Chapter 2

Answers to Review Problems

Finance For Executives – 4th Edition

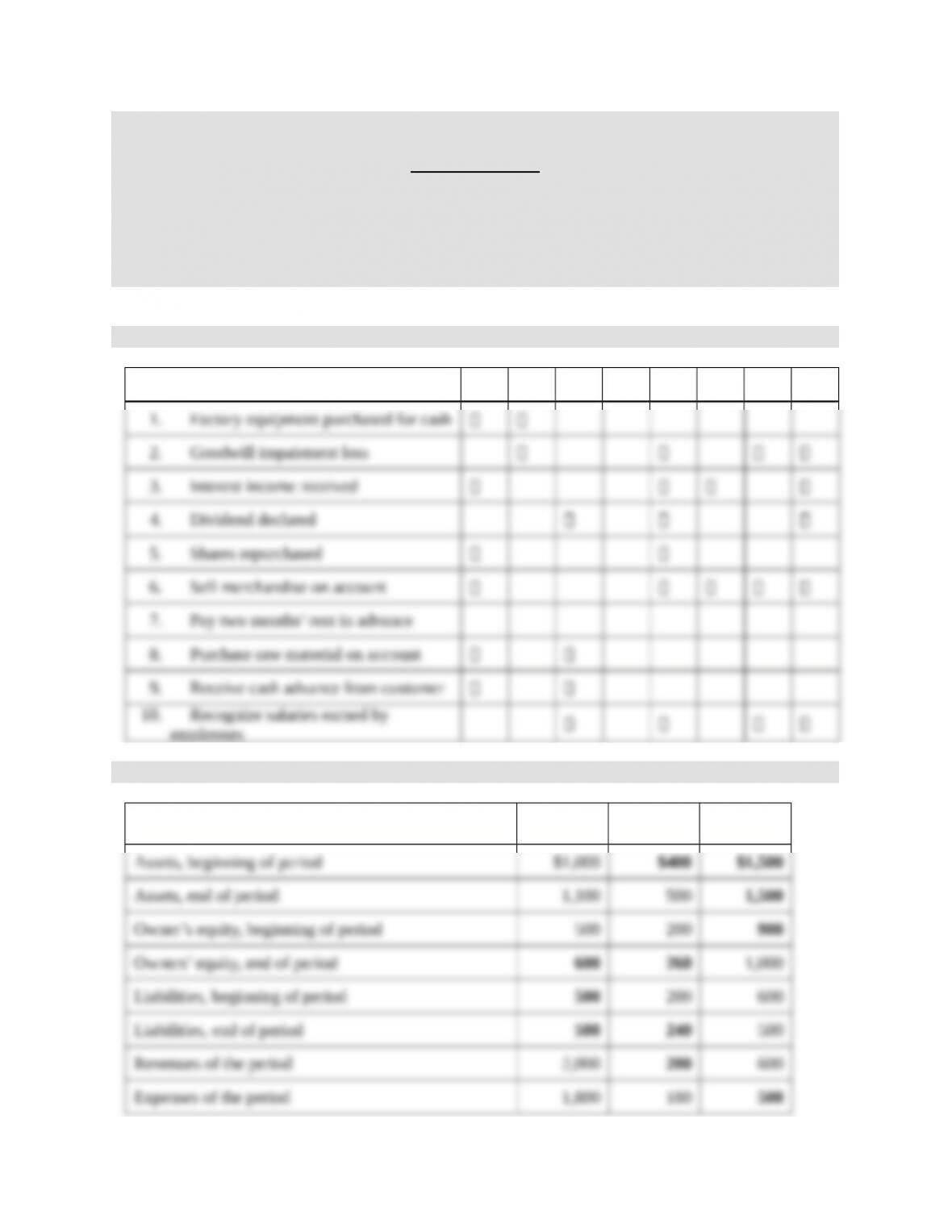

1. Accounting allocation of transactions.

CA NC

ACL NCL OE REV EXP RE

employees

