Chapter 9

Answers to Review Problems

Finance For Executives – 4th Edition

1. Structure and characteristics of financial markets.

a.

In a rights offering, shares are issued exclusively to the firm’s existing shareholders, whereas in a

b.

In an underwritten issue, the investment bank buys the securities from the issuer and then sells

them to the public at its own risk (the bank acts as a dealer in this case), whereas in a

c.

The originating house is the investment bank that has initiated the issue, whereas the selling

d.

A seasoned issue refers to the issue of securities by a firm that has already issued similar

securities in the past, whereas a secondary distribution refers to the sale to the public of a

e.

Credit risk refers to the ability of a firm to service the bonds it has issued (pay interest and repay

f.

Investment grade bonds are bonds with a credit rating of AAA, AA, A, and BBB (Standard and

2. Rights issue.

a.

9-1

b.

The number of rights (N) required to buy one new share is five:

5

million10

million50

sharesnewofNumber

sharesdingtanoutsofNumber

rightsofNumberN

c.

The price will drop to $25 to reflect the fact that the share has gone ex-rights, that is, it entitles the

holder to buy new shares at $20. The ex-rights price is (see equation 9.2):

25$

6

150$

6

20$26$5

1N

pricenSubsriptiopriceonRightsN

pricerightsEx

d.

The value of one right is simply $1, the difference between the rights-on price ($26) and the

