Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

EXERCISE 14-2

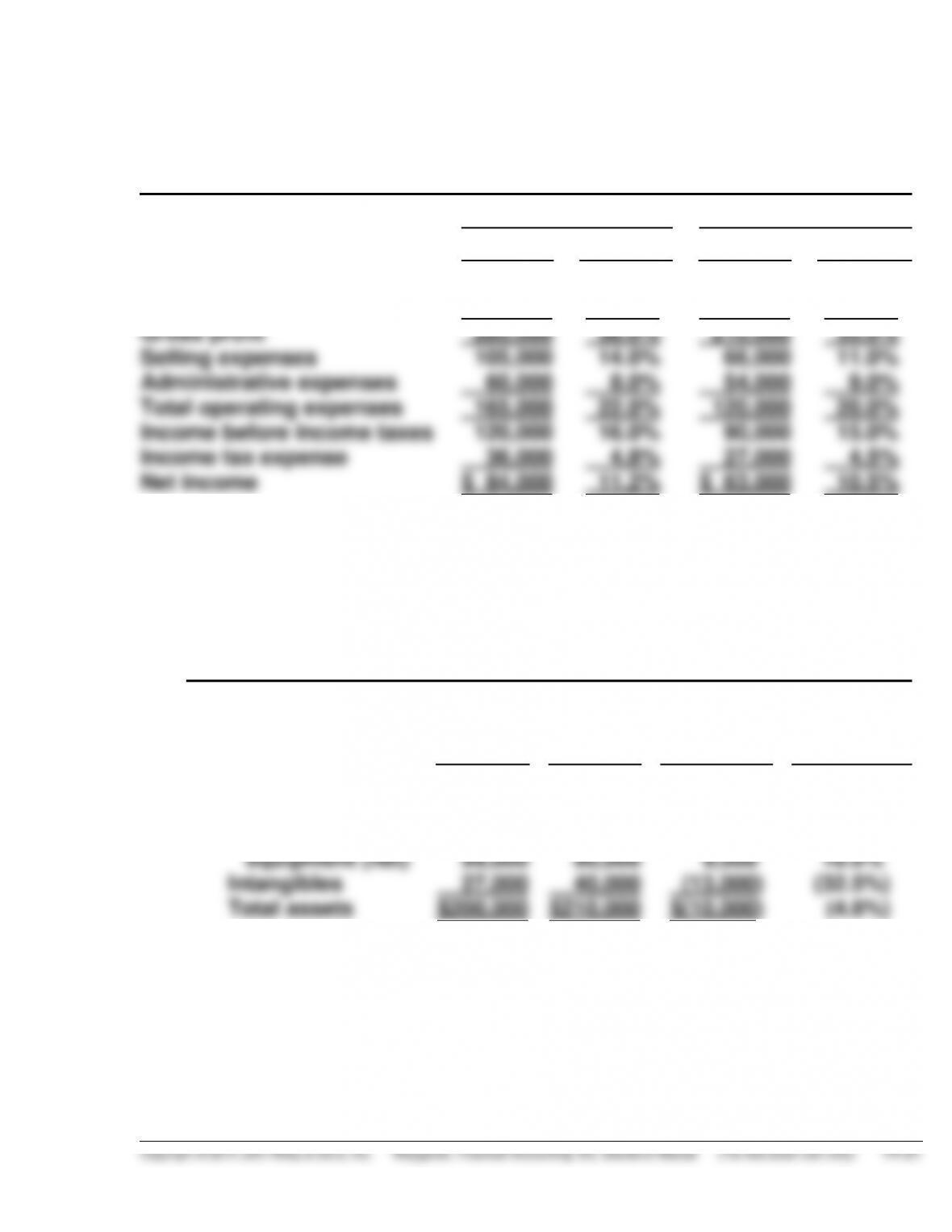

NAVARRO CORPORATION

Condensed Income Statements

For the Years Ended December 31

2015

2014

Amount

Percent

Amount

Percent

Net sales

Cost of goods sold

Gross profit

Selling expenses

Administrative expenses

Total operating expenses

Income before income taxes

Income tax expense

Net income

$750,000

