AN

Simple

40–50

P2A

1-3, 6

AP

Moderate

50–60

P3A

1-3, 6

AP

Moderate

40–50

P4A

1-3, 6

AN

Moderate

50–60

P5A

1-4, 6

AN

Complex

70–90

P6A

5

AN

Moderate

40–50

P1B

1-3, 6

AN

Simple

40–50

P2B

1-3, 6

AP

Moderate

50–60

P3B

1-3, 6

AP

Moderate

40–50

P4B

1-3, 6

AN

Moderate

50–60

P5B

1-4, 6

AN

Complex

70–90

BYP1

6

AN

Simple

10–12

BYP2

6

AN

Simple

8–10

BYP3

6

AN

Simple

8–10

BYP4

—

E

Simple

10–12

BYP5

6

AN

Moderate

15–20

BYP6

4

C

Simple

15–20

BYP7

—

E

Moderate

10–15

BYP8

6

AP

Moderate

12–16

BYP9

—

AP

Moderate

10–15

BLOOM’S TAXONOMY TABLE

Copyright © 2014 John Wiley & Sons, Inc. Weygandt, Financial Accounting, 9/e, Solutions Manual (For Instructor Use Only) 4-5

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

*1. Prepare a worksheet.

BE4-1

Q4-1

Q4-2

Q4-3

Q4-4

Q4-5

BE4-3

DI4-1

E4-1

E4-2

E4-3

P4-2A

P4–3A

P4–2B

P4–3B

BE4-2

E4-5

E4-6

P4–1A

P4–4A

P4–5A

P4–1B

P4–4B

P4–5B

*2. Explain the process of closing

the books.

Q4-6

Q4–11

Q4-7

BE4-4

BE4-5

BE4-6

DI4-2

E4-4

E4-7

E4-8

E4–11

P4–2A

P4–3A

P4–2B

P4–3B

E4–19

P4–1A

P4–4A

P4–5A

P4–1B

P4–4B

P4–5B

*3. Describe the content and

purpose of a post-closing trial

balance.

Q4-8

Q4-9

BE4-7

E4-4

E4-7

E4-8

P4–2A

P4–3A

P4–2B

P4–3B

P4–1A

P4–4A

P4–5A

P4–1B

P4–4B

P4–5B

*4. State the required steps in

the accounting cycle.

Q4–11

Q4–12

BE4-8

Q4–10

E4–10

E4–19

P4-5A

P4–5B

*5. Explain the approaches to

preparing correcting entries.

Q4–13

BE4-9

E4–12

E4–13

P4–6A

*6. Identify the sections of

a classified balance sheet.

Q4–14

Q4–15

Q4–16

Q4–17

Q4–18

BE4-11

DI4-4

E4–15

Q4–19

BE4-10

DI4-3

E4-3

E4-9

E4–14

E4-16

E4–17

P4–2A

P4–3A

P4–2B

P4–3B

P4–1A

P4–4A

P4–5A

P4–1B

P4–4B

P4–5B

*7. Prepare reversing entries.

Q4–10

Q4–20

Q4–21

BE4-12

E4–18

E4–19

Broadening Your Perspective

Communication

All About You

FASB Codification

Financial Reporting

Comparative

Analysis

Decision Making

Across the

Organization

Real-World

Focus

Ethics Case

ANSWERS TO QUESTIONS

1. No. A worksheet is not a permanent accounting record. The use of a worksheet is an optional

step in the accounting cycle.

2. The worksheet is merely a device used to make it easier to prepare adjusting entries and the

financial statements.

3. The amount shown in the adjusted trial balance column for an account equals the account

4. The net income of $12,000 will appear in the income statement debit column and the balance

balance sheet debit column.

5. Formal financial statements are needed because the columnar data are not properly arranged

6. (1) (Dr) Individual revenue accounts and (Cr) Income Summary.

(4) (Dr) Retained Earnings and (Cr) Dividends.

7. Income Summary is a temporary account that is used in the closing process. The account is

8. The post-closing trial balance contains only balance sheet accounts. Its purpose is to prove the

period.