2. Missing accounts.

Firm 1 Firm 2 Firm 3

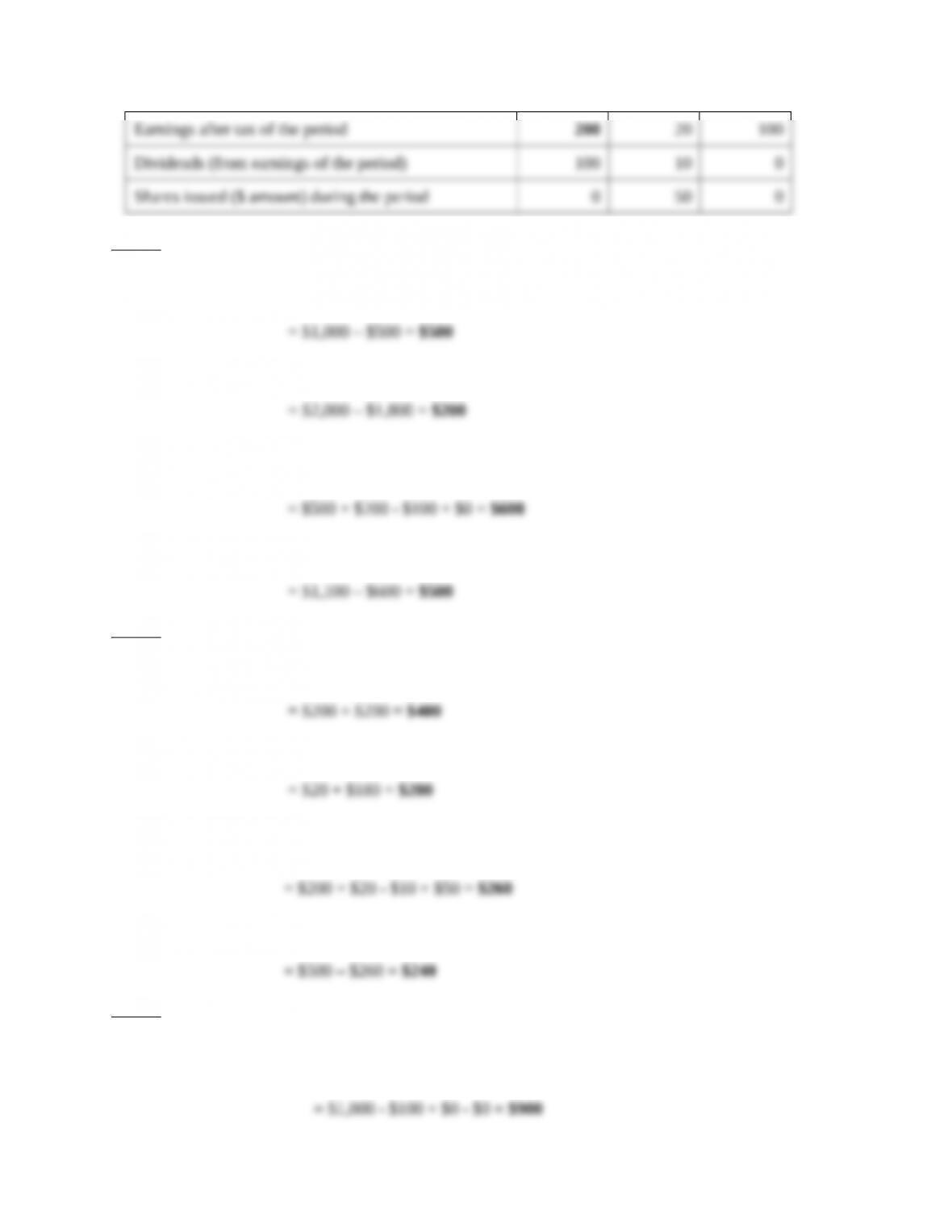

Firm 1

Liabilities beginning of period = Assets beginning of period – Owners’ equity beginning of period

