3 – 1

CHAPTER

3

Depreciation Accounting Techniques

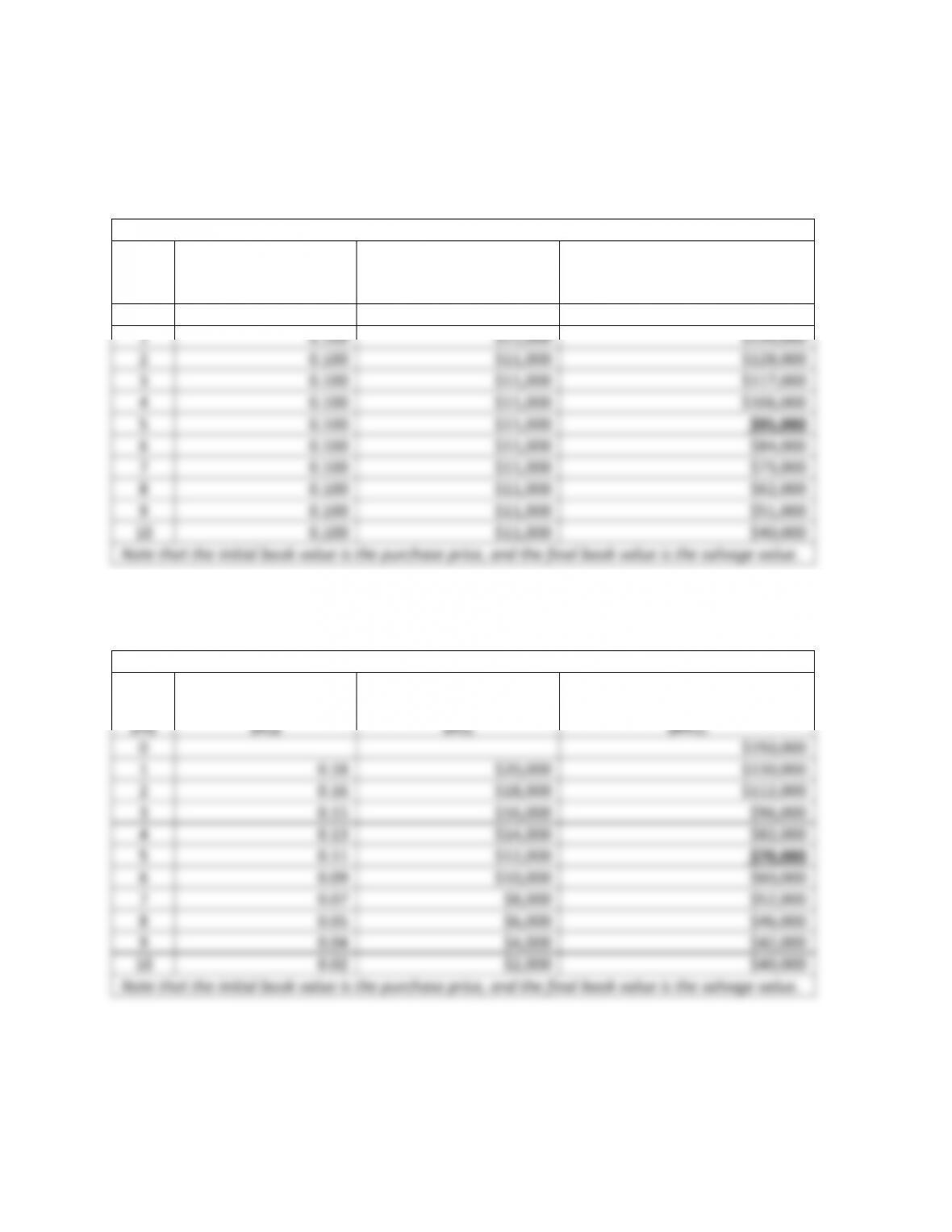

1. A contractor purchased a tractor for $180,000 and anticipates using it for nine years. The

salvage value of the tractor at the end of the nine years is estimated to be $27,000. Using the

straight-line method of depreciation accounting, determine the book value of the tractor at the

end of each of the nine years.

The annual depreciation rate can be determined with Equation 3.1 to be

The annual depreciation amount can be determined with Equation 3.2 to be

The book value for each year can be determined with Equation 3.3 as shown in the table

below.