1$

6

6$

6

20$26$

1N

priceonSubscriptipricen0Rights

rightoneofValue

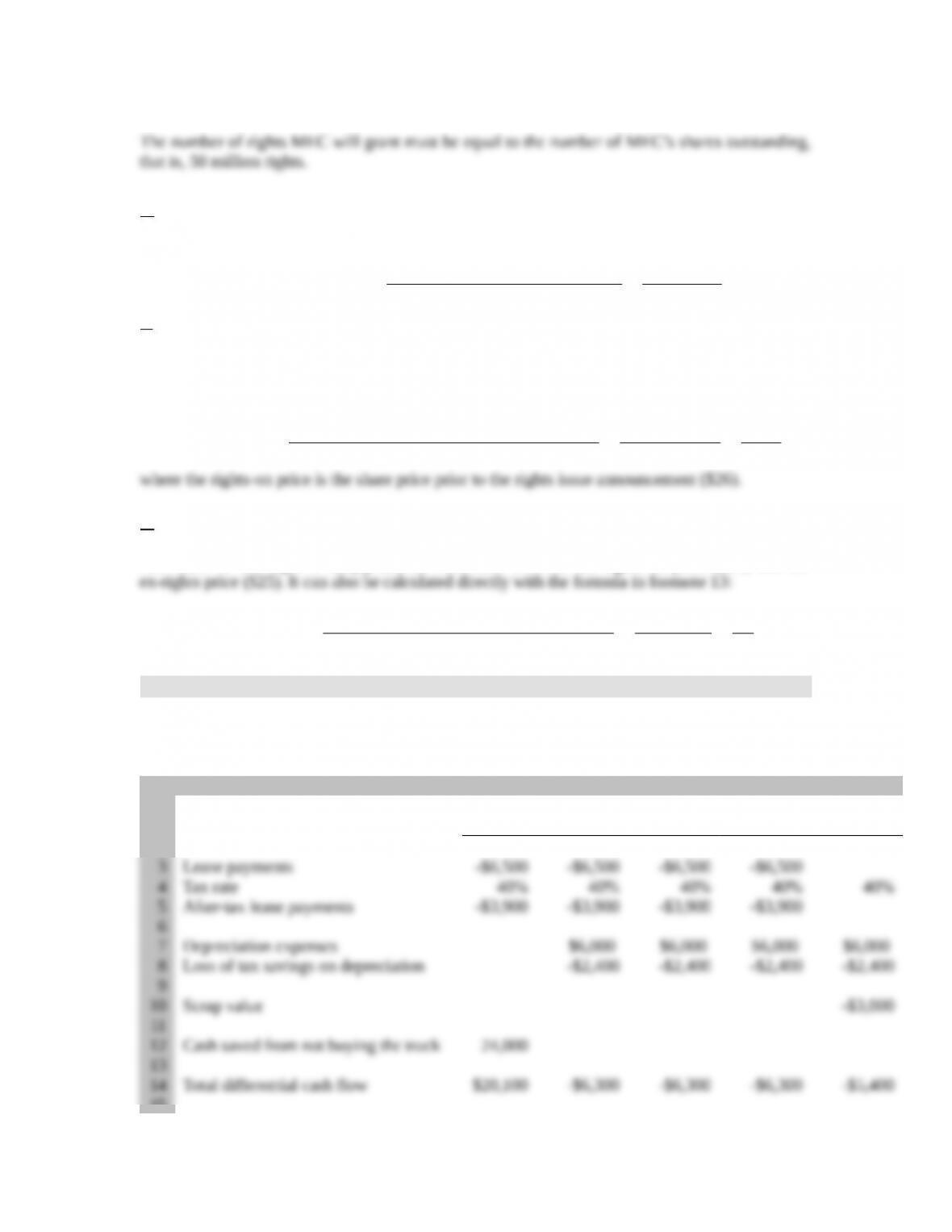

3. Leasing versus borrowing.

The relevant cash flows and the computation of the net present value of lease versus buy are

presented in a spreadsheet format.

A B C D E F

1Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

2

15

9-2

16 Cost of debt 6%

17

19

20 The values in rows 3, 4, 7, 10, 12, and 16 are data.

21 The formula in cell B5 is: =B3*(1-B4). Then copy formula in cell B5 to cells C5, D5, E5, and F5.

22 The formula in cell C8 is: =B7*B4.

23

The formula in cell B14 is: =B12+B10+B8+B5. Then copy formula in cell B14 to cells C14, D14, E14,

and F14.

