8. The effect of the management of the operating cycle on the firm’s profitability.

a.

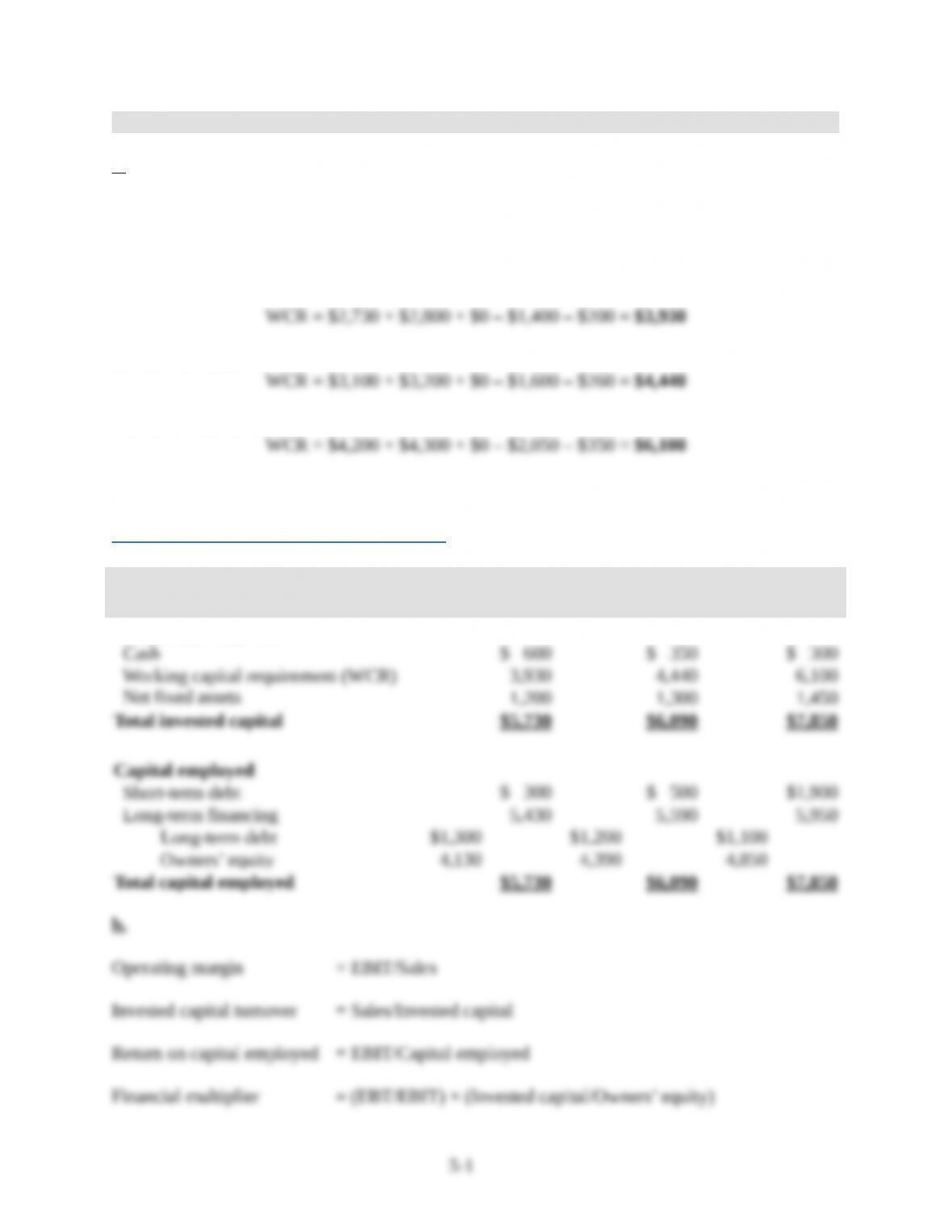

Working capital requirement (WCR) = Accounts receivable + Inventories + Prepaid expenses

– Accounts payable – Accrued expenses

December 31, 2008

December 31, 2009

December 31, 2010

Managerial balance sheets

in thousands

December 31,

2008

December 31,

2009

December 31,

2010

Invested capital

Cash

Working capital requirement (WCR)

Total invested capital

$5,730

$6,090

$7,850

Capital employed

Short-term debt

$ 300 $ 500 $1,900

Long-term financing

5,430

5,590

5,950

Long-term debt

$1,300 $1,200 $1,100

Owners’ equity

4,130 4,390 4,850

Total capital employed

$5,730

$6,090

$7,850

b.