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

N/A

N/A

$180,000

1

1/9 = 0.11

R1(P-F) = $17,000

$180,000 – $17,000 = $163,000

2

1/9 = 0.11

R1(P-F) = $17,000

$163,000 – $17,000 = $146,000

3

1/9 = 0.11

R1(P-F) = $17,000

$146,000 – $17,000 = $129,000

4

1/9 = 0.11

R1(P-F) = $17,000

$129,000 – $17,000 = $112,000

5

1/9 = 0.11

R1(P-F) = $17,000

$112,000 – $17,000 = $95,000

6

1/9 = 0.11

R1(P-F) = $17,000

$95,000 – $17,000 = $78,000

7

1/9 = 0.11

R1(P-F) = $17,000

$78,000 – $17,000 = $61,000

8

1/9 = 0.11

R1(P-F) = $17,000

$61,000 – $17,000 = $44,000

9

1/9 = 0.11

R1(P-F) = $17,000

$44,000 – $17,000 = $27,000

Note that the initial book value is the purchase price, and the final book value is the salvage value.

3 – 2

2. Determine the book value at the end of each of the nine years for the tractor described in

Problem 1, using the sum-of-the-years method of depreciation accounting.

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

N/A

N/A

$180,000

1

(9-1+1)/SOY

R1(P-F) = $30,600

$180,000 – $30,600 = $149,400

2

(9-2+1)/SOY

R1(P-F) = $27,200

$163,000 – $27,200 = $122,200

3

(9-3+1)/SOY

R1(P-F) = $23,800

$146,000 – $23,800 = $98,400

4

(9-4+1)/SOY

R1(P-F) = $20,400

$129,000 – $20,400 = $78,000

5

(9-5+1)/SOY

R1(P-F) = $17,000

$112,000 – $17,000 = $61,000

6

(9-6+1)/SOY

R1(P-F) = $13,600

$95,000 – $13,600 = $47,400

7

(9-7+1)/SOY

R1(P-F) = $10,200

$78,000 – $10,200 = $37,200

8

(9-8+1)/SOY

R1(P-F) = $6,800

$61,000 – $6,800 = $30,400

9

(9-9+1)/SOY

R1(P-F) = $3,400

$44,000 – $3,400 = $27,000

Note that the initial book value is the purchase price, and the final book value is the salvage value.

