8. Financing strategies.

The managerial balance sheet of the three firms can be directly constructed from the data with

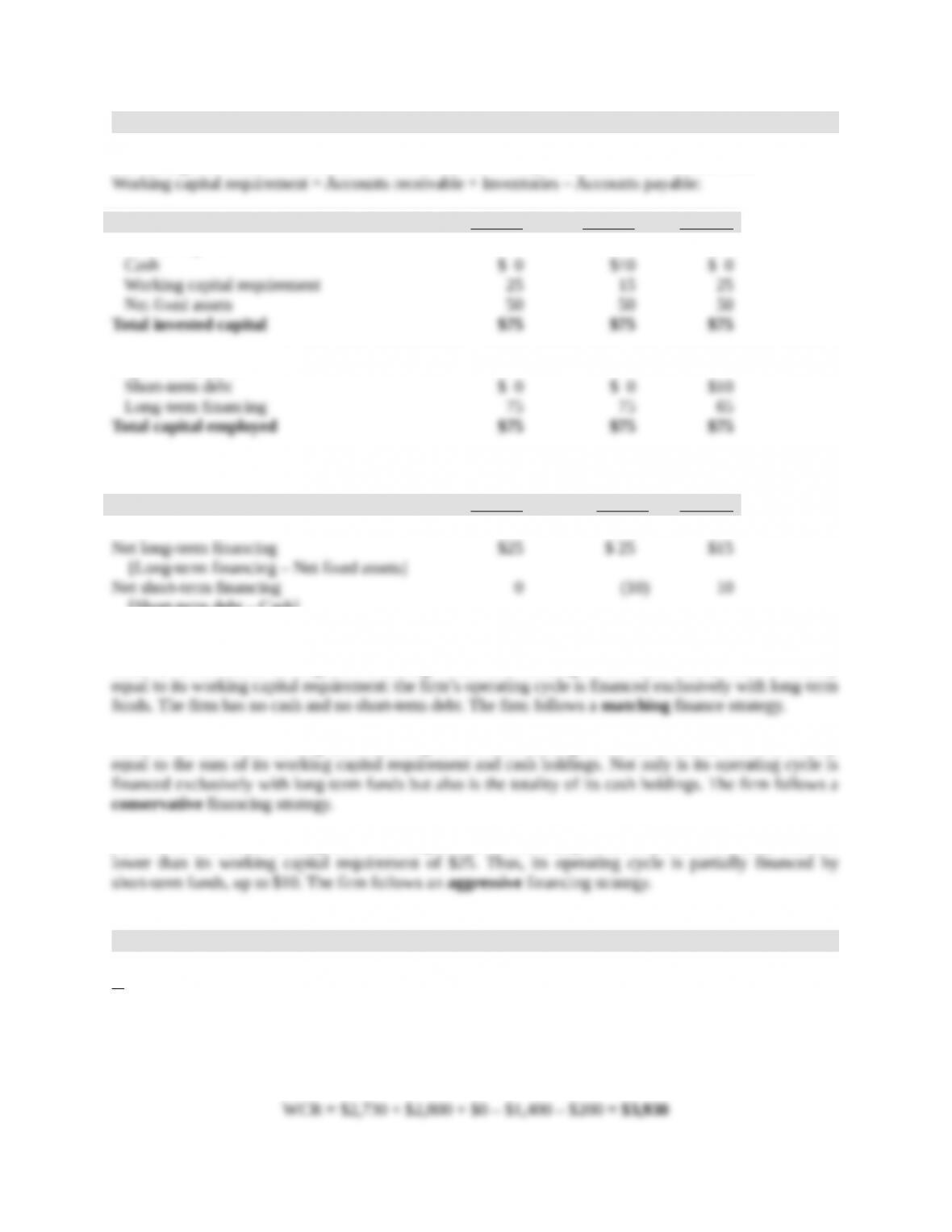

Firm A Firm B Firm C

Invested capital

Capital employed

It follows that:

Firm A Firm B Firm C

[Short-term debt – Cash]

Firm A has an excess of long-term financing of $25 after funding its net fixed assets, which is exactly

Firm B has an excess of long-term financing of $25 after funding its net fixed assets, which is exactly

Firm C has an excess of long-term financing of $15 after funding its net fixed assets of $50, which is

9. The financial effect of the management of the operating cycle.

a.