465,000

285,000

105,000

60,000

165,000

120,000

36,000

$ 84,000

100.0%

62.0%

38.0%

14.0%

8.0%

22.0%

16.0%

4.8%

11.2%

$600,000

390,000

210,000

66,000

54,000

120,000

90,000

27,000

$ 63,000

100.0%

65.0%

35.0%

11.0%

9.0%

20.0%

15.0%

4.5%

10.5%

EXERCISE 14-3

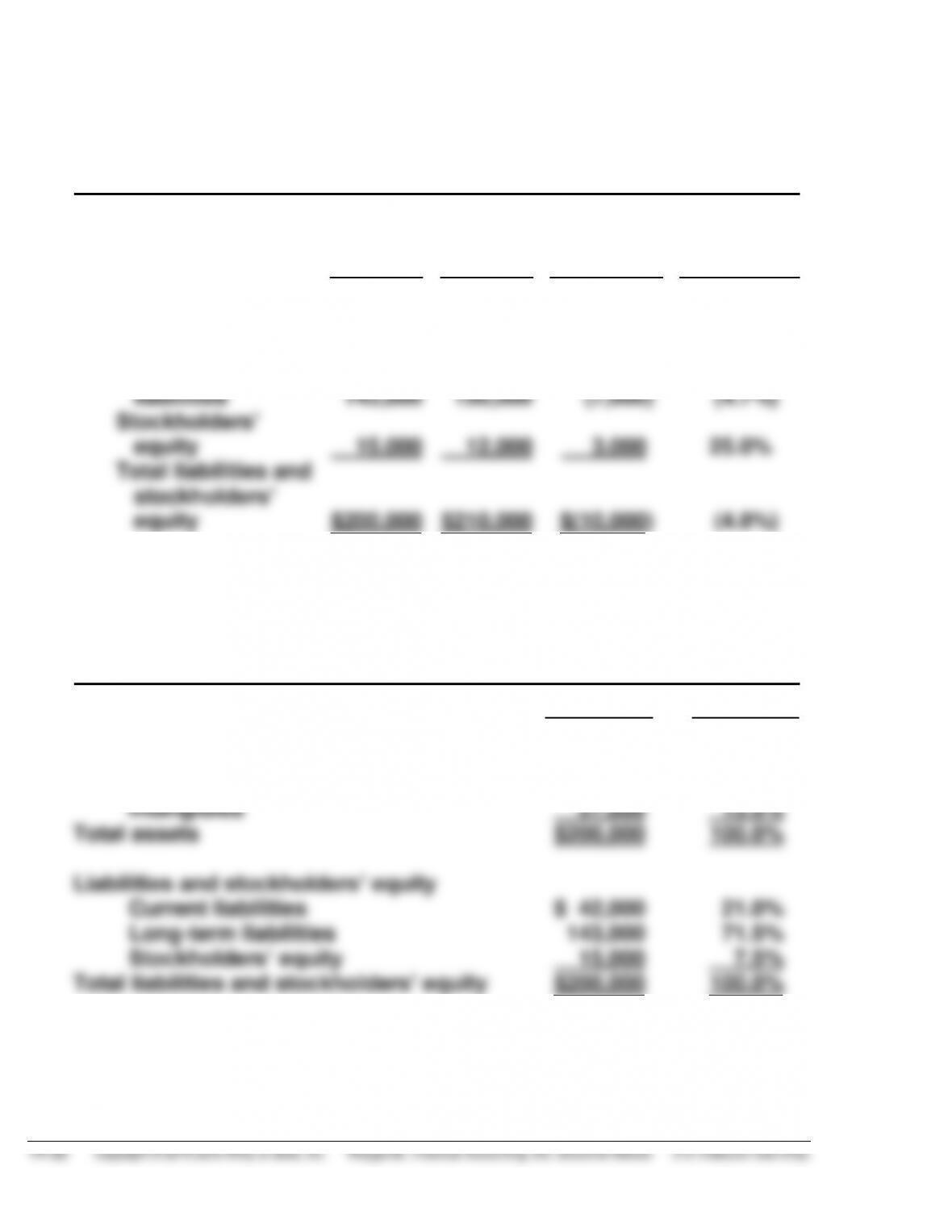

(a) GURLEY CORPORATION

Condensed Balance Sheets

December 31

2015

2014

Increase

(Decrease)