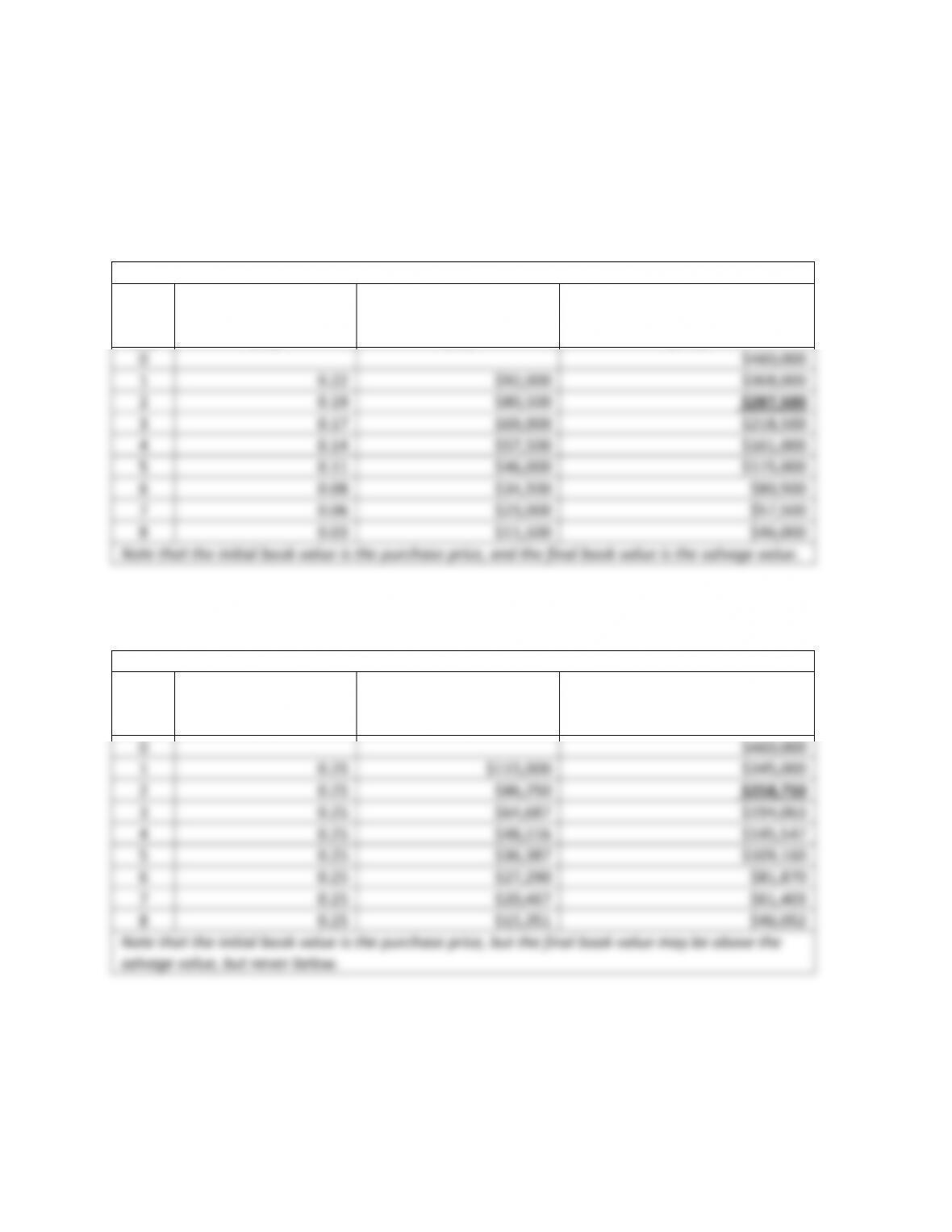

3. Determine the book value at the end of each of the nine years for the tractor described in

Problem 1, using the 1.80 declining-balance method of depreciation accounting.

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

N/A

N/A

$180,000

1

1.8/9=0.20

R1(P-F) = $36,000

$180,000 – $36,000 = $144,000

2

0.20

R1(P-F) = $28,800

$163,000 – $28,800 = $115,200

3

0.20

R1(P-F) = $23,040

$146,000 – $23,040 = $92,160

4

0.20

R1(P-F) = $18,432

$129,000 – $18,432 = $73,728

5

0.20

R1(P-F) = $14,746

$112,000 – $14,746 = $58,982

6

0.20

R1(P-F) = $11,796

$95,000 – $11,796 = $47,186

7

0.20

R1(P-F) = $9,437

$78,000 – $9,437 = $37,749

8

0.20

R1(P-F) = $7,549

$61,000 – $7,549 = $30,199

9

0.20

R1(P-F) = $3,199

$44,000 – $3,199 = $27,000

Note that the initial book value is the purchase price, but the final book value may be above the

salvage value, but never below.

3 – 3

4. An excavator has an initial cost of $150,000 and an estimated useful life of ten years. The

salvage value after ten years of use is estimated to be $40,000.

a. What is the book value at the end of the fifth year, if you use the straight-line method

of depreciation accounting?

Straight Line

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

$150,000

1

0.100

$11,000

$139,000

2

0.100

$11,000

$128,000

3

0.100

$11,000

$117,000

4

0.100

$11,000

$106,000

5

0.100

$11,000

$95,000

6

0.100

$11,000

$84,000

7

0.100

$11,000

$73,000

8

0.100

$11,000

$62,000

9

0.100

$11,000

$51,000

10

0.100

$11,000

$40,000

Note that the initial book value is the purchase price, and the final book value is the salvage value.

