Chapter 15

Answers to Review Problems

Finance For Executives – 4th Edition

1. Understanding market value added and economic value added.

a.

The firm with the highest market value added, which is not necessarily the one with the highest market

b.

Positive MVA means that the present value of the future stream of EVAs is positive. This does not

c.

d.

e.

Higher ROIC is only half the story. ROIC must exceed the WACC in order to create value. A business will

2. Value drivers.

Drivers related to the management of operations

Strategic value drivers

EVA

CHARGE FOR CAPITAL EMPLOYED

SALES GROWTH

AFTER-TAX OPERATING MARGIN

minus

OPERATING MARGIN

EFFECTIVE TAX RATE

SELF-SUSTAINABLE GROWTH RATE

ABILITY TO RAISE EQUITY

WEIGHTED AVERAGE COST OF CAPITAL

CASH

NET FIXED ASSETS

AFTER-TAX COST OF DEBT

COST OF EQUITY

4. Financial structure.

a.

Invested capital

$ millions

December 31,

2009

December 31,

2010

1 Working capital requirement = Accounts receivable + Inventories + Prepaid expenses – Accounts

payable – Accrued expenses

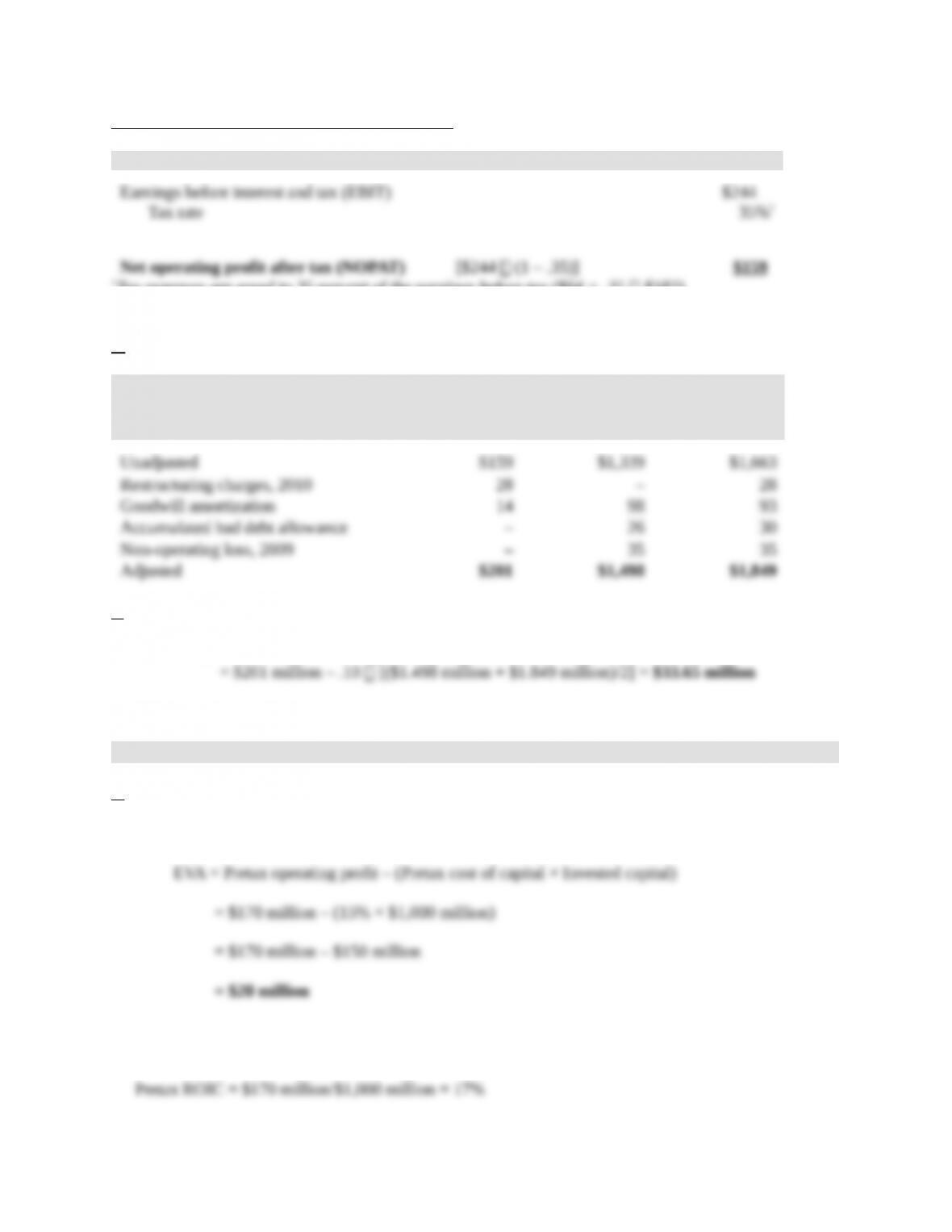

Net operating profit after tax (NOPAT) in 2010

$ millions 2010

1Tax expenses are equal to 35 percent of the earnings before tax ($64 = .35 $182).

b.

Invested Capital

$ millions NOPAT

December 31,

2009

December 31,

2010

c.

EVA10 = NOPAT10 – WACC Average adjusted invested capital10

4. Economic value added analysis.

a.

Pretax economic value added (EVA) based on initial invested capital:

Pretax economic value added (EVA) based on expected return on invested capital (ROIC):

EVA = (Pretax ROIC – Pretax cost of capital) × Invested capital

b.

1. Reducing operating expenses by $10 million would raise EVA by $10 million:

2. Reducing invested capital by $60 million would raise EVA by $9 million:

3. Lowering pretax cost of capital to 14 percent would raise EVA by $10 million:

4. Selling assets (at book value) for $100 million will reduce capital employed to $900 million

and cut pretax operating profit by $10 million, thus raising EVA by $5 million (note that these

5. Buying assets for $100 million will raise capital employed to $1,100 million and add $20

million in pretax operating profit, thus raising EVA by $5 million (note that these assets have

an expected ROIC of 20% which is higher than the WACC of 15%):

5. The relationship between a firm’s market value, its market value added, and its

economic value added.

a.

Equation 15.1 defines market value added (MVA) as the difference between the market value of capital

and the amount of capital employed, which is also equal to the amount of invested capital. Thus,:

Since MVA is also equal to the present value of the firm’s expected future economic value added (EVA),

we can write:

or

b.

We show in the chapter that the present value of a project’s expected future EVAs is equal to (1) the

change in the firm’s MVA if the project is undertaken and (2) the net present value of a project. In Chapter

6, we showed that the net present value of a project is equal to the change in the market value of the

firm’s equity after the project is announced. Thus, to get the change in the firm’s MVA and market value

following the adoption of the project, we just have to compute the present value of the expected future

EVAs of the project.

From equation 15.6 and the data given in the question, we can write:

Project EVA = (Return on invested capital – Weighted average cost of capital) Invested capital

Discounting these $3 million for 4 years at a cost of capital of 8 percent, we get:

PV of future expected EVAs

432

.08)(1

million$3

.08)(1

million$3

.08)(1

million$3

.081

million$3

Following the announcement of the project, we should expect that the market value of Value Inc. and its

