7. Financial deals.

a.

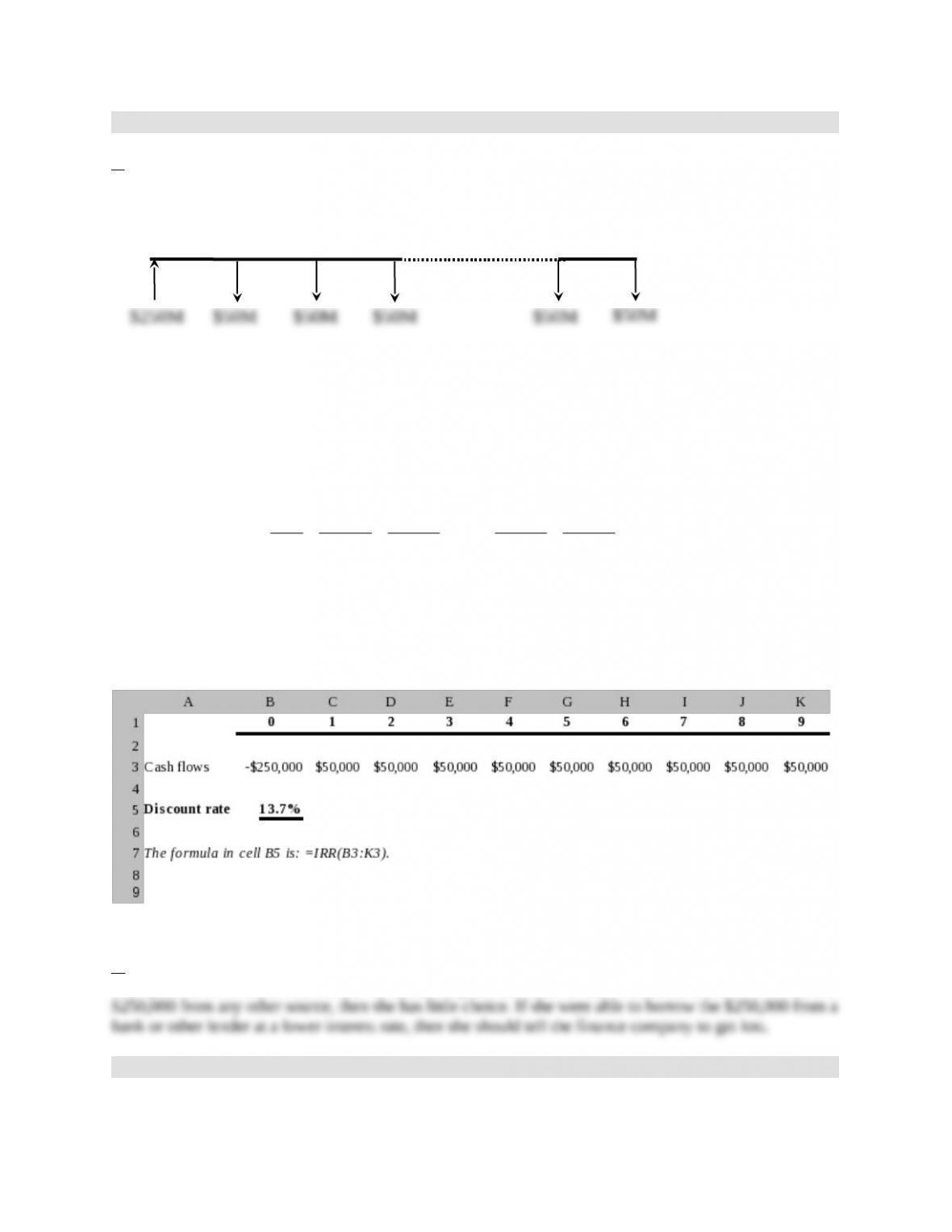

Time line:

The objective is to compute the discount rate implicit in the proposed “deal.” The aunt would receive

$250,000 now [present value] and give up $50,000 per year [annuity] for the next 9 years.

Using a calculator

The implicit discount rate k is the solution of:

9832

)k1(

1

)k1(

1

……

)k1(

1

)k1(

1

k1

1

000,50$000,250$

A trial-and-error calculation will show that the discount rate would be 13.7%.

Using a spreadsheet

b.

