BRIEF EXERCISE 14-2

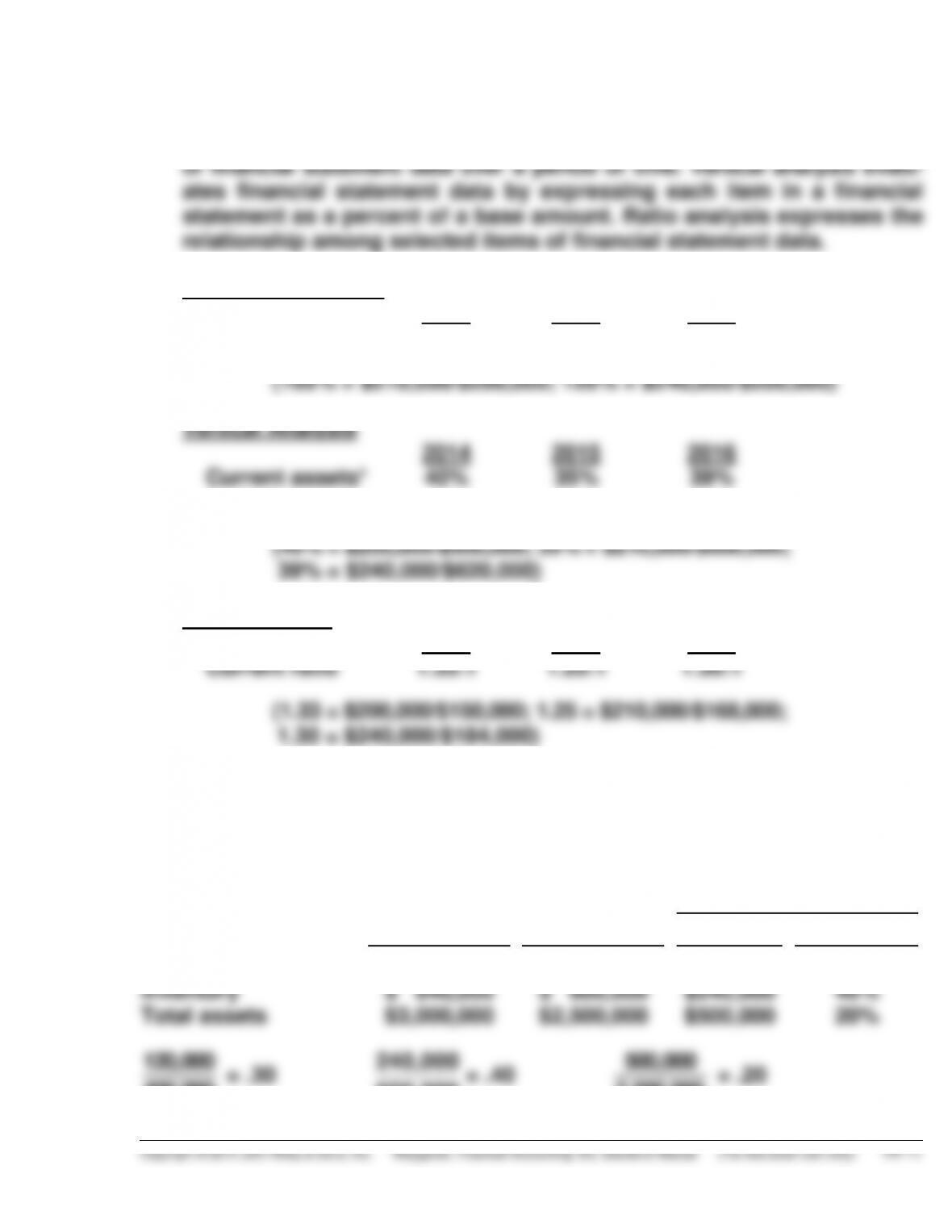

(a) The three tools of financial statement analysis are horizontal analysis,

vertical analysis, and ratio analysis. Horizontal analysis evaluates a series

(b) Horizontal Analysis

2014

2015

2016

Current assets

100%

105%

120%

2014

2015

2016

Current assets*

40%

35%

39%

*as a percentage of total assets

Ratio Analysis

2014

2015

2016

Current ratio

1.33:1

1.25:1

1.30:1

(1.33 = $200,000/$150,000; 1.25 = $210,000/$168,000;

1.30 = $240,000/$184,000)

BRIEF EXERCISE 14-3

Horizontal analysis:

Increase

or (Decrease)

Dec. 31, 2015

Dec. 31, 2014

Amount

Percentage

Accounts receivable

Inventory

Total assets

$ 520,000

$ 840,000

$3,000,000

$ 400,000

$ 600,000

$2,500,000

$120,000

$240,000

$500,000

30%

40%

20%

120,000

400,000

= .30

600,000

240,000

= .40

500,000

2,500,000

= .20

BRIEF EXERCISE 14-4

Vertical analysis:

Dec. 31, 2015

Dec. 31, 2014

Amount

Percentage*

Amount

Percentage**

Accounts receivable

Inventory

Total assets

$ 520,000

$ 840,000

$3,000,000

17.3%

28.0%

100%

$ 400,000

$ 600,000

$2,500,000

16.0%

24.0%

100%

*520,000

3,000,000

= .173

** 400,000

2,500,000

= .16

* 840,000

3, 000,000

= .28

** 600,000

2,500,000

= .24

BRIEF EXERCISE 14-5

2016

2015

2014

Net income

$522,000

$450,000

$500,000

Increase or (Decrease)

