Chapter 6

Answers to Review Problems

Finance For Executives – 4th Edition

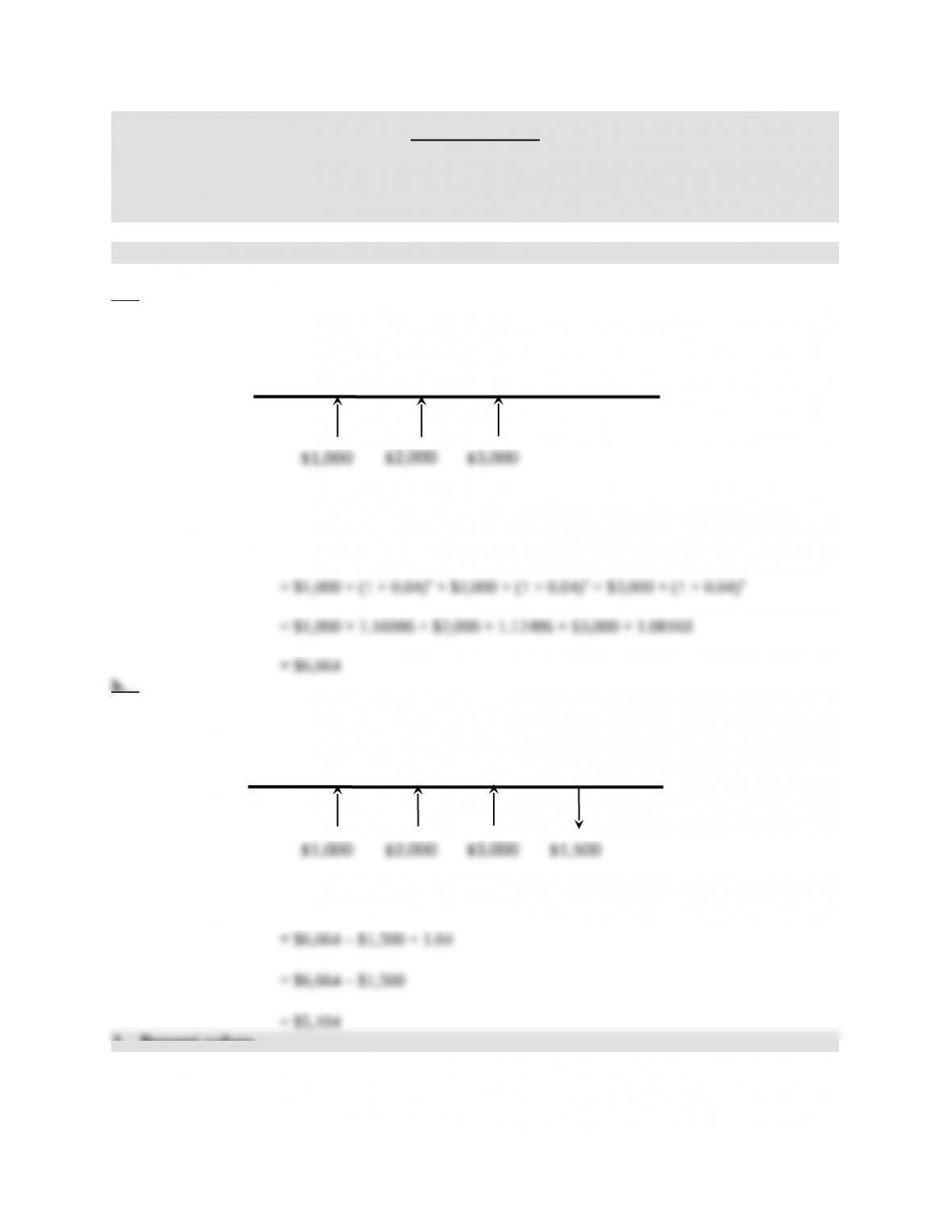

1. Future values.

a.