9. The accounts that will not appear in the post-closing trial balance are Depreciation Expense;

Dividends; and Service Revenue.

10. A reversing entry is the exact opposite, both in amount and in account titles, of an adjusting entry

11. The steps that involve journalizing are: (1) journalize the transactions, (2) journalize the adjusting

entries, and (3) journalize the closing entries.

12. The three trial balances are the: (1) trial balance, (2) adjusted trial balance, and (3) post-closing

trial balance.

Questions Chapter 4 (Continued)

*14. The standard classifications in a balance sheet are:

Assets

Liabilities and Stockholders’ Equity

Current Assets

Current Liabilities

Long-term Investments

Long-term Liabilities

Property, Plant, and Equipment

Stockholders’ Equity

Intangible Assets

*16. Current assets are assets that a company expects to convert to cash or use up in one year. Some

companies use a period longer than one year to classify assets and liabilities as current because they

*17. Long-term investments are generally investments in stocks and bonds of other companies that

*18. (a) The owner’s equity section for a corporation is called stockholders’ equity.

*19.. Apple’s current liabilities at September 24, 2011 and September 25, 2010 were $27,970 million

and $20,722 million respectively. Apple’s current liabilities were significantly lower than its current

assets in both years.

*20. After reversing entries have been made, the balances will be Interest Payable, zero balance;

Interest Expense, a credit balance.

*21. (a) Jan. 10 Salaries and Wages Expense …………………………………………… 8,000

Cash …………………………………………………………………….. 8,000

Because of the January 1 reversing entry that credited Salaries and Wages Expense for

Note that Salaries and Wages Expense will again have a debit balance of $4,500.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 4-1

The steps in using a worksheet are performed in the following sequence:

(1) prepare a trial balance on the worksheet, (2) enter adjustment data,

The solution to BRIEF EXERCISE 4-2 is on page 4-9.

BRIEF EXERCISE 4-3

Income Statement

Balance Sheet

Account

Dr.

Cr.

Dr.

Cr.

Accumulated Depr.–Equipment

X

Depreciation Expense

X

Common Stock

X

Dividends

X

Service Revenue

X

Supplies

X

Accounts Payable

X

BRIEF EXERCISE 4-4

Dec. 31 Service Revenue ……………………………………… 50,000

31 Income Summary …………………………………….. 34,000

31 Income Summary …………………………………….. 16,000

31 Retained Earnings……………………………………. 2,000

BRIEF EXERCISE 4-2

CLAYTON COMPANY

Worksheet

Trial Balance

Adjustments

Adjusted

Trial Balance

Income

Statement

Balance

Sheet

Account Titles

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Dr.

Cr.

Prepaid Insurance

Service Revenue

Salaries and Wages

Expense

Accounts Receivable

Salaries and Wages

Payable

Insurance Expense

3,000

25,000

58,000

(c) 800

(b) 1,100

(a) 1,800

(a) 1,800

(b) 1,100

(c) 800

1,200

25,800

1,100

1,800

59,100

800

25,800

1,800

59,100

1,200

1,100

800

Copyright © 2014 John Wiley & Sons, Inc. Weygandt, Financial Accounting, 9/e, Solutions Manual (For Instructor Use Only) 4-9

