BYP I-1 (Continued)

(d) BRYANT CO.

Income Statement

For the Month Ended January 31, 2014

Sales revenues

Sales ……………………………………….. $75,300

Less: Sales discounts………………. $ 90

Sales returns and

Operating expenses

Salaries and wages expense . $7,500

Rent expense …………………….. 850

supplies expense ……………….. 700

Other expenses and losses

Interest expense ……………………….. 50

BYP I-1 (Continued)

BRYANT CO.

Retained Earnings Statement

For the Month Ended January 31, 2014

Retained earnings, January 1, 2014 ……………………………….. $ 8,700

Add: Net income …………………………………………………………. 20,395

BRYANT CO.

Balance Sheet

January 31, 2014

Assets

Current assets

Cash …………………………………………………… $40,410

Accounts receivable ………………………….... 22,200

Notes receivable ………………………………….. 39,000

Property, plant, and equipment

Equipment …………………………………………… 6,450

Liabilities and Stockholders’ Equity

Current liabilities

Notes payable ……………………………………… $15,000

Stockholders’ equity

Common stock ……………………………………. 70,000

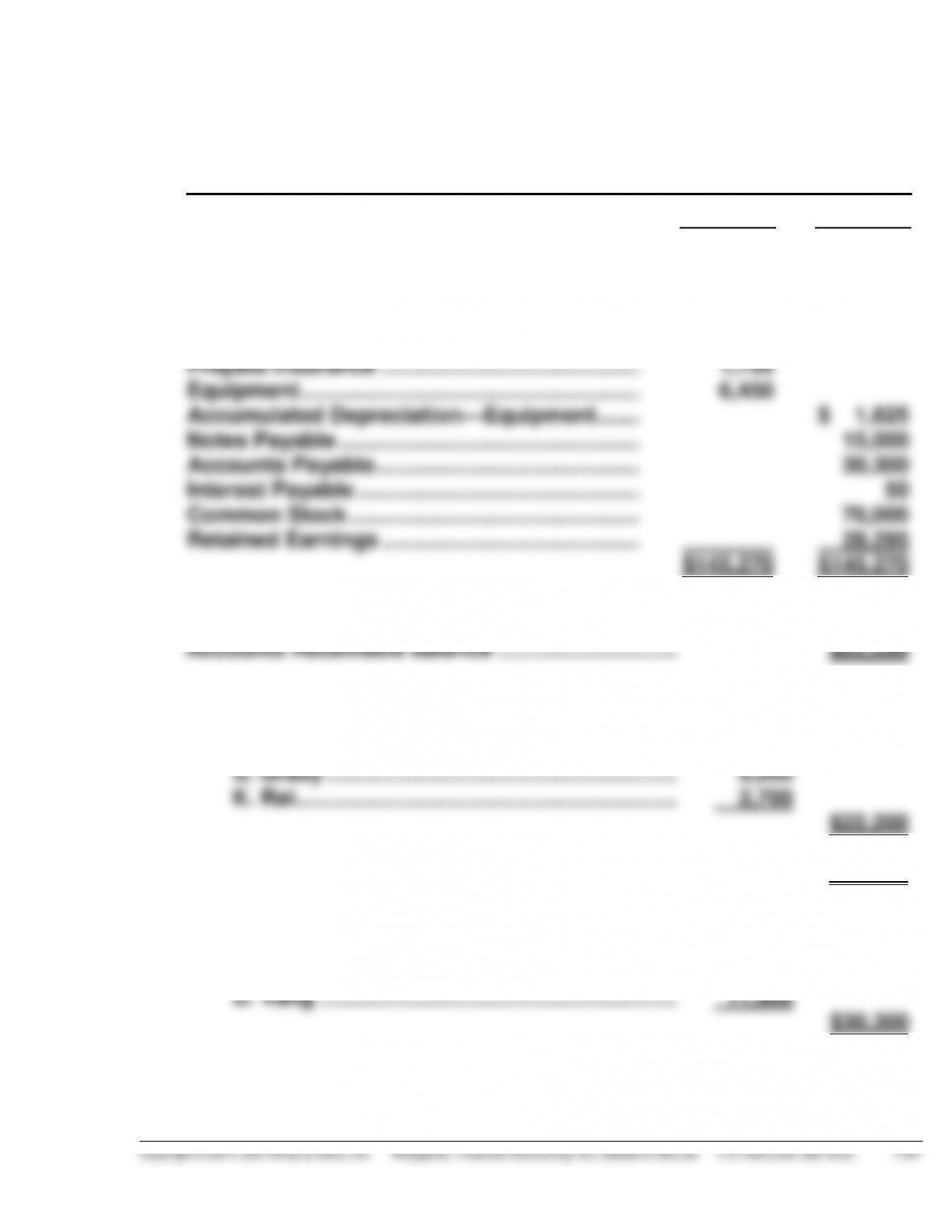

BYP I-1 (Continued)

(f) BRYANT CO.