Percentage

Change

from 2014

Assets

Current assets

Property, plant &

equipment (net)

Intangibles

Total assets

$ 74,000

99,000

27,000

$200,000

$ 80,000

90,000

40,000

$210,000

$ (6,000)

( 9,000)

(13,000)

$(10,000)

(7.5%)

(10.0%)

(32.5%)

(4.8%)

EXERCISE 14-3 (Continued)

GURLEY CORPORATION

Condensed Balance Sheets (Continued)

December 31

2015

2014

Increase

(Decrease)

Percentage

Change

from 2015

Liabilities and stock-

holders’ equity

Current liabilities

Long-term

liabilities

Stockholders’

equity

Total liabilities and

stockholders’

equity

$ 42,000

143,000

15,000

$200,000

$ 48,000

150,000

12,000

$210,000

$ (6,000)

(7,000)

3,000)

$(10,000)

(12.5%)

(4.7%)

(25.0%)

(4.8%)

(b) GURLEY CORPORATION

Condensed Balance Sheet

December 31, 2015

Amount

Percent

Assets

Current assets

Property, plant, and equipment (net)

Intangibles

Total assets

Liabilities and stockholders’ equity

Current liabilities

Long-term liabilities

Stockholders’ equity

Total liabilities and stockholders’ equity

$ 74,000

99,000

27,000

$200,000

$ 42,000

143,000

15,000

$200,000

37.0%

49.5%

13.5%

100.0%

21.0%

71.5%

7.5%

100.0%

EXERCISE 14-4

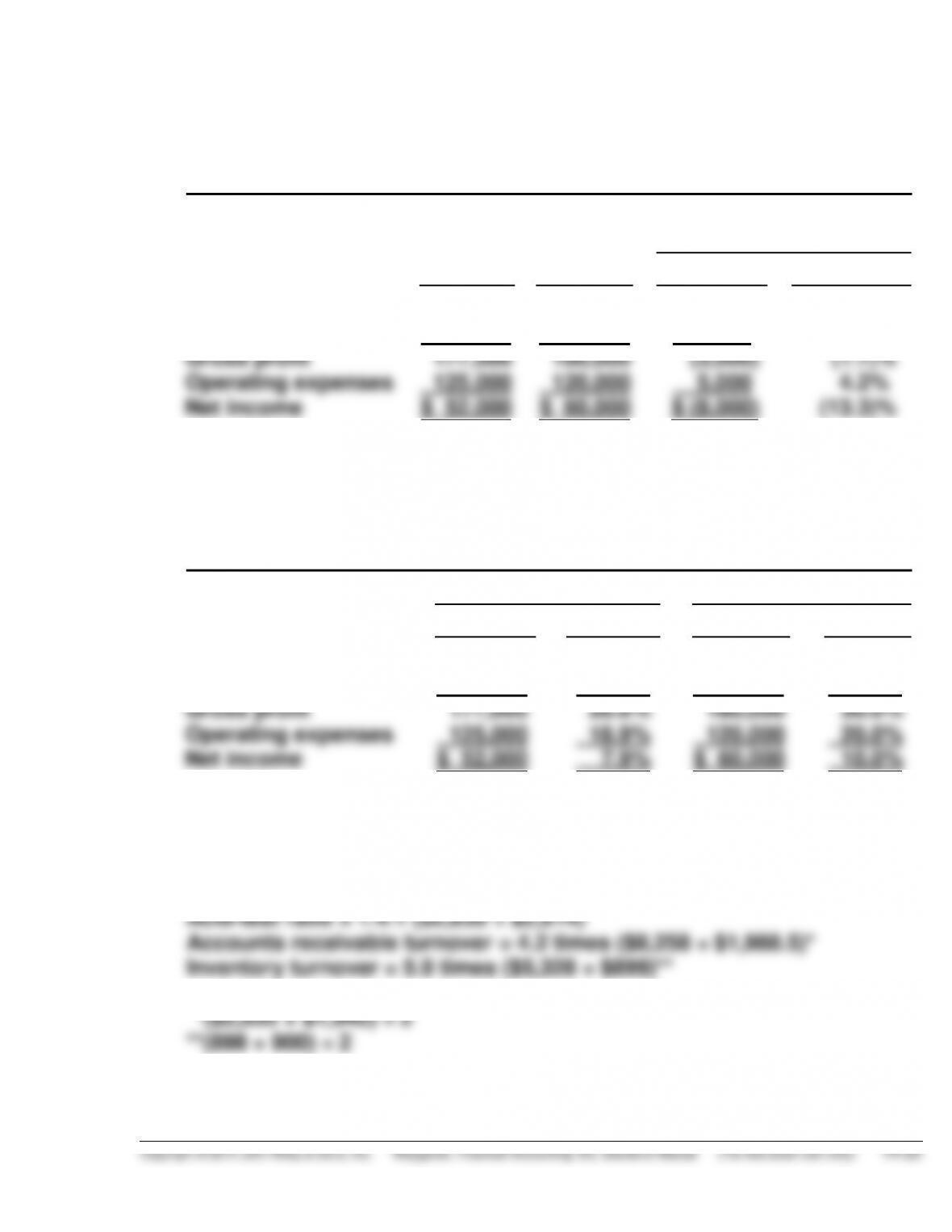

(a) EMLEY CORPORATION

Condensed Income Statements

For the Years Ended December 31

Increase or (Decrease)

During 2015

2016

2015