Working capital requirement (WCR) = Accounts receivable + Inventories + Prepaid expenses

– Accounts payable – Accrued expenses

December 31, 2008:

3-1

December 31, 2009:

December 31, 2010:

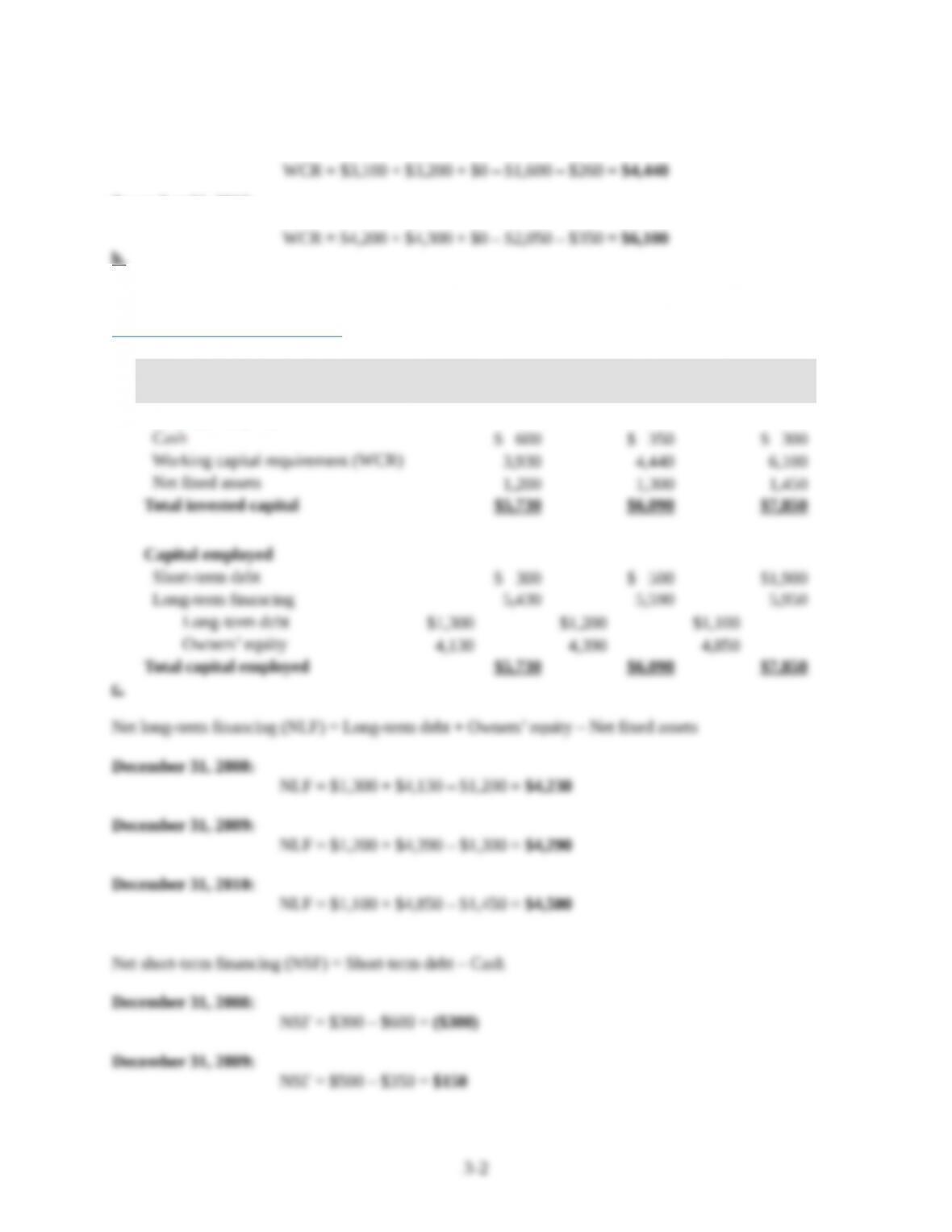

b.