Amount

Percentage

(a)

(b)

2014–2015

2015–2016

(50,000)

(72,000)

(10%)

(16%)

50,000

500,000

= .10

72,000

450,000

= .16

BRIEF EXERCISE 14-6

2015

2014

Increase

Net income

$585,000

X

20%

X .20 =

585,000 – X

X

.20X = 585,000 – X

BRIEF EXERCISE 14-6 (Continued)

1.20X = 585,000

BRIEF EXERCISE 14-7

Comparing the percentages presented results in the following conclusions:

The net income for Dody increased in 2015 because of the combination of

BRIEF EXERCISE 14-8

2016

2015

2014

Sales

Cost of goods sold

Expenses

Net income

100.0

60.2

25.0

14.8

100.0

62.4

25.6

12.0

100.0

63.5

27.5

9.0

Net income as a percent of sales for Kochheim increased over the three-

BRIEF EXERCISE 14-9

(a) Working capital = Current assets – Current liabilities

BRIEF EXERCISE 14-9 (Continued)

(b) Current ratio:

Current assets

Current liabilities

=

$45,918,000

$40,644,000

= 1.13:1

(c) Acid-test ratio:

Cash+ Short–term investments

+ Receivables (net)

Current liabilities

=

$8,041,000 + $4,947,000 + $12,545,000

$40,644,000

=

$25,533,000

$40,644,000

= .63:1

BRIEF EXERCISE 14–10

(a) Asset turnover =

Net sales

Average assets

=

$95,000,000

$14,000,000 + $18,000,000

2

= 5.9 times

(b) Profit margin =

Net income

Net sales

=

$11,440,000

$95,000,000

= 12.0%

BRIEF EXERCISE 14–11

(a) Accounts Receivable turnover =

Net credit sales

Average net accounts receivable

2016

2015

(1)

$3,960,000

$535,000*

= 7.4 times

$3,100,000

$500,000**

= 6.2 times

*($520,000 + $550,000) ÷ 2

**($480,000 + $520,000) ÷ 2

(2)

Average collection period

365

7.4

= 49.3 days

365

6.2

= 58.9 days

(b) Rainsberger Company should be pleased with the effectiveness of its

BRIEF EXERCISE 14–12

(a) Inventory turnover =

inventory Average

sold goods ofCost

(1)

2016

2015

$4,260,000

$940,000 + $1,020,000

2

= 4.3 times

$4,581,000

$860,000 + $940,000

2

= 5.1 times

Beginning inventory $ 940,000

Purchases 4,340,000

Goods available for sale 5,280,000

Ending inventory 1,020,000

Cost of goods sold $4,260,000

$ 860,000

4,661,000

5,521,000

940,000

$4,581,000

(2) Days in inventory

365

4.3

= 84.9 days

365

5.1

= 71.6 days

BRIEF EXERCISE 14-12 (Continued)

(b) Management should be concerned with the fact that inventory is moving

BRIEF EXERCISE 14–13

dividends Cash

BRIEF EXERCISE 14–14

SILVA CORPORATION

Partial Income Statement

Income before income taxes ………………………………………………… $450,000

BRIEF EXERCISE 14–15

HOLLOWAY CORPORATION

Partial Income Statement

Loss from operations of European facilities, net

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 14-1

Increase (Decrease) in 2015

Amount

Percent

Current assets $(21,000) (9.5)% [($199,000 – $220,000) ÷ $220,000]

DO IT! 14-2

2015 2014

(a) Current ratio:

(b) Inventory turnover:

(c) Profit margin ratio:

(d) Return on assets:

(e) Return on common stockholders’ equity:

(f) Debt to assets ratio:

(g) Times interest earned:

DO IT! 14-3

HRABIK CORPORATION

Income Statement (Partial)

Income before income taxes …………………………………. $500,000

Income tax expense ……………………………………………… 200,000

DO IT! 14-4

1.

Current ratio:

A measure used to evaluate a company’s

liquidity.

2.

Pro forma income:

Usually excludes items that a company

thinks are unusual or nonrecurring.

3.

Quality of earnings:

Indicates the level of full and transparent

information provided to users of the

financial statements.

4.

Discontinued operations:

The disposal of a significant component of a

business.

5.

Horizontal analysis:

Determines increases or decreases in a

series of financial statement data.

6.

Comprehensive income:

Includes all changes in stockholders’ equity

during a period except those resulting from

investments by stockholders and distribu-

tions to stockholders.

SOLUTIONS TO EXERCISES

EXERCISE 14-1

KURZEN INC.

Condensed Balance Sheets

December 31

Increase or (Decrease)

2015

2014

Amount

Percentage

Assets

Current assets

Plant assets (net)

Total assets

$125,000

396,000

$521,000

$100,000

330,000

$430,000

($25,000

( 66,000

91,000

(25.0%)

(20.0%)

(21.2%)

Liabilities

Current liabilities

Long-term liabilities

Total liabilities

$ 91,000

133,000

224,000

$ 70,000

95,000

165,000

($21,000)

( 38,000)

( 59,000)

(30.0%)

(40.0%)

(35.8%)

Stockholders’ Equity

Common stock, $1 par

Retained earnings

Total stockholders’

equity

Total liabilities and

stockholders’

equity

161,000

136,000

297,000

$521,000

115,000

150,000

265,000

$430,000

( 46,000

(14,000)

( 32,000)

($91,000)

(40.0%)

(9.3%)

( 12.1%)

21.2%