CHAPTER 13

Statement of Cash Flows

ASSIGNMENT CLASSIFICATION TABLE

Learning Objectives

Questions

Brief

Exercises

Do It!

Exercises

A

Problems

B

Problems

*1. Indicate the usefulness

of the statement of

cash flows.

1, 2, 15

*2. Distinguish among

operating, investing,

and financing activities.

3, 4, 5, 6, 7,

8, 9, 16, 17

1, 2, 3

1

1, 2, 3

1A

1B

*3. Prepare a statement

of cash flows using

the indirect method.

10, 11, 12,

13, 14

4, 5, 6, 7

2

4, 5, 6,

7, 8, 9

2A, 3A, 5A,

7A, 9A, 11A

2B, 3B, 5B,

7B, 9B, 11B

*4. Analyze the statement

of cash flows.

8, 9, 10, 11

3

7, 9

7A, 8A

7B, 8B

*5. Prepare a statement

of cash flows using

the direct method.

8, 18, 19, 20,

21

12, 13, 14

10, 11,

12, 13,

4A, 6A, 8A,

10A

4B, 6B, 8B,

10B

*6. Explain how to use a

worksheet to prepare the

statement of cash flows

using the indirect method.

22

15

14

12A

*Note: All asterisked Questions, Exercises, and Problems relate to material contained in the appendices*to the

chapter.

ASSIGNMENT CHARACTERISTICS TABLE

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

1A

Distinguish among operating, investing, and financing

activities.

Simple

10–15

2A

Determine cash flow effects of changes in equity accounts.

Simple

10–15

3A

Prepare the operating activities section—indirect method.

Simple

20–30

*4A

Prepare the operating activities section—direct method.

Simple

20–30

5A

Prepare the operating activities section—indirect method.

Simple

20–30

*6A

Prepare the operating activities section—direct method.

Simple

20–30

7A

Prepare a statement of cash flows—indirect method, and

compute free cash flow.

Moderate

40–50

*8A

Prepare a statement of cash flows—direct method, and

compute free cash flow.

Moderate

40–50

9A

Prepare a statement of cash flows—indirect method.

Moderate

40–50

*10A

Prepare a statement of cash flows—direct method.

Moderate

40–50

11A

Prepare a statement of cash flows—indirect method.

Moderate

40–50

*12A

Prepare a worksheet—indirect method.

Moderate

40–50

1B

Distinguish among operating, investing, and financing

activities.

Simple

10–15

2B

Determine cash flow effects of changes in plant asset

accounts.

Simple

10–15

3B

Prepare the operating activities section—indirect method.

Simple

20–30

*4B

Prepare the operating activities section—direct method.

Simple

20–30

5B

Prepare the operating activities section—indirect method.

Simple

20–30

*6B

Prepare the operating activities section—direct method.

Simple

20–30

7B

Prepare a statement of cash flows—indirect method, and

compute free cash flow.

Moderate

40–50

ASSIGNMENT CHARACTERISTICS TABLE (Continued)

Problem

Number

Description

Difficulty

Level

Time

Allotted (min.)

*8B

Prepare a statement of cash flows—direct method, and

compute free cash flow.

Moderate

40–50

9B

Prepare a statement of cash flows—indirect method.

Moderate

40–50

*10B

Prepare a statement of cash flows—direct method.

Moderate

40–50

11B

Prepare a statement of cash flows—indirect method.

Moderate

40–50

WEYGANDT FINANCIAL ACCOUNTING 9E

CHAPTER 13

STATEMENT OF CASH FLOWS

Number

LO

BT

Difficulty

Time (min.)