Post-Closing Trial Balance

January 31, 2014

Debit

Credit

Cash ……………………………………………………….

Accounts Receivable………………………………..

Notes Receivable ……………………………………..

Inventory …………………………………………………

Supplies …………………………..……………………..

Prepaid Insurance ……………………………………

Equipment ……………………………………………….

Accumulated Depreciation—Equipment …….

Notes Payable ………………………………………….

Accounts Payable …………………………………….

Interest Payable ……………………………………….

Common Stock ………………………………………..

Retained Earnings ……………………………………

$ 40,410

22,200

39,000

34,560

900

1,750

6,450

$145,270

$ 1,625

15,000

30,300

50

70,000

28,295

$145,270

Subsidiary account balances

C. Dunlap ………………………………………………. $ 4,400

J. Fieber ………………………………………………… 6,100

Accounts Payable balance …………………………….. $30,300

Subsidiary account balances

W. Lachey ……………………………………………… $ 3,900

I. Maida ………………………………………………….. 14,500

BYP I-2 REAL-WORLD FOCUS

Some of the key features of the general ledger module highlighted by

the company are:

Highly flexible account and fiscal period setup, including different

account structures for separate companies.

Account numbers can be up to 20 characters long in 10 segments.

Statistical accounts for tracking nonfinancial information, such as

by the company are:

Handles purchases on account, manual and computer check payments,

and credit memos.

vendor.

Enter recurring transactions.

Put transactions on “hold” until you want to pay them.

BYP I-3 DECISION–MAKING ACROSS THE ORGANIZATION

(a) The special journals for Garin & Clark should be: (1) sales journal, (2)

purchases journal, (3) cash receipts journal, and (4) cash payments

journal.

1. Sales Journal columns:

Date.

Account Debited.

2. Purchases Journal columns:

Date.

Account Credited.

Terms.

Reference.

Accounts Payable, Cr.

Inventory—Appliances, Dr.

Inventory—Parts, Dr.

3. Cash Receipts Journal columns:

Date.

Account Credited.

Reference.

Cash, Dr.

Accounts Receivable, Cr.

Note: A Sales Discounts, Dr. column is not needed because all credit

terms are net/30 days.

BYP I-3 (Continued)

4. Cash Payments Journal columns:

Date.

Check Number.

Account Debited.

Reference.

Other Accounts, Dr.

(b) Garin & Clark should have:

1. An accounts receivable control account with individual customers’

accounts in a customers’ subsidiary ledger.

2. An accounts payable control account with individual creditors in a

creditors’ subsidiary ledger.

The use of control accounts and subsidiary ledgers will: (1) provide

necessary up-to-date information on specific customer and creditor

BYP I-4 COMMUNICATION ACTIVITY

Mr. Peter Gogan

2 Main Street

Central City, Michigan 48172

Dear Mr. Gogan:

Thank you for hiring two additional bookkeepers a month ago to help me with

the accounting. Unfortunately, the inefficiencies in recording transactions

I would like to suggest some changes in the accounting system. Because of

the increased volume of business, I believe it is time for us to use special

1. Sales journal—for all sales of merchandise on account.

2. Cash receipts journal—for all cash received.

To use special journals, we will need columnar journal paper which can be

obtained at any office supply store at very low cost. I can also quickly train the

Special journals also make it possible to do some postings monthly. This

will significantly reduce the time required to make daily postings. As a result,

Yours sincerely,

Kate

BYP I-5 ETHICS CASE

(a) The stakeholders in this case are:

Orlando Cepeda, manager of Stanton’s centralized computer

accounting operation.

(b) Orlando instructions to assign the Bayport code to all uncoded and

incorrectly coded sales documents overstates the sales of Bayport

(c) Stanton Products Company should have a written policy covering un–

coded and incorrectly coded sales documents. This would prevent the