Amount

Percentage

Net sales

Cost of goods sold

Gross profit

Operating expenses

Net income

$660,000

483,000

177,000

125,000

$ 52,000

$600,000

420,000

180,000

120,000

$ 60,000

$60,000

63,000

(3,000)

5,000

$ (8,000)

10.0%

15.0%

(1.7)%

4.2%

(13.3)%

(b) EMLEY CORPORATION

Condensed Income Statements

For the Years Ended December 31

2015

2014

Amount

Percent

Amount

Percent

Net sales

Cost of goods sold

Gross profit

Operating expenses

Net income

$660,000

483,000

177,000

125,000

$ 52,000

100.0%

73.2%

26.8%

18.9%

7.9%

$600,000

420,000

180,000

120,000

$ 60,000

100.0%

70.0%

30.0%

20.0%

10.0%

EXERCISE 14-5

(a) Current ratio = 2.0:1 ($4,054 ÷ $2,014)

EXERCISE 14-5 (Continued)

(b)

Ratio

Nordstrom

Macy’s

Industry

Current

Acid-test

Accounts Receivable

Turnover

Inventory turnover

2.0:1

1.4:1

4.2

5.9

1.40:1

0.51:1

74.8

3.2

1.70:1

.70:1

46.4

4.3

Nordstrom is better than Macy’s for the current ratio and its acid-test

EXERCISE 14-6

Feb. 3 2.2:1 No change in total current assets or liabilities.

7 1.6:1 ($82,000 ÷ $50,000).

Feb. 3 1.9:1 No change in total quick assets or current liabilities.

7 1.3:1 ($65,000 ÷ $50,000).

EXERCISE 14-7

(a)

$145,000

$50,000

= 2.9:1.

(b)

$85,000

$50,000

= 1.7:1.

(c)

$390,000

$65,000 (1)

= 6.0 times.

(d)

$198,000

$55,000 (2)

= 3.6 times.