Managerial balance sheets

in thousands December 31,

2008

December 31,

2009

December 31,

2010

Invested capital

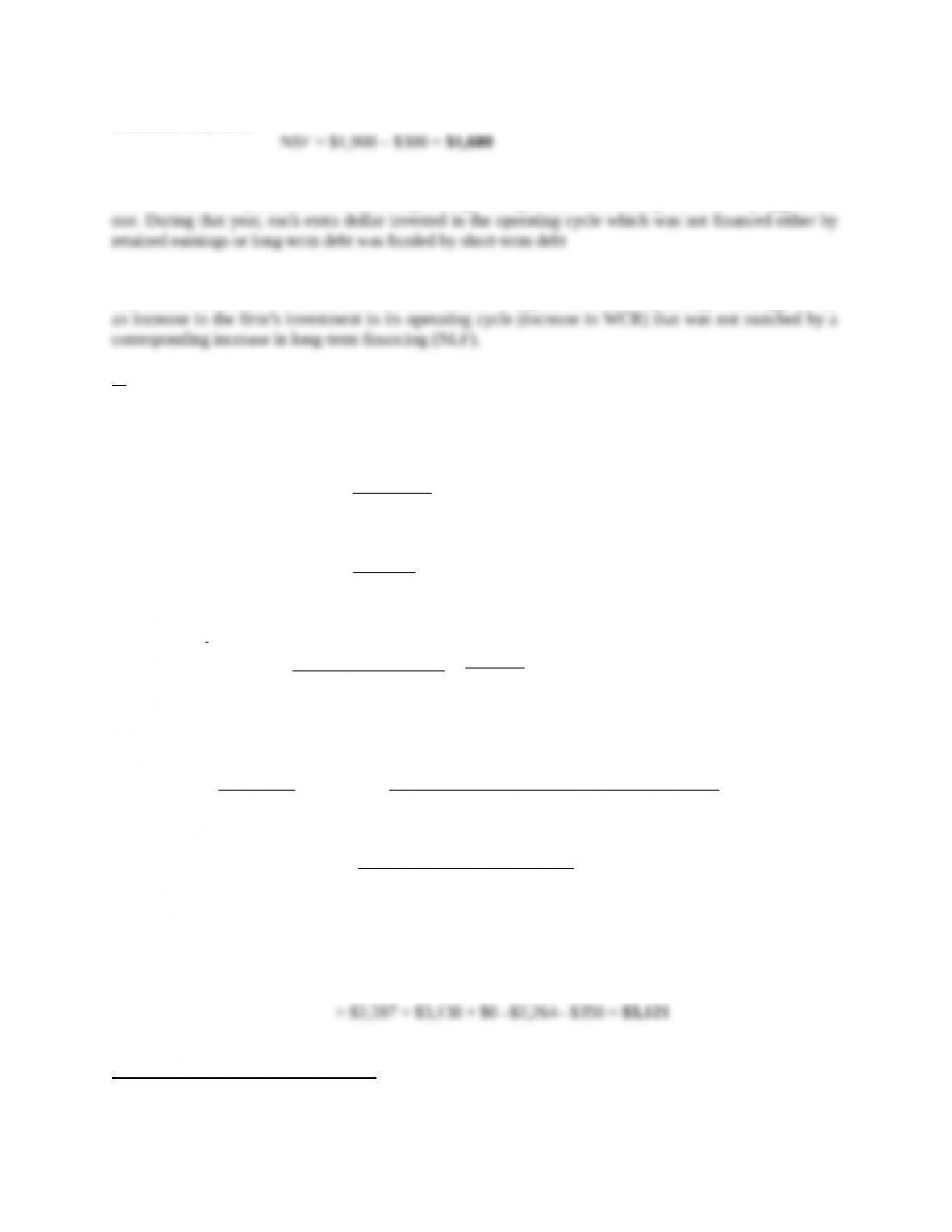

December 31, 2010:

Note that net short-term financing (NSF) went up drastically from December 31, 2008, to December 31,

2010. In the third year, the firm’s financing strategy changed from a matching one to a very aggressive

NSF can increase only if the firm’s net long-term financing (NLF) decreases, and/or its working capital

requirement increases. It is clear from the data that the change in the financing strategy was triggered by

d.

Pro forma working capital requirement (WCR)12/31/10

Accounts receivable12/31/10 =

days30

365

salesNet

$2,597 days30

365

$31,600

Inventory 12/31/10 =

8

soldgoodsofCost

$3,138 8

100,25$

Accounts payable12/31/10 =

days33

365

sinventorieinChangesoldgoodsofCost

days33

365

Purchases

¿$25,100+($3,138−$3,200)

365 ×33 days=$2,264

Working capital requirement = Accounts receivable + Inventories + Prepaid expenses

– Accounts payable – Accrued expenses

Pro forma managerial balance sheet

3-3

in thousands

December 31,

2010

Invested capital

Payment period days =

180/]sinventorieinChangesoldgoodsofCost[

payableAccounts

180/Purchases

payableAccounts

June 30, 2009

Collection period days =

180/655,10$

953,1$

= 33 days (rounded)

Inventories turnover =

986,1$

2940,8$

= 9.0

Payment period = 29 days (given)

December 31, 2009

Collection period days =

180/851,13$

616,2$

= 34 days (rounded)

Inventories turnover =

6942

267111

,$

,$

= 8.7

=

694,2$

671,11$

= 8.7

Payment period

180/)]986,1$694,2($671,11[$

950,1$

180/]708$671,11[$

950,1$

3-5

180/379,12$

950,1$

June 30, 2010

Collection period days =

180/720,11$

100,2$

= 32.3 days (rounded)

Inventories turnover =

085,2$

2834,9$ x

= 9.4

Payment period

180/)]694,2$085,2($834,9[$

650,1$

180/)]609($834,9[$

650,1$

180/225,9$

950,1$

b.

Managerial balance sheet

in thousands

June 30,

2009

December 31,

2009

June 30,

2010

Invested capital

Cash

$ 160

$ 60

$ 70

Working capital requirement (WCR)

((WC(WCR)

2,471

3,288

2,422

Net fixed assets

733

818

830

Total invested capital

$3,364

$4,166

$3,322

Capital employed

Short-term debt

$ 50

$ 880

$ 50

Long-term financing

3,314

3,286

3,272

3-6