BRIEF EXERCISE G-18

0 1 2 3 4 9 10

Discount rate from Table 4 is 7.72173. Present value of 10 payments of

BRIEF EXERCISE G-19

0 1 2 3

To determine the present value of the future cash inflows, discount the future

cash flows at 8%, using Table 3.

Year 1 ($40,000 X .92593) = $ 37,037.20

To achieve a minimum rate of return of 8%, Coleman Company should pay

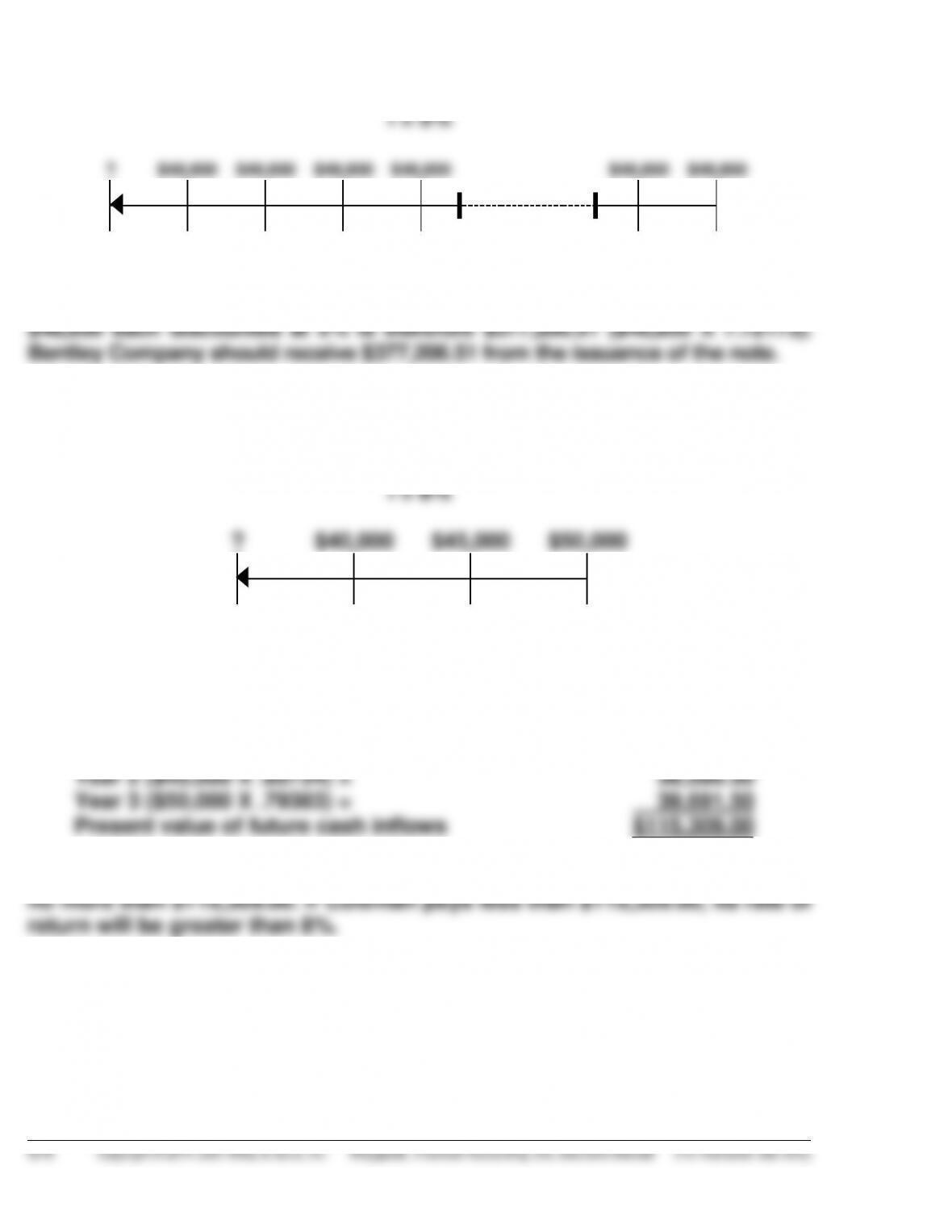

BRIEF EXERCISE G-20