Operating margin = EBIT/Sales

Invested capital turnover = Sales/Invested capital

5-1

Tax effect = EAT/EBT

Return on equity = EAT/Owners’ equity

2008

2009

2010

5-2

The relationship between these ratios and the firm’s return on equity is that ROE is simply equal

c.

Note the drastic increase of the return on equity which nearly doubles between 2008 and 2010,

The tax effect, which stayed between 0.59 to 0.61 (i.e., reducing the profitability by 41 to 39

The financial multiplier, which increased the return on invested capital by 15 percent in 2008,

increased it by 31 percent in 2010, thus improving the profitability of the firm. Had the return on

invested capital been 11.34 percent in 2010 as in 2008, the return on equity would have been

equal to 9.06 percent (11.34% 1.31 0.61), which indicates that the change in the financial

multiplier explains 22.35 percent of the change in the return on equity ([9.06% – 7.75%]/

[13.61% – 7.75%]). The increase in the financial multiplier was the result of the increase in the

The return on invested capital (ROIC), which increased drastically from 11.34 percent in 2008 to

17.20 percent in 2010, was the main driver of the increase of the firm’s profitability during that

d.

From the data on the industry, we can compute what Sentec’s working capital requirement would

have been at the end of 2010 if it had the same activity ratios as the average of its competitors,