BE1

2

AP

Simple

3–5

BE2

2

C

Simple

2–4

BE3

2

AP

Simple

3–5

BE4

3

AP

Simple

4–6

BE5

3

AP

Simple

3–5

BE6

3

AP

Simple

4–6

BE7

3

AN

Moderate

3–5

BE8

4

AN

Simple

2–4

BE9

4

AN

Simple

2–3

BE10

4

AN

Simple

2–3

BE11

4

AN

Simple

4–6

BE12

5

AP

Simple

2–4

BE13

5

AP

Simple

3–5

BE14

5

AP

Moderate

3–5

BE15

6

AP

Simple

4–6

DI1

2

C

Simple

2–4

DI2

3

AP

Simple

4–6

DI3

4

AN, C

Simple

4–6

EX1

2

C

Simple

5–7

EX2

2

C

Simple

6–8

EX3

2

AP

Simple

8–10

EX4

3

AP

Simple

5–7

EX5

3

AP

Simple

6–8

EX6

3

AN

Moderate

10–12

EX7

3, 4

AP

Simple

12–14

EX8

3

AP

Simple

10–12

EX9

3, 4

AP

Simple

12–14

EX10

5

AP

Moderate

6–8

EX11

5

AP

Moderate

6–8

EX12

5

AP

Simple

5–7

EX13

5

AP

Moderate

6–8

STATEMENT OF CASH FLOWS (Continued)

Number

LO

BT

Difficulty

Time (min.)

EX14

6

AP

Moderate

16–20

P1A

2

C

Simple

10–15

P2A

3

AN

Simple

10–15

P3A

3

AP

Simple

20–30

P4A

5

AP

Simple

20–30

P5A

3

AP

Simple

20–30

P6A

5

AP

Simple

20–30

P7A

3, 4

AP, AN

Moderate

40–50

P8A

4, 5

AP, AN

Moderate

40–50

P9A

3

AP

Moderate

40–50

P10A

5

AP

Moderate

40–50

P11A

3

AP

Moderate

40–50

P12A

6

AP

Moderate

40–50

P1B

2

C

Simple

10–15

P2B

3

AN

Simple

10–15

P3B

3

AP

Simple

20–30

P4B

5

AP

Simple

20–30

P5B

3

AP

Simple

20–30

P6B

5

AP

Simple

20–30

P7B

3, 4

AP, AN

Moderate

40–50

P8B

4, 5

AP, AN

Moderate

40–50

P9B

3

AP

Moderate

40–50

P10B

5

AP

Moderate

40–50

P11B

3

AP

Moderate

40–50

BYP1

2

AN

Simple

15–20

BYP2

4

AP, E

Simple

8–12

BYP3

4

AP, E

Simple

8–12

BYP4

—

C

Simple

15–20

BYP5

—

C

Simple

10–15

BYP6

3

AP, E

Moderate

25–30

BYP7

2

AP

Simple

10–15

BYP8

2

E

Simple

10–15

BYP9

—

E

Simple

15–20

BYP10

—

AP

Moderate

10–15

BLOOM’S TAXONOMY TABLE

13-2 Copyright © 2014 John Wiley & Sons, Inc. Weygandt, Financial Accounting, 9/e, Solutions Manual (For Instructor Use Only)