(1)

$70,000 + $60,000

2

(2)

$60,000 + $50,000

2

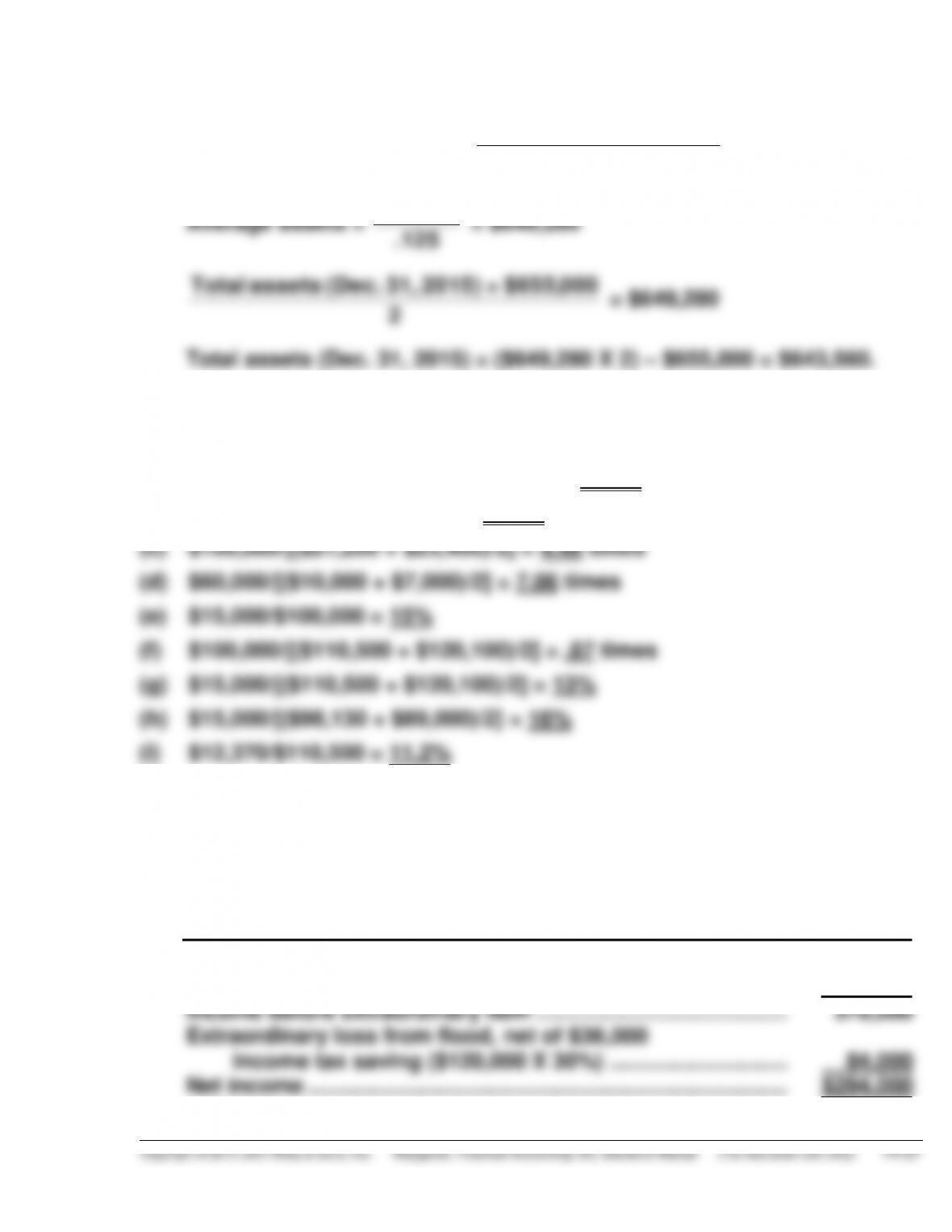

EXERCISE 14-8

$45,000

$750,000

(b) Asset turnover

$750,000

$500,000 + $580,000

2

= 1.4 times.

