PROBLEM 11-3A (Continued)

(c) CASTLE CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

8% Preferred stock, $50

par value, cumulative,

are in arrears.

PROBLEM 11-4A

(a) Feb. 1 Cash Dividends (60,000 X $1) …………… 60,000

Mar. 1 Dividends Payable …………………………... 60,000

Apr. 1 Memo—two-for-one stock split

July 1 Stock Dividends (12,000 X $13) ………… 156,000

31 Common Stock Dividends

Distributable ………………………………… 120,000

31 Income Summary …………………………….. 350,000

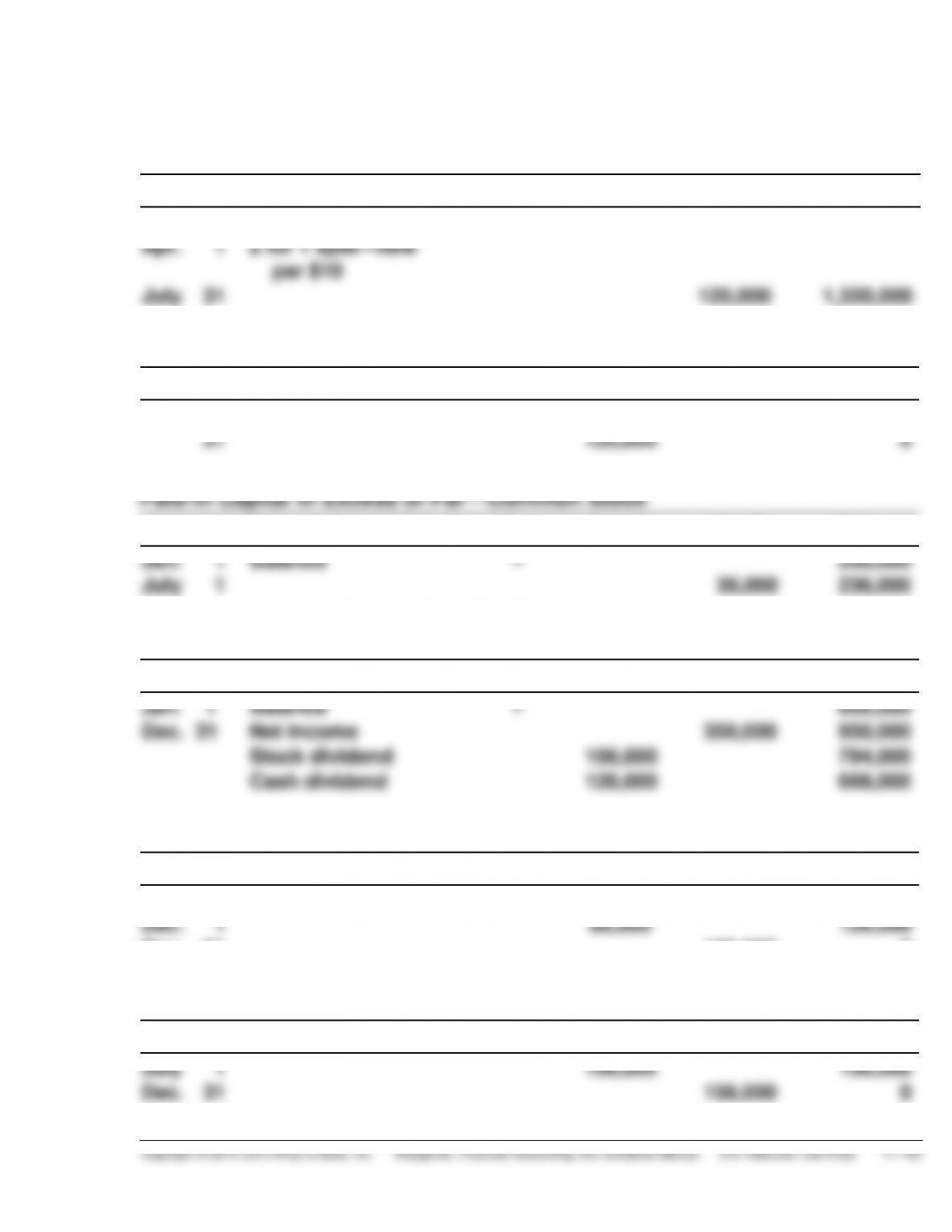

PROBLEM 11-4A (Continued)

(b)

Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Apr. 1

July 31

Balance

2 for 1 split—new

par $10

120,000

1,200,000

1,320,000

Common Stock Dividends Distributable

Date

Explanation

Ref.