Pro forma working capital requirement (WCR)12/31/10

5-3

365

salesNet

10

=

365

600,31$

30 days = $2,597

Inventories 12/31/10 =

8

sold goods ofCost

10

8

100,25$

$3,138

Accounts payable12/31/10 =

365

Purchases

10

365

sinventoriein Changesold goods ofCost

1010

=

365

)200,3$138,3($100,25$

33 days = $2,264

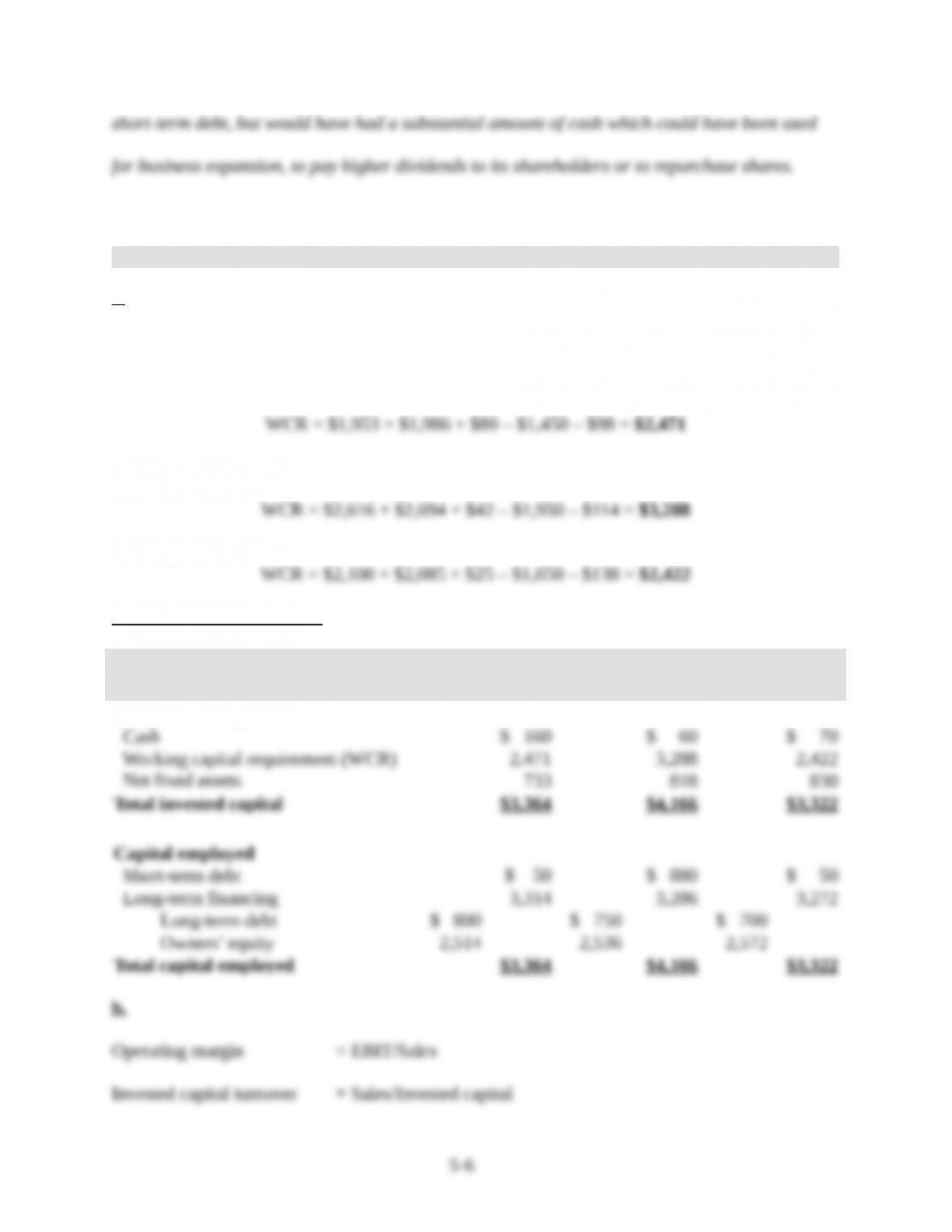

Working capital requirement (WCR) = Accounts receivable + Inventories + Prepaid expenses

– Accounts payable – Accrued expenses

Pro forma managerial balance sheet

in thousands December 31, 2010

Invested capital

Capital employed

Short-term debt

Long-term financing

5,950

Long-term debt

Owners’ equity

Total capital employed

$5,950

Note that the amount of long-term financing ($5,950) would have been higher than the

investment in fixed assets and in the operating cycle ($1,450 + $3,121 = $4,571). Sentec Inc.

would not have needed any short-term debt, and had $1,379 million (5,950 – $4,571) in cash.

The structure of the pro forma return on equity

1 If the interest charges to EBIT ratio is 4 percent, then the ratio EBT/EBIT is .96

Note the drastic impact of a better management of the operating cycle on the return on invested

capital, which would have jumped from 4.03 to 5.31. As a result, the return on invested capital

would have reached 22.7 percent and the return on equity 16.05 percent, instead of 17.2 percent

5-5

9. Seasonal business.

a.

Working capital requirement (WCR) = Accounts receivable + Inventories + Prepaid expenses

– Accounts payable – Accrued expenses

June 30, 2009

December 31, 2009

June 30, 2010

Managerial balance sheets

in thousands

June 30,

2009

December 31,

2009

June 30,

2010

Invested capital

6 Months to 6/30/2009

6 Months to 12/31/2009

6 Months to 6/30/2010

5-7

c.

Return on equity is higher in the second part of the year than in the first half (2.6 percent versus

1.3/1.4 percent) for the following reasons:

10. Self-sustainable growth rate.

a.

The five percent target growth rate would be attainable only if the firm’s self-sustainable growth rate is at least equal to 5 percent. Ambersome’s

self-sustainable rate can be computed as follows:

1 Since Ambersome has not debt, its earnings after tax is earnings before interest and tax (1-tax rate of 40 percent)

and owners’ equity = total assets.

b.

Ambersome would have to increase its asset turnover ratio or its profit margin so that its return

on equity is equal to at least 5 percent, which represents an increase of 93 percent (5%/2.59% –

c.

The firm’s return on equity, and as a result, its self-sustainable rate, would increase through debt

financing only if the rate at which the firm can borrow is lower than the return on assets. Since

5-8