Time line:

Value at year-end 5 = FV($1,000)4 + FV($2,000)3 + FV($3,000)3 – FV($1,500)1

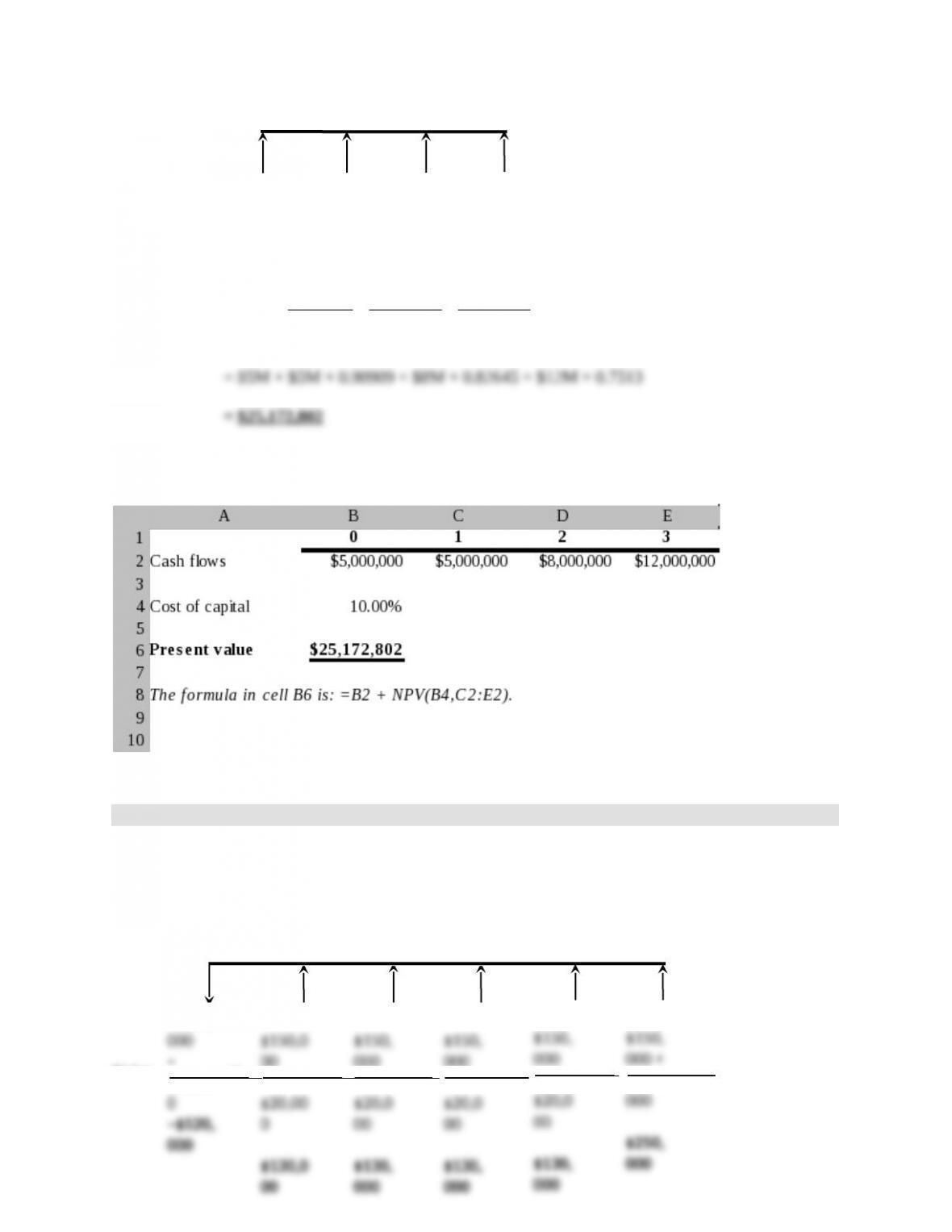

2. Present values.

Time line:

1 432 50

1 320

Using a calculator

Contract value =

32

)10.01(

M12$

)10.01(

M8$

)10.01(

M5$

M5$

Using a spreadsheet

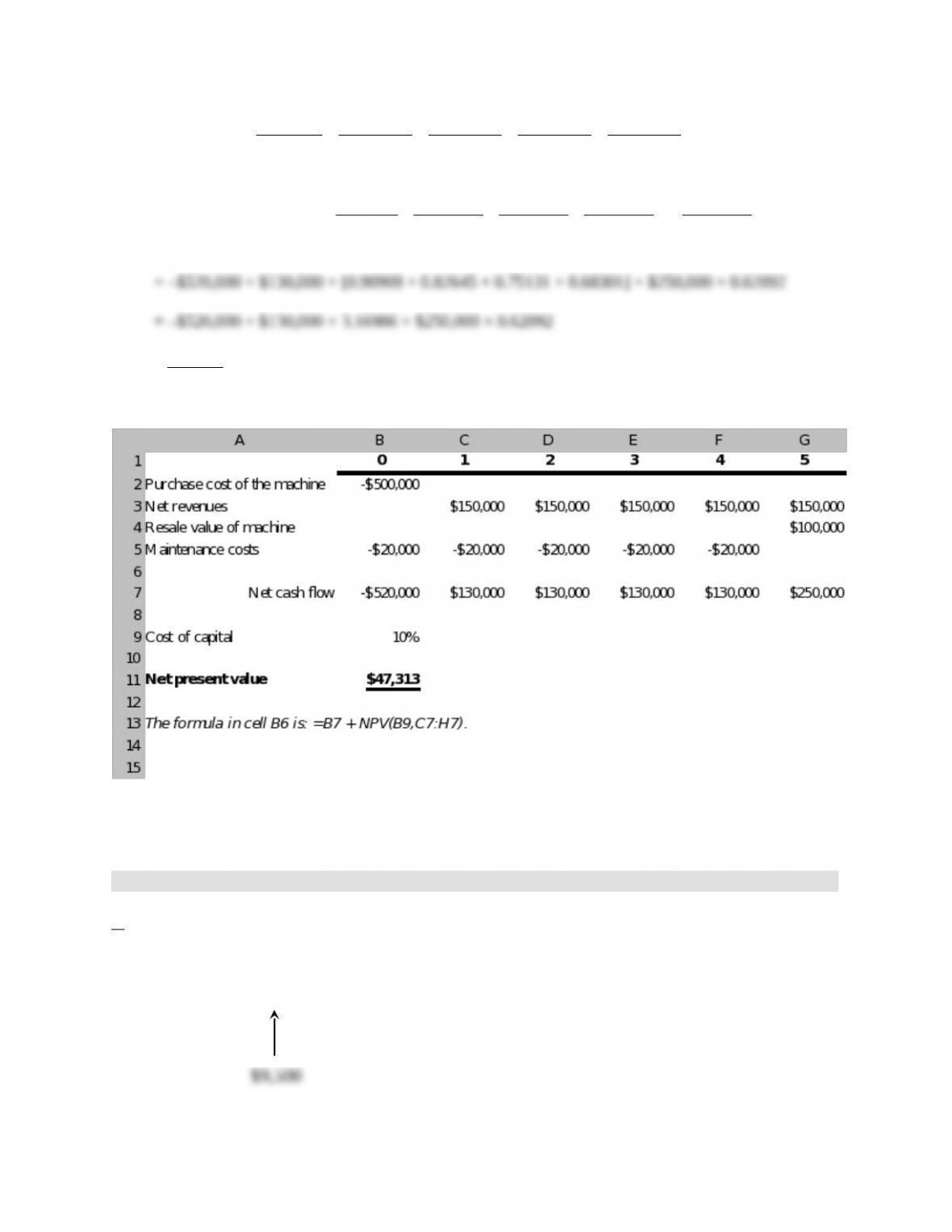

3. Present values.

The investment is worth undertaking if its net present value is positive.

Time line:

Using a calculator

$5M

$5M

$8M

$12M

1 432 50

–$500,

–

$20,00

00

–

000

–

000

–

000

–

000 +

$100,

5432

)10.01(

000,250$

)10.01(

000,130$

)10.01(

000,130$

)10.01(

000,130$

)10.01(

000,130$

000,520$NPV

5432

)10.01(

000,250$

)10.01(

1

)10.01(

1

)10.01(

1

)10.01(

1

000,130$000,520$NPV

= $47,313

Using a spreadsheet

NPV is positive, so the machine should be purchased.