Debit

Credit

Balance

July 1

31

120,000

120,000

120,000

0

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

July 1

Balance

36,000

200,000

236,000

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Dec. 31

Balance

Net income

Stock dividend

Cash dividend

156,000

126,000

350,000

600,000

950,000

794,000

668,000

Cash Dividends

Date

Explanation

Ref.

Debit

Credit

Balance

Feb. 1

Dec. 1

Dec. 31

60,000

66,000

126,000

60,000

126,000

0

Stock Dividends

Date

Explanation

Ref.

Debit

Credit

Balance

July 1

Dec. 31

156,000

156,000

156,000

0

PROBLEM 11-4A (Continued)

(c) GEFFREY CORPORATION

Balance Sheet (Partial)

December 31, 2015

Stockholders’ equity

Paid-in capital

Capital stock

Common stock, $10 par value, 132,000

shares issued and outstanding …………… $1,320,000

Additional paid-in capital

PROBLEM 11-5A

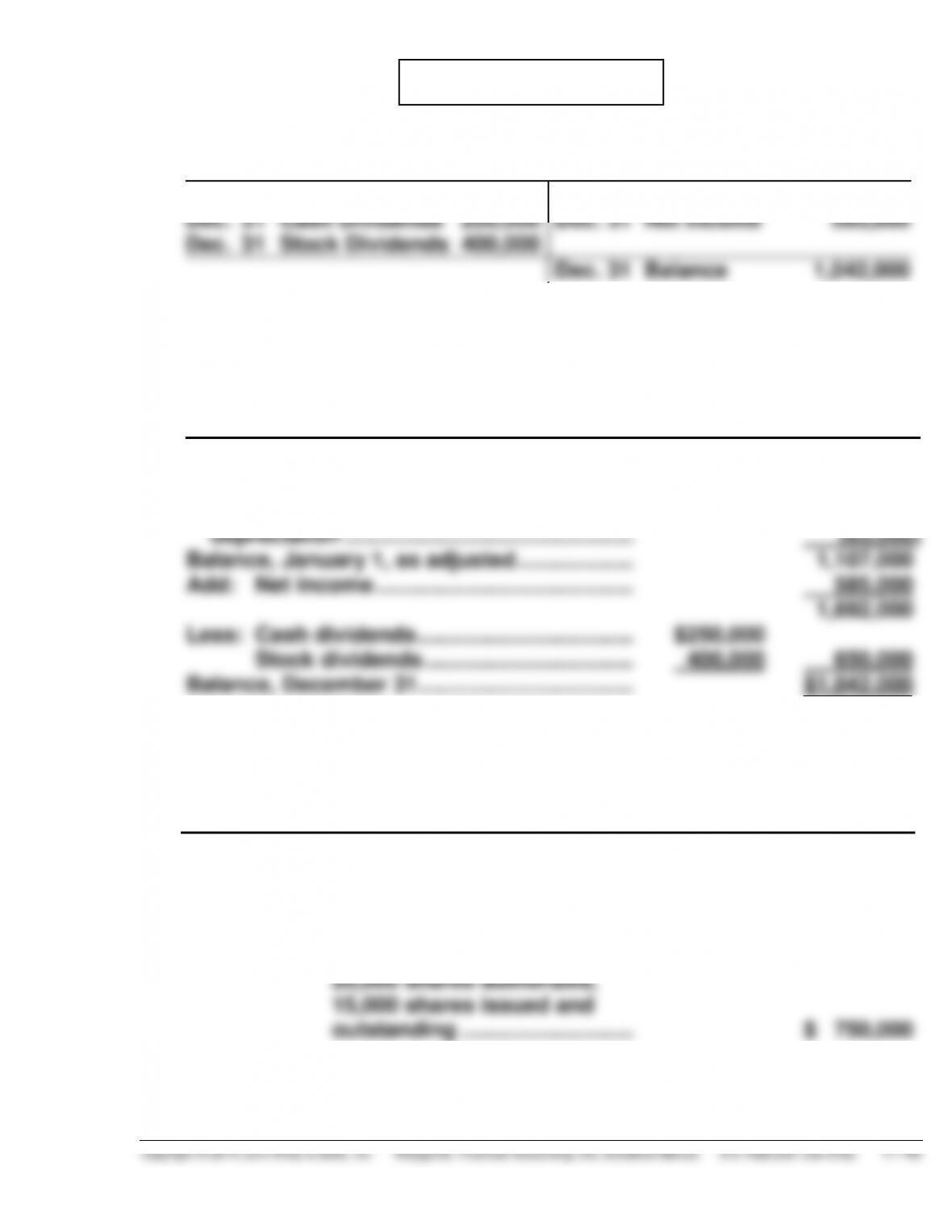

(a)

Retained Earnings

Sept. 1 Prior Per. Adj. 63,000

Dec. 31 Cash Dividends 250,000

Dec. 31 Stock Dividends 400,000

Jan. 1 Balance 1,170,000

Dec. 31 Net Income 585,000

Dec. 31 Balance 1,042,000

(b) STOREY CORPORATION

Retained Earnings Statement

For the Year Ended December 31, 2015

Balance, January 1, as reported ………………. $1,170,000

Correction of overstatement of 2014 net

