1

CHAPTER 2

The Recording Process

LEARNING OBJECTIVES

THE RECORDING PROCESS.

2. DEFINE DEBITS AND CREDITS AND EXPLAIN THEIR

USE IN RECORDING BUSINESS TRANSACTIONS.

3. IDENTIFY THE BASIC STEPS IN THE RECORDING

PROCESS.

THE RECORDING PROCESS.

THE RECORDING PROCESS.

RECORDING PROCESS.

7. PREPARE A TRIAL BALANCE AND EXPLAIN ITS

PURPOSES.

CHAPTER REVIEW

The Account

1. (L.O. 1) An account is an individual accounting record of increases and decreases in a specific

asset, liability, or stockholders’ equity item.

2. In its simplest form, an account consists of (a) the title of the account, (b) a left or debit side, and (c) a

form is called a T-account.

Debits and Credits

3. (L.O. 2) The terms debit and credit mean left and right, respectively.

is true, the account has a credit balance.

4. In a double-entry system, equal debits and credits are made in the accounts for each transaction.

5. The effects of debits and credits on assets and liabilities and the normal balances are:

Accounts Debits Credits Normal Balance

Assets Increase Decrease Debit

Liabilities Decrease Increase Credit

6. Accounts are kept for each of the five subdivisions of stockholders’ equity: Common Stock, Retained

Earnings, Dividends, Revenues, and Expenses.

7. The effects of debits and credits on the stockholders’ equity accounts and the normal balances are:

Accounts Debits Credits Normal Balance

Common Stock Decrease Increase Credit

Retained Earnings Decrease Increase Credit

Dividends Increase Decrease Debit

Revenues Decrease Increase Credit

Expenses Increase Decrease Debit

8. The expanded basic equation is:

The Recording Process

9. (L.O. 3) The basic steps in the recording process are:

a. Analyze each transaction for its effect on the accounts.

3

The Journal

11. The journal makes several significant contributions to the recording process:

readily compared.

12. Entering transaction data in the journal is known as journalizing. When three or more accounts are

The Ledger

13. (L.O. 5) The ledger is the entire group of accounts maintained by a company. It keeps in one place

management.

14. The standard form of a ledger account has three columns and the balance in the account is

determined after each transaction.

15. (L.O. 6) Posting is the procedure of transferring journal entries to the ledger accounts. The following

steps are used in posting:

posted.

c. Perform the same steps in a. and b. for the credit amount.

The Chart of Accounts

16. A chart of accounts is a listing of the accounts and the account numbers which identify their location

the income statement accounts.