(c) Return on assets

$45,000

$540,000

= 8.3%.

(d)

Return on common stockholders’

equity

$45,000

$325,000 + $430,000

2

= 11.9%.

EXERCISE 14-9

(a)

$65,000 –$5,000

30,000 shares

= $2.00.

(b)

$13.00

$2.00

= 6.5 times.

(c)

$21,000

$65,000

= 32%.

(d)

$65,000 + $16,000 + $24,000

$16,000

=

$105,000

$16,000

= 6.6 times.

EXERCISE 14-10

Cost of goods sold

EXERCISE 14-10 (Continued)

(d) Return on assets = 12.5% =

$81,160 [see (c) above]

Average assets

$81,160

EXERCISE 14-11

(a) ($4,300 + $21,200+ $10,000)/$12,370 = 2.87:1

(b) ($4,300 + $21,200)/$12,370 = 2.06:1

EXERCISE 14-12

(a) HAAS CORPORATION

Partial Income Statement

For the Year Ended October 31, 2015

Income before income taxes .................................................. $540,000

Income tax expense ($540,000 X 30%) .................................. 162,000

EXERCISE 14-12 (Continued)

(b) To: Chief Accountant

From: Your name, Independent Auditor

After reviewing your income statement for the year ended 10/31/15, we

believe it is misleading for the following reasons:

the extraordinary loss.

EXERCISE 14-13

(a) TRAYER CORPORATION

Partial Income Statement

For the Year Ended December 31, 2015

Income from continuing operations ...................................... $290,000

Discontinued operations

Gain on discontinued division, net of $9,000

(b) The correction of an error in last year’s financial statements is a prior period