24 The formula in cell B18 is: =B14 + NPV(B16,C14:F14).

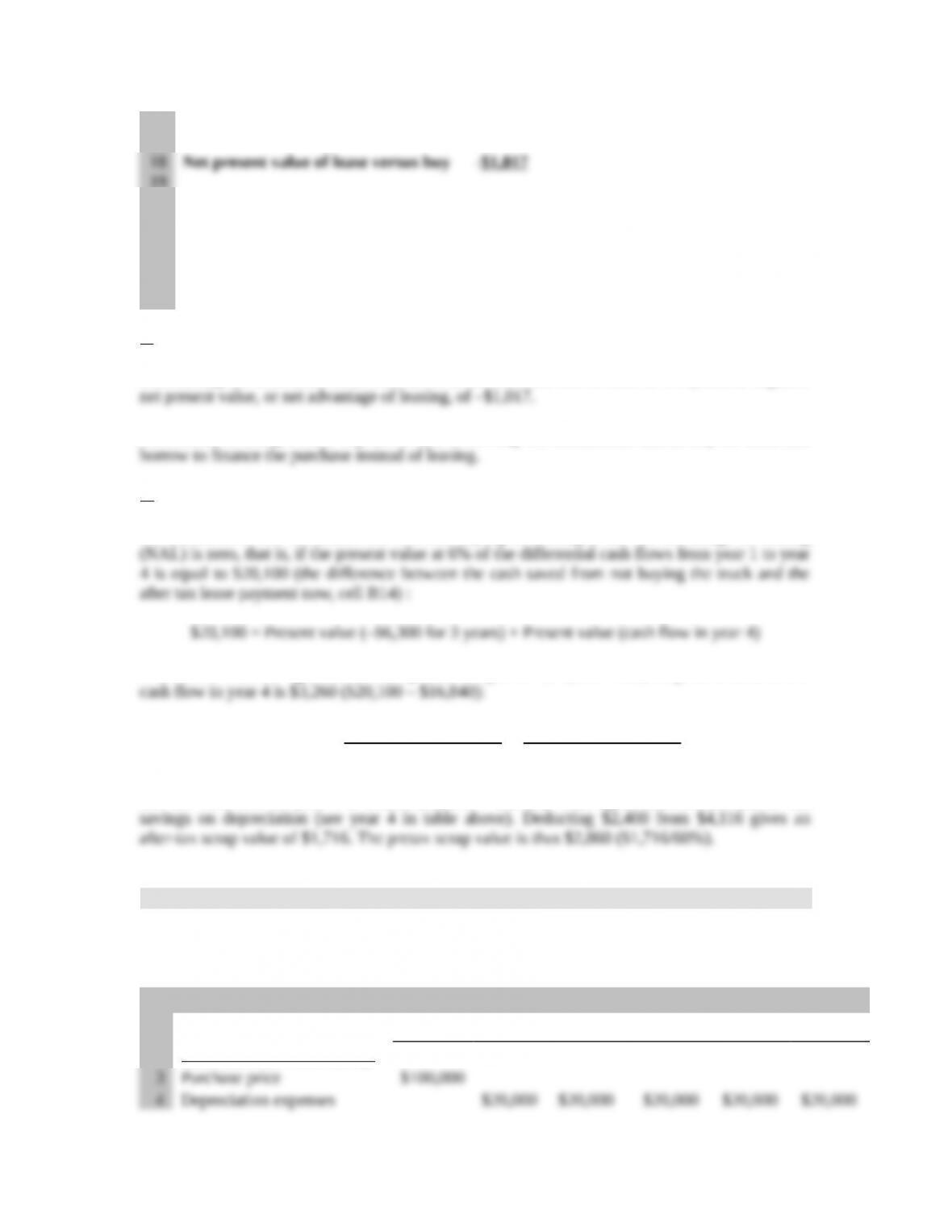

a.

Discounting the total differential cash flows at the after-tax cost of debt of 6% yields a negative

Conclusion: Leasing is more expensive than borrowing. OS Distributors should buy the truck and

b.

OS Distributors will be indifferent between buying or leasing if the net advantage of leasing

The first term on the right side of the equation is equal to –$16,840. Thus, the present value of the

1

3

1

1

5

16

The formula in cell C4 is: =SLN($B$3,0,5), where 5 is the depreciation life. Then copy formula in

cell C4 to cells D4, E4, F4, and G4.

17 The values in row 5 and 6 are data.

18

The formula in cell B7 is: =B5*(1-B6). Then copy formula in cell B7 to cells C7, D7, E7, F7, and

G7.

1

9The formula in cell C8 is: =C4*C6. Then copy formula in cell C8 to cells, D8, E8, F8, and G8.

20

The formula in cell B9 is: -B7-B8+B3. Then copy formula in cell B9 to cells C9, D9, E9, F9, and

G9.