0 1 2 3 4 11 12

Present value = Future value X Present value of 1 factor

The .39713 for 12 periods approximates the value found in the 8% column

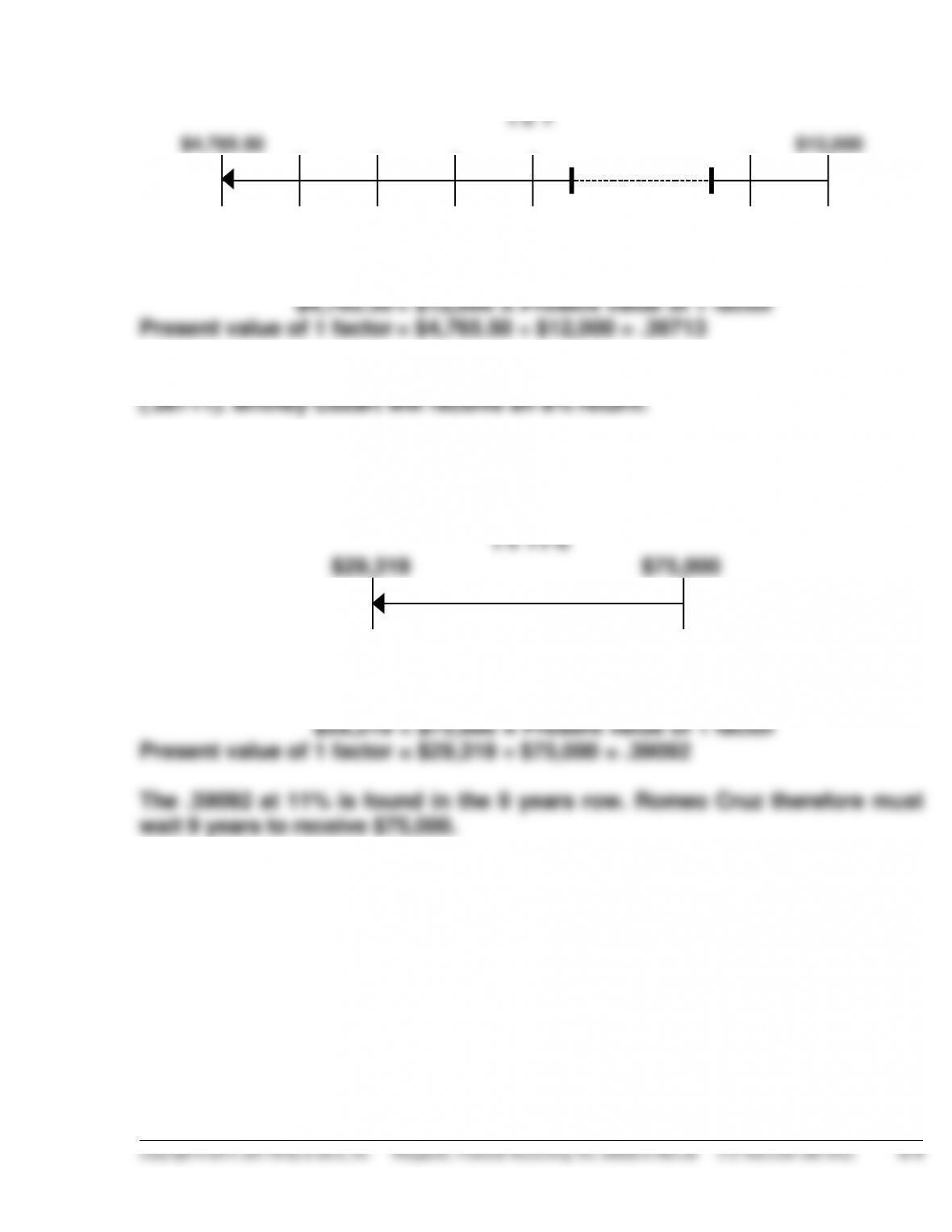

BRIEF EXERCISE G-21

n = ?

Present value = Future value X Present value of 1 factor

BRIEF EXERCISE G-22

i = ?

0 1 2 3 4 5 6 14 15

Present value = Future amount X Present value of an annuity factor

BRIEF EXERCISE G-23

n = ?