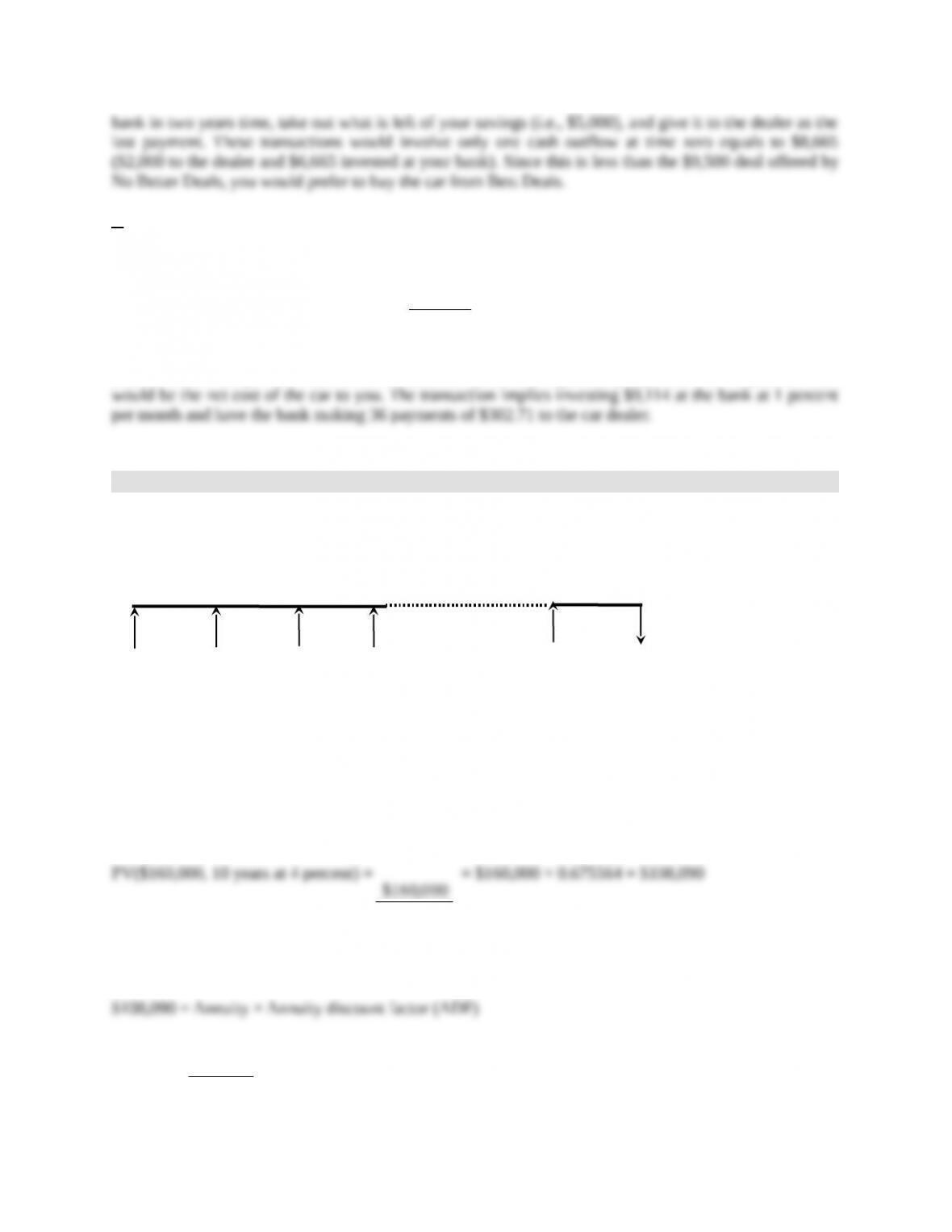

4. Buying a car.

a.

Time line of No Better Deals offer:

0

Time line of Best Deals offer:

The cash flows related to the two offers cannot be directly compared since they do not take place at the

same time. To make them comparable you have to imagine a financial transaction which, combined with

This financial transaction is straightforward: lend at 12 percent a $ amount at time zero, such that you will

2

)12.1(

000,6$

the Best Deals offer you would have to pay $4,000 to the dealer, get your car, and drive to your bank

where you would invest $5,237 at 12 percent. In two years time, you would go to your bank and take your

savings out. You would get exactly $6,000 that you would immediately give to Best Deals, as final

b.

Time line of New Best Deals offer:

0

1

2

We showed in part a. that the old Best Deals offer is equivalent to spending $8,783 at time zero. Using the

2

)12.1(

000,5$

12.1

000,3$

at the same time you get your car and pay $2,000 to the dealer. In one year time, you would go to the bank

and retrieve $3,000 that you would immediately turn to Best Deals. You would have to go again to the

0

1

2

0

1

2

c.

1. For No Better Deals, the present value of the 36 monthly payments must be equal to $10,000 at 0.5

percent per month. Since the present value of an annuity of $1 at 0.5 percent per period over 36 periods is

$, the monthly payments would have to be

22.304$

871.32

000,10$

.

