Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

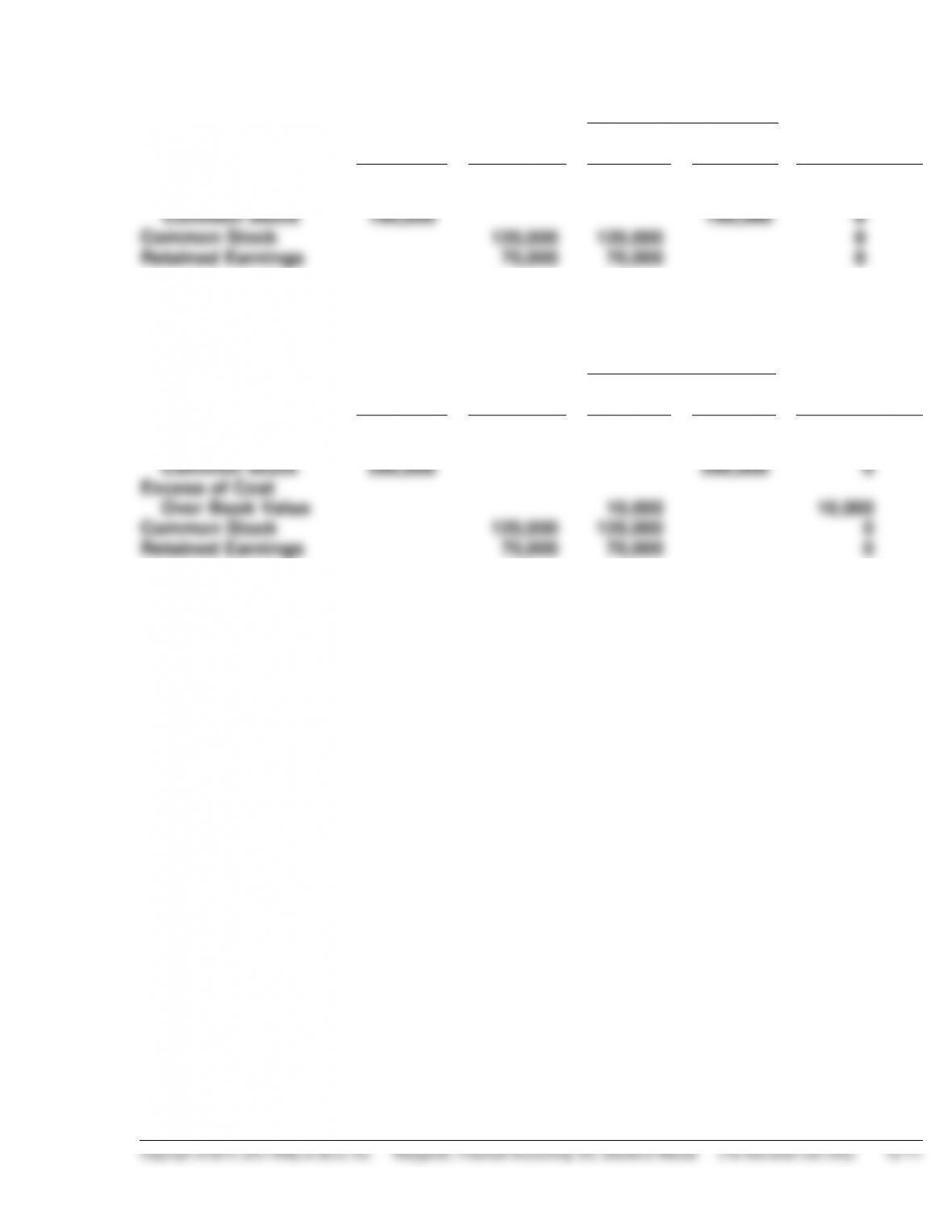

*BRIEF EXERCISE 12-9

Eliminations

Paula

Company

Shannon

Company

Dr.

Cr.

Consolidated

Data

Investment in

Shannon

Common Stock

190,000

190,000

0

Common Stock

120,000

120,000

0

Retained Earnings

70,000

70,000

0

*BRIEF EXERCISE 12-10

Eliminations

Paula

Company

Shannon

Company

Dr.

Cr.