6. The effect of the management of the operating cycle on the firm’s economic value added.

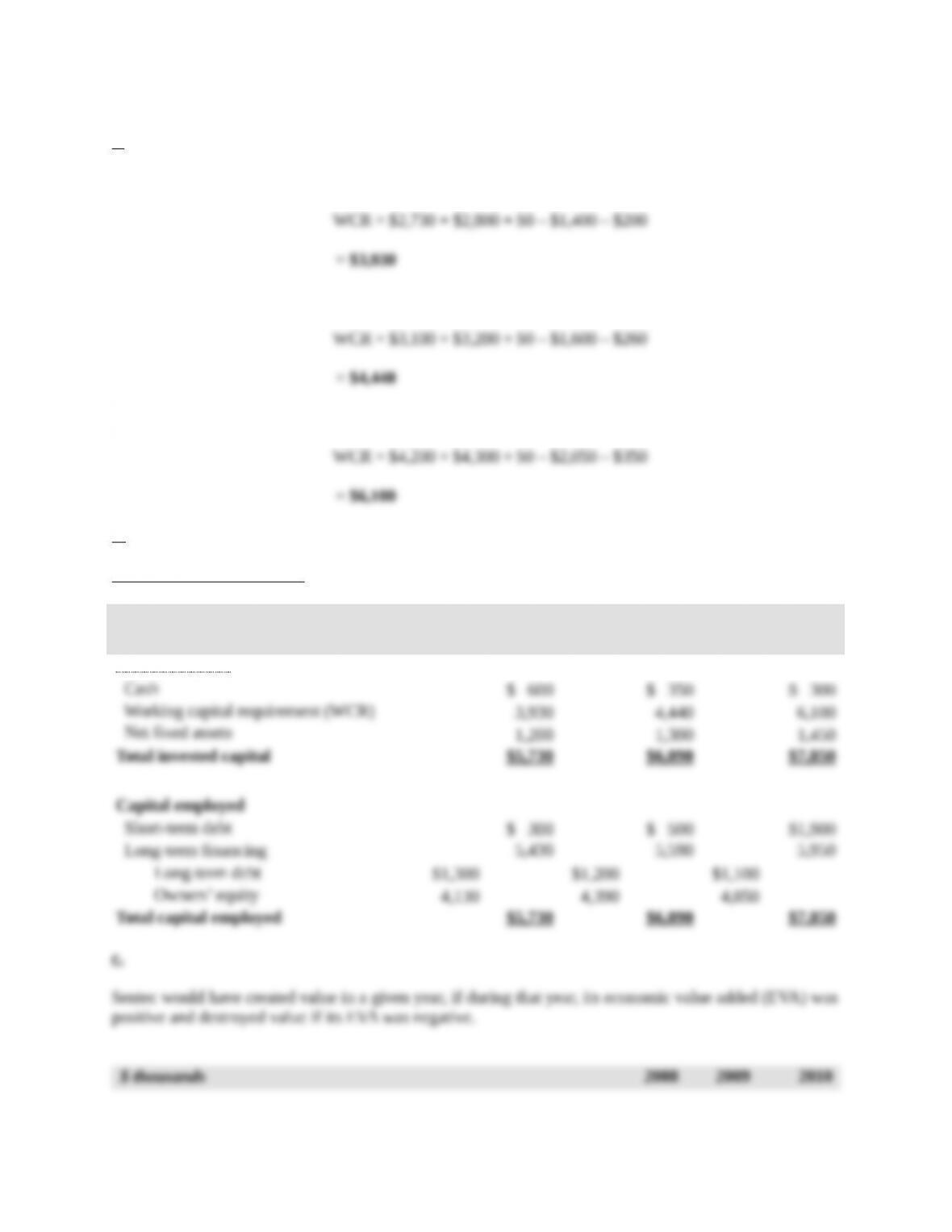

Working capital requirement (WCR) = Accounts receivable + Inventories + Prepaid expenses

a.

December 31, 2008:

December 31, 2009

December 31, 2010

b.