Earnings of the period = Revenues of the period – Expenses of the period

Owners’ equity end of period = Owners’ equity beginning of period + Earnings after tax of the period – Dividends

+ $Amount of shares issued during the period

Liabilities end of period = Assets end of period – Owners’ equityend of period

Firm 2

Assets beginning of period = Liabilities beginning of period + Owners’ equity beginning of period

Revenues of period = Earnings after tax of period + Expenses of period

Owners’ equity end of period = Owners’ equity beginning of period + Earnings after tax of the period – Dividends

+ $Amount of shares issued during the period

Liabilities end of period = Assets end of period – Owners’ equityend of period

Firm 3

Owners’ equity beginning of period = Owners’ equity end of period – Earnings after tax of the period + Dividends

– $Amount of shares issued during the period

Assets beginning of period = Liabilities beginning of period + Owners’ equitybeginning of period

Assets end of period = Liabilities end of period + Owners’ equityend of period

Expenses of the period = Revenues of the period – Earnings after tax of the period

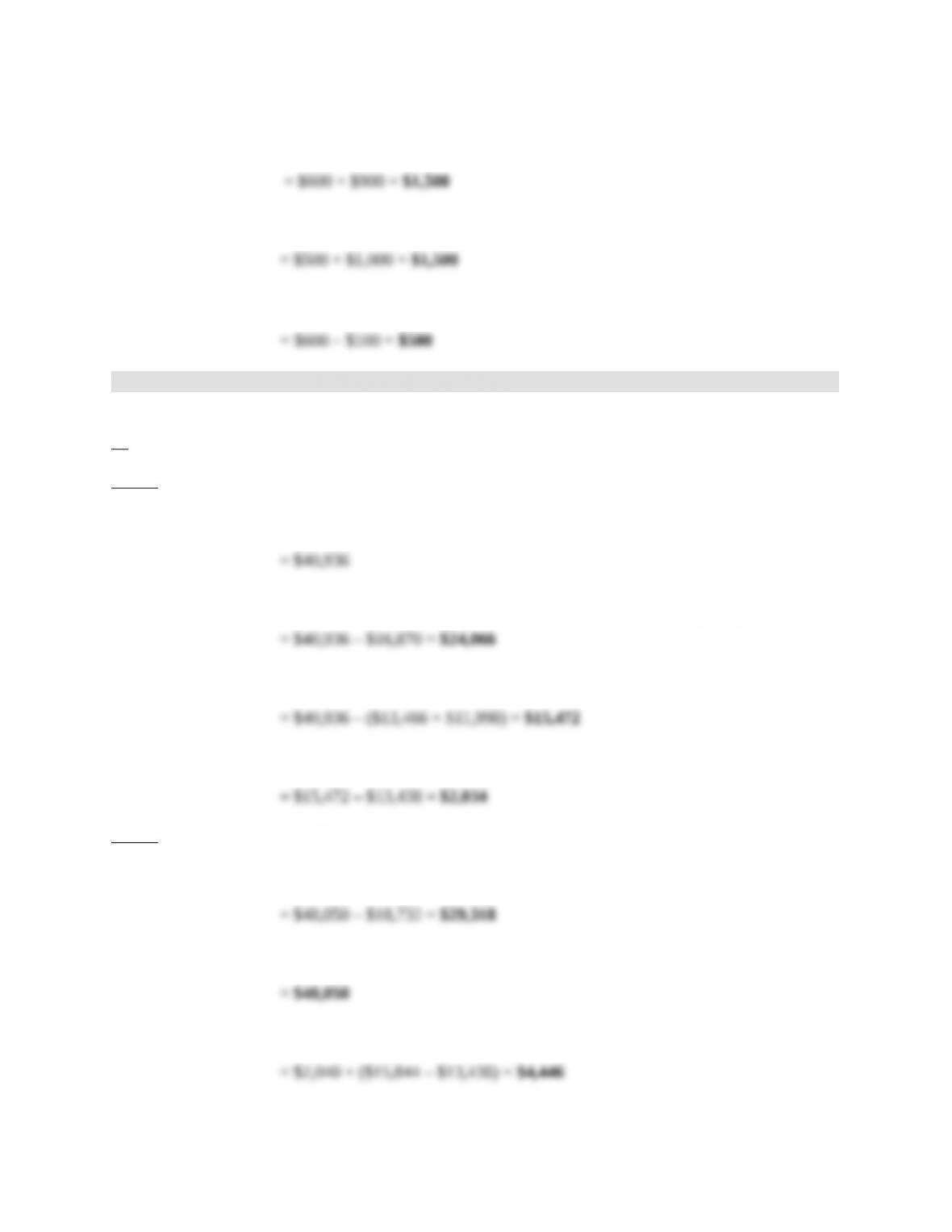

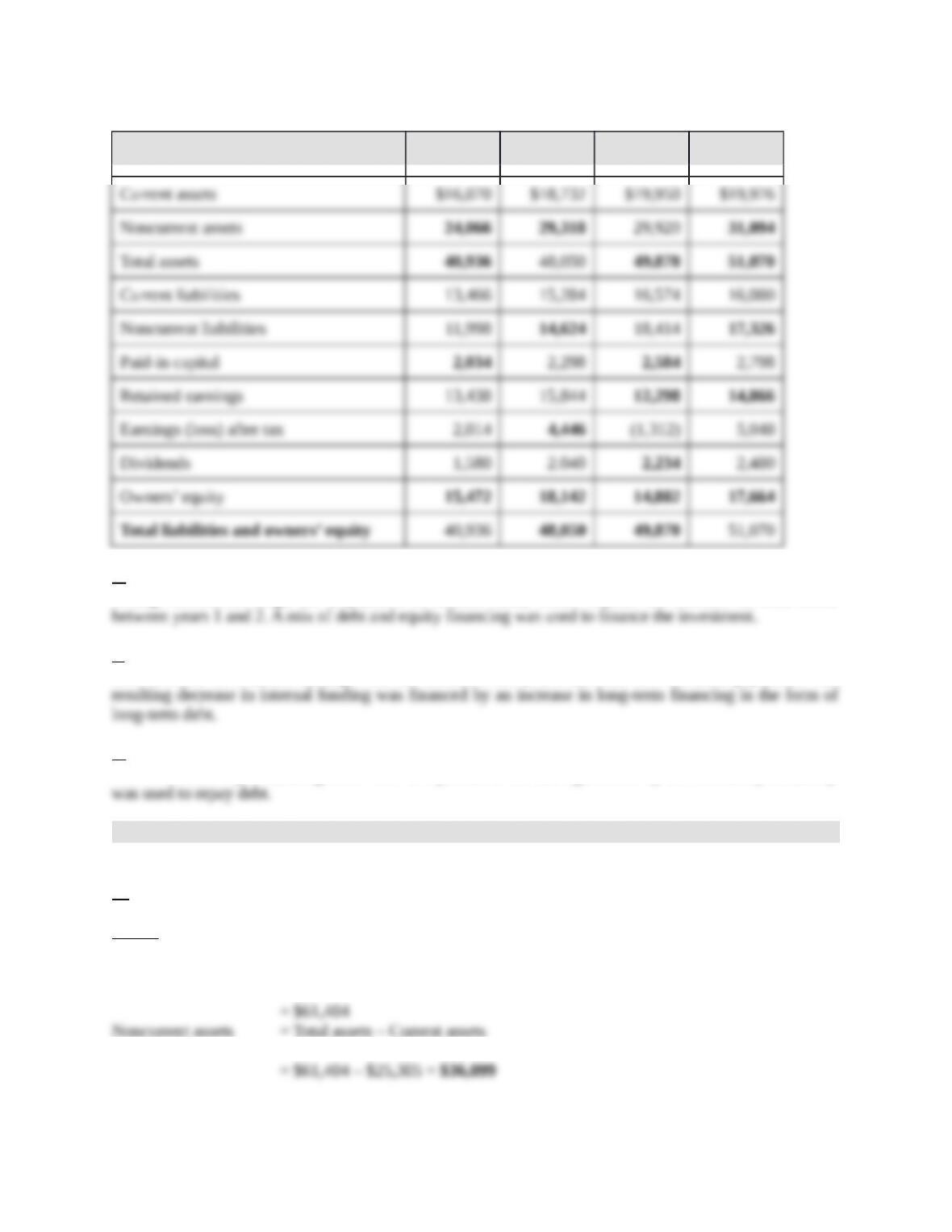

3. Balance sheet changes.

Figures in millions

a.

Year 1

Total assets = Total liabilities and Owners’ equity

Noncurrent assets = Total assets – Current assets

Owners’ equity = Total assets – (Current Liabilities + Noncurrent liabilities)

Paid-in capital = Owners’ equity – Retained earnings

Year 2

Noncurrent assets = Total assets – Current assets

Total liabilities and owners’ equity = Total assets

Earnings after tax = Dividends + (Accumulated earningsyear 2 – Accumulated Earnings year 1)