The Basic Steps

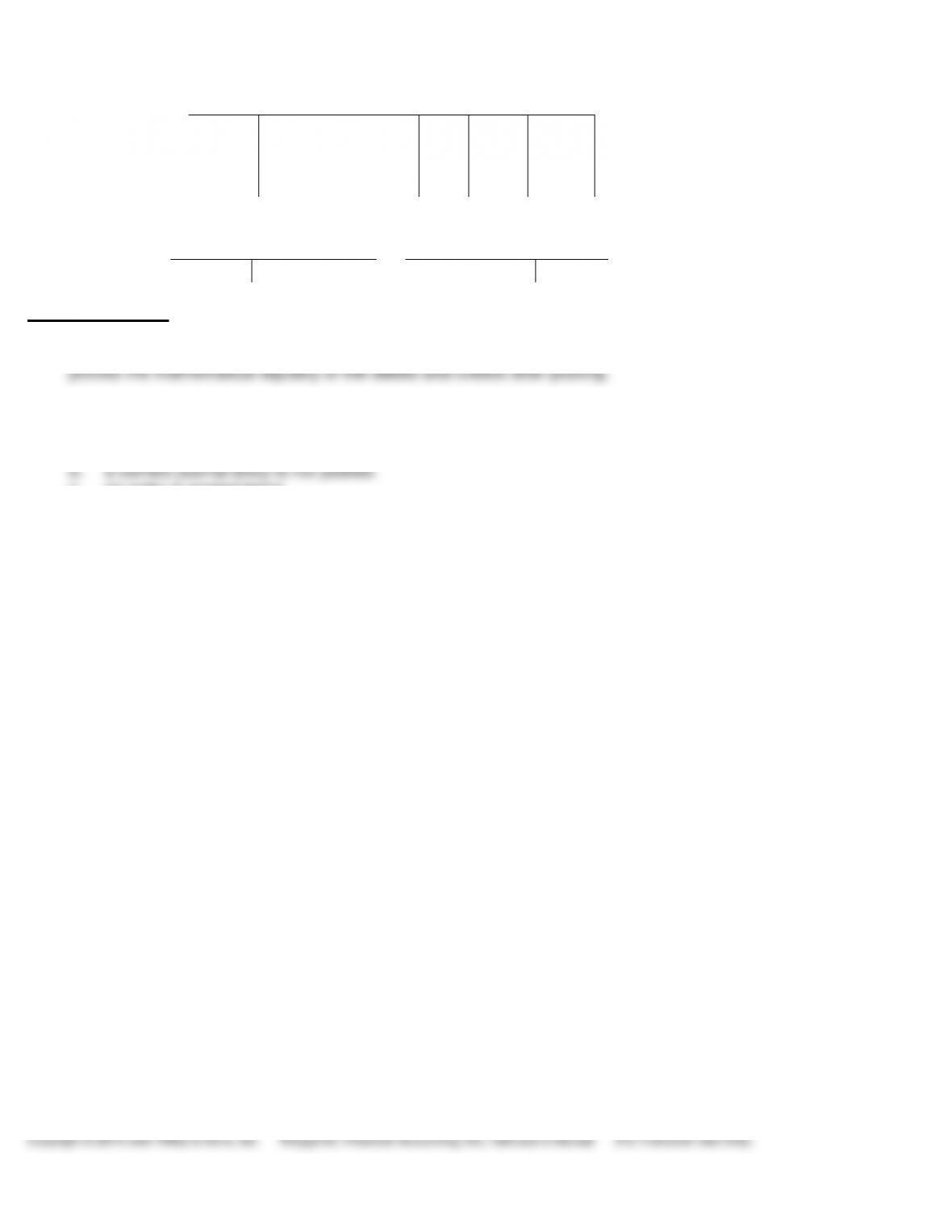

17. The basic steps in the recording process are illustrated as follows:

Transaction On September 4, Fesmire Inc. pays $3,000 cash to a creditor in full payment of the

balance due.

decreased $3,000.

Debit-credit Debits decrease liabilities: debit Accounts Payable $3,000.

analysis Credits decrease assets: credit Cash $3,000.

Journal

entry

Sept. 4

Accounts Payable

Cash

(Paid creditor

in full)

201

101

3,000

3,000

Posting

Cash 1

Accounts Payable 201

Sept. 4 3,000

Sept. 4 3,000

The Trial Balance

18. (L.O. 7) A trial balance is a list of accounts and their balances at a given time. The trial balance

19. A trial balance does not prove that the company has recorded all transactions or that the ledger is

correct because the trial balance may still balance when

a. a transaction is not journalized.

c. an entry is posted twice.

d. incorrect accounts are used in journalizing or posting.

e. offsetting errors are made in recording the amount of a transaction.

5

LECTURE OUTLINE

A. The Account.

asset, liability, or stockholders’ equity item.

An account consists of three parts:

1. A title.

2. A left or debit side.

3. A right or credit side.

B. Debits and Credits.

indicates right.

1. Assets, dividends, and expenses are increased by debits and decreased by

credits.

credits and decreased by debits.

C. Steps in the Recording Process.

D. The General Journal/Journalizing.

Entering transaction data in the general journal is called journalizing.

The general journal:

2. Provides a chronological record of transactions.

3. Helps to prevent or locate errors because the debit and credit amounts for

each entry can be easily compared.

4. A simple journal entry involves only two accounts (one debit and one credit)

whereas a compound journal entry involves three or more accounts.

7

E. The Ledger.

track of changes in these balances.

2. Companies arrange the ledger in the sequence in which they present the

accounts in the financial statements, beginning with the balance sheet

accounts.

F. Posting/Chart of Accounts.

2. Posting involves the following steps:

a. In the ledger, in the appropriate columns of the account(s) debited,

enter the date, journal page, and debit amount shown in the journal.

which the debit amount was posted.

c. In the ledger, in the appropriate columns of the account(s) credited,

enter the date, journal page, and credit amount shown in the journal.

which the credit amount was posted.

3. A chart of accounts lists the accounts and the account numbers that identify

their location in the ledger. Accounts are usually numbered starting with the