Present value = Future amount X Present value of an annuity factor

BRIEF EXERCISE G-24

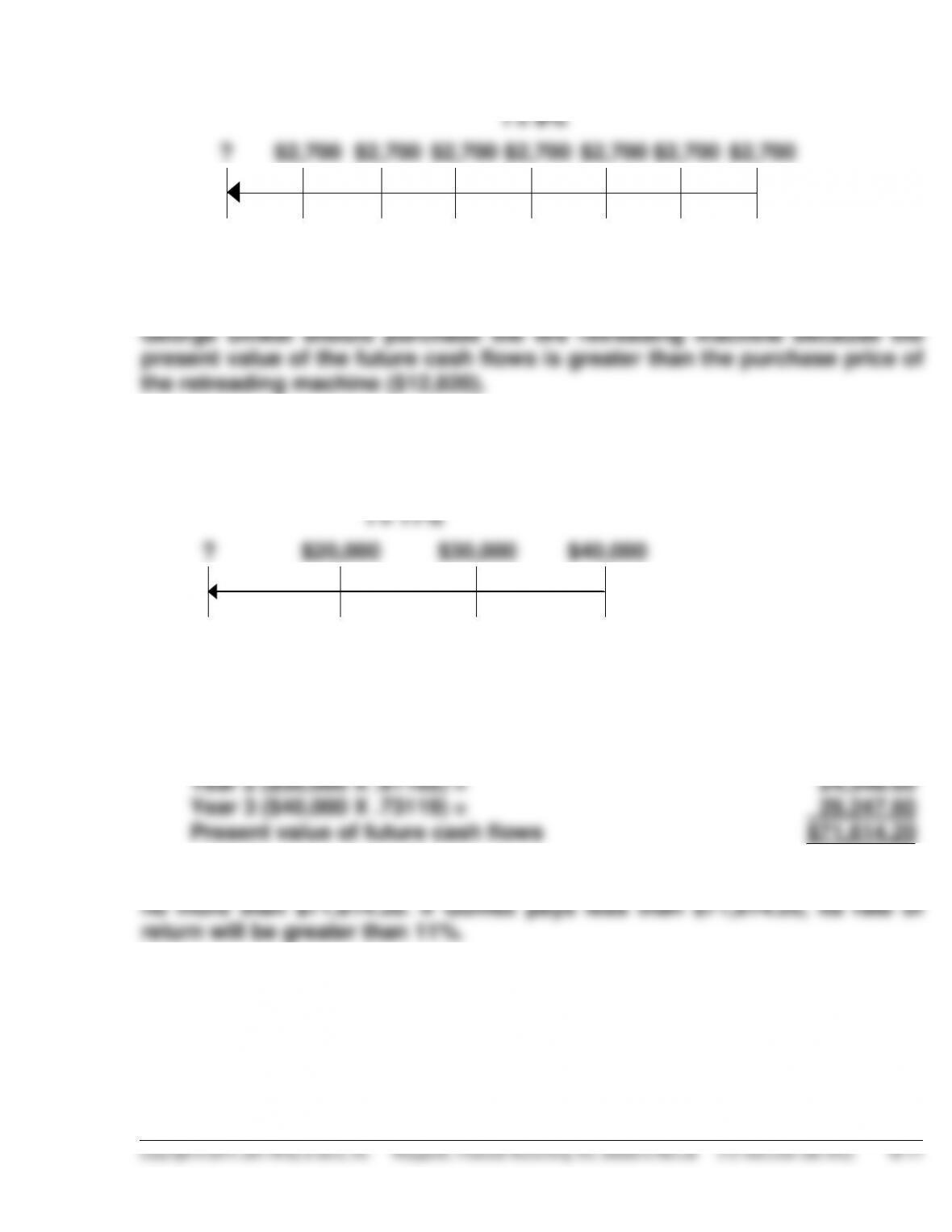

i = 9%

?

$2,700

$2,700

$2,700

$2,700

$2,700

$2,700

$2,700

0

1

2

3

4

5

6

7

Discount rate from Table 4 is 5.03295. Present value of 7 payments of

$2,700 each discounted at 9% is therefore $13,588.97 ($2,700 X 5.03295).

BRIEF EXERCISE G-25

i = 11%

?

$20,000

$30,000

$40,000

0

1

2

3

To determine the present value of the future cash flows, discount the future

cash flows at 11%, using Table 3.

Year 1 ($20,000 X .90090) =

$18,018.00

Year 2 ($30,000 X .81162) =

24,348.60

Year 3 ($40,000 X .73119) =

29,247.60

Present value of future cash flows

$71,614.20

To achieve a minimum rate of return of 11%, Gomez Company should pay

BRIEF EXERCISE G-26

10*

?

–18,000

0

50,000

N

I/YR.

PV

PMT

FV

10.76%

BRIEF EXERCISE G-27

10

?

60,000

–8,860

0

N

I/YR.

PV

PMT

FV

7.80%

BRIEF EXERCISE G-28

40

?

178,000*

–8,400

0

N

I/YR.

PV

PMT

FV

3.55%

(semiannual)

BRIEF EXERCISE G-29

(a)

Inputs:

7

6.9

?

–16,000

0

N

I

PV

PMT

FV

Answer:

86,530.07

(b)

Inputs:

10

8.65

?

14,000**

200,000*

N

I

PV

PMT

FV

Answer:

–178,491.52

*200 X $1,000 **$200,000 X .07

BRIEF EXERCISE G-30

(a)

Note—set payments at 12 per year.

Inputs:

96

7.8

42,000

?

0

N

I

PV

PMT

FV

Answer:

–589.48

(b)

Note—set payments to 1 per year.

Inputs:

5

7.25

8,000

?

0

N

I

PV

PMT

FV

Answer:

–1,964.20