Owners’ equity = Paid-in capital + Accumulated earnings

Noncurrent liabilities = Total assets – Current liabilities – Owners’ equity

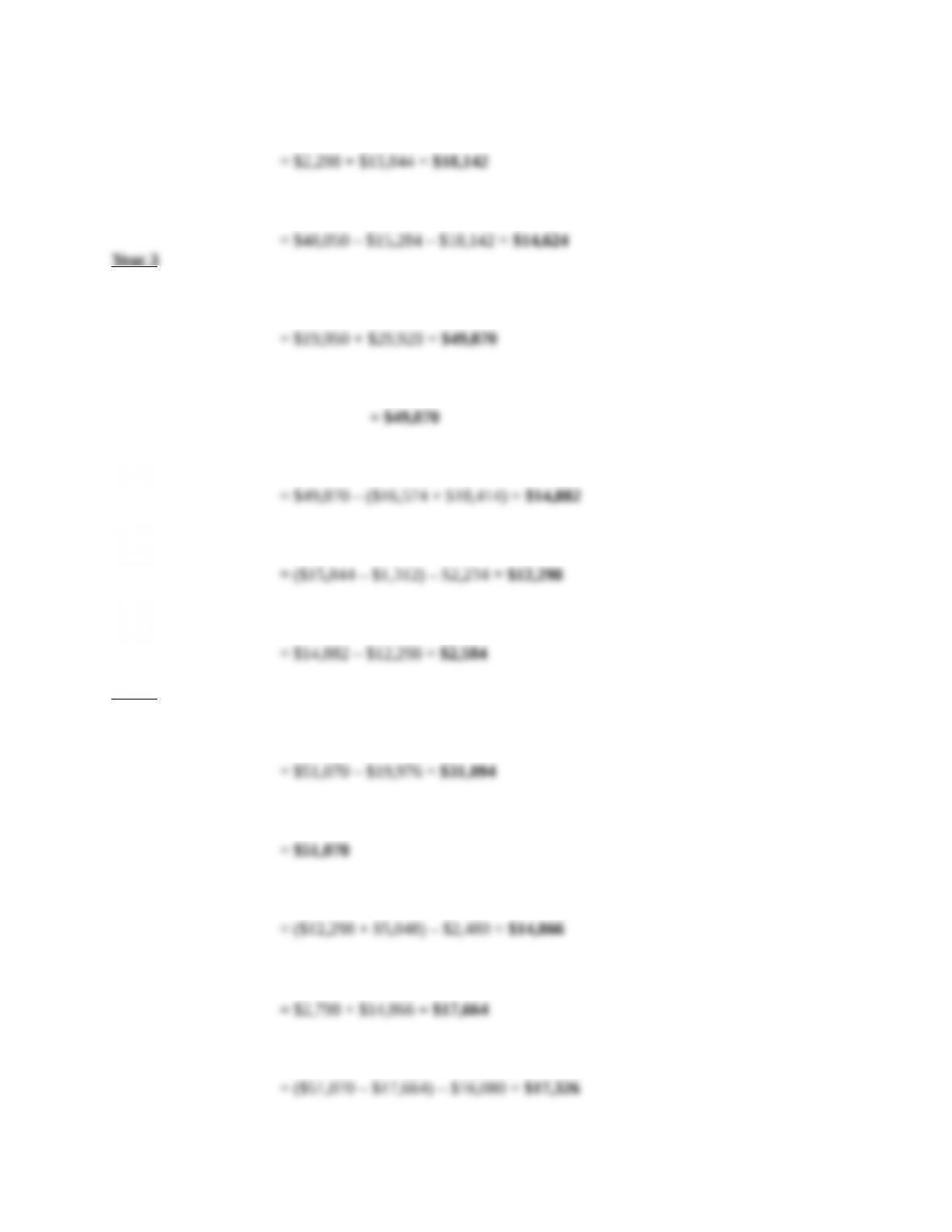

Year 3

Total assets = Current assets + Noncurrent assets

Total liabilities and owners’ equity = Total assets

Owners’ equity = Total assets – (Current Liabilities + Noncurrent liabilities)

Retained earnings year 3 = (Retained earnings year 2+ Earnings (loss) after tax) – Dividends

Paid-in capital = Owners’ equity – Retained earnings

Year 4

Noncurrent assets = Total liabilities and owners’ equity – Current assets

Total assets = Total liabilities and owners’ equity

Retained earnings year 4 = (Retained earnings year 3 + Earnings (loss) after tax) – Dividends

Owners’ equity = Paid-in capital + Retained earnings

Noncurrent liabilities = (Total liabilities and owners’ equity – Owners’ equity) – Current liabilities

End-of-year for balance sheet items Year 1 Year 2 Year 3 Year 4

b.

A large investment (e.g., the acquisition of another firm) would explain the increase in total assets

c.

The decrease in retained earnings was the result of the year’s net loss and dividend payments. The

d.

The firm became profitable again in Year 4. A portion of the cash generated by the renewed profitability

4. Balance sheet changes.

Figures in millions

a.

Year 1

Total assets = Total liabilities and Owners’ equity

Noncurrent assets = Total assets – Current assets