income because of understatement of

(c) STOREY CORPORATION

Partial Balance Sheet

December 31, 2015

Stockholders’ equity

Paid-in capital

Capital stock

6% Preferred stock,

$50 par value, cumulative,

PROBLEM 11-5A (Continued)

STOREY CORPORATION (Continued)

Common stock, $10 par value,

500,000 shares authorized,

250,000 shares issued and

outstanding ………………………. $2,500,000

Common stock dividends

(d) Total cash dividend ………………………………… $250,000

Allocated to preferred stock

Dividend in arrears—2014

PROBLEM 11–6A

(a) (1) Land ………………………………………………….. 140,000

(2) Cash (400,000 X $7.00) ………………………… 2,800,000

(3) Treasury Stock (1,500 X $11) ……………….. 16,500

(4) Cash (500 X $14) …………………………………. 7,000

PROBLEM 11-6A (Continued)

(b) IRWIN CORPORATION

Stockholders’ equity

Paid-in capital

Capital stock

10% Preferred stock, $100

par value, noncumulative,

20,000 shares authorized,

PROBLEM 11-7A

(a) Jan. 15 Cash Dividends (75,000 X $1) ………….. 75,000

Feb. 15 Dividends Payable ………………………….. 75,000

Apr. 15 Stock Dividends (7,500 X $14) …………. 105,000

May 15 Common Stock Dividends

July 1 Memo—two-for-one stock split

31 Income Summary ……………………………. 250,000

31 Retained Earnings ………………………….. 174,000

31 Retained Earnings ………………………….. 105,000

PROBLEM 11-7A (Continued)

