Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

PROBLEM 14-2

(a) Earnings per share =

$203,000

57,000

= $3.56.

(b) Return on common stockholders’ equity =

$203,000

$465,400 + $566,700

2

=

$203,000

$516,050

= 39.3%.

(c) Return on assets =

$203,000

$852,800 + $970,200

2

=

$203,000

$911,500

= 22.3%.

(d) Current ratio =

$203,500

$369,900

= 1.82:1

(e) Acid-test ratio =

$236,900

$203,500

= 1.16:1

(f) Accounts receivable turnover =

$1,818,500

($102,800 + $107,800 )

2

=

$1,818,500

$105,300

= 17.3 times.

PROBLEM 14-2 (Continued)

(g) Inventory turnover =

$1,011,500

$115,500 + $133,000

2

=

$1,011,500

$124,250

= 8.1 times.

(h) Times interest earned =

$308,000

$18,000

= 17.1 times.

(i) Asset turnover =

$1,818,500

$911,500*

= 2.0 times.

*($852,800 + $970,200) ÷ 2

(j) Debt to assets =

$970,200

$403,500

= 41.6%.

PROBLEM 14-3

(a)

2015

2016

(1)

Profit margin.

$30,000

$650,000

= 4.6%

$45,000

$700,000

= 6.4%

(2)

Asset turnover.

$650,000

$533,000 + $600,000

2

= 1.1 times

$700,000

$600,000 + $640,000

2

= 1.1 times

(3)

Earnings per share.

$30,000

31,000

= $.97

$45,000

32,000

= $1.41

(4)

Price-earnings ratio.

$5.00

$.97

= 5.2 times

$8.00

$1.41

= 5.7 times

(5)

Payout ratio.

$18,000

$30,000

*

= 60.0%

*($113,000 + $30,000 – $125,000)

$25,000

$45,000

**

= 55.6%

**($125,000 + $45,000 – $145,000)

(6)

Debt to assets.

$165,000

$600,000

= 27.5%

$155,000

$640,000

= 24.2%

PROBLEM 14-3 (Continued)

(b) The underlying profitability of the corporation appears to have improved.

For example, profit margin and earnings per share have both increased.