Owners’ equity = Total assets – (Current Liabilities + Noncurrent liabilities)

Paid-in capital = Owners’ equity – Retained earnings

Current assets – current liabilities

Year 2

Current assets = (Current assets – current liabilities) + Current liabilities

Noncurrent assets = Total assets – Current assets

Total liabilities and owners’ equity = Total assets

Owners’ equity = Paid-in capital + Retained earnings

Noncurrent liabilities = (Total assets – Current liabilities) – Owners’ equity

Year 3

Total assets = Current assets + Noncurrent assets

Total liabilities and owners’ equity = Total assets

Owners’ equity = Total assets – (Current liabilities + Noncurrent liabilities)

Retained earnings year 3 = (Retained earnings year 2 + Earnings (loss) after tax) – Dividends

Paid-in capital = Owners’ equity – Retained earnings

Current assets – current liabilities

Year 4

Total assets = Total liabilities and owners’ equity

Noncurrent assets = Total assets – Current assets

Current liabilities = Current assets – (Current assets – current liabilities)

Retained earnings year 4 = (Retained earningsyear 3 + Earnings (loss) after tax) – Dividends

Owners’ equity = Paid-in capital + Retained earnings

Noncurrent liabilities = (Total assets – Current liabilities) – Owners’ equity

End-of-year for balance sheet items Year 1 Year 2 Year 3 Year 4

b.

A large investment (e.g., the acquisition of another firm) would explain the increase in total assets