2. The present value of 36 monthly payments of $302.71 when you can invest at 1 percent per month is

$9,114. This is the present value of 36 annuities of $302.71 at 1 percent per period over 36 periods. This

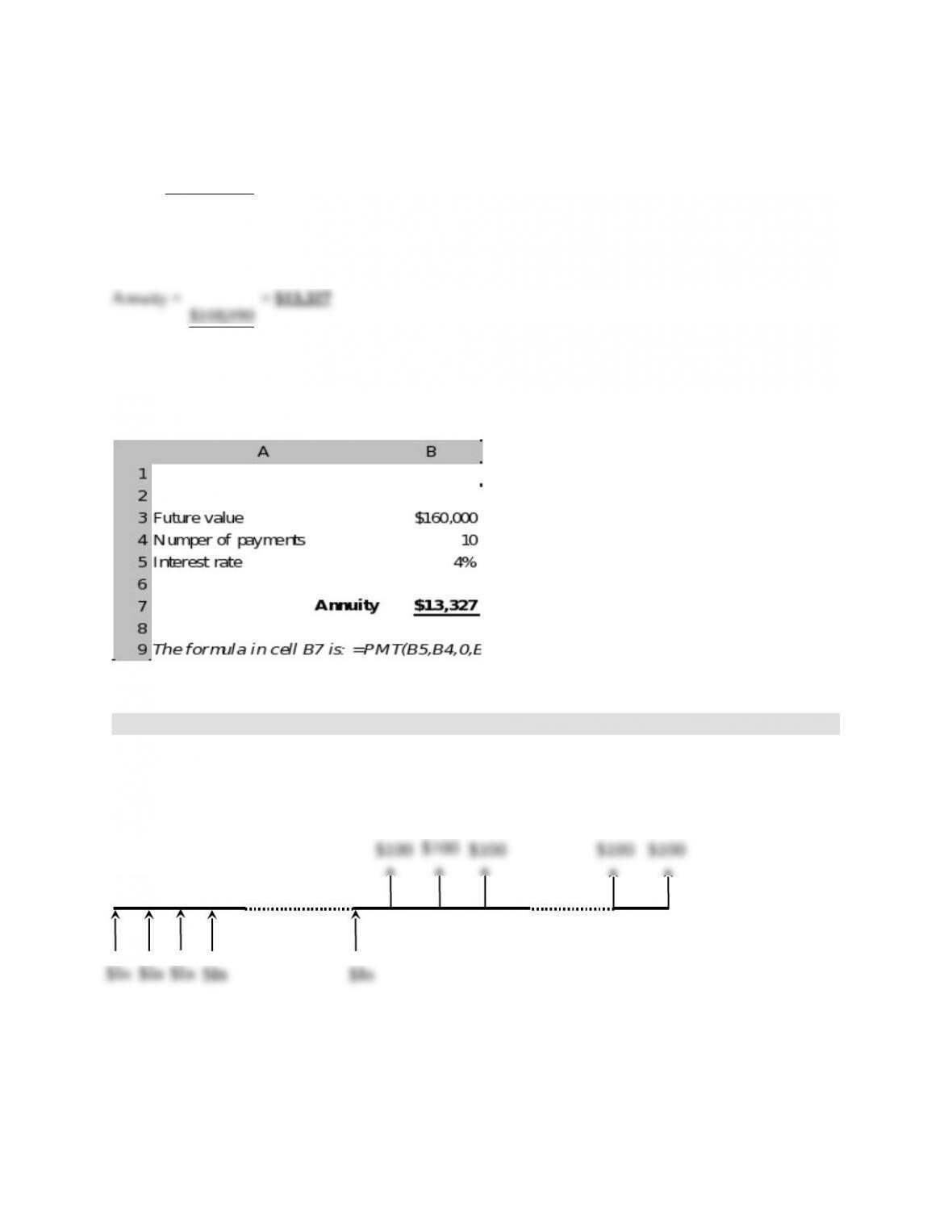

5. Saving for college.

Time line:

where X is the annual payment to the saving account.

Using a calculator

First, find the present value of $160,000 and second, using the annuity formula A6.1.2, compute the

annuity.

10

)04.01(

000,160$

From equation A6.1.2:

Annuity =

ADF

090,108$

19

32 10

0

$X $X $X $X $X $160,000

From Appendix 1:

11.8

04.