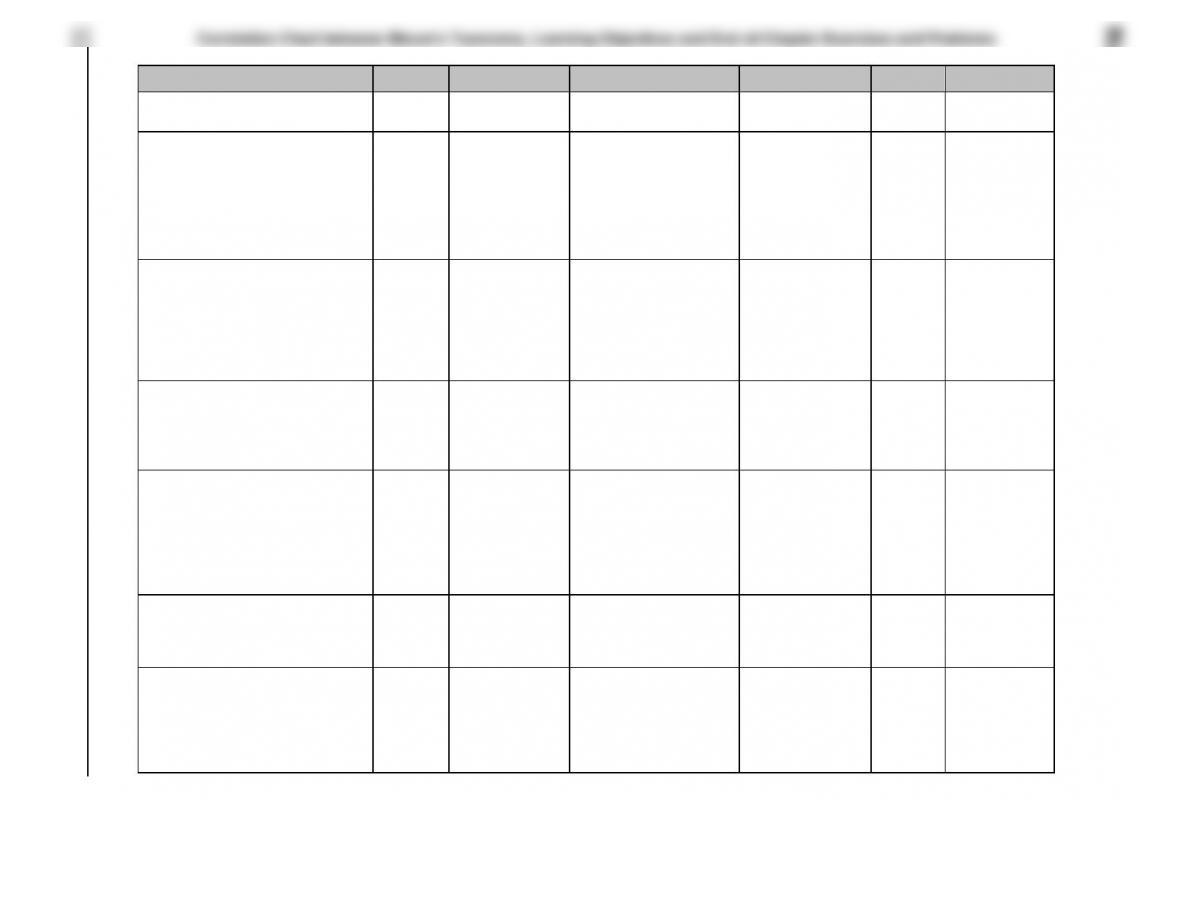

Correlation Chart between Bloom’s Taxonomy, Learning Objectives and End–of-Chapter Exercises and Problems

Learning Objective

Knowledge

Comprehension

Application

Analysis

Synthesis

Evaluation

1. Indicate the usefulness of the

statement of cash flows.

Q13-1

Q13-2

Q13-15

2. Distinguish among operating,

investing, and financing

activities.

Q13-4

Q13-6

Q13-3

Q13-5

Q13-7

Q13-8

Q13-9

Q13-16

Q13-17

BE13-2

DI13-1

E13-1

E13-2

P13-1A

P13-1B

BE13-1

BE13-3

E13-3

3. Prepare a statement of cash

flows using the indirect

method.

Q13-13

Q13-10

Q13-11

Q13-12

Q13-14

BE13-4

BE13-5

BE13-6

DI13-2

E13-4

E13-5

E13-7

E13-8

E13-9

P13-3A

P13-5A

P13-7A

P13-9A

P13-11A

P13-3B

P13-5B

P13-7B

P13-9B

P13-11B

BE13-7

E13-6

P13-2A

P13-7A

P13-2B

P13-7B

4. Analyze the statement of

cash flows.

Dl13-3

E13-7

E13-9

P13-7A

P13-8A

P13-7B

P13-8B

BE13-8

BE13-9

BE13-10

BE13-11

DI13-3

P13-7A

P13-8A

P13-7B

P13-8B

*5. Prepare a statement of cash

flows using the direct

method.

Q13-8

Q13-18

Q13-21

Q13-19

Q13-20

BE13-12

BE13-13

BE13-14

E13-10

E13-11

E13-12

E13-13

P13-4A

P13-6A

P13-8A

P13-10A

P13-4B

P13-6B

P13-8B

P13-10B

P13-8A

P13-8B

*6 Explain how to use a

worksheet to prepare the

statement of cash flows

using the indirect method.