BRIEF EXERCISE 4-5

Salaries and Wages

Expense

Income Summary

Service Revenue

Bal. 27,000

(2) 27,000

(2) 34,000

(1) 50,000

(1) 50,000

Bal. 50,000

(3) 16,000

50,000

50,000

Supplies Expense

Retained Earnings

Dividends

Bal. 7,000

(2) 7,000

(4) 2,000

Bal. 30,000

Bal. 2,000

(4) 2,000

(3) 16,000

Bal. 44,000

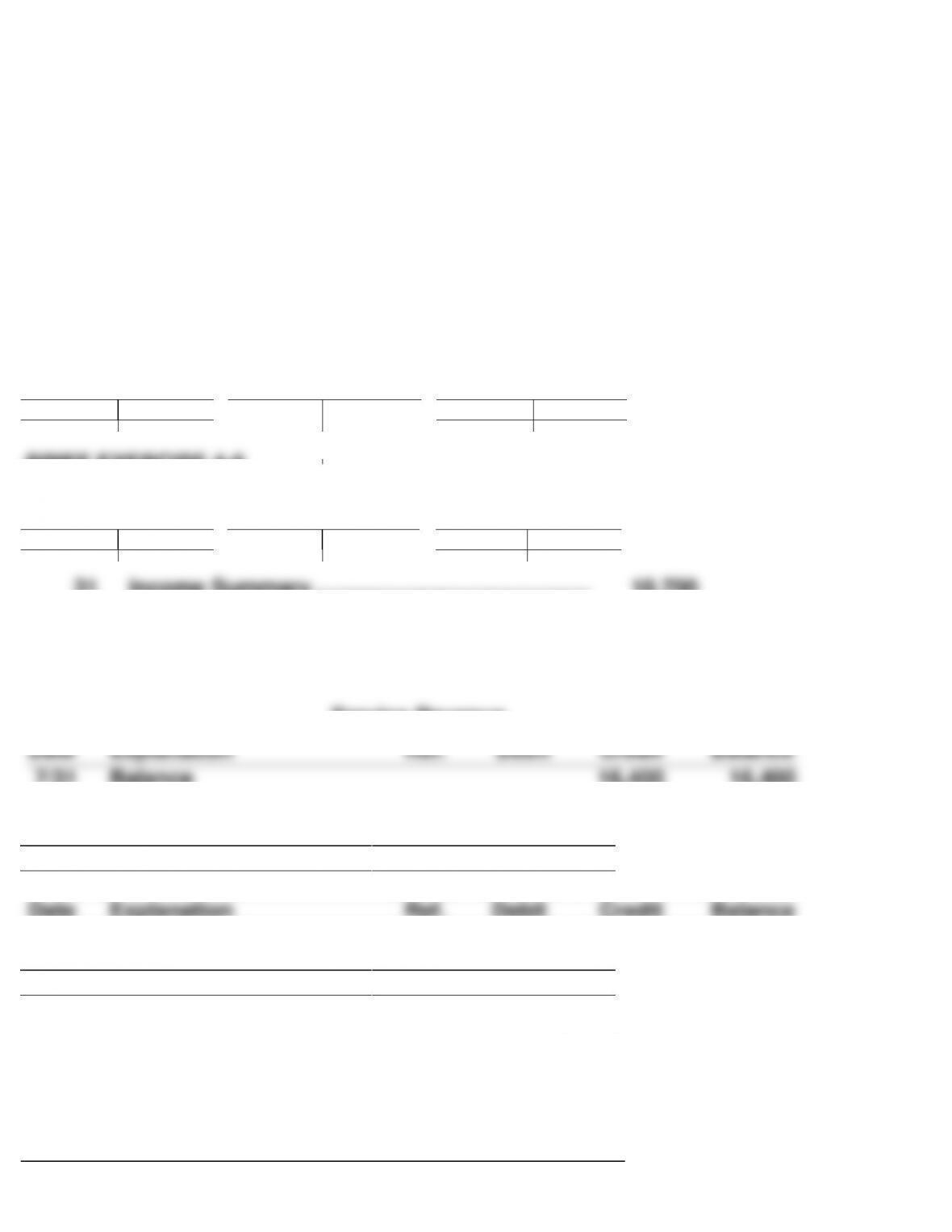

BRIEF EXERCISE 4-6

July 31 Service Revenue ………………………………………. 16,400

31 Income Summary ……………………………………… 10,700

Service Revenue

Date

Explanation

Ref.

Debit

Credit

Balance

7/31

Balance

16,400

16,400

7/31

Closing entry

16,400

0

Salaries and Wages Expense

Date

Explanation

Ref.

Debit

Credit

Balance

7/31

Balance

8,200

8,200

7/31

Closing entry

8,200

0