21 The formula in cell B12 is: =B11*(1-B6).

22 The formula in cell B14 is: =B9 + NPV(B12,C9:G9).

2

3

2

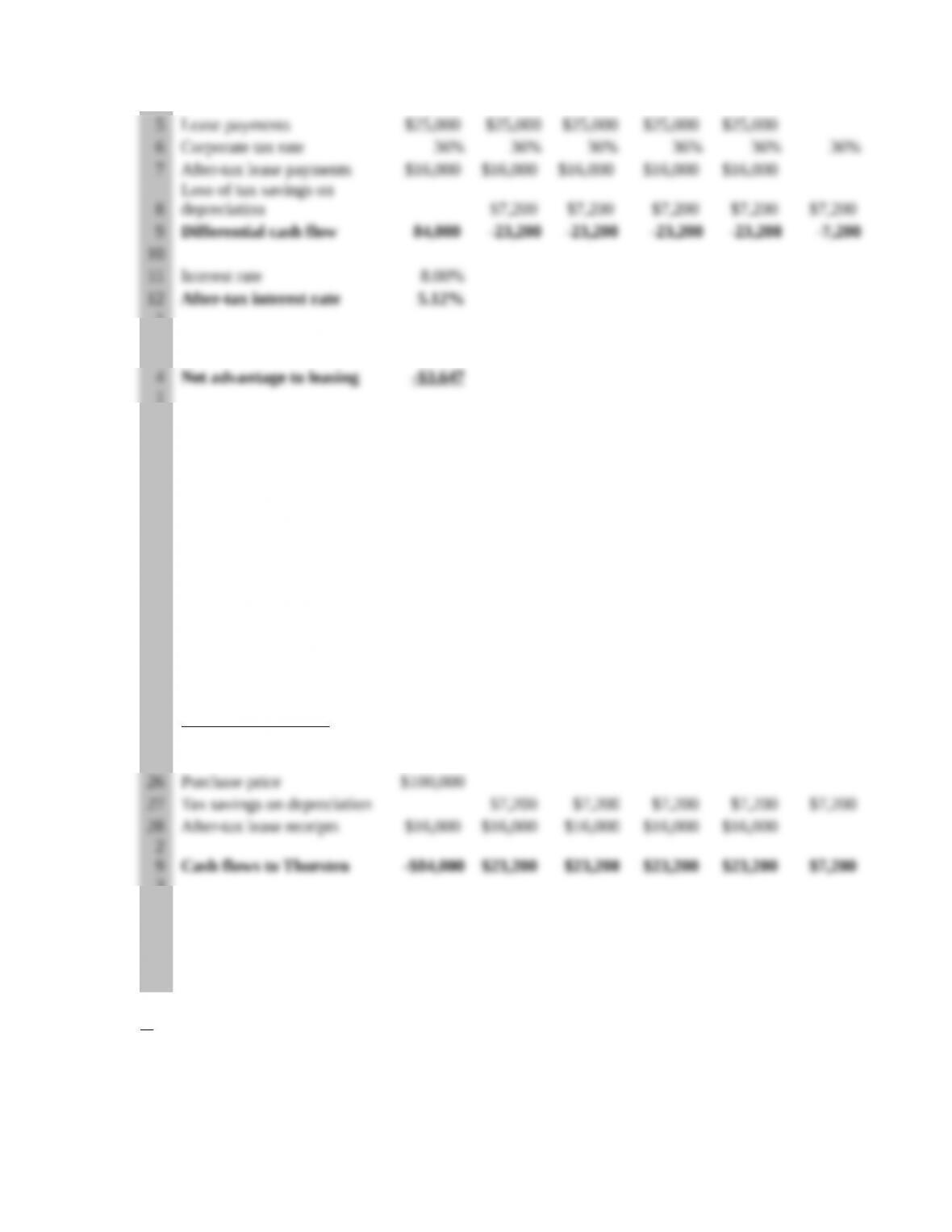

4Cash flows to Foster Now Year 1 Year 2 Year 3 Year 4 Year 5

2

5

3

0

3

1The values in rows 26, 27, and 28 are the same as in rows 3, 8, and 7 respectively.

3

2

The formula in cell B29 is: =B27+B28-B26. Then copy formula in cell B29 to cells C29, D29,

E29, F29, and G29.

a.

The net advantage to leasing is negative for Thorenberg Inc.: –$3,646. Thus, the firm should buy

rather than lease the equipment.

9-4

b.

The cash flows to the lessor (Thorsten) are just the opposite of those to the lessee (Thorenberg).

c.

Leasing cannot take place if the cash flows to the lessee and the lessor are exactly the opposite

and if their borrowing rate is the same. The leasing will take place only if any of these two

conditions is not met. That would happen if:

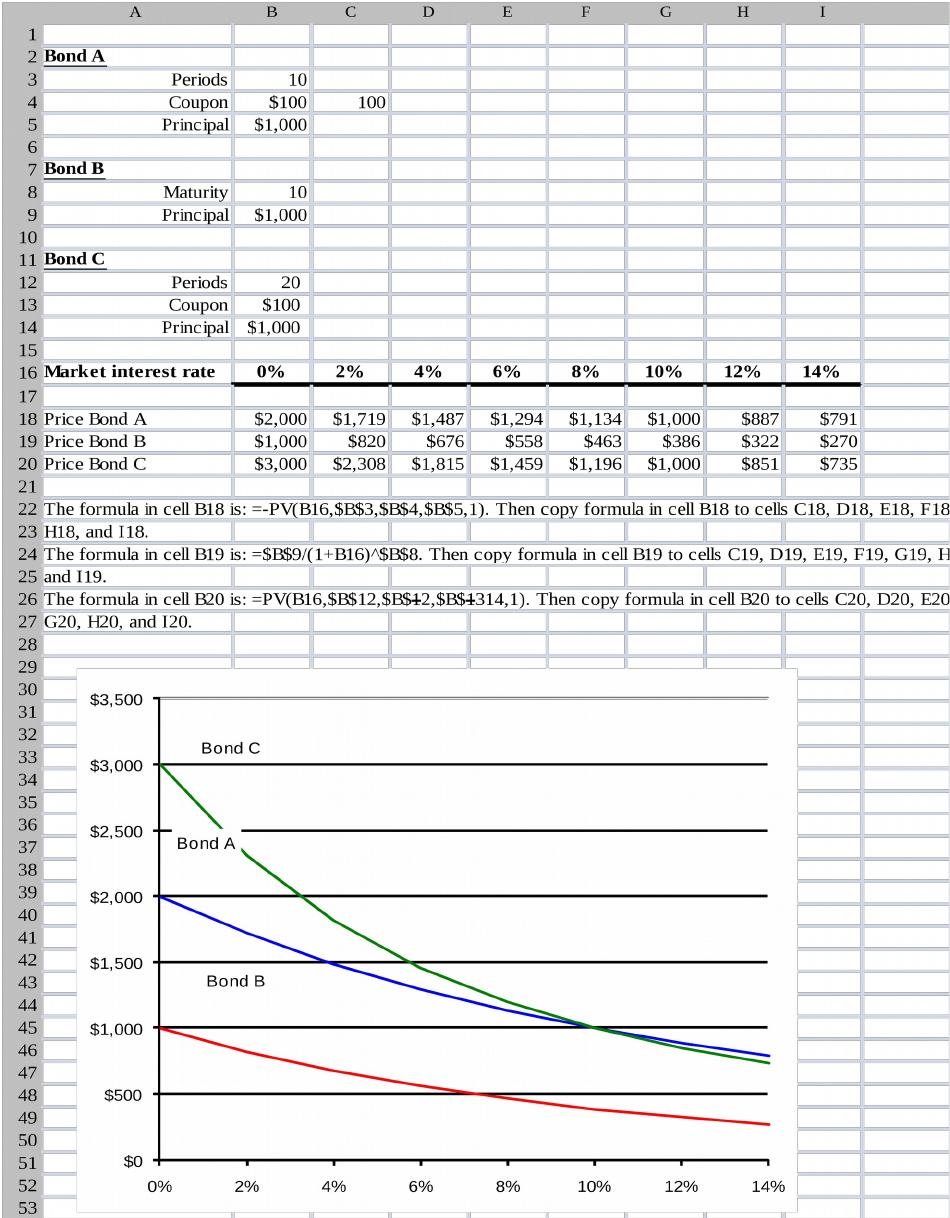

5. Bond valuation.

The market value of a bond is the present value of the bond’s future coupons and principal

repayment discounted at the market interest rate relevant to the risk and maturity of the bond:

T

D

T

1T

D

1T

2

D

2

D

1

)k1(

repaymentincipalPrCoupon

)k1(

Coupon

…..

)k1(

Coupon

)k1(

Coupon

valuemarketBond

where T is the maturity date of the bond.

The cash-flow stream of the coupons, assumed to be paid at the end of each year, and the

principal repayment for the three bonds are as follows:

End of Year 1 …. 9 10 11 ….. 19 20

The following spreadsheet and graph show the market price of the three bonds at increasing

interest rates. The PV function of the spreadsheet is used to compute the market price of the

9-5

Market interest rates increase (decrease) usually because the financial markets expect the inflation

rate to increase (decrease) or the credit risk of the borrower to increase (decrease). As a result, the

9-6

6. Bond valuation.

The rate on the new bond must be the same as the current market yield on the outstanding bond

since both bonds have the same maturity (10 years) and same credit risk (they are both issued by

The market yield on the outstanding bond is the internal rate of return of the bond (i.e., that

The cash-flow stream of coupons assumed to be paid at the end of each year, and principal

repayment of the outstanding bond are as follows:

Year 1 2 …. 9 10

The bond’s yield kD is the solution of the following equation:

1092 )1(

100,1$

)1(

100$

…..