Q13-22

BE13-15

E13-14

P13-12A

Broadening Your Perspective

Real-World Focus

Comparative Analysis

Decision Making Across

the Organization

Communication

FASB Codification

Financial Reporting

Comp. Analysis

Decision Making

Across the

Organization

Ethics Case

All About You

ANSWERS TO QUESTIONS

1. (a) The statement of cash flows reports the cash receipts, cash payments, and net change in cash

period.

2. The statement of cash flows answers the following questions about cash: (a) Where did the cash

3. The three types of activities are:

equipment and (b) lending money and collecting loans.

4. (a) Major inflows of cash in a statement of cash flows include cash from operations; issuance of

property, plant, and equipment.

5. The statement of cash flows presents investing and financing activities so that even noncash

schedule to the financial statements.

6. Examples of significant noncash activities are: (1) issuance of stock for assets, (2) conversion of

of property, plant, and equipment.

7. Comparative balance sheets, a current income statement, and certain transaction data all provide

transactions provide additional detailed information needed to determine how cash was provided

or used during the period.

8. The advantage of the direct method is that it presents the major categories of cash receipts and

cash payments in a format that is similar to the income statement and familiar to statement users. Its

The advantage of the indirect method is it is often considered easier to prepare, and it focuses

on the differences between net income and net cash provided by operating activities. It also tends to

Both methods are acceptable but the FASB expressed a preference for the direct method. Yet,

the indirect method is the overwhelming favorite of companies.

Questions Chapter 13 (Continued)

9. When total cash inflows exceed total cash outflows, the excess is identified as a “net increase in cash”

10. The indirect method involves converting accrual net income to net cash provided by operating activities.

and current liability accounts from one period to the next.

11. It is necessary to convert accrual–based net income to cash-basis income because the unadjusted

income must be adjusted to reflect the net cash provided by operating activities.

12. A number of factors could have caused an increase in cash despite the net loss. These are (1) high

accounting, e.g. depreciation.

13. Depreciation expense.

Increase/decrease in accounts receivable.

Increase/decrease in inventory.

Increase/decrease in accounts payable.

14. Under the indirect method, depreciation is added back to net income to reconcile net income to net

15. The statement of cash flows is useful because it provides information to the investors, creditors,

during the period.

16. This transaction is reported in the note or schedule entitled “Noncash investing and financing activities”

17. In its 2011 statement of cash flows, Apple reported $37,529 million net cash provided by

operating activities, $40,419 million used for investing activities, and $1,444 million provided by

financing activities.

*18. Net cash provided by operating activities under the direct approach is the difference between cash

revenues and cash expenses. The direct approach adjusts the revenues and expenses directly

to reflect the cash basis. This results in cash net income, which is equal to “net cash provided by

operating activities.”

Questions Chapter 13 (Continued)

+ Decrease in accounts receivable

*19.

(a)

Cash receipts from customers = Revenues from sales

– Increase in accounts receivable

+ Increase in inventory

(b)

Purchases = Cost of goods sold

– Decrease in inventory

+ Decrease in accounts payable

Cash payments to suppliers = Purchases

– Increase in accounts payable

*20. Sales revenue………………………………………………………………………………………….. $2,000,000

Add: Decrease in accounts receivable ………………………………………………………… 200,000

Cash receipts from customers ……………………………………………………………………. $2,200,000

*22. A worksheet is desirable because it allows the accumulation and classification of data that will

appear on the statement of cash flows. It is an optional but efficient device that aids in the prepa–

ration of the statement of cash flows.

SOLUTIONS TO BRIEF EXERCISES

BRIEF EXERCISE 13-1

BRIEF EXERCISE 13-2

BRIEF EXERCISE 13-3

Cash flows from financing activities

Proceeds from issuance of bonds payable ………………….. $300,000)

BRIEF EXERCISE 13-4

Net income …………………………..…………………….. $2,800,000

Adjustments to reconcile net income

to net cash provided by operating activities