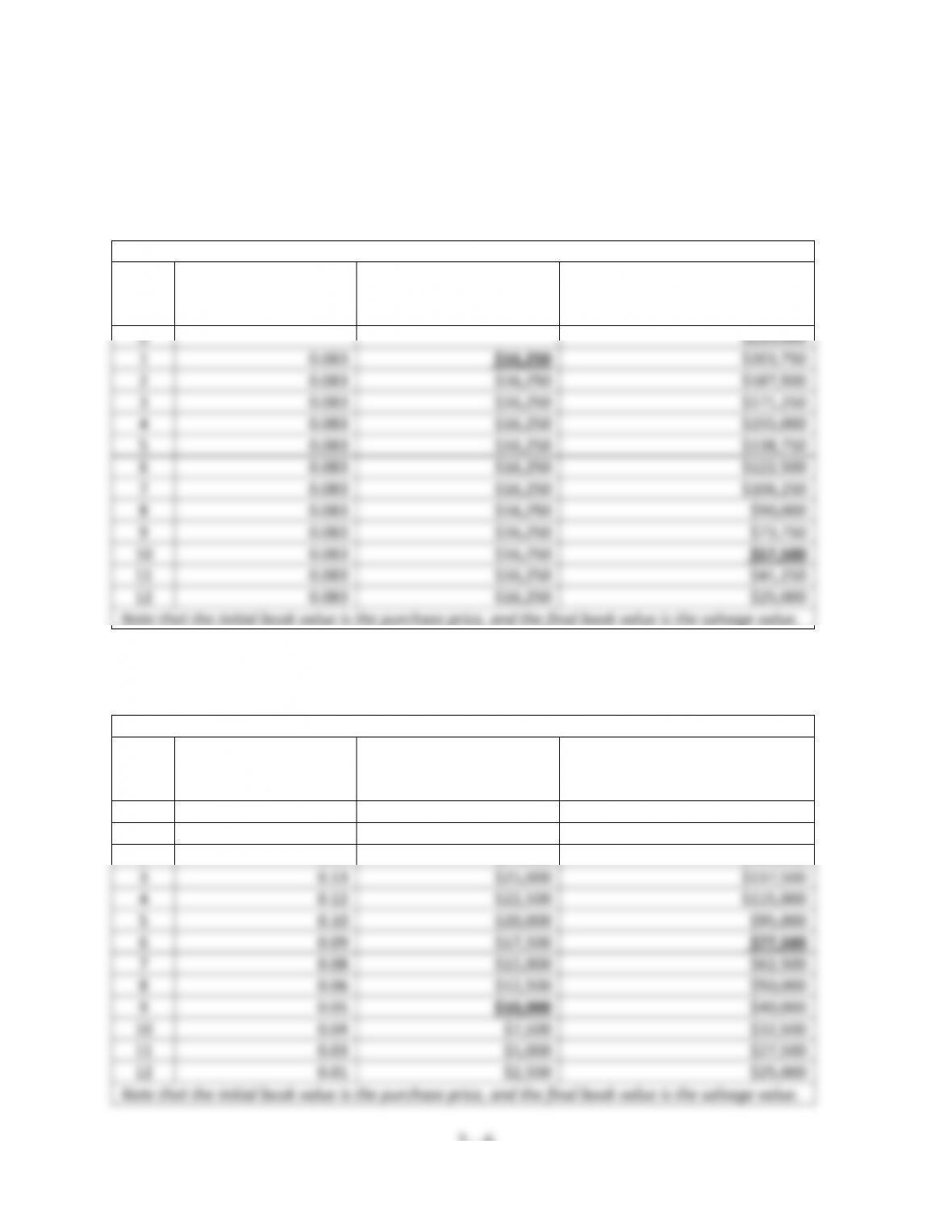

b. What is the book value at the end of the fifth year, if you use the sum-of-the-year

method of depreciation accounting?

SOY

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

$150,000

1

0.18

$20,000

$130,000

2

0.16

$18,000

$112,000

3

0.15

$16,000

$96,000

4

0.13

$14,000

$82,000

5

0.11

$12,000

$70,000

6

0.09

$10,000

$60,000

7

0.07

$8,000

$52,000

8

0.05

$6,000

$46,000

9

0.04

$4,000

$42,000

10

0.02

$2,000

$40,000

Note that the initial book value is the purchase price, and the final book value is the salvage value.

3 – 4

c. What is the book value at the end of the fifth year, if you use the double declining-

balance method of depreciation accounting?

2.0 Declining Balance

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

$150,000

1

0.20

$30,000

$120,000

2

0.20

$24,000

$96,000

3

0.20

$19,200

$76,800

4

0.20

$15,360

$61,440

5

0.20

$12,288

$49,152

6

0.20

$9,152

$40,000

7

0.20

$-

$40,000

8

0.20

$-

$40,000

9

0.20

$-

$40,000

10

0.20

$-

$40,000

Note that the initial book value is the purchase price, but the final book value may be above the

salvage value, but never below.

3 – 5

5. A contractor purchased a crane for $460,000 and plans to use the crane for eight years, at

which time she plans to sell the crane for 10% of its acquisition cost. The contractor is

considering using either the sum-of-the-years method of depreciation accounting or the

double declining-balance method of depreciation accounting.

a. If the contractor uses the sum-of-the-years method of depreciation accounting, what

will be the book value of the crane after two years of use?