SOLUTIONS TO PROBLEMS

PROBLEM 14-1

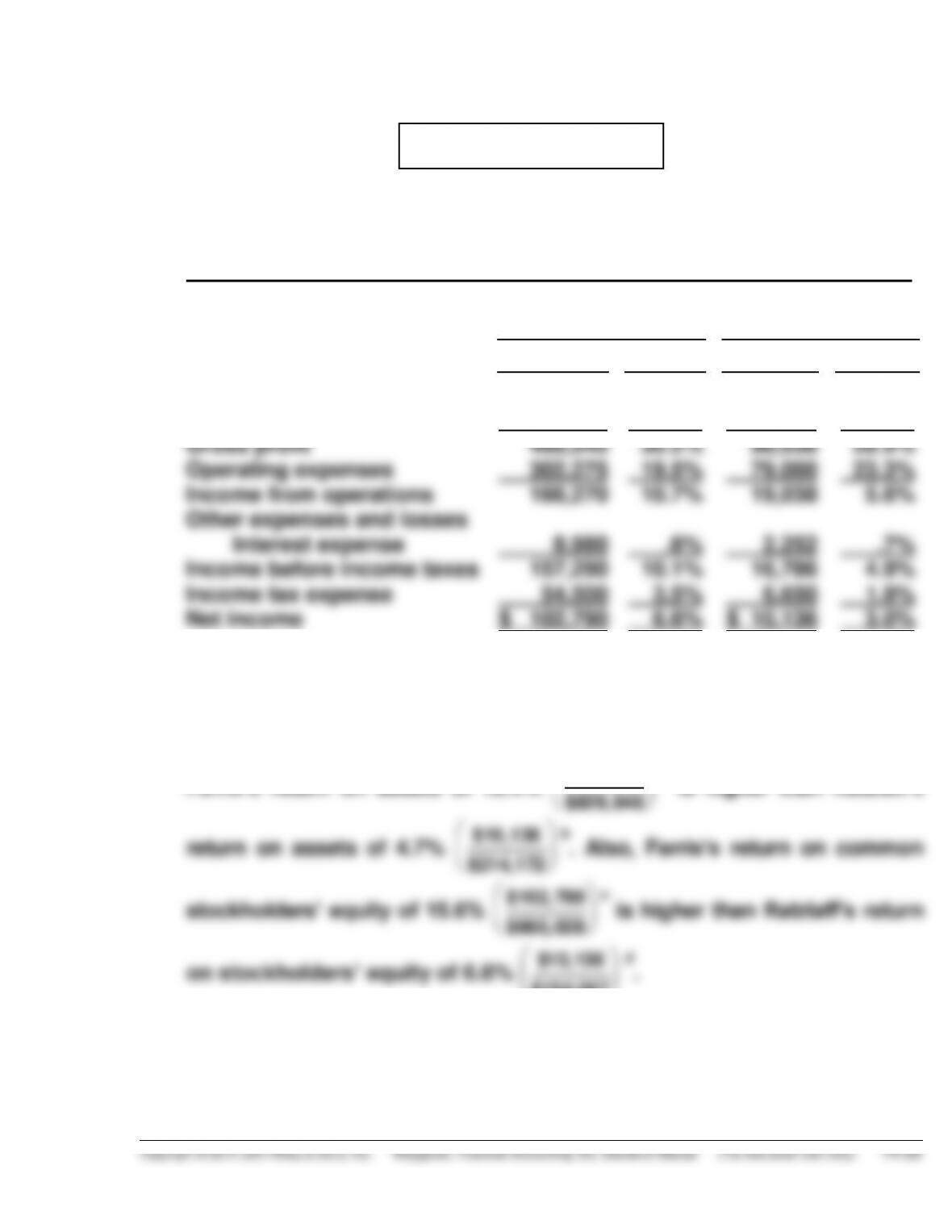

(a) Condensed Income Statement

For the Year Ended December 31, 2015

Farris Company

Ratzlaff

Company

Dollars

Percent

Dollars

Percent

Net sales

Cost of goods sold

Gross profit

Operating expenses

Income from operations

Other expenses and losses

Interest expense

Income before income taxes

Income tax expense

Net income

$1,549,035

1,080,490

468,545

302,275

166,270

8,980

157,290

54,500

$ 102,790

100.0%

69.8%

30.2%

19.5%

10.7%

.6%

10.1%

3.5%

6.6%

$339,038

241,000

98,038

79,000

19,038

2,252

16,786

6,650

$ 10,136

100.0%

71.1%

28.9%

23.3%

5.6%

.7%

4.9%

1.9%

3.0%

(b) Farris Company appears to be more profitable. It has higher relative

gross profit, income from operations, income before taxes, and net income.

Farris’s return on assets of 12.4%

$102, 790

$829, 848

a is higher than Ratzlaff’s

return on assets of 4.7%

$10,136

$214,172

b. Also, Farris’s return on common

stockholders’ equity of 15.6%

$102, 790

$660, 028

c is higher than Ratzlaff’s return

on stockholders’ equity of 6.6%

$10,136

$154,047

d.

PROBLEM 14-1 (Continued)

2015

2014

Current assets

Plant assets

Total assets

$325,975

521,310

$847,285

+

$312,410

500,000

$812,410

=

2

$1,659,695

b$10,136 is Ratzlaff’s 2015 net income. $214,172 is Ratzlaff’s 2015 average

assets:

2015

2014

Current assets

Plant assets

Total assets

$ 83,336

139,728

$223,064

+

$ 79,467

125,812

$205,279

=

2

$428,343

c$102,790 is Farris’s 2015 net income. $660,028 is Farris’s 2015

average stockholders’ equity:

2015

2014

Common stock

Retained earnings

Stockholders’ equity

$500,000

173,460

$673,460

+

$500,000

146,595

$646,595

=

$1, 320, 055

2

d$10,136 is Ratzlaff’s 2015 net income. $154,047 is Ratzlaff’s 2015

average stockholders’ equity:

2015

2014

Common stock

Retained earnings

Stockholders’ equity

$120,000

38,096

$158,096

+

$120,000

29,998

$149,998

=

2

$308,094