Managerial balance sheets

$ thousands

December 31,

2008

December 31,

2009

December 31,

2010

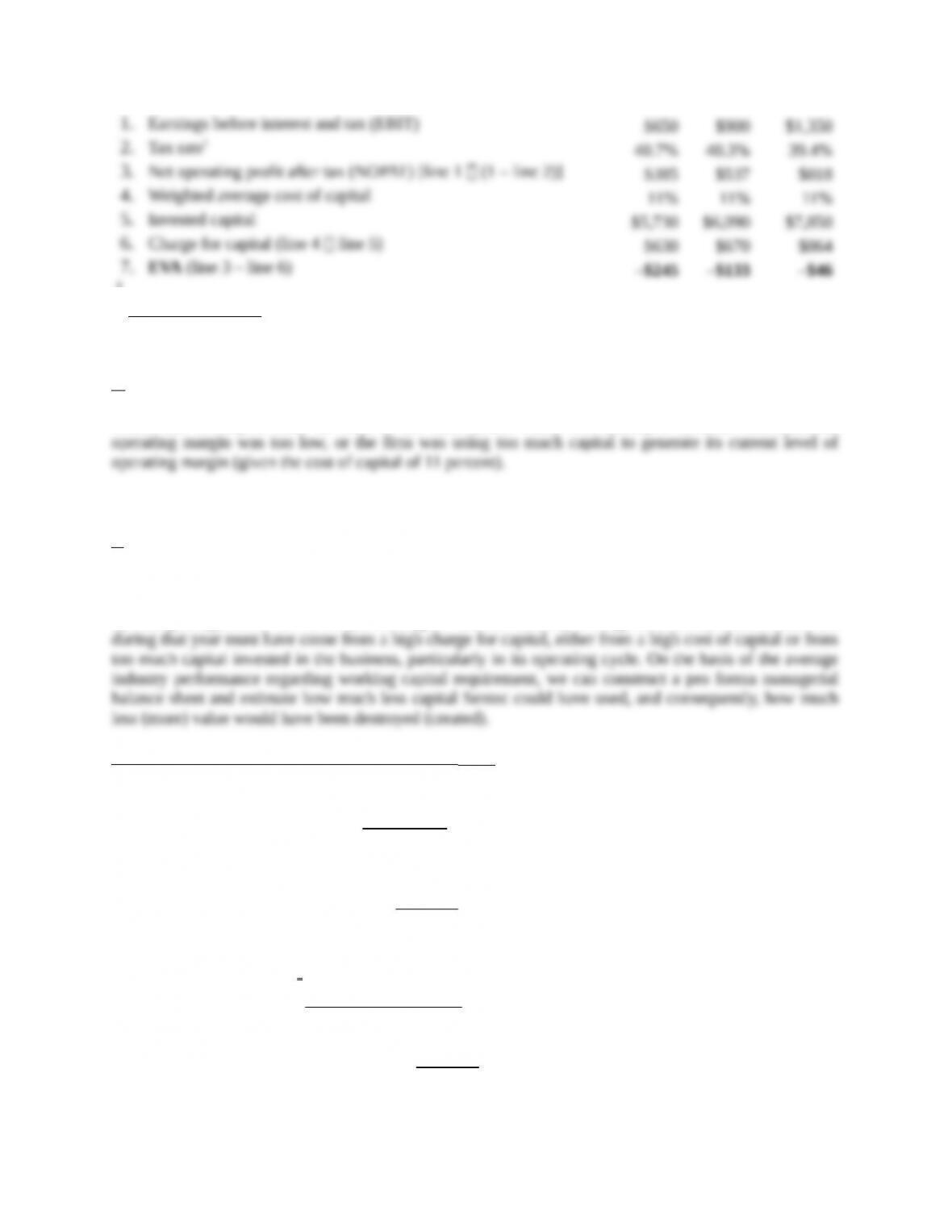

Invested capital

1

taxbeforeEarnings

ensesexptaxIncome

d.

Sentec has destroyed value in each of the three years. Value was destroyed because either/and the

The next question is intended to identify which of the two caused value destruction.

e.

In 2010, Sentec’s operating margin was equal to 4.3 percent ($1,350/$31,600), compared to 3.3 percent

for the industry as a whole. If Sentec destroyed value in 2010, it was certainly not due to an insufficient

operating margin since it was 30 percent higher than the industry average. Therefore, value destruction

Pro forma working capital requirement (WCR) 12/31/10

Accounts receivable12/31/10 =

days30

365

salesNet

10

$2,597days30

365

$31,600

Inventory 12/31/10 =

8

soldgoodsofCost

10

$3,138

8

$25,100

Accounts payable12/31/10 =

days

sinventorieinChangesoldgoodsofCost

days

Purchases 33

365

33

365

101010

=

$2,264days33

365

$3,200)($3,138$25,100

Working capital requirement = Accounts receivable + Inventories + Prepaid expenses – Accounts payable

– Accrued expenses

Pro forma net fixed assets

Same as before= $1,450

Pro forma long-term financing = pro forma owners’ equity + pro forma long-term debt

Same as before =$5,950

Pro forma short-term debt

Note that the amount of long-term financing ($5,950) would have been higher than the investment in

Pro forma managerial balance sheet

$ thousands

December 31,

2010

Invested capital

If Sentec had managed its operating cycle like the average firm in the industry in year 2010, its invested

capital would have been equal to $5.950 million instead of $7.850 million. As a result, its economic value

added would have been positive and equal to $164 million, as shown in the following table:

$ thousands

Pro forma

2010

1

taxbeforeEarnings

ensesexptaxIncome

Note that a better management of the operating cycle in 2010 would have created $164,000 of value