The question is whether this would be satisfactory for the aunt. If she would not be able to obtain the

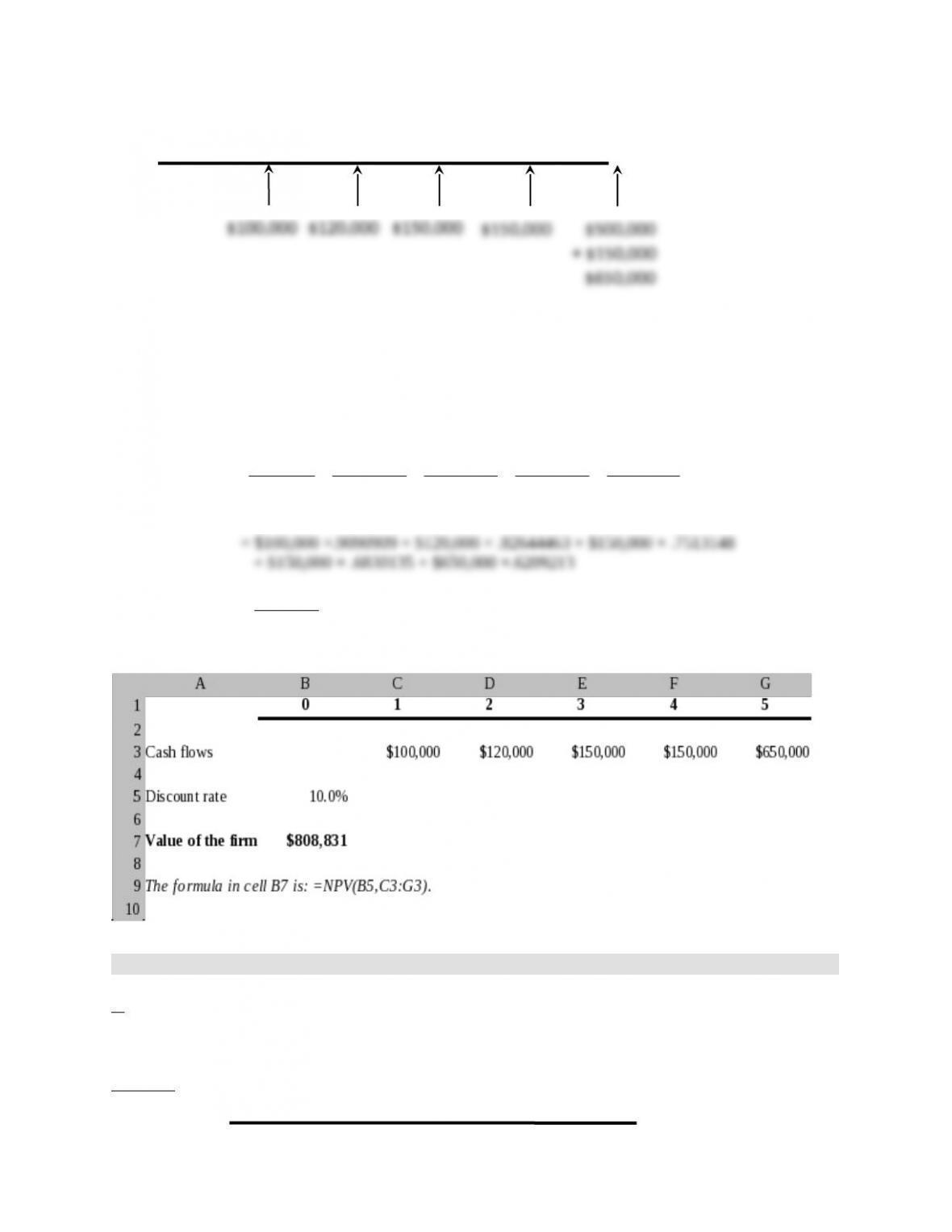

8. Value of a firm.

Time line:

6-1

19

320

m

8

m

m

m

The value of the firm is the present value of this series of cash flows discounted at 10 percent.