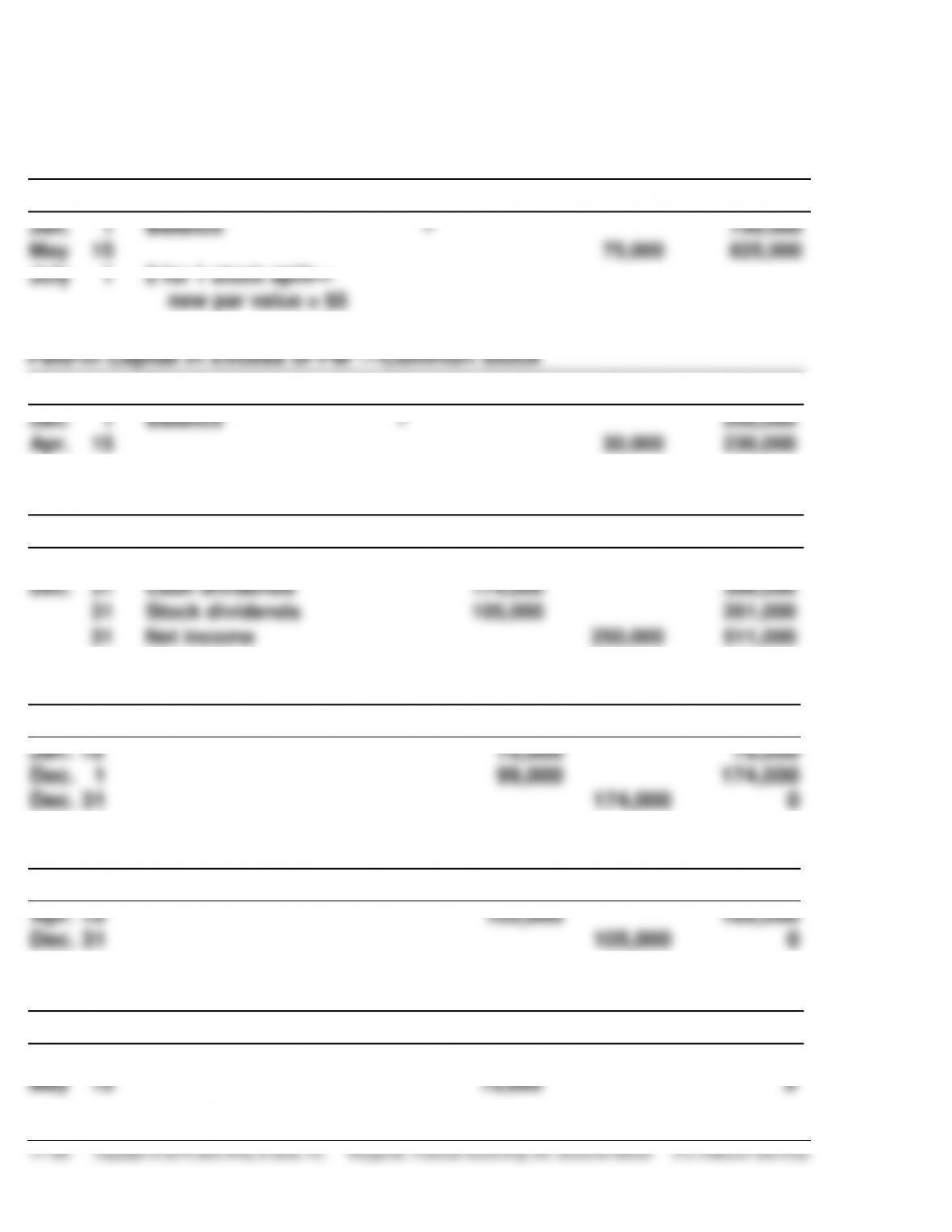

(b)

Common Stock

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

May 15

July 1

Balance

2 for 1 stock split—

new par value = $5

75,000

750,000

825,000

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Apr. 15

Balance

30,000

200,000

230,000

Retained Earnings

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 1

Dec. 31

31

31

Balance

Cash dividends

Stock dividends

Net income

174,000

105,000

250,000

540,000

366,000

261,000

511,000

Cash Dividends

Date

Explanation

Ref.

Debit

Credit

Balance

Jan. 15

75,000

75,000

Dec. 1

99,000

174,000

Dec. 31

174,000

0

Stock Dividends

Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 15

105,000

105,000

Dec. 31

105,000

0

Common Stock Dividends Distributable

Date

Explanation

Ref.

Debit

Credit

Balance

Apr. 15

May 15

75,000

75,000

75,000

0