SOY

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

$460,000

1

0.22

$92,000

$368,000

2

0.19

$80,500

$287,500

3

0.17

$69,000

$218,500

4

0.14

$57,500

$161,000

5

0.11

$46,000

$115,000

6

0.08

$34,500

$80,500

7

0.06

$23,000

$57,500

8

0.03

$11,500

$46,000

Note that the initial book value is the purchase price, and the final book value is the salvage value.

b. If the contractor uses the double declining-balance method of depreciation

accounting, what will be the book value of the crane after two years of use?

2.0 Declining Balance

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

$460,000

1

0.25

$115,000

$345,000

2

0.25

$86,250

$258,750

3

0.25

$64,687

$194,063

4

0.25

$48,516

$145,547

5

0.25

$36,387

$109,160

6

0.25

$27,290

$81,870

7

0.25

$20,467

$61,403

8

0.25

$15,351

$46,052

Note that the initial book value is the purchase price, but the final book value may be above the

salvage value, but never below.

3 – 6

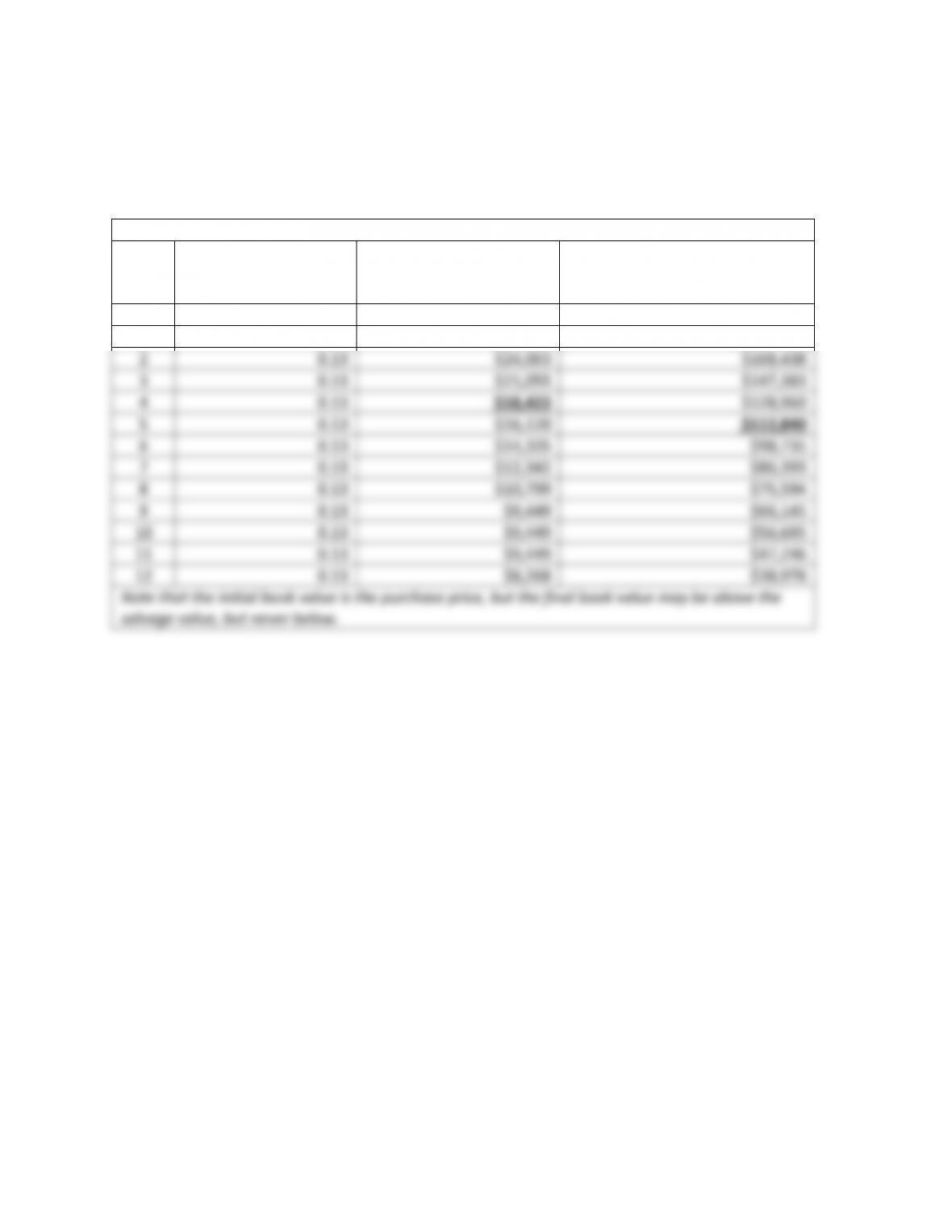

6. A grader has an initial cost of $220,000 and an estimated useful life of 12 years. The salvage

value after 12 years of use is estimated to be $25,000.

a. What is the annual depreciation amount, if the straight-line method of depreciation

accounting is used?

b. What is the book value after ten years, if the straight-line method of depreciation

accounting is used?