Using a calculator

Value of the firm =

5432

)010.1(

000,650$

)10.01(

000,150$

)10.01(

000,150$

)10.01(

000,120$

10.01

000,100$

= $808,831

Using a spreadsheet

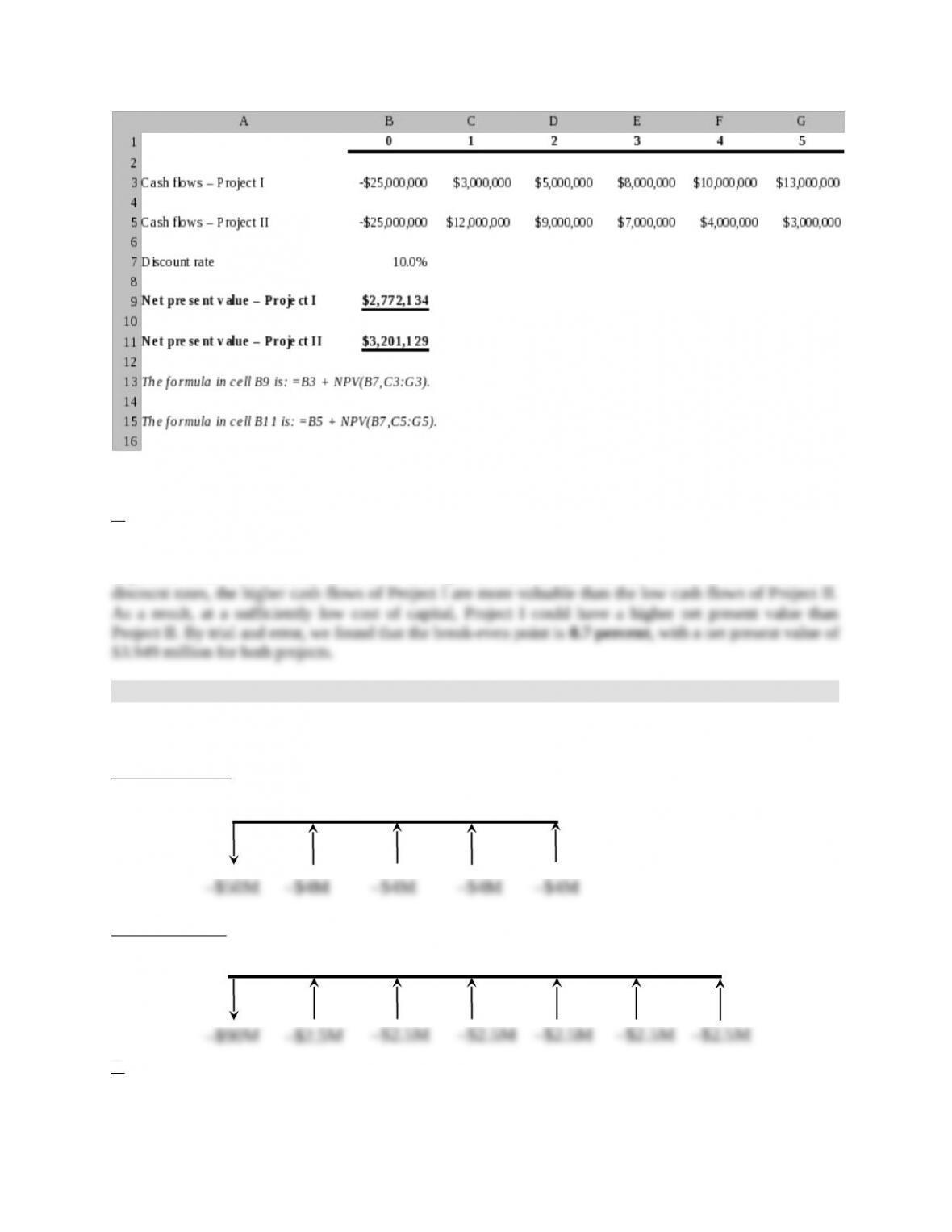

9. Competing investment projects.

a.

Time lines:

Project I

6-2

1 432 50

1 432 50

Project II

Using a calculator

5432

)10.01(

M13$

)10.01(

M10$

)10.01(

M8$

)10.01(

M5$

10.01

M3$

M25$)I(NPV

5432

)10.01(

M3$

)10.01(

M4$

)10.01(

M7$

)10.01(

M9$

10.01

M12$

M25$)II(NPV

Using a spreadsheet

6-3

1 432 50

Project II must be preferred to Project I since its net present value is higher.

b.

It is not necessarily the case that Project II would be always better than Project I when the cost of capital

changes from 10 percent. Since the cash flows increase in size over time for Project I, they are worth less

in present value terms than the cash flows of Project II when the discount rate increases. However, at low