675564.01

ADF

So that:

11.8

090,108$

Using a spreadsheet

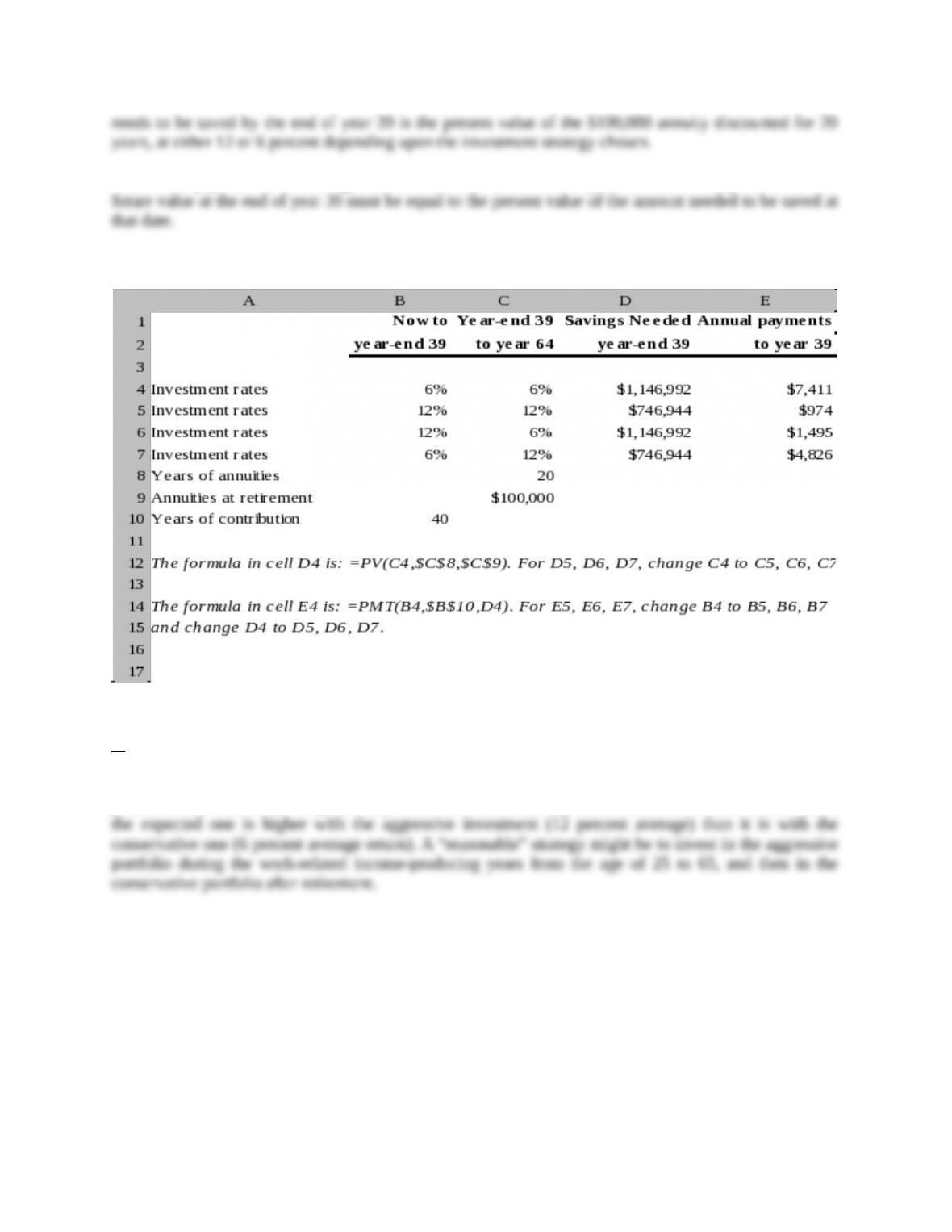

6. Saving for retirement.

a.

Time line ($ thousands):

where $In is the annual payment to the pension fund.

Using a calculator

To get $100,000 at the end of each year from the end of year 40 to the end of year 59, the amount that

0

1

2

3

39

40

41

42

58

59

The annual payment to the savings account from now to the end of year 39 is an annuity for which the

Using a spreadsheet

b.

The strategy to adopt depends upon your attitude towards risk. The 12 and 6 percent returns used in the

computations are based on historical average returns. These are returns that can be expected over a long

period of time. However, the probability that the investor will experience an actual return different from