PROBLEM 14-4

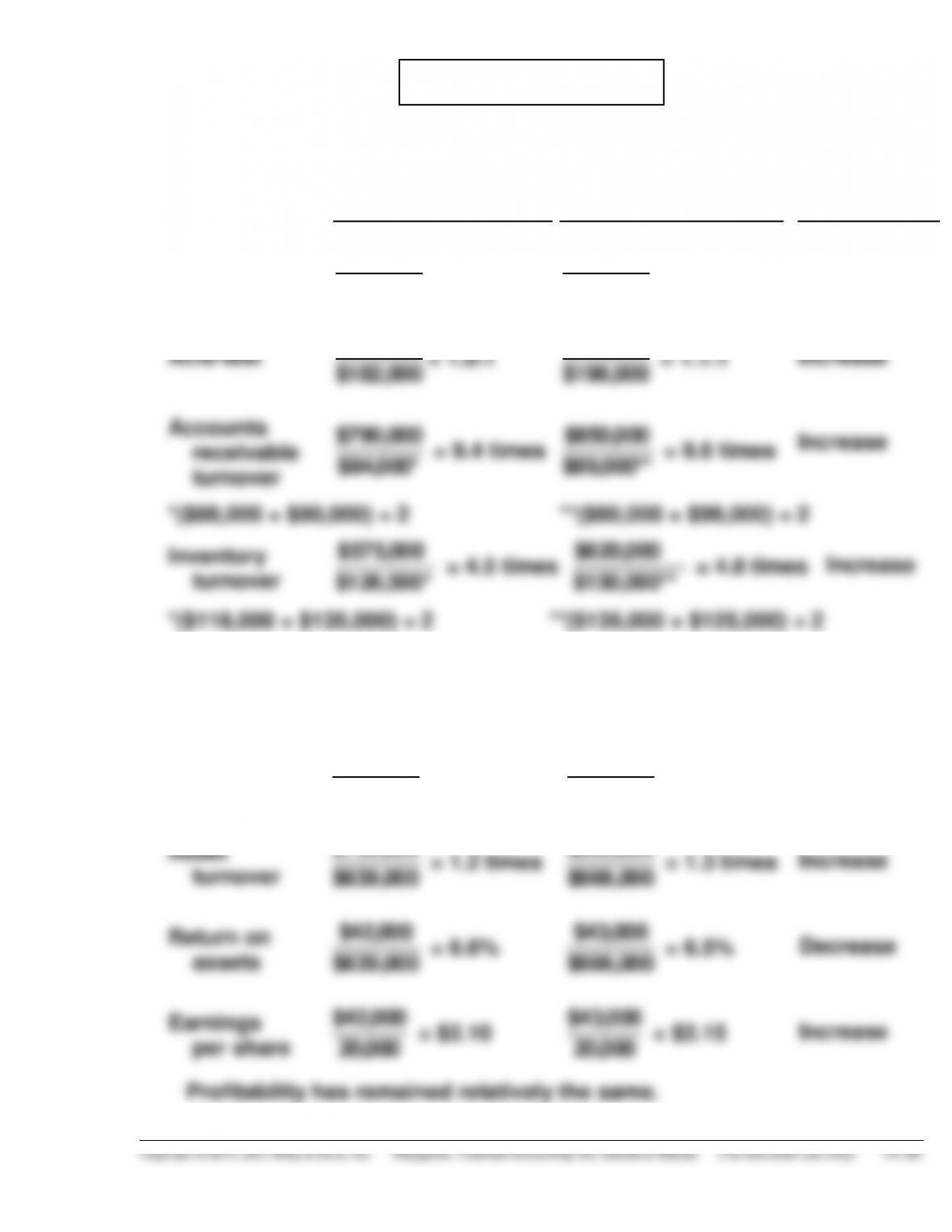

(a) LIQUIDITY

2014

2015

Change

Current

$343,000

$182,000

= 1.9:1

$374,000

$198,000

=1.9:1

No change

Acid-test

$185,000

$182,000

= 1.0:1

$220,000

$198,000

= 1.1:1

Increase

Accounts

receivable

turnover

$790,000

$84,000*

= 9.4 times

$850,000

$89,000**

= 9.6 times

Increase

*($88,000 + $80,000) ÷ 2 **($80,000 + $98,000) ÷ 2

Inventory

turnover

$575,000

$126,500*

= 4.5 times

$620,000

$130,000**

= 4.8 times

Increase

*($118,000 + $135,000) ÷ 2 **($135,000 + $125,000) ÷ 2

An overall increase in short-term liquidity has occurred.

PROFITABILITY

Profit

margin

$42,000

$790,000

= 5.3%

$43,000

$850,000

= 5.1%

Decrease

Asset

turnover

$790,000

$639,000

= 1.2 times

$850,000

$666,000

= 1.3 times

Increase

Return on

assets

$42,000

$639,000

= 6.6%

$43,000

$666,000

= 6.5%

Decrease

Earnings

per share

$42,000

20,000

= $2.10

$43,000

20,000

= $2.15

Increase

PROBLEM 14-4 (Continued)

(b)

2015

2016

Change

1.

Return on

common

stockholders’

equity

$43,000

$326,000 (a)

= 13.2%

$50,000

$451,000 (b)

= 11.1%

Decrease

2.

Debt to assets

$348,000 (c)

$684,000

= 50.9%

$248,000

$700,000

= 35.4%

Decrease

3.

Price-earnings

ratio

$9.00

$2.15

= 4.2 times

$12.80

$2.50 (d)

= 5.1 times

Increase

PROBLEM 14-5

(a)

Ratio

Target

Wal-Mart

(All Dollars Are in Millions)

(1)

(2)

(3)

(4)

(5)

(6)

(7)

(8)

(9)

(10)

(11)

Current

Accounts receivable

turnover

Average collection

period

Inventory turnover

Days in inventory

Profit margin

Asset turnover

Return on assets

Return on common

stockholders’ equity

Debt to assets

Times interest earned

1.6:1 ($18,906 ÷ $11,782)

8.6 ($61,471 ÷ $7,124)

42.4 (365 ÷ 8.6)

6.4 ($41,895 ÷ $6,517)

57.0 (365 ÷ 6.4)

4.6% ($2,849 ÷ $61,471)

1.5 ($61,471 ÷ $40,954.5a)

7.0 % ($2,849 ÷ $40,954.5a)

18.4 % ($2,849 ÷ $15,470b)

65.6% ($29,253 ÷ $44,560)

8.1 ($5,272 ÷ $647)

.8:1 ($47,585 ÷ $58,454)

115.3 ($374,526 ÷ $3,247)

3.2 (365 ÷ 115.3)

8.3 ($286,515 ÷ $34,433)

44.0 (365 ÷ 8.3)

3.4% ($12,731 ÷ $374,526)

2.4 ($374,526 ÷ $157,550.5c)

8.1 % ($12,731 ÷ $157,550.5c)

20.2% ($12,731 ÷ $63,090.5d)

60.5% ($98,906 ÷ $163,514)

11.9 ($21,437 ÷ $1,798)

a($44,560 + $37,349) ÷ 2 c($163,514 + $151,587) ÷ 2

b($15,307 + $15,633) ÷ 2 d($64,608 + $61,573) ÷ 2

(b) The comparison of the two companies shows the following:

Liquidity—Target’s current ratio of 1.6:1 is significantly better than

Wal-Mart’s .8:1. However, Wal-Mart has a better inventory turnover ratio

PROBLEM 14-6

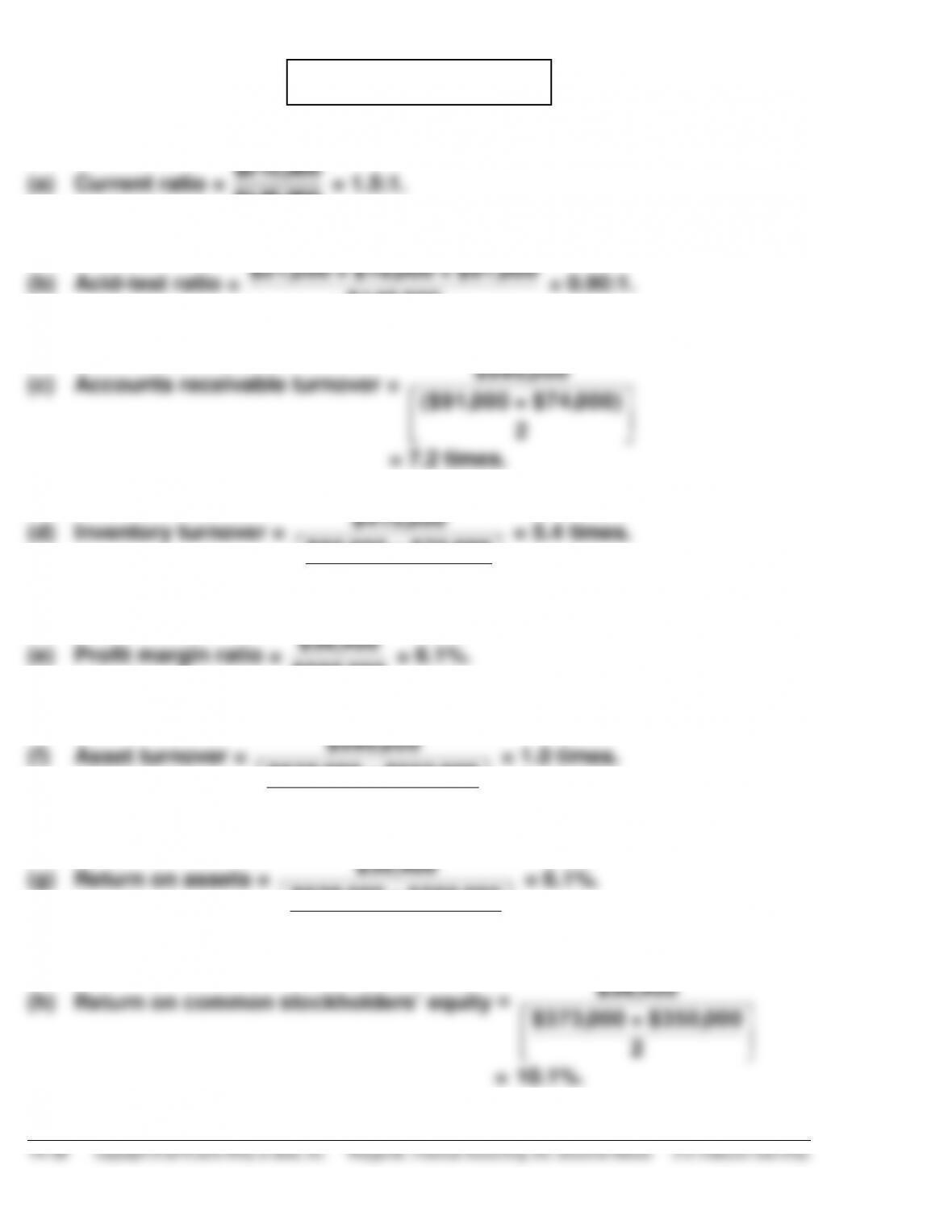

(a) Current ratio =

$215,000

$145,000

= 1.5:1.

(b) Acid-test ratio =

$21,000 + $18,000 + $91,000

$145,000

= 0.90:1.

(c) Accounts receivable turnover =

$595,000

($91,000 + $74,000)

2

= 7.2 times.

(d) Inventory turnover =

$415,000

$85,000 + $70,000

2

= 5.4 times.

(e) Profit margin ratio =

$36,400

$595,000

= 6.1%.

(f) Asset turnover =

$595,000

$638,000 + $560,000

2

= 1.0 times.

(g) Return on assets =

$36,400

$638,000 + $560,000

2

= 6.1%.

(h) Return on common stockholders’ equity =

$36,400

$373,000 + $350,000

2

= 10.1%.

PROBLEM 14-6 (Continued)

(i) Earnings per share =

$36,400

30,000 (1)

= $1.21.

$1.21

(k) Payout ratio =

$13,400 (2)

$36,400

= 36.8%.

(2) $200,000 + $36,400 – $223,000

(l) Debt to assets =

$265,000

$638,000

= 41.5%.

(m) Times interest earned =

$59,200 (3)

$7,800

= 7.6 times.

(3) $36,400 + $15,000 + $7,800

PROBLEM 14-7

Accounts receivable turnover = 10 =

$11,000,000

Average accounts receivable

Averages accounts receivable =

$11,000,000

10

= $1,100,000

Net accounts receivables 12/31/15 + $950,000

2

= $1,100,000

Net accounts receivable 12/31/15 + $950,000 = $2,200,000

Net accounts receivable 12/31/15 = $1,250,000

Profit margin = 14.5% = .145 =

Net income

$11,000,000

Net income = $11,000,000 X .145 = $1,595,000

Income before income taxes = $1,595,000 + $560,000 = $2,155,000

Return on assets = 22% = .22 =

$1,595,000

Average assets