Straight Line

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

$220,000

1

0.083

$16,250

$203,750

2

0.083

$16,250

$187,500

3

0.083

$16,250

$171,250

4

0.083

$16,250

$155,000

5

0.083

$16,250

$138,750

6

0.083

$16,250

$122,500

7

0.083

$16,250

$106,250

8

0.083

$16,250

$90,000

9

0.083

$16,250

$73,750

10

0.083

$16,250

$57,500

11

0.083

$16,250

$41,250

12

0.083

$16,250

$25,000

Note that the initial book value is the purchase price, and the final book value is the salvage value.

c. What is the annual depreciation amount in the ninth year, if the sum-of-the-years

method of depreciation accounting is used?

d. What is the book value at the end of the sixth year, if the sum-of-the-years method of

depreciation accounting is used?

SOY

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

$220,000

1

0.15

$30,000

$190,000

2

0.14

$27,500

$162,500

3

0.13

$25,000

$137,500

4

0.12

$22,500

$115,000

5

0.10

$20,000

$95,000

6

0.09

$17,500

$77,500

7

0.08

$15,000

$62,500

8

0.06

$12,500

$50,000

9

0.05

$10,000

$40,000

10

0.04

$7,500

$32,500

11

0.03

$5,000

$27,500

12

0.01

$2,500

$25,000

Note that the initial book value is the purchase price, and the final book value is the salvage value.

3 – 7

e. What is the annual depreciation amount in the fourth year, if the 1.5 declining-

balance method of depreciation accounting is used?

f. What is the book value at the end of the fifth year, if the 1.5 declining-balance

method of depreciation accounting is used?

1.5 Declining Balance

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

$220,000

1

0.13

$27,500

$192,500

2

0.13

$24,063

$168,438

3

0.13

$21,055

$147,383

4

0.13

$18,423

$128,960

5

0.13

$16,120

$112,840

6

0.13

$14,105

$98,735

7

0.13

$12,342

$86,393

8

0.13

$10,799

$75,594

9

0.13

$9,449

$66,145

10

0.13

$9,449

$56,695

11

0.13

$9,449

$47,246

12

0.13

$8,268

$38,978

Note that the initial book value is the purchase price, but the final book value may be above the

salvage value, but never below.