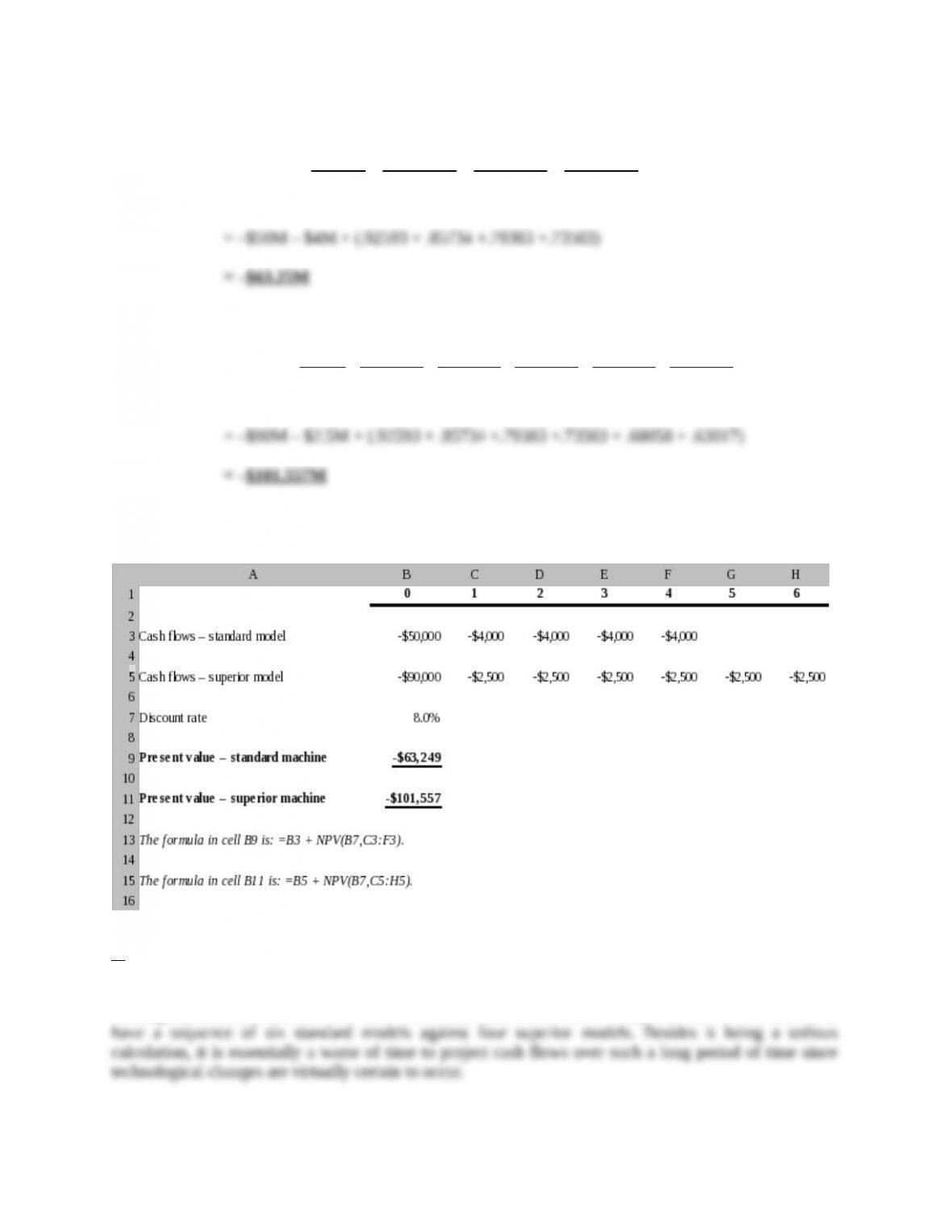

10. Comparing projects with unequal economic life.

Time lines:

Standard Model

Superior Model

a.

Using a calculator

6-4

1 432 50

14

3

2

6

0

PV(Standard) =

432

)08.01(

M4$

)08.01(

M4$

)08.01(

M4$

08.01

M4$

M50$

PV(Superior) =

65432

)08.01(

M5.2$

)08.01(

M5.2$

)08.01(

M5.2$

)08.01(

M5.2$

)08.01(

M5.2$

08.01

M5.2$

M90$

Using a spreadsheet

b.

The cash flows obviously cannot be directly compared because the standard model would have to be

replaced at the end of the fourth year whereas the superior model would still have two years before

needing replacement. In order to be able to evaluate them on the basis of equal lives, one would have to

6-5

c.

The constant annuity-equivalent cash flow cost of each model [at an 8 percent discount rate], using the

following equation from the appendix of the chapter:

Constant annuity-equivalent cash flow

factordiscountAnnuity

flowcashoriginalofvalueesentPr

one.

Annuity discount factor

k

k

N

)1(

1

1

where k is the cost of capital (8 percent for Rollon) and N is the useful life of the equipment (4 years for

the standard model and 6 years for the superior model).

Applying the formula, we get:

Annuity discount factor standard

312.3

08.

)08.1(

1

14

Annuity discount factor superior

623.4

08.

)08.1(

1

1

6

and

312.3

24 9,63$

Constant annuity-equivalent cash flow superior

623.4

557,101$

= –$21,968

d.

On the basis of expected costs, the company should purchase the standard model. This may also be

6-7