Chapter 4

Answers to Review Problems

Finance For Executives – 4th Edition

1. Transactions.

2. Profits, losses, and cash flows.

A company can show a profit, while, during the same period, the cash flows from operating activities are

At the opposite, a firm can show a loss when its cash flows from operating activities is positive in two

cases:

a. The margin component of the operating cycle is negative and the working capital requirement

WCR CFOPE CFINV CFFIN

Owners’

Equity

3. Depreciation and cash flows.

Depreciation expense is not a cash transaction. Thus, before tax, depreciation expense has no impact on

the firm’s cash flows. Depreciation expense appears in the indirect approach to the cash-flow statement

in order to cancel out with the same amount that negatively affects earnings after tax.

Since depreciation expense is a tax deductible expense, the higher it is , the lower the tax bill and the

However, the statement may signify that an increase in the reported depreciation expense account reduces

4. Building a cash flow statement

a.

Receivables12/31/09 + Sales10 – Cash inflow from sales10 = Receivables12/31/10

Cash inflow from operations10 = Sales10– (Receivables’12/31/10 – Receivables12/31/09)

b.

Cash outflow from operations = Cash outflow from the purchase of material

Cash outflow from the purchase of material:

Payables12/31/09 + Purchases10 – Cash outflow from purchases10 = Payables12/31/10

Cash outflow from purchases10 = Purchases10 – (Payables12/31/10 – Payables12/31/09)

The material purchased in 2010 was either sold that year or went to the inventories:

Cash outflow from purchases10

Cash outflow from labor expenses:

Accrued expenses12/31/09 + Labor expenses10 – Cash outflow from labor expenses10

= Accrued expenses12/31/10

Cash outflow from labor expenses10 = Labor expenses10

– (Accrued expenses12/31/10 – Accrued expenses12/31/09)

Cash outflow from SG&A:

Prepaid expenses12/31/09 – SG&A expenses10 + Cash outflow from SG& expenses10

= Prepaid expenses12/31/10

Cash outflow from SG&A expenses10 = SG&A expenses10

+ (Prepaid expenses 12/31/10 – Prepaid expenses12/31/09)

Cash outflow from tax expenses10:

Cash outflow from operations10:

c.

NOCF10 = Cash inflow from operations10 – Cash outflow from operations10

Note that this is the same amount one would have found using equation 4.1:

change in working capital requirement in 2010.

Working capital requirement (WCR) = Accounts receivable + Inventories + Prepaid expenses

December 31, 2009:

December 31, 2010:

d.

Net fixed assets12/31/09 + Acquisitions10 – Disposals10 – Depreciation expenses10 = Net fixed

assets12/31/10

Since there was no disposal of fixed assets in 2010, the net cash flow from investing activities was equal

to the amount of acquisitions during that year.

Acquisitions10 = Net fixed assets12/31/10 – Net fixed assets12/31/09 + Depreciation expenses10

e.

Net cash flow from financing activities = Long-term borrowing + Short-term borrowing

+ Repayment of long-term debt + Interest payments + Dividends

f.

Total net cash flow = Net operating cash flow + Net cash flow from investing activities

+ Net cash flow from financing activities

which is, as expected, the same as the difference between the amount of cash held by the company at the

5. Two cash flow statements.

a.

Working capital requirement (WCR) = Accounts receivable + Inventories + Prepaid expenses

– Accounts payable – Accrued expenses

December 31, 2009:

December 31, 2010:

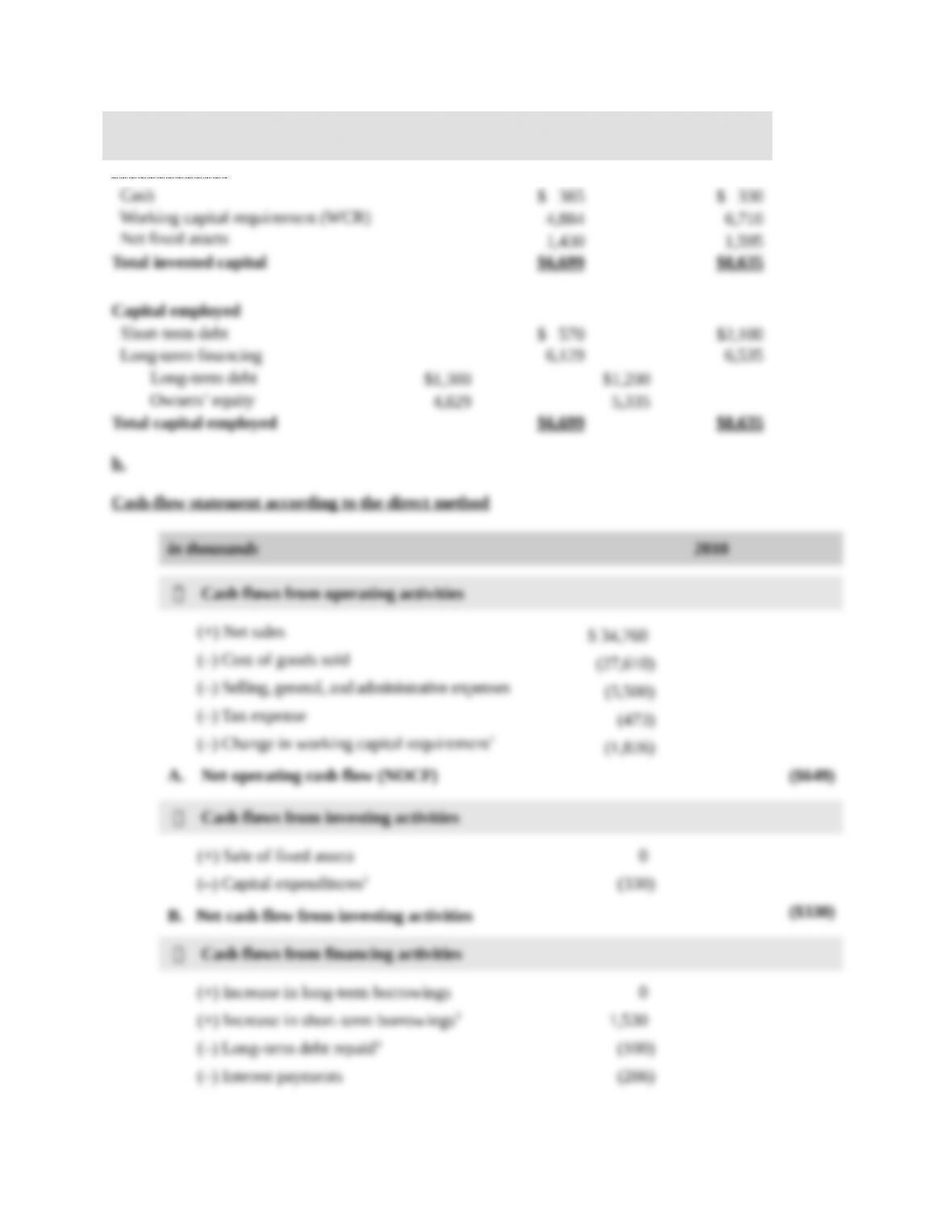

Managerial balance sheets

in thousands December 31,

2009

December 31,

2010

Invested capital

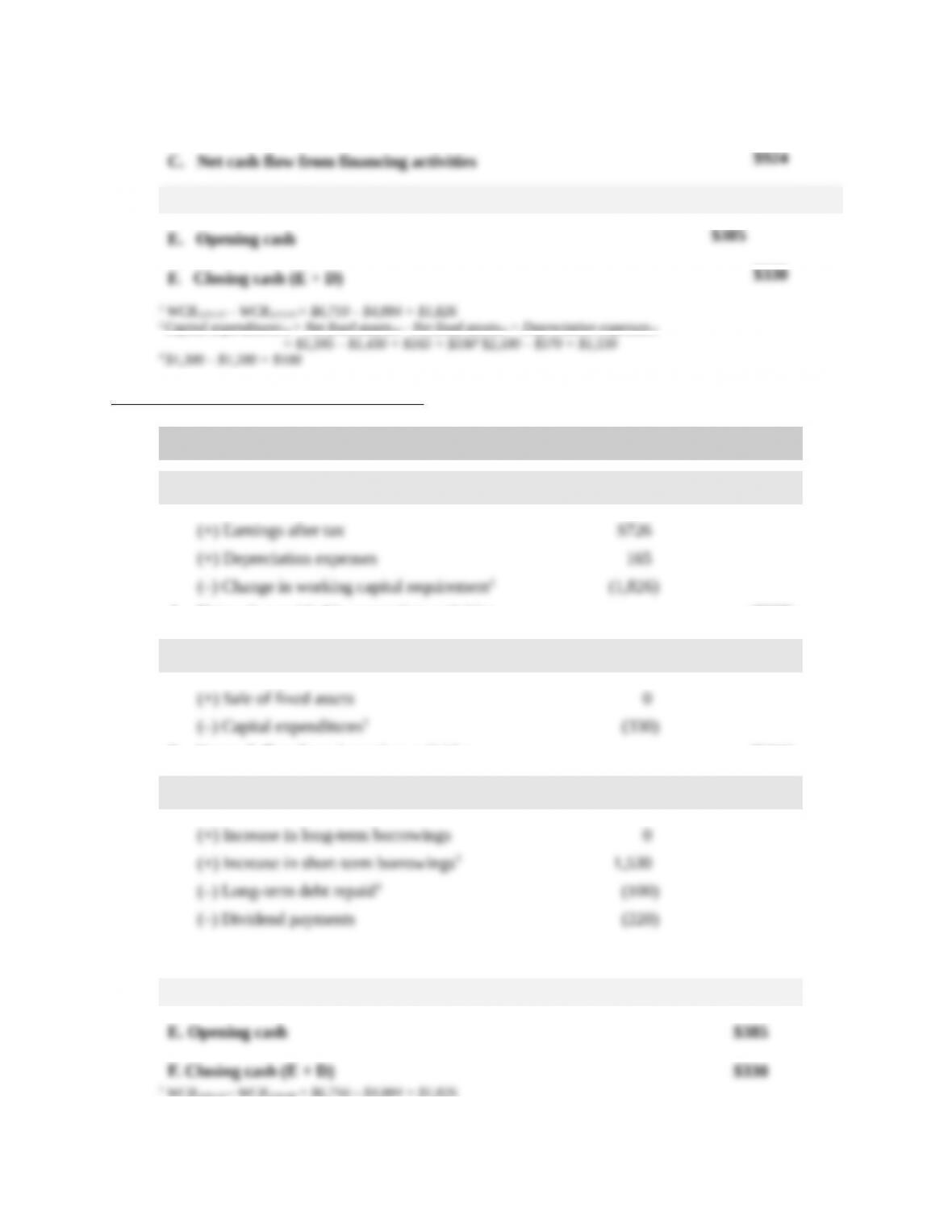

(–) Dividend payments (220)

D. Total net cash flow (A + B + C) ($55)

2 Capital expenditures10 = Net fixed assets10 – Net fixed assets09 + Depreciation expenses10

4 $1,300 – $1,200 = $100

Cash-flow statement according to FASB 95

in thousands 2010

Cash flows from operating activities

A. Net cash provided by operating activities ($935)

Cash flows from investing activities

B. Net cash flow from investing activities ($330)

Cash flows from financing activities

C. Net cash flow from financing activities $1,210

D. Total net cash flow (A + B + C) ($55)

1 WCR12/31/10 – WCR12/31/09 = $6,710 – $4,884 = $1,826

2 Capital expenditures10 = Net fixed assets10 – Net fixed assets09+ Depreciation expenses10