)1(

100$

)1(

100$

065,1$

DDD

Dkkk

k

which solves for kD = 9%

A B C D E F G H

10

7. Valuation of bonds.

a.

9-7

Using a spreadsheet as in the chapter the market prices of the three bonds are calculated as

follows:

A B C D E F G

1

2Coupon bond

24

25 The formula in cell B16 is: =PV(B15,$B$3,$B$4,$B$5). Then copy formula in cell B16 to cell C16.

26 The formula in cell B17 is: =$B$9/ (1+B15)^$B$8. Then copy formula in cell B17 to cell C17.

27 The formula in cell B18 is: =$B$12/B15).

28 The formula in cell B21 is: =(C16-B16)B16. Then copy formula in cell B21 to cells B22 and B23.

29

b.

Bond values are below their face values because the market yield (7%) is above the coupon rate

c.

Because the convertible provides its holder with a valuable option (the option to convert the bond

d.

9-8

e.

See bond values at 7.5% in the spreadsheet above. Yield has gone up and, thus, bond values have

gone down. The most sensitive bond to a change in yield is the perpetual because it has the

8. Common stock valuation.

In an efficient market, the market value of a security is the present value of the cash-flow stream

The payments expected from Therol Co. to the current and future owners of a firm’s share of

Year-end 1 2 3

Year-end 4 5

Year-end 6 7 … t…

After the end of year 5, the dividend is expected to grow forever at a constant rate of six percent.

Since the dividend at that point in time is expected to be $2.350, the expected share price at the

The present value of the next five years’ expected dividends and of the expected share price at the

end of the fifth year is the price of the stock today S0:

5432

517.41$350.2$

12.1

098.2$

12.1

873.1$

12.1

615.1$

12.1

392.1$

The same calculations could have been done with a spreadsheet as follows:

A B C D E F G

1Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

Year-end

5

9-9

Expect growth rate

11

12 Data in rows 2 and 4 are given.

1

1

1

16

9. Growth stocks versus income stocks.

a.

Therol’s stock price, P0, is the value of a constant annuity equal to the expected dividend per

share discounted at the required rate of return of 10 percent. Since the firm pays out all of its

earnings, the expected dividend per share is $5.00 and the share price is:

10.

00.5$

0

P

$50.00

b.

If the firm plows back 40 percent of its earnings with an expected return of 10 percent, its

earnings will grow at a rate of 10 percent .40 = 4 percent. So will its dividend per share, which

04.10.

00.3$

0

P

$50.00

The stock price is the same as the one found in the previous question. This should not come as a

surprise since Therol would reinvest earnings at a rate which is the same as the 10 percent rate

c.

9-10

If the return on 40 percent of earnings is 15 percent instead of 10 percent, then dividends can be

06.10.

00.3$

0

P

$75.00

The $25.00 difference in stock price is the present value of the extra cash-flow returns provided

by the new investments made by the firm out of retained earnings. It is the result of expectations

10. Valuation of preferred shares and common stocks.

a.

Value of the preferred =

51.46$

086.0

4$

b.

The yield of 8.60%, which we took to estimate the value of the preferred, must overestimate the

c.

A B C D E F

1Now

Year-end

1

Year-end

2

Year-end

3

Year-end

4

9

10

The formula in cell C3 is: =B3*(1+C2). The formula in cell D3 is: =C3*(1+D2). Then

copy formula in D3 to cells E3 and F3.

11 The formula in cell F4 is: =F3*(1+F2)/(B6-F2).

12 The formula in cell C5 is: =C3+C4. Then copy formula in C5 to cells D5, E5, and F5.

13 The formula in cell B8 is: =NPV(B6,C5:F5).

14

d.

The observed market price of $53.24 is 5.3% higher than the estimated value of $50.56. This can

be interpreted as follows. If we assume that the estimated value is “correct,” then the shares are

9-11