Consolidated

Data

Investment in

Shannon

Common Stock

200,000

200,000

0

Excess of Cost

Over Book Value

10,000

10,000

Common Stock

120,000

120,000

0

Retained Earnings

70,000

70,000

0

SOLUTIONS FOR DO IT! REVIEW EXERCISES

DO IT! 12-1

(a) Jan. 1 Debt Investments ..................................... 50,000

July 1 Cash .......................................................... 2,500

July 1 Cash .......................................................... 29,000

Loss on Sale of Debt Investments .......... 1,000

(b) Dec. 31 Interest Receivable .................................. 1,000

DO IT! 12-2

(a) June 17 Stock Investments .................................... 550,000

Sept. 3 Cash ........................................................... 16,000

(b) Jan. 1 Stock Investments .................................... 540,000

May 15 Cash ........................................................... 45,000

Dec. 31 Stock Investments .................................... 81,000

DO IT! 12-3

Trading securities:

Unrealized Loss—Income ................................................. 14,600*

Available-for-sale securities:

**$5,750 + $4,200

DO IT! 12-4

Item

Financial statement

Category

1. Loss on sale of investments

in stock.

Income statement

Other expenses

and losses

2. Unrealized gain on available-

for-sale securities.

Balance sheet

Stockholders’

equity

3. Fair value adjustment—

trading.

Balance sheet

Current assets

4. Interest earned on

investments in bonds.

Income statement

Other revenues

and gains

5. Unrealized loss on trading

securities.

Income statement

Other expenses

and losses

SOLUTIONS TO EXERCISES

EXERCISE 12-1

1. Companies purchase investments in debt or stock securities because

2. A corporation would have excess cash that it does not need for operations

3. The typical investment when investing cash for short periods of time

4. The typical investments when investing cash to generate earnings are

debt securities and stock securities.

5. A company would invest in securities that provide no current cash flows

increase in value.

6. The typical investment when investing cash for strategic reasons is

stock of companies in a related industry or in an unrelated industry that

the company wishes to enter.

EXERCISE 12-2

(a) Jan. 1 Debt Investments ..................................... 50,000

July 1 Cash ($50,000 X 9% X 1/2) ....................... 2,250

1 Cash .......................................................... 33,000

EXERCISE 12-2 (Continued)

(b) Dec. 31 Interest Receivable ................................... 900

EXERCISE 12-3

January 1, 2015

Debt Investments .............................................................. 70,000

July 1, 2015

Cash ($70,000 X 12% X 6/12) ............................................ 4,200

December 31, 2015

Interest Receivable ............................................................ 4,200

January 1, 2016

Cash ................................................................................... 4,200

January 1, 2016

Cash ................................................................................... 38,500

EXERCISE 12-4

(a) Feb. 1 Stock Investments ................................... 7,200

July 1 Cash (600 X $1) ........................................ 600

Sept. 1 Cash .......................................................... 4,300

Dec. 1 Cash (300 X $1) ........................................ 300

EXERCISE 12-5

Jan. 1 Stock Investments ........................................... 152,000

July 1 Cash (2,500 X $3) ............................................. 7,500

Dec. 1 Cash ................................................................. 32,000

EXERCISE 12-6

February 1

Stock Investments ............................................................. 16,000

March 20

Cash ................................................................................... 2,900

April 25

Cash (400 X $1) .................................................................. 400

June 15

Cash ................................................................................... 7,600

July 28

Cash (200 X $1.25) ............................................................. 250

EXERCISE 12-7

(a) Jan. 1 Stock Investments .................................... 180,000

Dec. 31 Cash ($60,000 X 25%) ............................... 15,000

31 Stock Investments .................................... 50,000

(b) Investment in Helbert, January 1 ........................................ $180,000

EXERCISE 12-8

(a) 2015

Mar. 18 Stock Investments .................................. 260,000

June 30 Cash ........................................................ 6,000

Dec. 31 Fair Value Adjustment—Available-

(b) Jan. 1 Stock Investments .................................. 108,000

June 15 Cash ........................................................ 12,000

Dec. 31 Stock Investments .................................. 32,000

EXERCISE 12-9

(b) When a company owns more than 50% of the common stock of another

control.

EXERCISE 12-10

(a) Dec. 31 Unrealized Loss—Income ............................. 2,000

(b) Balance Sheet

Current assets

Income Statement

Other expenses and losses

EXERCISE 12-11

(a) Dec. 31 Unrealized Gain or Loss—Equity ................. 2,000

(b) Balance Sheet

Investments

Investments in stock of less than 20% owned

Stockholders’ equity

Less: Unrealized loss on available-for-sale

EXERCISE 12-11 (Continued)

(c) Dear Ms. Kretsinger:

Investments which are classified as trading (held for sale in the near

term) are reported at fair value in the balance sheet, with unrealized

stockholders’ equity section.

Fair value is used as a reporting basis because it represents the cash

realizable value of the securities. Unrealized gains or losses on trading

investments are reported in the income statement because of the like-

reported directly in stockholders’ equity.

I hope that the preceding discussion clears up any misunderstandings.

Please contact me if you have any questions.

Sincerely,

Student