3 – 8

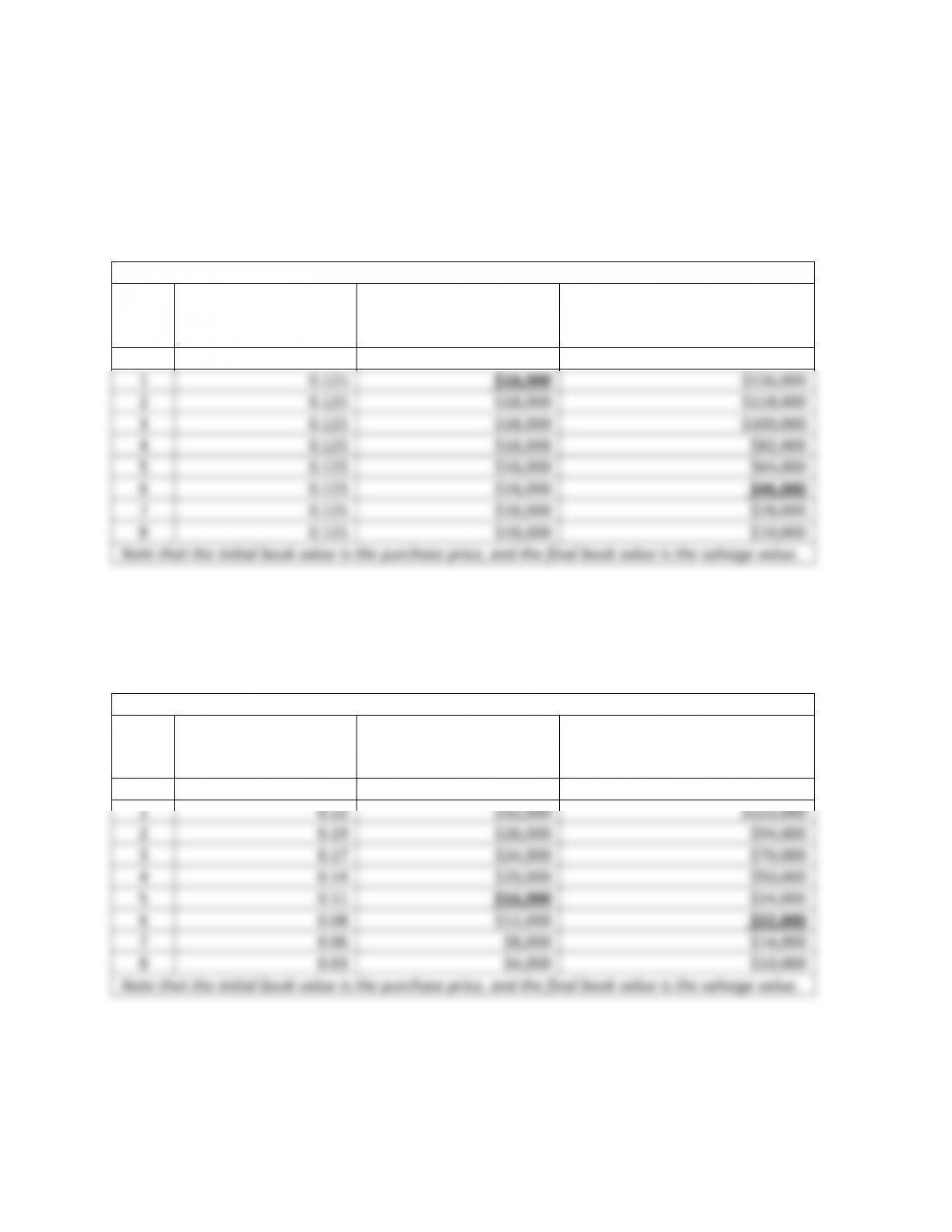

7. A loader has an initial cost of $154,000 and an estimated useful life of eight years. The

salvage value after eight years of use is estimated to be $10,000.

a. What is the annual depreciation amount, if the straight-line method of depreciation

accounting is used?

b. What is the book value after six years, if the straight-line method of depreciation

accounting is used?

Straight Line

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

$154,000

1

0.125

$18,000

$136,000

2

0.125

$18,000

$118,000

3

0.125

$18,000

$100,000

4

0.125

$18,000

$82,000

5

0.125

$18,000

$64,000

6

0.125

$18,000

$46,000

7

0.125

$18,000

$28,000

8

0.125

$18,000

$10,000

Note that the initial book value is the purchase price, and the final book value is the salvage value.

c. What is the annual depreciation amount in the fifth year, if the sum-of-the-years

method of depreciation accounting is used?

d. What is the book value at the end of the sixth year, if the sum-of-the-years method of

depreciation accounting is used?

SOY

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

$154,000

1

0.22

$32,000

$122,000

2

0.19

$28,000

$94,000

3

0.17

$24,000

$70,000

4

0.14

$20,000

$50,000

5

0.11

$16,000

$34,000

6

0.08

$12,000

$22,000

7

0.06

$8,000

$14,000

8

0.03

$4,000

$10,000

Note that the initial book value is the purchase price, and the final book value is the salvage value.

3 – 9

e. What is the annual depreciation amount in the fourth year if the double declining-

balance method of depreciation accounting is used?

f. What is the book value at the end of the fifth year if the double declining-balance

method of depreciation accounting is used?

1.5 Declining Balance

After

Year

(m)

Annual Depreciation

Rate

(Rm)

Annual Depreciation

Amount

(Dm)

Book Value

(BVm)

0

$154,000

1

0.25

$38,500

$115,500

2

0.25

$28,875

$86,625

3

0.25

$21,656

$64,969

4

0.25

$16,242

$48,727

5

0.25

$12,182

$36,545

6

0.25

$9,136

$27,409

7

0.25

$6,852

$20,557

8

0.25

$5,139

$15,417

Note that the initial book value is the purchase price, but the final book value may be above the

salvage value, but never below.